UK Employment: November 2025 Report

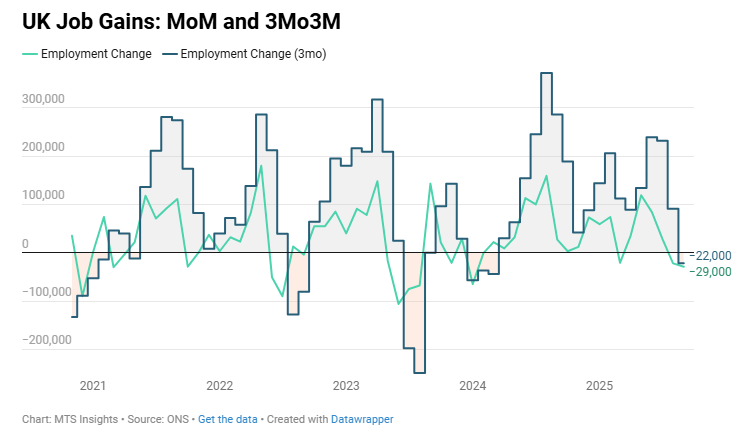

UK employment fell by -22k in the three months to September, the first decline in employment since March 2024.

- The overall employment rate dropped -0.1 ppts to 75.0% but was still up 0.1 ppt from a year ago. This is the lowest since March 2025.

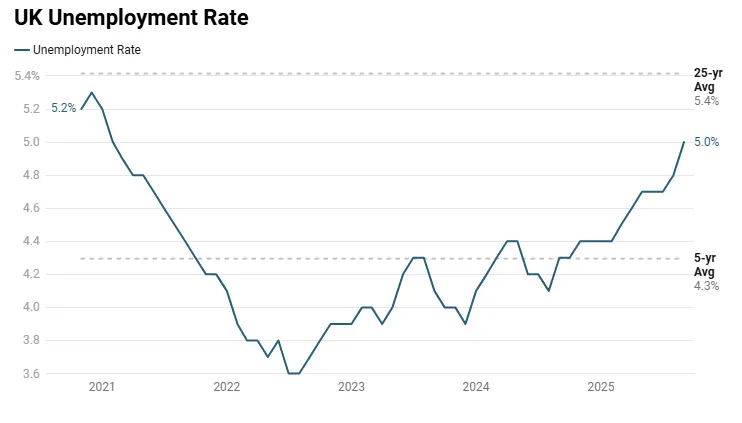

- The unemployment rate increased 0.2 ppts to 5.0% in September, ahead of expectations of an increase to 4.9% and the highest since February 2021.

- Total redundancies increased 27k to 134k, and total unemployment increased 117k in the three months to September. The redundancy rate is up significantly (+1.3 ppts YoY) to 4.5 per thousand.

- The economic inactivity rate was unchanged at 21.0% but down -0.7 ppts YoY.

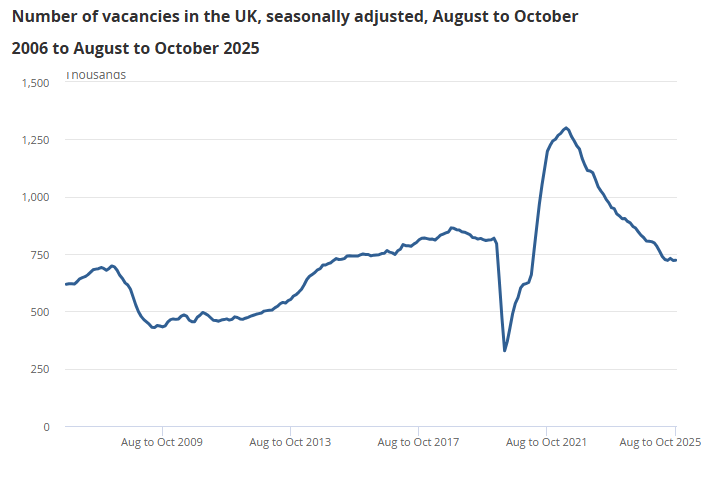

UK job vacancies were broadly unchanged in the three months to Oct 2025, edging up +2k (+0.2% QoQ) to 723k, after 39 consecutive quarterly declines, though vacancies remained -99k (-12.0% YoY), signaling stabilization at lower levels as labor-market tightness continued to ease.

-

The number of unemployed people per vacancy rose to 2.5 (from 2.3 in Apr–Jun and 1.8 a year earlier), marking the highest level since mid-2015 (ex-pandemic), reflecting softer hiring conditions.

-

Vacancies increased in half of the 18 industries QoQ, led by professional, scientific & technical activities (+5k) and education (+4k), while “other services” saw the largest percentage gain (+19.6%).

-

Annual declines were broad-based, with 16 of 18 sectors lower; mining & quarrying (-26.7% YoY), real estate (-24.4%), and construction (-20.0%) posted the steepest drops.

-

Compared with pre-pandemic Jan–Mar 2020, total vacancies remained -72k (-9.1%) lower, highlighting a sustained reduction in labor demand from peak 2022 levels.

-

By firm size, vacancies rose QoQ in three of five categories, led by small firms (1–9 employees, +6.0%), while all bands recorded YoY decreases, with the largest decline among firms with 10–49 employees (-21.1% YoY).

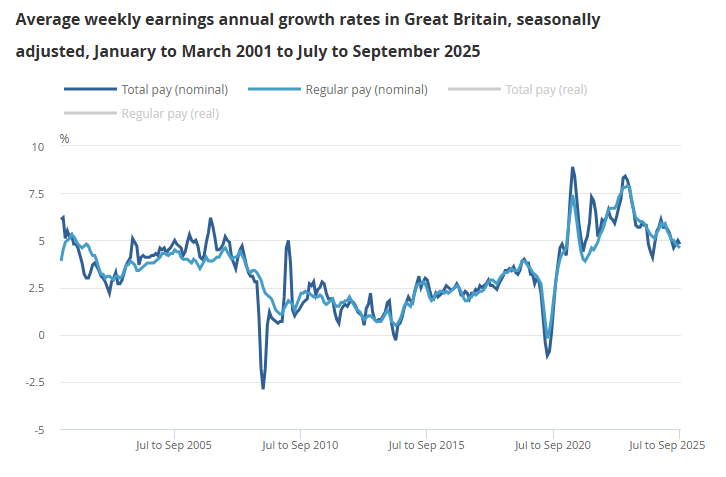

UK average weekly earnings growth remained firm in September 2025, with regular pay up +4.6% YoY (vs +4.7% prior) and total pay up +4.8% YoY (vs +5.0% prior), marking a slight moderation but still indicating solid nominal wage momentum.

-

In real terms (CPIH-adjusted), regular pay rose +0.5% YoY and total pay +0.7% YoY, maintaining positive growth for a second consecutive quarter; using CPI, gains were +0.8% and +1.0%, respectively.

-

Average weekly earnings reached £684 for regular pay and £733 for total pay, continuing a steady long-term upward trend.

-

Public sector regular pay growth accelerated to +6.6% YoY (from +6.0%), supported by timing effects from earlier 2025 pay rises, while private sector growth eased to +4.2% (from +4.4%), its weakest since early 2021.

-

Total pay rose +6.8% YoY in the public sector (vs +5.8% prior) and +4.4% YoY in the private sector (vs +4.8%), showing a similar divergence.

-

By industry, wholesaling, retailing, hotels & restaurants posted the strongest regular pay growth after the public sector (+5.7% YoY), while finance & business services recorded the weakest (+2.7%).

-

CPIH inflation averaged 4.1% during the quarter, meaning nominal pay growth continues to outpace consumer price increases modestly.

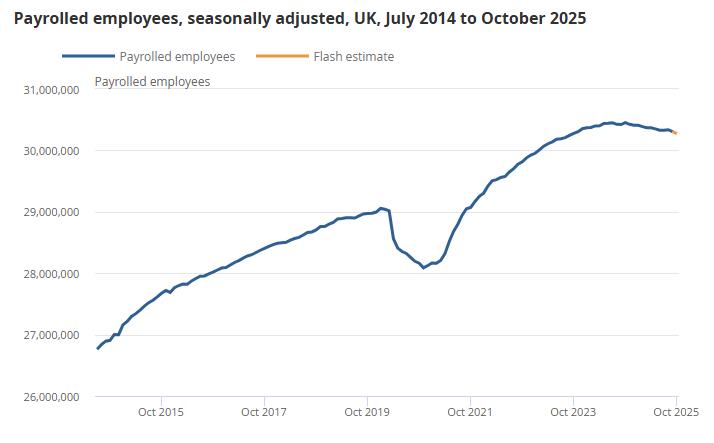

The early PAYE estimate of UK payrolled employment fell -32k (or -0.1% MoM) in October 2025 to 30.3 million, marking continued labor market cooling after peaking in 2024. On an annual basis, employment dropped -0.6% YoY (-180k).

-

The largest industry gain came from public administration and defence (+16k employees), while wholesale and retail recorded the steepest drop (-71k).

-

September’s data were revised downward to show a -32k MoM decline (from -10k previously), reflecting additional RTI submissions.

-

Median monthly pay increased +3.1% YoY to £2,538 (down significantly from 5.9% YoY in September), the slowest growth in median monthly pay since August 2020.

-

Pay growth was strongest in public administration and defence (+6.5% YoY) and weakest in health and social work (-1.9% YoY).

-

The data suggest employment growth has been negative since early 2025, extending a steady slowdown that began in 2022 as hiring momentum eased post-recovery.