UK Employment: January 2026 Report

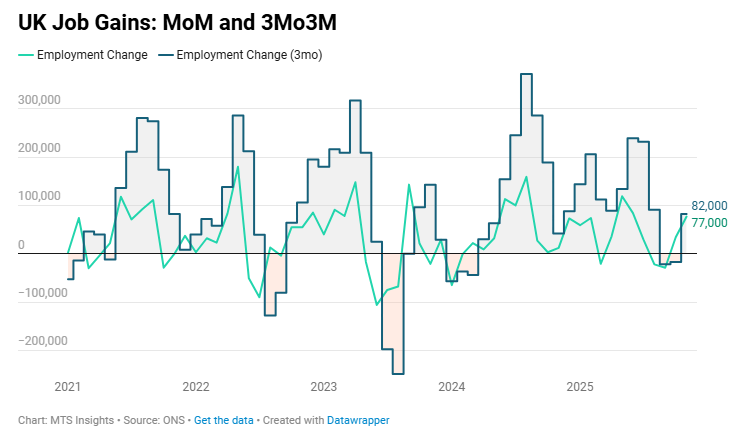

UK employment increased by 82k (vs 27k) in the three months to November, with employment increasing by 77k in November alone.

- The overall employment rate improved from 74.9% in October to 75.1% in November, up 0.2 ppts from a year ago.

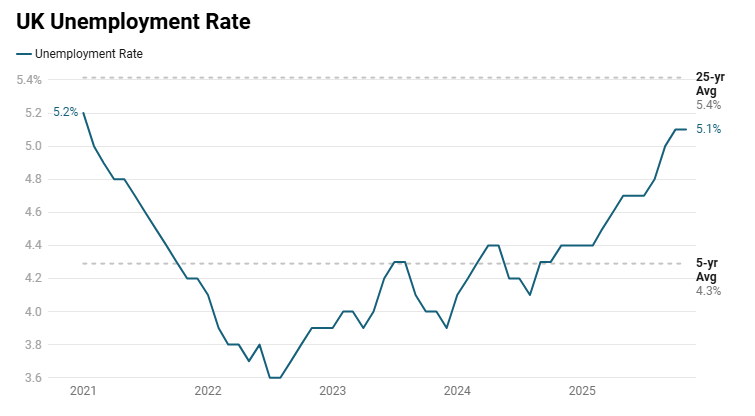

- The unemployment rate was unchanged at 5.1% in November but has increased 0.3 ppts in the three months to November and 0.7 ppts YoY.

- The overall unemployment level is up 103k in the last three months and 280k in the last year.

- The economic inactivity rate fell another -0.2 ppts to 20.8%, now down -0.8 ppts YoY.

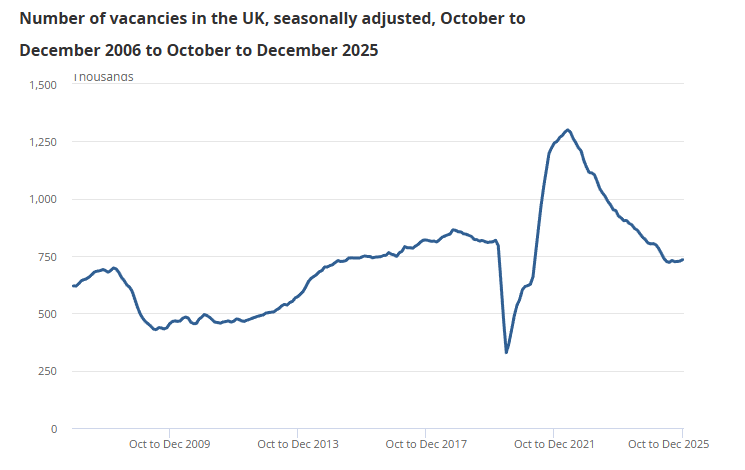

UK job vacancies rose +1.3% QoQ and fell -8.6% YoY in Oct–Dec 2025, signaling stabilization at lower levels as labor-market tightness continued to ease.

-

Total vacancies increased by +10k (+1.3%) to 734k in Oct–Dec versus Jul–Sep 2025, though the ONS noted vacancies have been broadly flat over the last six periods and the quarterly change remains within the ±32k confidence interval.

-

On a YoY basis, vacancies declined by -69k (-8.6%) versus Oct–Dec 2024, with declines in 13 of 18 industry sectors, indicating the annual cooling in labor demand remains broad-based.

-

Vacancies were 61k (-7.7%) below the pre-pandemic Jan–Mar 2020 level, reinforcing that hiring demand remains below pre-COVID norms despite recent stabilization.

-

Labor market tightness eased further, with 2.5 unemployed people per vacancy in Sep–Nov 2025, up from 2.4 in Jun–Aug 2025 and 1.9 in Sep–Nov 2024.

-

Industry detail showed mixed quarterly movement, with vacancies rising in 11 of 18 sectors; arts, entertainment and recreation posted the largest percentage increase (+31.7%) and one of the largest volume gains (+5k), while transport and storage rose by +4k.

-

Annual declines were steepest in mining and quarrying (-31.3%) and electricity/gas/steam/air conditioning supply (-30.0%), highlighting sharper pullbacks in more cyclical or resource-linked segments.

-

By firm size, three of five business size bands saw QoQ vacancy increases, led by firms with 250–2,499 employees (+7k; +4.0%), while all size bands showed YoY declines, with the largest drops in businesses with 10–49 employees and 2,500+ employees (both -20k).

-

Workforce jobs fell to 36.6M in September 2025 (-116k QoQ; -0.3% QoQ and -115k YoY; -0.3% YoY), driven mainly by a -120k (-2.9%) QoQ and -201k (-4.7%) YoY decline in self-employment jobs.

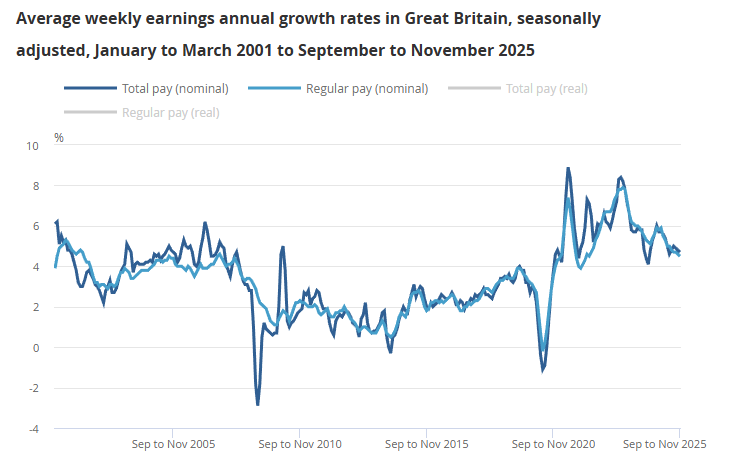

UK average weekly earnings growth eased slightly in Sep–Nov 2025, with regular pay up +4.5% YoY (+4.6% YoY previously) and total pay up +4.7% YoY (+4.8% YoY previously) as nominal wage momentum remained positive.

-

In real terms using CPIH inflation adjustment, regular pay increased +0.6% YoY and total pay +0.8% YoY, holding steady versus the prior period and indicating modest positive real wage growth.

-

Using CPI inflation (excluding owner occupiers’ housing costs), real regular pay rose +0.9% YoY and real total pay +1.1% YoY, also unchanged from the prior three-month period.

-

Average weekly earnings levels in November 2025 were estimated at £689 for regular pay and £741 for total pay, consistent with the long-run upward trend in nominal earnings.

-

Public sector earnings growth remained elevated, with regular pay up +7.9% YoY and total pay up +7.8% YoY, though the ONS noted this is being boosted by a timing base effect from pay rises being paid earlier in 2025 than in 2024, which has now reached its peak and is expected to fade over the next three months.

-

Private sector wage growth softened further, with regular pay up +3.6% YoY (down from +3.9%) and total pay up +3.9% YoY (down from +4.1%), marking the weakest pace since Sep–Nov 2020 in both measures.

-

By sector, after the public sector, wholesaling/retailing/hotels/restaurants recorded the strongest regular pay growth at +5.1% YoY, while finance and business services was weakest at +2.2% YoY, showing dispersion across industries.

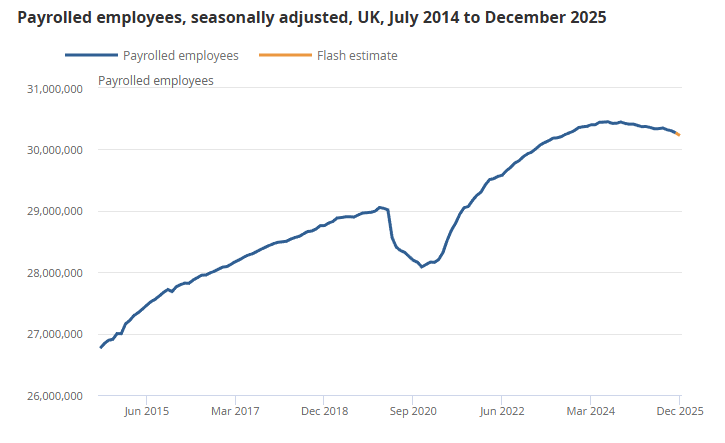

UK payrolled employment fell -0.1% MoM and -0.6% YoY in December 2025, indicating continued softening in employee counts alongside moderating pay growth.

-

Early estimates showed 30.2M payrolled employees in December (-43k; -0.1% MoM), with the ONS noting December figures are provisional and likely to be revised as more RTI submissions are received.

-

On a YoY basis, payrolled employees were down -184k (-0.6%) versus December 2024, extending the negative trend in annual employee growth that has been declining steadily since 2022.

-

The largest sector increase in payrolled employees over the year was in health and social work (+37k), while the largest decline was in wholesale and retail (-72k), pointing to uneven labor demand across industries.

-

November 2025 payrolled employment was revised to a smaller decline of -33k MoM (from -38k previously), reflecting the incorporation of additional real-time PAYE submissions and reduced imputation needs.

-

Median monthly pay rose +4.0% YoY in December to £2,555, with the series described as showing little change in recent months, suggesting pay growth has become more stable after prior volatility.

-

Sectoral median pay growth in December was strongest in wholesale and retail (+5.9% YoY) and weakest in education (+1.4% YoY), indicating dispersion in wage growth across the economy.

-

The bulletin highlighted that early estimates are based on roughly 85% of information and are lower quality than later revisions (typically 98%–99% coverage), underscoring uncertainty around the latest month’s level changes.