UK Employment: December 2025 Report

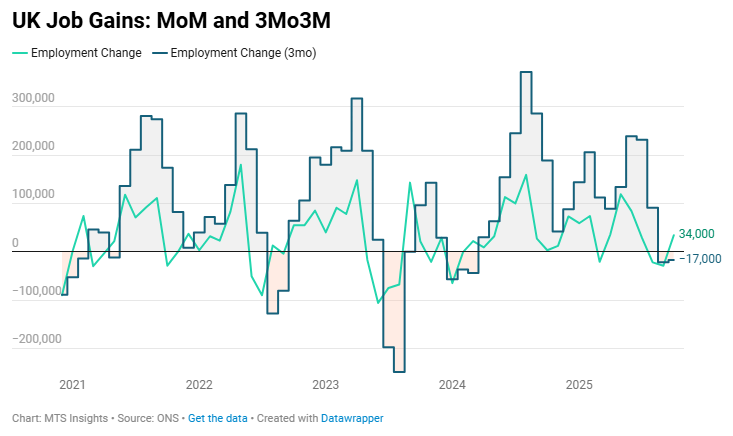

UK employment fell by -17k in the three months to October, with employment increasing 34k in October alone.

- The overall employment rate is now down -0.3 ppts to 74.9% and was unchanged from a year ago, the lowest since November 2024.

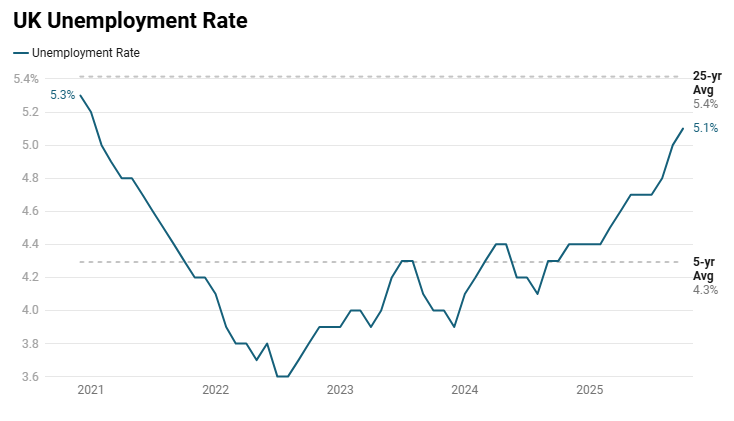

- The unemployment rate has increased 0.4 ppts in the three months to October to 5.1%, now up 0.8 ppts from a year ago to the highest jobless level since January 2021.

- The overall unemployment level increased 158k in the three months to October with redundancies up 52k and the redundancy rate up 1.7 to 5.3.

- The economic inactivity rate was down -0.1 ppt to 21.0% but down -0.7 ppts YoY.

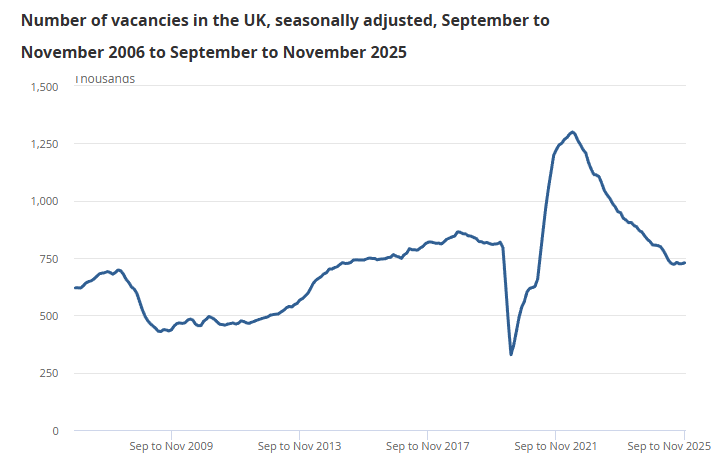

UK job vacancies were broadly flat in Sep–Nov 2025, edging down -0.2% QoQ and -9.6% YoY, signaling stabilization at lower levels as labor-market tightness continued to ease.

- Total vacancies slipped by just -2k QoQ to 729k in Sep–Nov, remaining broadly unchanged for the sixth consecutive period, indicating little near-term momentum in hiring.

- On a YoY basis, vacancies fell -77k (-9.6%), with declines in 16 of 18 industry sectors, showing widespread cooling in labor demand.

- Vacancies now sit -66k (-8.3%) below their pre-pandemic Jan–Mar 2020 level, underscoring a sustained downshift from peak post-pandemic conditions.

- The unemployment-to-vacancy ratio rose to 2.5 in Aug–Oct (from 2.3 QoQ and 1.8 YoY), marking a continued easing in labor-market tightness.

- Sectorally, the largest QoQ percentage decline in vacancies was in electricity, gas, steam & air conditioning supply (-18.9%), while human health & social work saw the largest volume drop (-8k).

- By firm size, vacancies declined most sharply QoQ and YoY among businesses with 10–49 employees (-6.3% QoQ; -19.6% YoY), indicating particular softness among smaller employers.

- Workforce jobs fell to 36.6M in September, down -116k (-0.3%) QoQ and -115k YoY, driven primarily by a -120k (-2.9%) QoQ and -201k (-4.7%) YoY drop in self-employment.

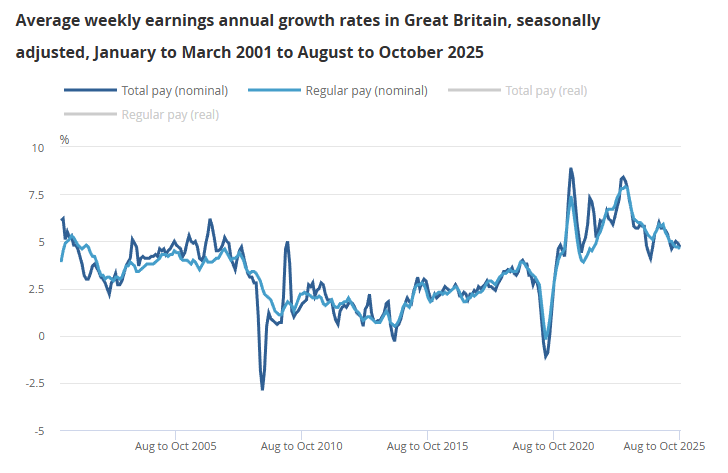

UK average weekly earnings growth eased slightly in Aug–Oct 2025, with regular pay up +4.6% YoY and total pay up +4.7% YoY, indicating continued but moderating nominal wage momentum.

- In real terms using CPIH, regular pay rose +0.5% YoY and total pay +0.6% YoY, maintaining positive growth as inflation averaged about 4.0% over the period.

- Using CPI inflation, real regular pay increased +0.9% YoY and real total pay +1.0% YoY, showing slightly stronger purchasing power gains under the narrower inflation measure.

- Average weekly earnings reached £687 for regular pay and £739 for total pay in October, extending the long-run upward trend in nominal earnings.

- Public sector regular pay growth accelerated to +7.6% YoY (from +6.6%), reflecting timing effects from earlier pay settlements in 2025.

- Private sector regular pay growth slowed to +3.9% YoY (from +4.2%), its weakest rate since late 2020, indicating softer wage momentum outside the public sector.

- By industry, wholesaling, retailing, hotels and restaurants recorded the strongest regular pay growth after the public sector at +5.5% YoY, while finance and business services posted the weakest increase at +2.3% YoY.

The early PAYE estimate of UK payroll employment continued to decline in November 2025, falling -38k (-0.1% MoM) and -0.6% YoY in November, indicating ongoing labor market cooling alongside slower pay growth.

- The number of payrolled employees slipped by -38k MoM to 30.3M in November, with the monthly estimate flagged as provisional and subject to revision.

- On a YoY basis, employment was down -171k (-0.6%), extending the steady negative trend in employee growth that has been in place since 2022.

- Sectorally, health and social work recorded the largest employment increase (+31k), while wholesale and retail saw the sharpest decline (-70k), highlighting uneven labor demand across industries.

- October payrolled employment was revised to a smaller decline of -22k MoM (from -32k), reflecting additional real-time PAYE submissions.

- Median monthly pay rose +2.7% YoY in November to £2,543, showing continued deceleration in pay growth compared with earlier in the year.

- Pay growth varied widely by sector, with wholesale and retail posting the strongest median pay increase (+6.2% YoY) and education recording a decline (-3.3% YoY).

- Longer-run trends show payrolled employment has fallen from a peak in early 2024, while median pay growth has slowed through 2024–25 after stronger post-pandemic gains.