UK Employment

About

-

August 18th, 2026 · 2:00 AM

-

September 15th, 2026 · 2:00 AM

-

October 20th, 2026 · 2:00 AM

-

November 17th, 2026 · 2:00 AM

-

December 15th, 2026 · 2:00 AM

Latest Releases

12

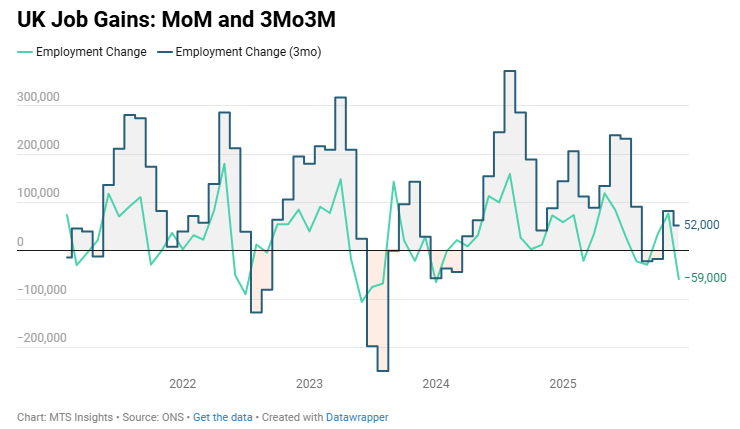

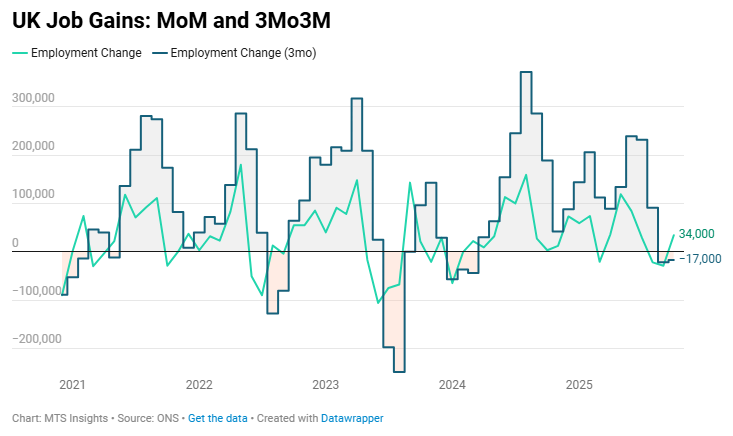

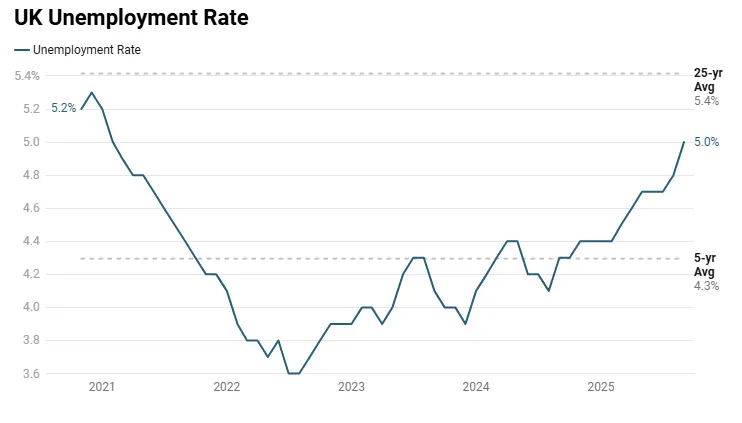

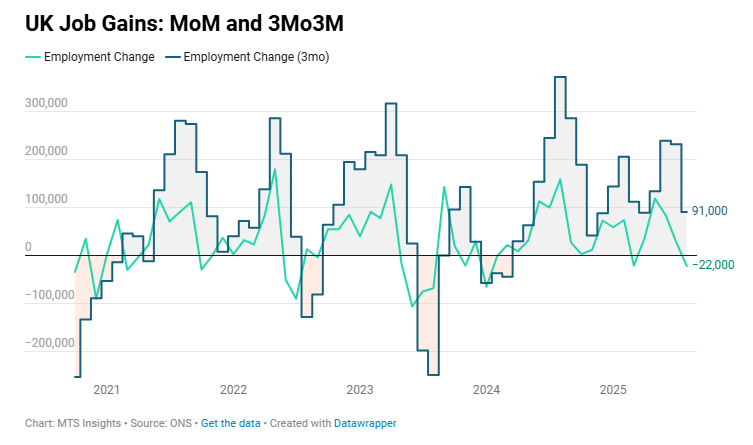

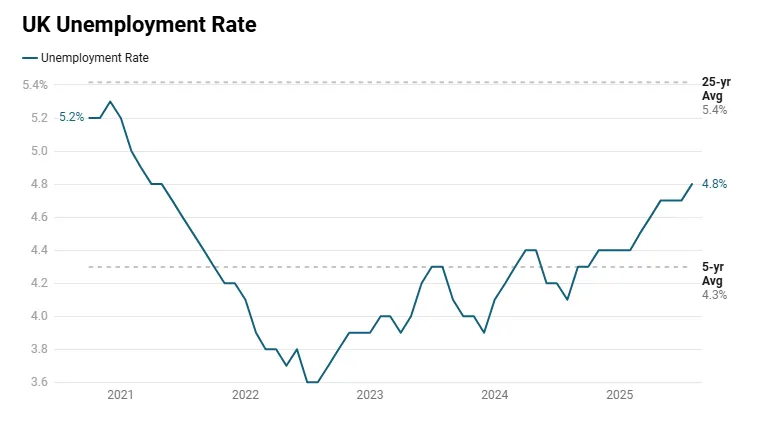

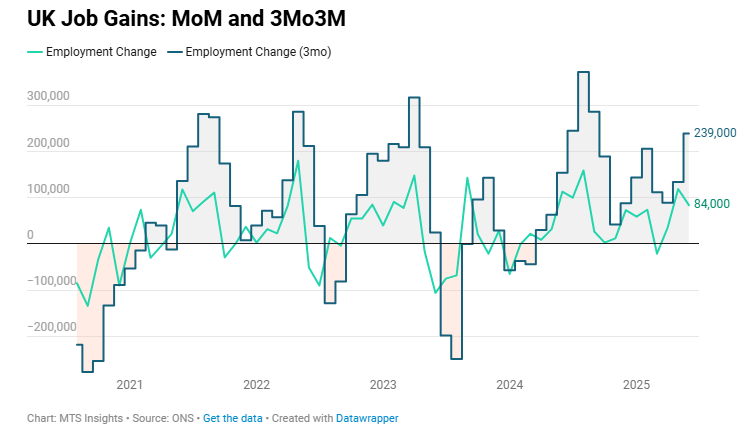

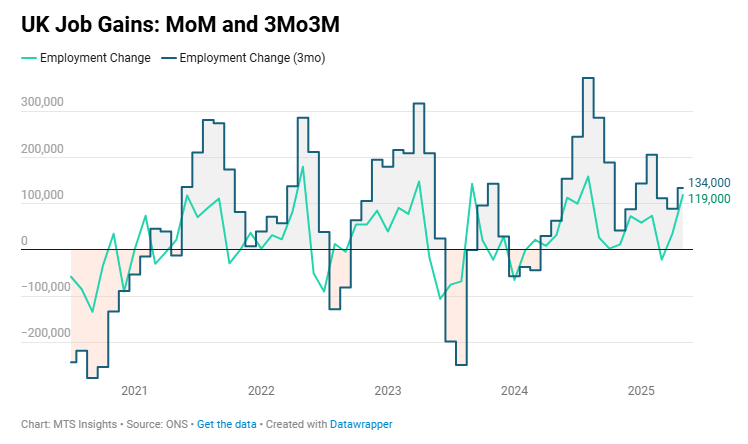

UK employment increased by 52k in the three months to December, with employment dropping -59k in December alone.

- The overall employment rate edged down -0.1 ppt to 75.0% in December, unchanged from a year ago.

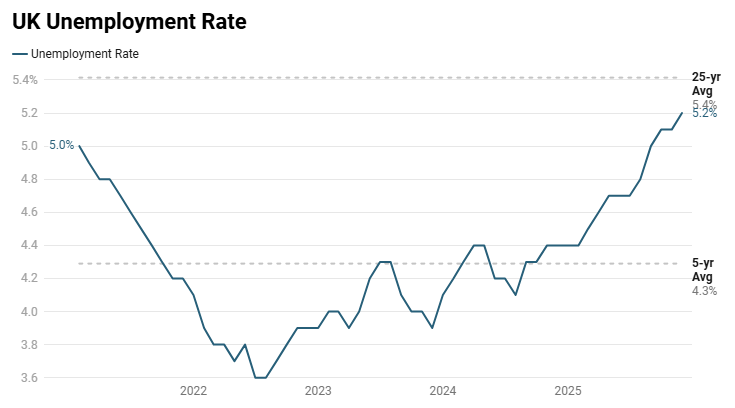

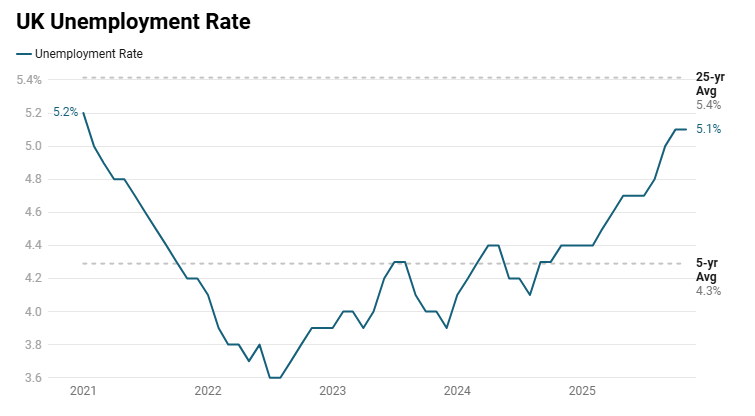

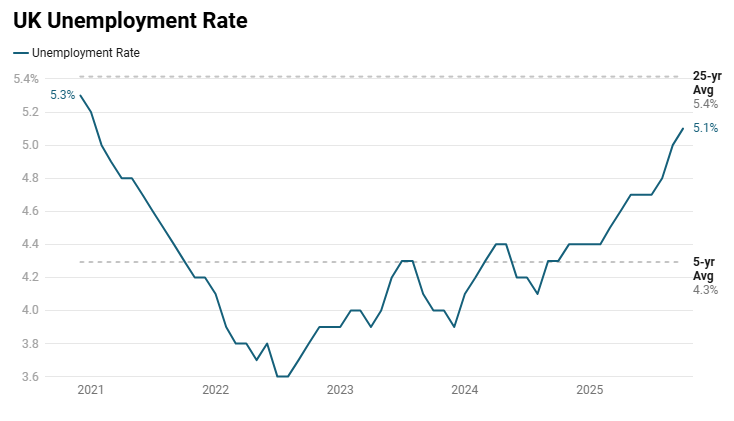

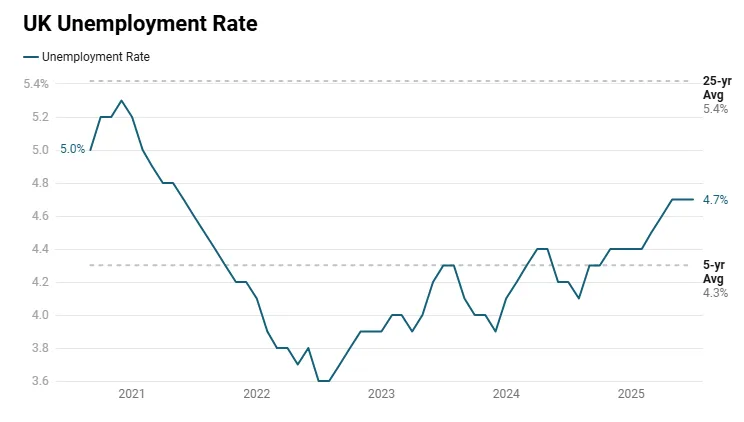

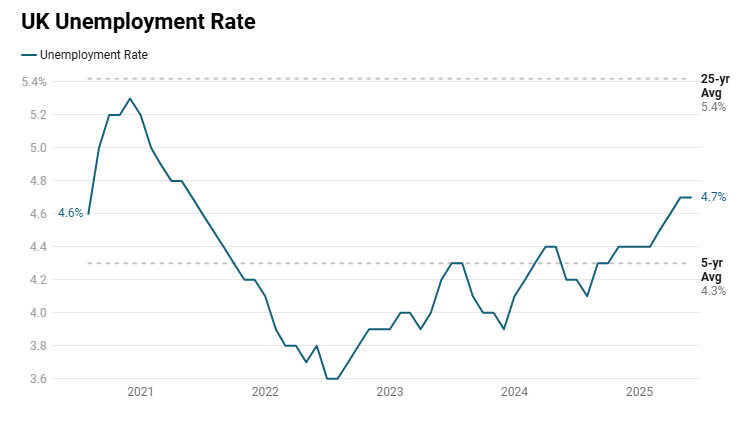

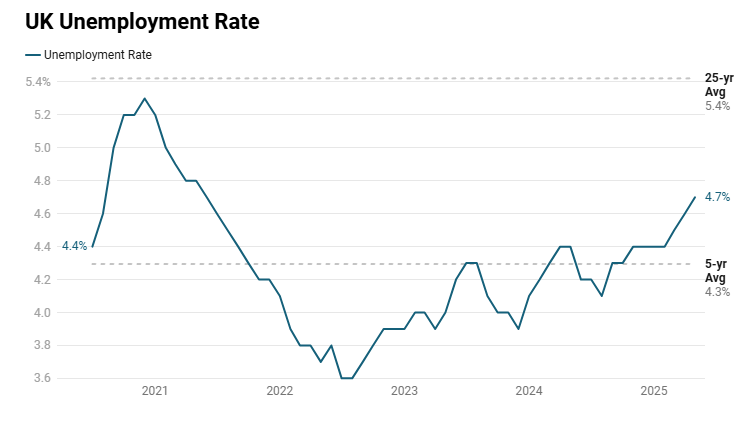

- The unemployment rate increased 0.1 ppt to 5.2% (vs 5.1% expected) in December, the highest since February 2021 and a 0.8 ppt increase from a year ago.

- The overall unemployment level has increased by 94k in the last three months and is up 331k in the last year.

- The economic inactivity rate remained at 20.8% and is down -0.7 ppts YoY.

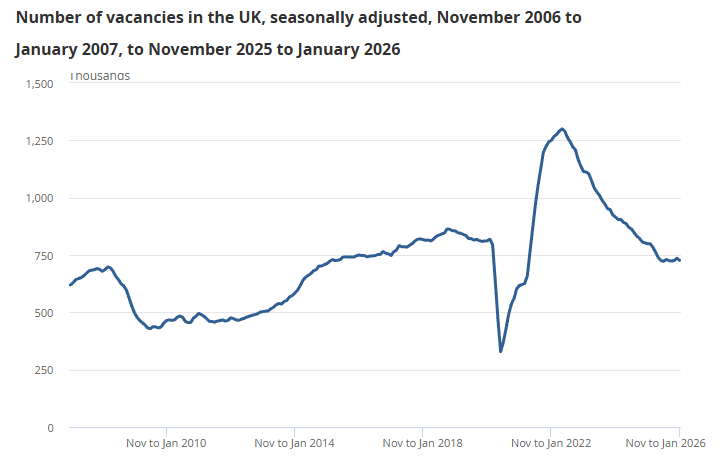

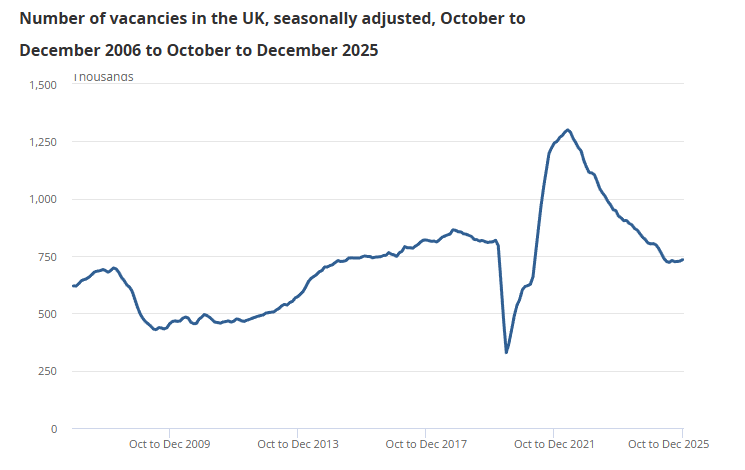

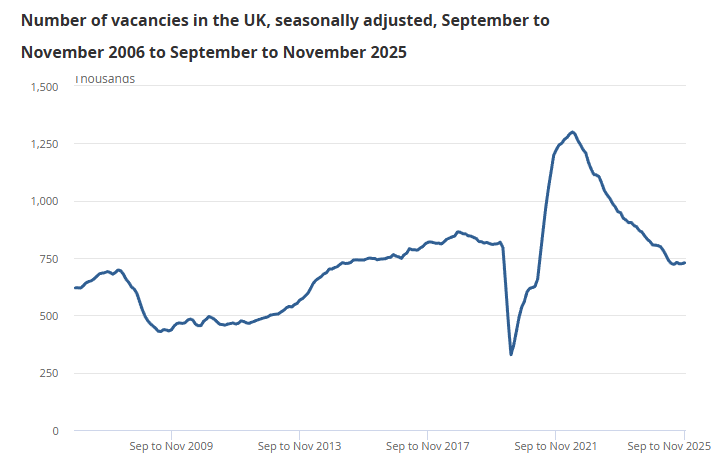

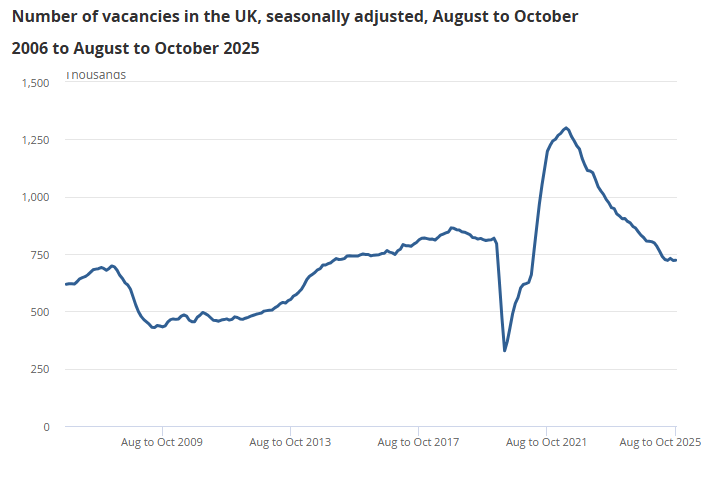

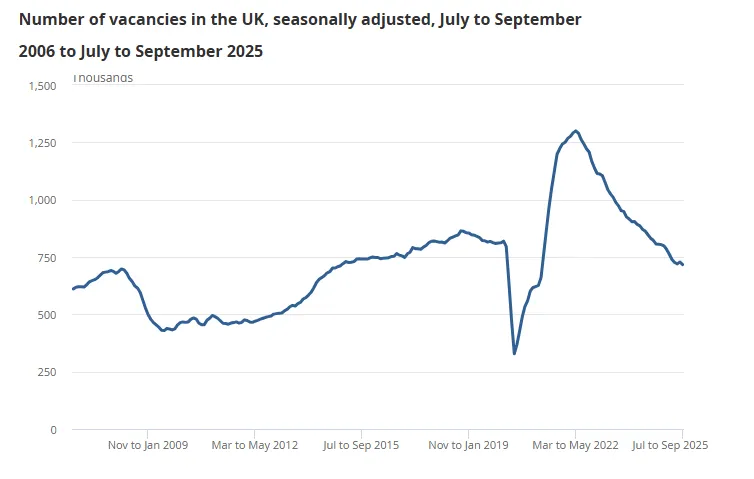

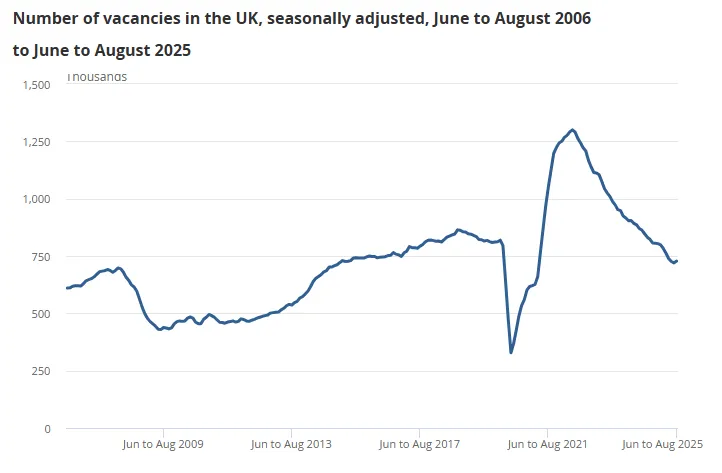

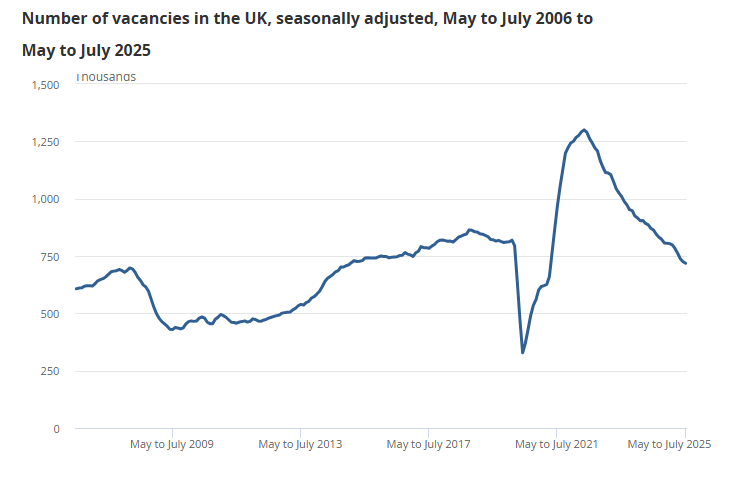

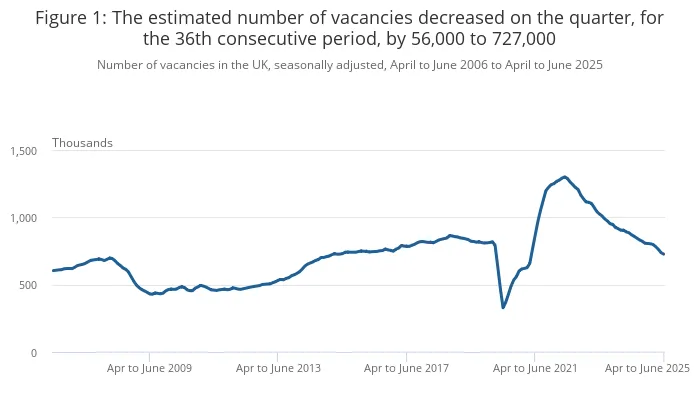

UK vacancies rose +0.3% QoQ to 726k but were still down -9.2% YoY, signaling stabilization after a prolonged decline.

-

Vacancies increased by +2k QoQ (Aug–Oct vs Nov–Jan) but remained broadly flat and within the ±32k confidence interval, indicating little meaningful short-term change.

-

Compared with a year earlier, vacancies declined -73k (-9.2%) and sit -69k (-8.7%) below pre-pandemic Jan–Mar 2020 levels, showing hiring demand remains structurally lower.

-

Labour market tightness eased, with 2.6 unemployed persons per vacancy (vs 2.5 prior quarter; 1.9 YoY), the highest non-pandemic level since Nov 2014–Jan 2015.

-

Quarterly increases occurred in 7 of 18 sectors, led by arts & recreation (+12.3%), while manufacturing and transport/storage posted the largest volume gains (+4k each), reflecting limited sectoral improvement.

-

YoY declines were broad-based across 14 of 18 sectors, steepest in construction (-32.4%) and mining & quarrying (-26.7%), indicating ongoing cooling across cyclical industries.

-

Larger firms drove quarterly gains, with businesses employing 2,500+ workers up +8k (+3.5%) QoQ, while small firms (1–49 employees) recorded the largest annual declines (-18k each), showing weaker small-business hiring.

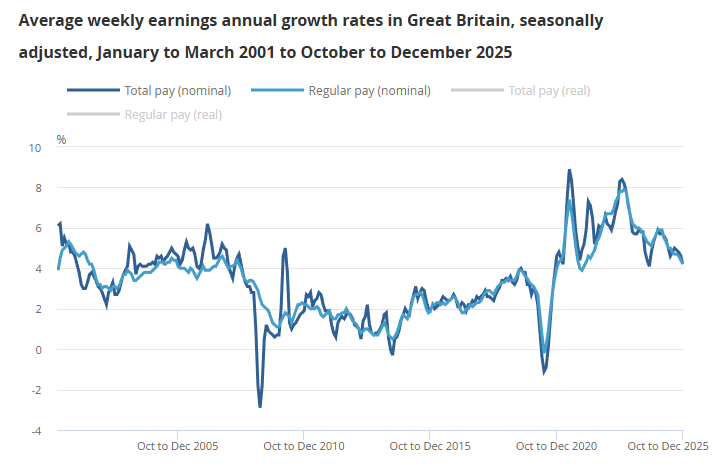

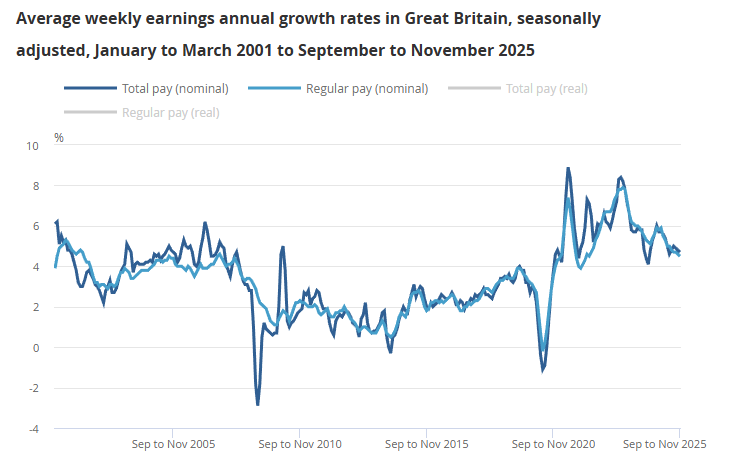

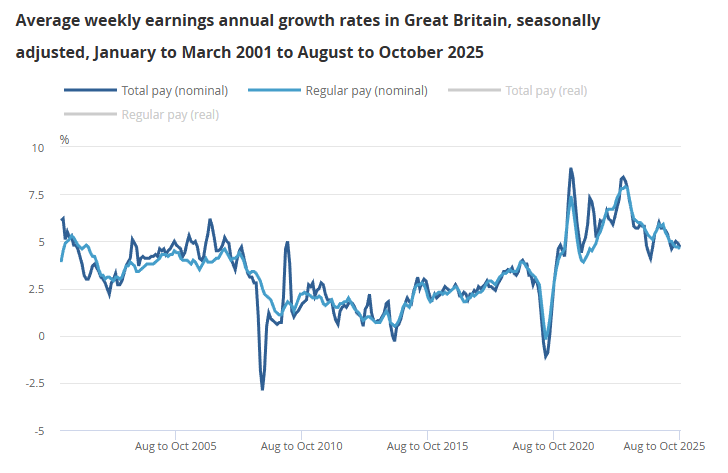

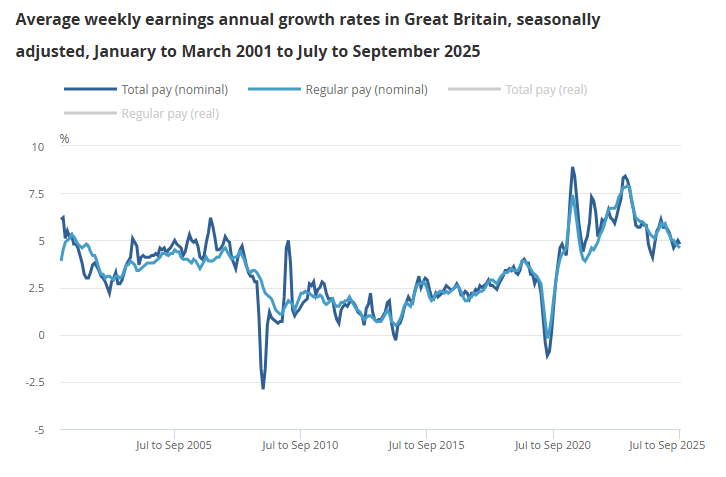

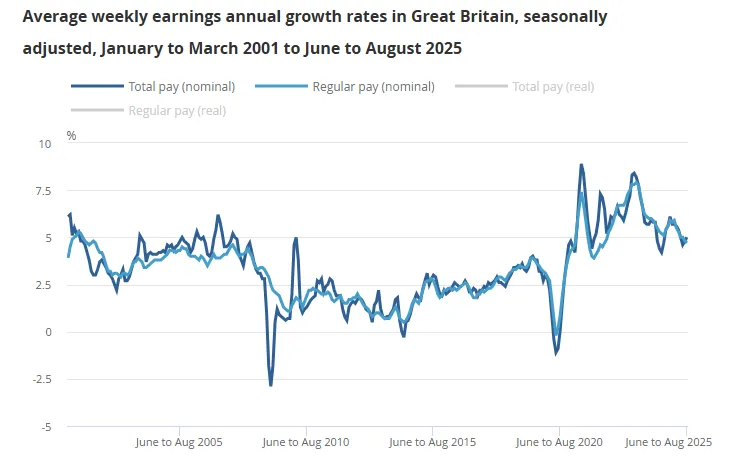

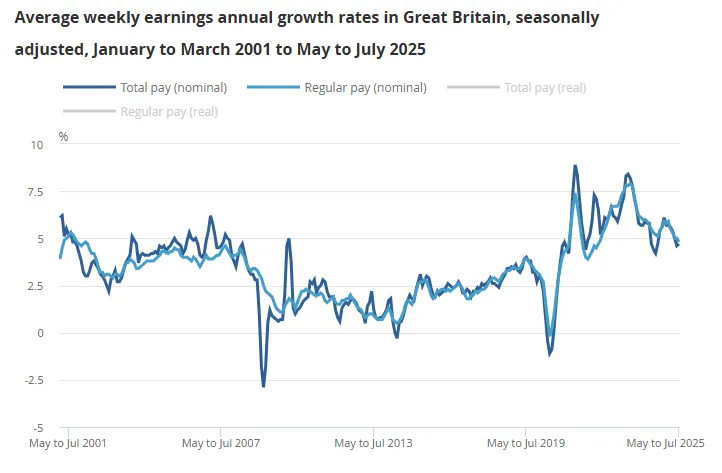

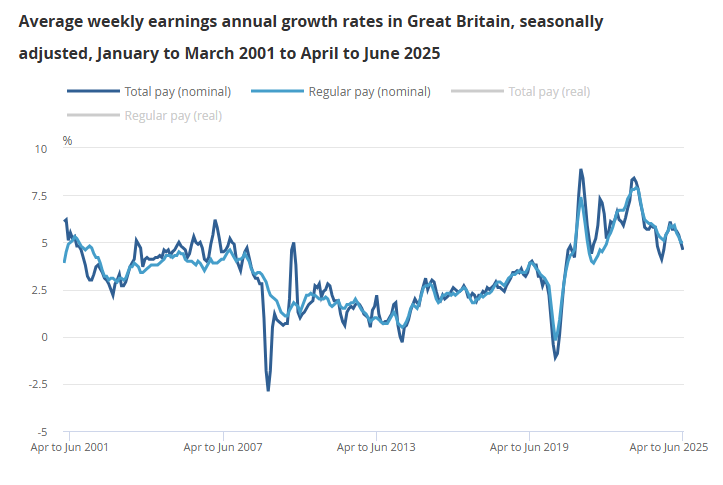

UK average weekly earnings (including bonuses) grew +4.2% YoY in Oct–Dec 2025, easing from +4.6% YoY in Sep-Nov 2025 to the lowest growth since August 2021.

-

UK regular pay (average weekly earnings excluding bonuses) was up +4.2% YoY in December, down from +4.4% YoY in November and the lowest since January 2022.

-

Real earnings rose +0.5% YoY using CPIH for both regular and total pay, indicating modest positive real wage gains after inflation adjustment.

-

Using CPI, real regular pay increased +0.8% YoY and real total pay +0.7% YoY, slightly stronger than CPIH-adjusted measures but still subdued.

-

Public sector regular earnings rose +7.2% YoY (total +7.0%), boosted by timing-related base effects from earlier 2025 pay settlements that will fade soon.

-

Private sector regular earnings grew +3.4% YoY and total pay +3.5% YoY, down from prior periods and the weakest pace since 2020, reflecting ongoing cooling.

-

Nominal wage growth has slowed over the past year, with 4.2% the lowest since late 2021–early 2022 for regular pay and mid-2024 for total pay.

-

Sector dispersion remained, with wholesaling/retailing/hotels/restaurants strongest at +5.1% YoY while finance & business services lagged at +2.0% YoY.

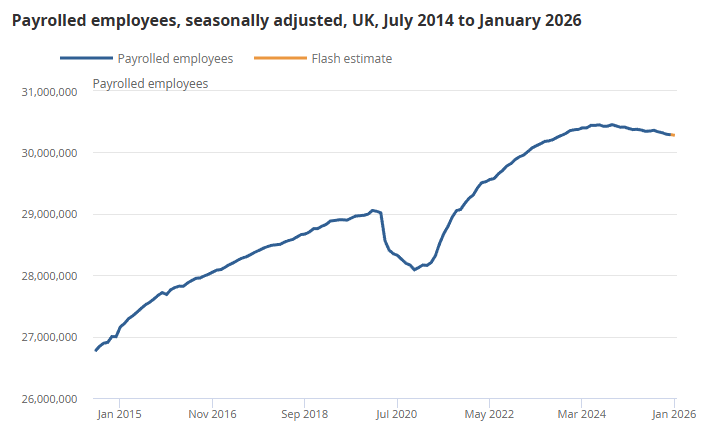

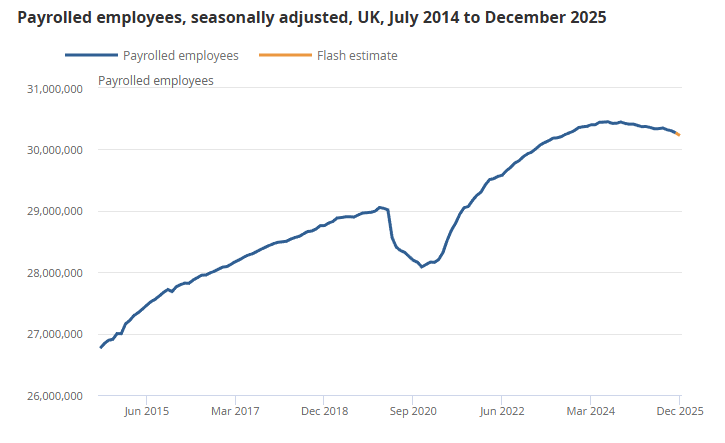

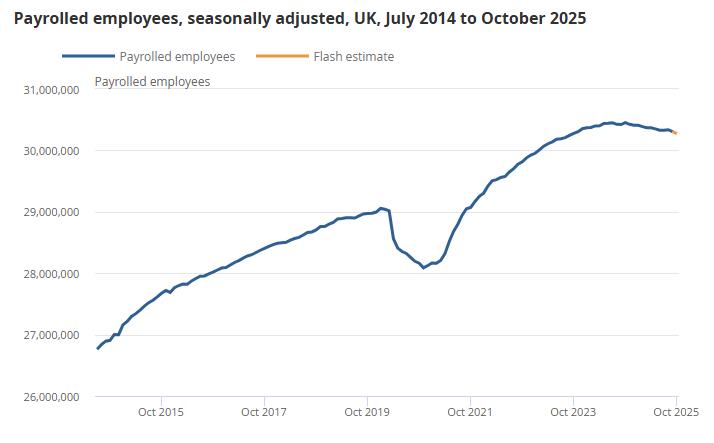

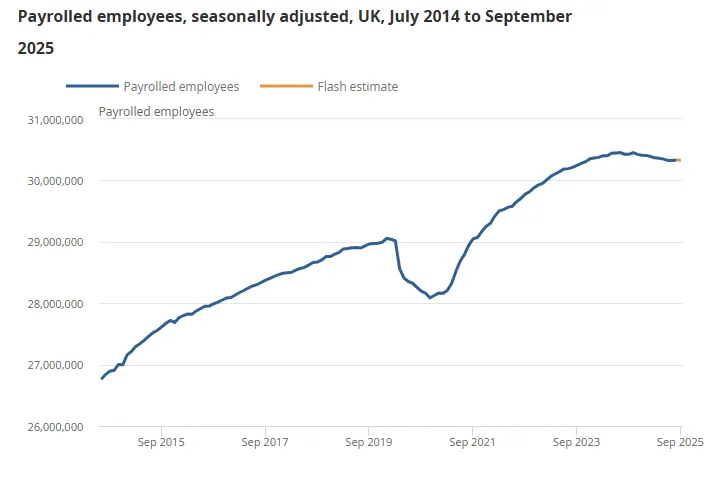

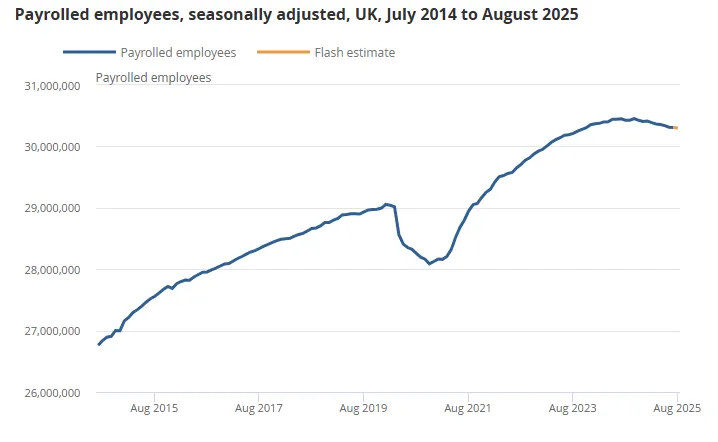

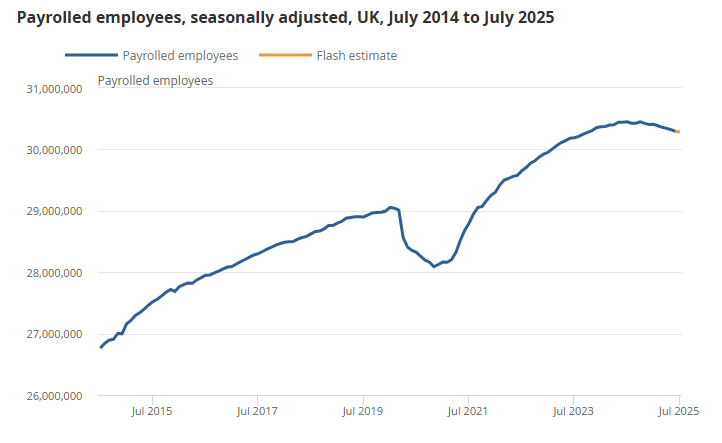

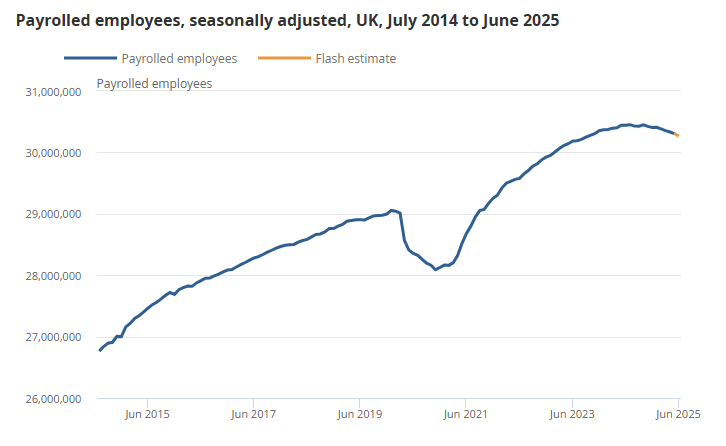

UK payrolled employment was broadly flat MoM and -0.4% YoY in January 2026, continuing negative employee growth trend.

-

Total payrolled employees were 30.3M (-11k MoM; -134k YoY), with January figures provisional and subject to revision as more RTI submissions arrive.

-

December 2025 employment was revised from -43k MoM to -6k MoM, showing typical upward revisions as additional PAYE data are incorporated.

-

Health and social work added +39k employees YoY while wholesale and retail lost -65k, indicating uneven sectoral labor demand.

-

Annual employee growth has been declining steadily since 2022 and is now negative, following earlier post-pandemic recovery strength.

-

Median monthly pay rose +4.6% YoY to £2,588, consistent with pay growth remaining near recent ranges after slowing from earlier peaks.

-

Sector pay growth was highest in wholesale and retail (+6.2% YoY) and lowest in finance and insurance (+2.1%), showing dispersion across industries.

-

Early estimates are based on roughly 85% of available data and typically revised toward 98–99% coverage in later releases.

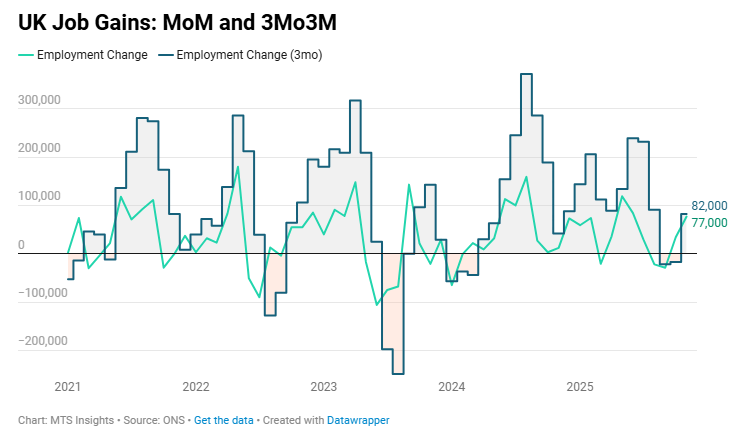

UK employment increased by 82k (vs 27k) in the three months to November, with employment increasing by 77k in November alone.

- The overall employment rate improved from 74.9% in October to 75.1% in November, up 0.2 ppts from a year ago.

- The unemployment rate was unchanged at 5.1% in November but has increased 0.3 ppts in the three months to November and 0.7 ppts YoY.

- The overall unemployment level is up 103k in the last three months and 280k in the last year.

- The economic inactivity rate fell another -0.2 ppts to 20.8%, now down -0.8 ppts YoY.

UK job vacancies rose +1.3% QoQ and fell -8.6% YoY in Oct–Dec 2025, signaling stabilization at lower levels as labor-market tightness continued to ease.

-

Total vacancies increased by +10k (+1.3%) to 734k in Oct–Dec versus Jul–Sep 2025, though the ONS noted vacancies have been broadly flat over the last six periods and the quarterly change remains within the ±32k confidence interval.

-

On a YoY basis, vacancies declined by -69k (-8.6%) versus Oct–Dec 2024, with declines in 13 of 18 industry sectors, indicating the annual cooling in labor demand remains broad-based.

-

Vacancies were 61k (-7.7%) below the pre-pandemic Jan–Mar 2020 level, reinforcing that hiring demand remains below pre-COVID norms despite recent stabilization.

-

Labor market tightness eased further, with 2.5 unemployed people per vacancy in Sep–Nov 2025, up from 2.4 in Jun–Aug 2025 and 1.9 in Sep–Nov 2024.

-

Industry detail showed mixed quarterly movement, with vacancies rising in 11 of 18 sectors; arts, entertainment and recreation posted the largest percentage increase (+31.7%) and one of the largest volume gains (+5k), while transport and storage rose by +4k.

-

Annual declines were steepest in mining and quarrying (-31.3%) and electricity/gas/steam/air conditioning supply (-30.0%), highlighting sharper pullbacks in more cyclical or resource-linked segments.

-

By firm size, three of five business size bands saw QoQ vacancy increases, led by firms with 250–2,499 employees (+7k; +4.0%), while all size bands showed YoY declines, with the largest drops in businesses with 10–49 employees and 2,500+ employees (both -20k).

-

Workforce jobs fell to 36.6M in September 2025 (-116k QoQ; -0.3% QoQ and -115k YoY; -0.3% YoY), driven mainly by a -120k (-2.9%) QoQ and -201k (-4.7%) YoY decline in self-employment jobs.

UK average weekly earnings growth eased slightly in Sep–Nov 2025, with regular pay up +4.5% YoY (+4.6% YoY previously) and total pay up +4.7% YoY (+4.8% YoY previously) as nominal wage momentum remained positive.

-

In real terms using CPIH inflation adjustment, regular pay increased +0.6% YoY and total pay +0.8% YoY, holding steady versus the prior period and indicating modest positive real wage growth.

-

Using CPI inflation (excluding owner occupiers’ housing costs), real regular pay rose +0.9% YoY and real total pay +1.1% YoY, also unchanged from the prior three-month period.

-

Average weekly earnings levels in November 2025 were estimated at £689 for regular pay and £741 for total pay, consistent with the long-run upward trend in nominal earnings.

-

Public sector earnings growth remained elevated, with regular pay up +7.9% YoY and total pay up +7.8% YoY, though the ONS noted this is being boosted by a timing base effect from pay rises being paid earlier in 2025 than in 2024, which has now reached its peak and is expected to fade over the next three months.

-

Private sector wage growth softened further, with regular pay up +3.6% YoY (down from +3.9%) and total pay up +3.9% YoY (down from +4.1%), marking the weakest pace since Sep–Nov 2020 in both measures.

-

By sector, after the public sector, wholesaling/retailing/hotels/restaurants recorded the strongest regular pay growth at +5.1% YoY, while finance and business services was weakest at +2.2% YoY, showing dispersion across industries.

UK payrolled employment fell -0.1% MoM and -0.6% YoY in December 2025, indicating continued softening in employee counts alongside moderating pay growth.

-

Early estimates showed 30.2M payrolled employees in December (-43k; -0.1% MoM), with the ONS noting December figures are provisional and likely to be revised as more RTI submissions are received.

-

On a YoY basis, payrolled employees were down -184k (-0.6%) versus December 2024, extending the negative trend in annual employee growth that has been declining steadily since 2022.

-

The largest sector increase in payrolled employees over the year was in health and social work (+37k), while the largest decline was in wholesale and retail (-72k), pointing to uneven labor demand across industries.

-

November 2025 payrolled employment was revised to a smaller decline of -33k MoM (from -38k previously), reflecting the incorporation of additional real-time PAYE submissions and reduced imputation needs.

-

Median monthly pay rose +4.0% YoY in December to £2,555, with the series described as showing little change in recent months, suggesting pay growth has become more stable after prior volatility.

-

Sectoral median pay growth in December was strongest in wholesale and retail (+5.9% YoY) and weakest in education (+1.4% YoY), indicating dispersion in wage growth across the economy.

-

The bulletin highlighted that early estimates are based on roughly 85% of information and are lower quality than later revisions (typically 98%–99% coverage), underscoring uncertainty around the latest month’s level changes.

UK employment fell by -17k in the three months to October, with employment increasing 34k in October alone.

- The overall employment rate is now down -0.3 ppts to 74.9% and was unchanged from a year ago, the lowest since November 2024.

- The unemployment rate has increased 0.4 ppts in the three months to October to 5.1%, now up 0.8 ppts from a year ago to the highest jobless level since January 2021.

- The overall unemployment level increased 158k in the three months to October with redundancies up 52k and the redundancy rate up 1.7 to 5.3.

- The economic inactivity rate was down -0.1 ppt to 21.0% but down -0.7 ppts YoY.

UK job vacancies were broadly flat in Sep–Nov 2025, edging down -0.2% QoQ and -9.6% YoY, signaling stabilization at lower levels as labor-market tightness continued to ease.

- Total vacancies slipped by just -2k QoQ to 729k in Sep–Nov, remaining broadly unchanged for the sixth consecutive period, indicating little near-term momentum in hiring.

- On a YoY basis, vacancies fell -77k (-9.6%), with declines in 16 of 18 industry sectors, showing widespread cooling in labor demand.

- Vacancies now sit -66k (-8.3%) below their pre-pandemic Jan–Mar 2020 level, underscoring a sustained downshift from peak post-pandemic conditions.

- The unemployment-to-vacancy ratio rose to 2.5 in Aug–Oct (from 2.3 QoQ and 1.8 YoY), marking a continued easing in labor-market tightness.

- Sectorally, the largest QoQ percentage decline in vacancies was in electricity, gas, steam & air conditioning supply (-18.9%), while human health & social work saw the largest volume drop (-8k).

- By firm size, vacancies declined most sharply QoQ and YoY among businesses with 10–49 employees (-6.3% QoQ; -19.6% YoY), indicating particular softness among smaller employers.

- Workforce jobs fell to 36.6M in September, down -116k (-0.3%) QoQ and -115k YoY, driven primarily by a -120k (-2.9%) QoQ and -201k (-4.7%) YoY drop in self-employment.

UK average weekly earnings growth eased slightly in Aug–Oct 2025, with regular pay up +4.6% YoY and total pay up +4.7% YoY, indicating continued but moderating nominal wage momentum.

- In real terms using CPIH, regular pay rose +0.5% YoY and total pay +0.6% YoY, maintaining positive growth as inflation averaged about 4.0% over the period.

- Using CPI inflation, real regular pay increased +0.9% YoY and real total pay +1.0% YoY, showing slightly stronger purchasing power gains under the narrower inflation measure.

- Average weekly earnings reached £687 for regular pay and £739 for total pay in October, extending the long-run upward trend in nominal earnings.

- Public sector regular pay growth accelerated to +7.6% YoY (from +6.6%), reflecting timing effects from earlier pay settlements in 2025.

- Private sector regular pay growth slowed to +3.9% YoY (from +4.2%), its weakest rate since late 2020, indicating softer wage momentum outside the public sector.

- By industry, wholesaling, retailing, hotels and restaurants recorded the strongest regular pay growth after the public sector at +5.5% YoY, while finance and business services posted the weakest increase at +2.3% YoY.

The early PAYE estimate of UK payroll employment continued to decline in November 2025, falling -38k (-0.1% MoM) and -0.6% YoY in November, indicating ongoing labor market cooling alongside slower pay growth.

- The number of payrolled employees slipped by -38k MoM to 30.3M in November, with the monthly estimate flagged as provisional and subject to revision.

- On a YoY basis, employment was down -171k (-0.6%), extending the steady negative trend in employee growth that has been in place since 2022.

- Sectorally, health and social work recorded the largest employment increase (+31k), while wholesale and retail saw the sharpest decline (-70k), highlighting uneven labor demand across industries.

- October payrolled employment was revised to a smaller decline of -22k MoM (from -32k), reflecting additional real-time PAYE submissions.

- Median monthly pay rose +2.7% YoY in November to £2,543, showing continued deceleration in pay growth compared with earlier in the year.

- Pay growth varied widely by sector, with wholesale and retail posting the strongest median pay increase (+6.2% YoY) and education recording a decline (-3.3% YoY).

- Longer-run trends show payrolled employment has fallen from a peak in early 2024, while median pay growth has slowed through 2024–25 after stronger post-pandemic gains.

UK employment fell by -22k in the three months to September, the first decline in employment since March 2024.

- The overall employment rate dropped -0.1 ppts to 75.0% but was still up 0.1 ppt from a year ago. This is the lowest since March 2025.

- The unemployment rate increased 0.2 ppts to 5.0% in September, ahead of expectations of an increase to 4.9% and the highest since February 2021.

- Total redundancies increased 27k to 134k, and total unemployment increased 117k in the three months to September. The redundancy rate is up significantly (+1.3 ppts YoY) to 4.5 per thousand.

- The economic inactivity rate was unchanged at 21.0% but down -0.7 ppts YoY.

UK job vacancies were broadly unchanged in the three months to Oct 2025, edging up +2k (+0.2% QoQ) to 723k, after 39 consecutive quarterly declines, though vacancies remained -99k (-12.0% YoY), signaling stabilization at lower levels as labor-market tightness continued to ease.

-

The number of unemployed people per vacancy rose to 2.5 (from 2.3 in Apr–Jun and 1.8 a year earlier), marking the highest level since mid-2015 (ex-pandemic), reflecting softer hiring conditions.

-

Vacancies increased in half of the 18 industries QoQ, led by professional, scientific & technical activities (+5k) and education (+4k), while “other services” saw the largest percentage gain (+19.6%).

-

Annual declines were broad-based, with 16 of 18 sectors lower; mining & quarrying (-26.7% YoY), real estate (-24.4%), and construction (-20.0%) posted the steepest drops.

-

Compared with pre-pandemic Jan–Mar 2020, total vacancies remained -72k (-9.1%) lower, highlighting a sustained reduction in labor demand from peak 2022 levels.

-

By firm size, vacancies rose QoQ in three of five categories, led by small firms (1–9 employees, +6.0%), while all bands recorded YoY decreases, with the largest decline among firms with 10–49 employees (-21.1% YoY).

UK average weekly earnings growth remained firm in September 2025, with regular pay up +4.6% YoY (vs +4.7% prior) and total pay up +4.8% YoY (vs +5.0% prior), marking a slight moderation but still indicating solid nominal wage momentum.

-

In real terms (CPIH-adjusted), regular pay rose +0.5% YoY and total pay +0.7% YoY, maintaining positive growth for a second consecutive quarter; using CPI, gains were +0.8% and +1.0%, respectively.

-

Average weekly earnings reached £684 for regular pay and £733 for total pay, continuing a steady long-term upward trend.

-

Public sector regular pay growth accelerated to +6.6% YoY (from +6.0%), supported by timing effects from earlier 2025 pay rises, while private sector growth eased to +4.2% (from +4.4%), its weakest since early 2021.

-

Total pay rose +6.8% YoY in the public sector (vs +5.8% prior) and +4.4% YoY in the private sector (vs +4.8%), showing a similar divergence.

-

By industry, wholesaling, retailing, hotels & restaurants posted the strongest regular pay growth after the public sector (+5.7% YoY), while finance & business services recorded the weakest (+2.7%).

-

CPIH inflation averaged 4.1% during the quarter, meaning nominal pay growth continues to outpace consumer price increases modestly.

The early PAYE estimate of UK payrolled employment fell -32k (or -0.1% MoM) in October 2025 to 30.3 million, marking continued labor market cooling after peaking in 2024. On an annual basis, employment dropped -0.6% YoY (-180k).

-

The largest industry gain came from public administration and defence (+16k employees), while wholesale and retail recorded the steepest drop (-71k).

-

September’s data were revised downward to show a -32k MoM decline (from -10k previously), reflecting additional RTI submissions.

-

Median monthly pay increased +3.1% YoY to £2,538 (down significantly from 5.9% YoY in September), the slowest growth in median monthly pay since August 2020.

-

Pay growth was strongest in public administration and defence (+6.5% YoY) and weakest in health and social work (-1.9% YoY).

-

The data suggest employment growth has been negative since early 2025, extending a steady slowdown that began in 2022 as hiring momentum eased post-recovery.

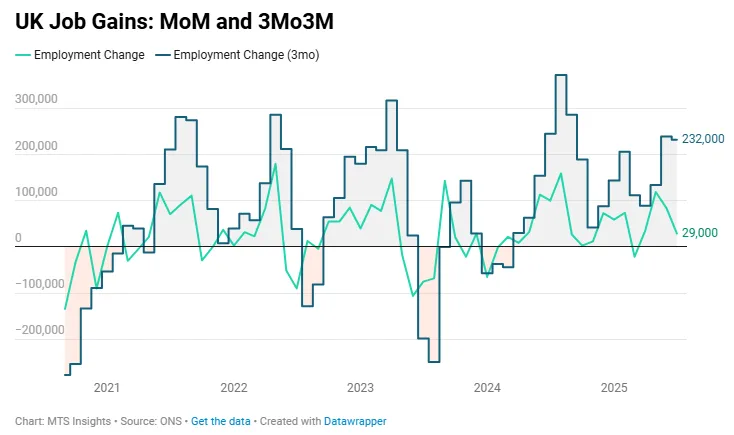

The UK added 91k jobs in the three months to August, down from the 232k increase in the three months to July and the smallest increase since April.

- The unemployment rate ticked up 0.1 ppt to 4.8% in August, slightly ahead of expectations of it remaining at 4.7%. This is the highest unemployment rate since May 2021.

- The economic inactivity rate dropped again, down -0.1 ppt to 21.0% in August and was down -0.7 ppts from a year ago.

UK job vacancies fell -9k (or -1.3% QoQ) to 717k in Jul-Sep 2025 and were -13.8% YoY, extending a three-year slide and signaling further easing in labor-market tightness.

- This was the 39th consecutive quarterly decline, with vacancies now -78k (-9.8%) below the pre-COVID Jan-Mar 2020 level.

- The unemployment-to-vacancy ratio rose to 2.4 in Jun-Aug (from 2.3 in the prior quarter and 1.7 a year earlier), indicating looser hiring conditions.

- Quarterly moves were mixed across industries: 9 of 18 sectors fell, led by real estate activities (-20.6% QoQ); the largest volume drop was in human health & social work (-10k), followed by accommodation & food service (-5k).

- On a YoY basis, vacancies declined in 16 of 18 sectors, with construction showing the steepest fall (-25.9% YoY).

- Relative to pre-pandemic levels, 12 sectors were lower, including wholesale & retail trade, repair of motor vehicles and motorcycles (-37k, -28.3%).

- By firm size, the biggest quarterly decrease was among businesses with 10-49 employees (-8k, -7.0% QoQ); all size bands recorded YoY declines, led again by the 10-49 group (-26k, -19.9% YoY).

UK average weekly earnings rose 4.7% YoY (vs 4.7% YoY expected) for regular pay in August, down from 4.8% YoY in July and the lowest annual growth since May 2022.

- Total pay increased 5.0% YoY (vs 4.7% YoY) in August, up from 4.8% YoY previously as growth in bonus pay appears to have accelerated.

- In real terms (CPIH-adjusted), regular pay grew +0.6% YoY and total pay +0.8% YoY, both remaining positive for a second consecutive quarter.

- Using CPI as the deflator, real regular pay increased +0.9% YoY and total pay +1.2% YoY, up slightly from the prior period.

- Average weekly earnings reached £682 for regular pay and £733 for total pay, continuing a steady long-term upward trend.

- Public sector regular pay rose +6.0% YoY, boosted by timing effects of earlier pay settlements, while private sector pay growth eased to +4.4% YoY, its lowest since late 2021.

- Total pay rose +5.8% YoY in the public sector and +4.8% YoY in the private sector.

- Among industries, the wholesaling, retailing, hotels, and restaurants sector showed the second-strongest regular pay growth (+5.9% YoY), while finance and business services recorded the weakest (+2.9% YoY).

UK payrolled employment edged down -10k (0.0%) MoM in September 2025 to 30.3 million, and was -100k (-0.3%) lower YoY, extending the gradual softening seen since 2022.

- August 2025 data were revised upward from -8k to +10k MoM after incorporating additional RTI submissions.

- The health and social work sector added +45k employees YoY, the largest gain across industries.

- Accommodation and food service activities saw the sharpest decline, with employment down -59k YoY.

- Median monthly pay rose +5.5% YoY in September 2025, with transportation and storage posting the strongest growth (+8.0% YoY) and professional, scientific, and technical activities the weakest (+3.0% YoY).

- The ONS noted that employment growth has been trending lower since early 2022, following post-pandemic recovery highs in 2021.

The UK added 232k jobs in the three months to July, slightly lower than the 239k added in the three months to June, slightly ahead of expectations of a 220k increase. In July alone, 29k jobs were added, the 4th straight month of job gains.

- The unemployment rate was unchanged at 4.7%, as expected, and was up 0.1 ppts in the last three months and 0.5 ppts in the last year.

- The total number of unemployed is only up 34k in the three months to July, down from 59k in the three months to June.

- The economic inactivity rate dropped -0.2 ppts to 21.1% in the three months to July and was down -0.8 ppts from a year ago.

UK job vacancies fell -10k (-1.4%) in the three months to August 2025 to 728k, marking the 38th consecutive quarterly decline and reflecting sustained labor market cooling.

- Vacancies were down -119k (-14.0% YoY) compared with the same period in 2024, and remain -67k (-8.4%) below their pre-COVID Jan–Mar 2020 level.

- Half of the 18 industry sectors reported declines in vacancies, showing broad-based weakness.

- The number of unemployed people per vacancy rose to 2.3 in May–Jul 2025, up from 2.2 in the prior quarter, indicating easing hiring conditions.

- UK workforce jobs totaled 36.8M in June 2025, down -182k (-0.5%) from March 2025, with a sharp drop in self-employment (-159k, -3.7%) offsetting stable employee jobs (-3k).

- On a YoY basis, workforce jobs were up +139k (+0.4%), led by human health and social work activities (+68k, +1.3%).

UK regular pay growth slowed to 4.8% YoY in July 2025 (from 5.0% YoY previously), the lowest since early 2022, while total pay growth was 4.7% YoY, slightly higher than 4.6% YoY in June.

- In real terms (CPIH-adjusted), regular pay rose 0.7% YoY (vs 0.9% previously), and total pay increased 0.5% YoY, unchanged from the prior three-month period.

- Using CPI as the deflator, real regular pay grew 1.2% YoY, while real total pay rose 1.0%, both above CPIH-based measures.

- Public sector regular pay growth was 5.6% YoY, slightly down from 5.7%, while total pay growth was 5.1% (vs 5.3% previously).

- Private sector regular pay growth slowed to 4.7% YoY (from 4.8%), with total pay at 4.6% YoY, its lowest since Jan–Mar 2021.

- The wholesaling, retailing, hotels, and restaurants sector recorded the strongest annual regular earnings growth among industries.

UK payrolled employment fell -8k (0.0%) MoM in August 2025 to 30.3M, down -127k (-0.4%) YoY, reflecting ongoing softness in the labor market.

- July’s decline was revised from -8k to -6k as additional real-time information submissions were incorporated.

- The health and social work sector added +80k employees YoY, the largest gain across industries.

- Accommodation and food service activities saw the largest drop, with employment down -90k YoY.

- Median monthly pay rose +6.6% YoY in August 2025, showing strong wage growth despite weaker employment trends.

- Pay growth was highest in health and social work (+11.0% YoY) and lowest in professional, scientific, and technical activities (+3.3% YoY).

The UK added 239k jobs in the three months to June, up from the 134k added in the three months to May and ahead of expectations.

- The unemployment rate was unchanged at 4.7% in June, as expected, but has increased 0.5 ppts over the last year.

- The total number of unemployed increased 59k in the three months to June and 206k over the last year.

- The economic inactivity rate is down -0.4 ppts to 21.0% in the three months to June and is down -1.1 ppts over the last year.

The total number of job vacancies was down -44k to 718k in the three months to June, a smaller decline than the -56k drop in the three months to May and the lowest number of vacancies since April 2021.

- Total vacancies decreased by -145k (-16.8% YoY) when comparing May to July 2025 with the same period last year.

- There were declines in 16 of the 18 industry sectors. The industry with the largest percentage decrease in vacancies was the manufacturing industry, which was down by -26.6% YoY.

- The number of unemployed people per vacancy was 2.3 in April to June 2025; this is up from 2.1 in the previous quarter (January to March 2025).

Total pay growth in June was 4.6% YoY (vs 4.7% YoY expected), down from 5.0% YoY in May and the lowest since September 2024.

- Regular pay growth was 5.0% YoY (5.0% YoY expected) in June, unchanged from May and at the lowest since June 2022.

- Annual average regular earnings growth was 4.8% YoY for the private sector. This is similar to the previous three-month period, when it was 4.9% YoY.

The early estimate of payroll employment in July indicates that there was a decline of just -8k, up from the decline of -26k in June (revised up from -41k).

- This would be a decline of -164k over the last year, or a -0.5% YoY drop.

- Early estimates for July 2025 indicate that median monthly pay increased by 5.7% YoY in July, up from 5.6% YoY in June.

The UK added 134k jobs in the three months to May, up from 89k jobs added in the three months to April and well ahead of expectations of a 46k increase.

- The unemployment rate increased another 0.1 ppts to 4.7% (vs 4.6% expected) and is up 0.2 ppts in the last three months.

- The total number of unemployed has increased 98k in the three months to May and is up 124k YoY.

- The economic inactivity rate is down -0.4 ppts to 21.0% in the three months to May and is down -1.1 ppts over the last year.

- While unemployment has increased, the redundancy rate is actually down -0.1 to 3.9 in the three months to May.

The total number of job openings fell again, dropping -56k or -7.2% MoM in the three months to June to 727k, the lowest since April 2021.

- The total number of vacancies has dropped by an estimated 573k since its peak in March to May 2022.

- The number of unemployed people per vacancy was 2.3 in March to May 2025; this is up from 2.0 in the previous quarter (December 2024 to February 2025).

Total pay growth in May was 5.0% YoY (vs 5.0% YoY expected), down significantly from 5.4% YoY in April and the lowest since September 2024.

- Regular pay growth also eased to 5.0% YoY (vs 4.9% YoY expected) in May, down from 5.3% YoY in April and the lowest since June 2022.

- Regular pay growth in the private sector eased to 4.9% YoY (from 5.2% YoY), the lowest since February 2022.

- Regular pay growth in the public sector saw a smaller deceleration to 5.5% YoY (from 5.6% YoY).

The early estimate of payroll employment in June indicates a decline of -41k in June, a larger drop than the -25k decline seen in May (revised up from -10.9k initial estimate).

- This would be a decline of -178k over the last year, or a -0.6% YoY drop.

- The flash estimate of median pay growth for June is 5.6% YoY, down from the estimate of 5.7% YoY in May.