Philadelphia Fed Manufacturing Business Outlook Survey

About

-

July 16th, 2026 · 8:30 AM

-

August 20th, 2026 · 8:30 AM

-

September 17th, 2026 · 8:30 AM

-

October 15th, 2026 · 8:30 AM

-

November 19th, 2026 · 8:30 AM

-

December 17th, 2026 · 8:30 AM

Latest Releases

12

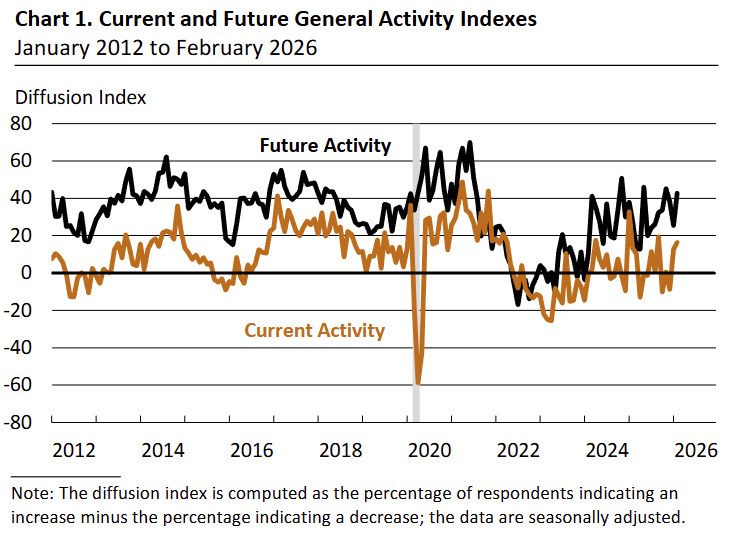

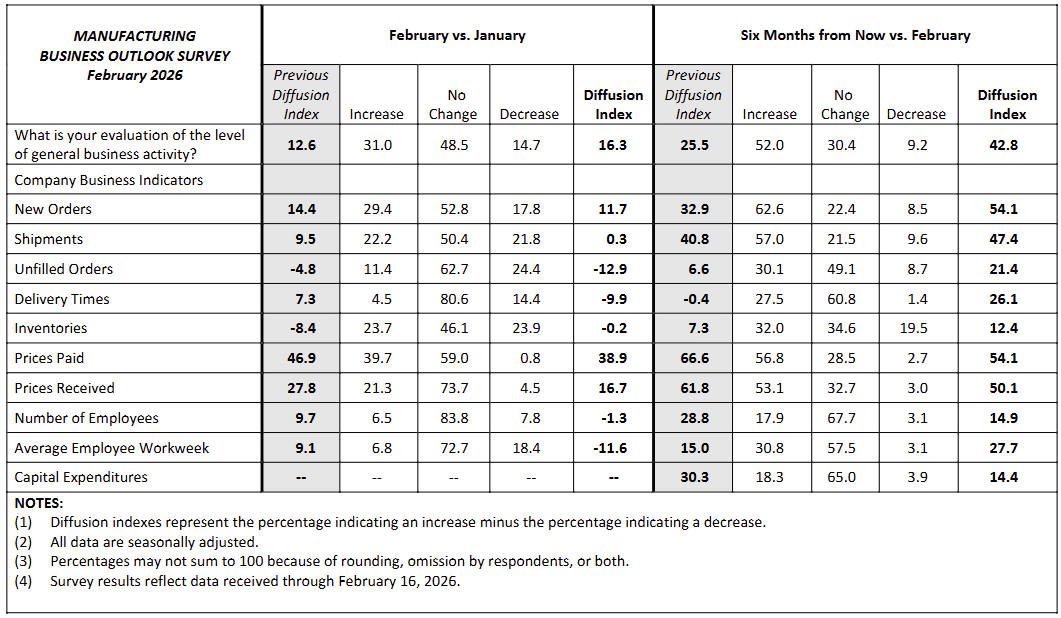

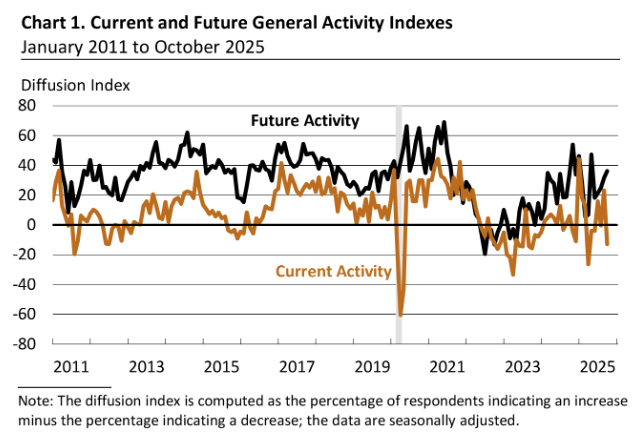

The Philadelphia Fed Manufacturing Business Outlook Survey regional manufacturing activity index rose to 16.3 in February (+4 pts MoM), indicating continued expansion overall.

-

The new orders index declined to 11.7 (from 14.4 MoM) while shipments fell to 0.3 (-9 pts), showing demand remained positive but output momentum weakened.

-

Employment slipped to -1.3 (from 9.7 MoM) and the average workweek dropped to -11.6, suggesting mostly steady staffing but reduced hours.

-

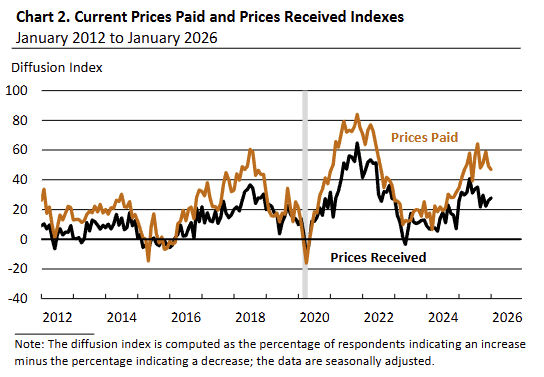

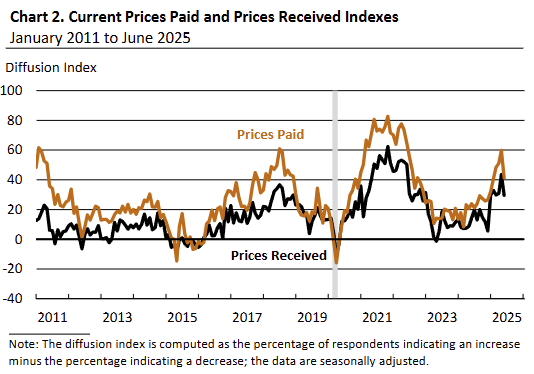

Prices paid decreased to 38.9 (from 46.9 MoM), its third consecutive decline yet still elevated, indicating ongoing but moderating input cost pressures.

-

Prices received fell to 16.7 (-11 pts MoM), the lowest since December 2024, showing slower selling price increases.

-

31% of firms reported increased activity while 15% reported declines, with nearly half unchanged, consistent with modest expansion breadth.

-

Forward expectations strengthened: the future activity index rose to 42.8 and future new orders to 54.1, indicating more widespread anticipated growth over the next six months.

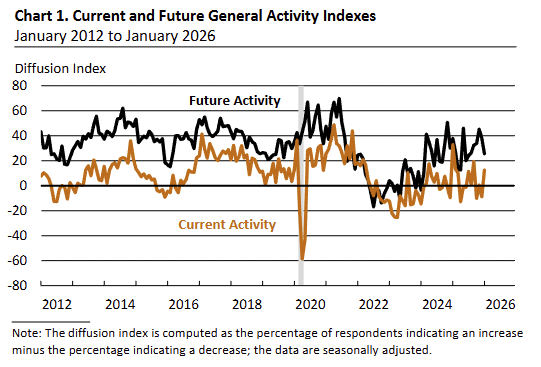

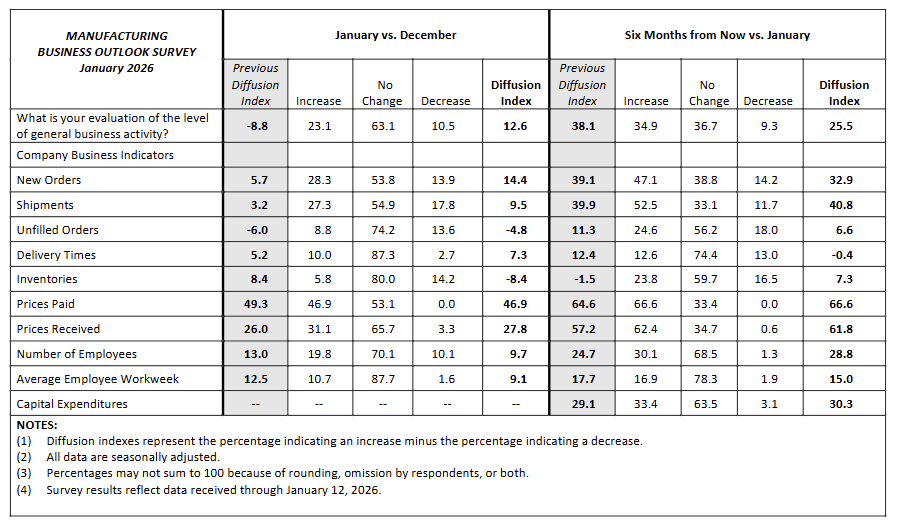

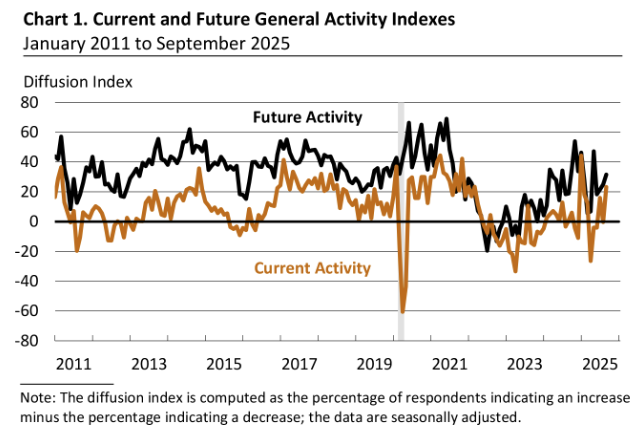

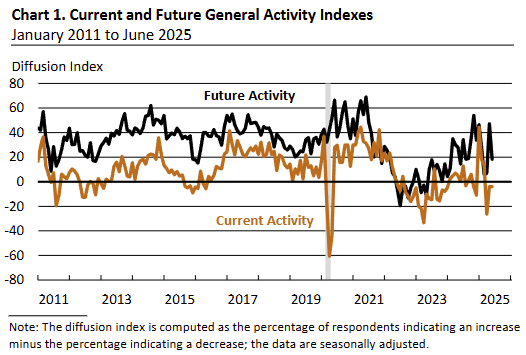

Manufacturing activity improved in January, with the general activity index jumping +21.4 pts to 12.6 and turning positive, alongside firmer demand and shipment growth.

-

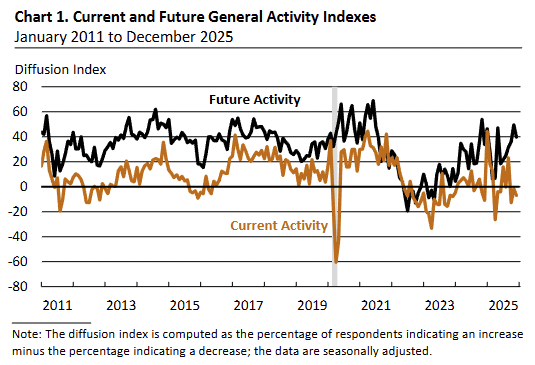

The diffusion index for current general activity rose to 12.6 in January (from -8.8 in December), the highest reading since September, with 23.1% of firms reporting increases vs 10.5% reporting decreases (63.1% no change).

-

Demand indicators strengthened: the current new orders index increased +8.7 pts to 14.4, and the current shipments index rose +6.3 pts to 9.5, signaling broader improvement in near-term activity.

-

Inventories moved lower, with the inventories index falling -16.8 pts to -8.4 (lowest since July 2024), indicating more firms reported inventory declines than builds.

-

Employment conditions remained positive but cooled slightly, with the number of employees index down -3.3 pts to 9.7; nearly 19.8% reported higher employment vs 10.1% reporting declines (70.1% unchanged).

-

The average workweek index declined from 12.5 to 9.1, suggesting a slower pace of hours growth even as the survey still pointed to expansion.

-

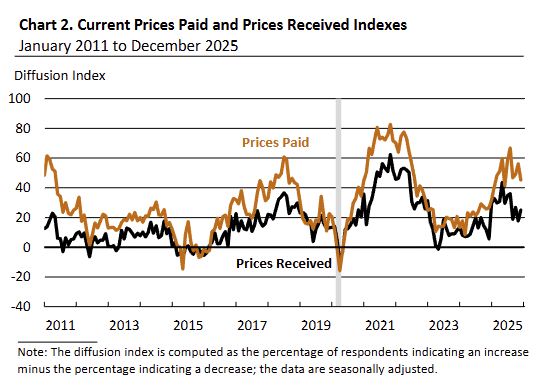

Price pressures stayed elevated: prices paid edged down -2.4 pts to 46.9 (second consecutive decline, lowest since June), while prices received ticked up +1.8 pts to 27.8, indicating ongoing input inflation with continued (but uneven) selling-price increases.

-

Forward-looking activity expectations softened but remained expansionary, with the future general activity index falling from 38.1 to 25.5 (lowest since July); future new orders slipped to 32.9 (-6.2 pts) while future shipments increasedIse edged up to 40.8 (+0.9 pt).

-

Firms continued to anticipate inflationary pressure ahead, with future prices paid at 66.6 and future prices received at 61.8, and the future capital expenditures index edging up to 30.3 (+1.2 pts), signaling modest capex plans.

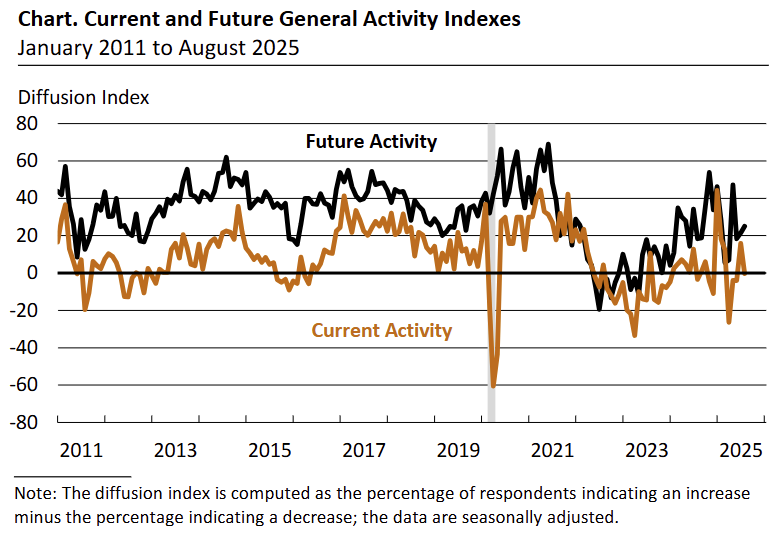

Manufacturing activity weakened in December, with the general activity index falling further into negative territory, reflecting continued softness despite improvements in some demand indicators.

-

The General Activity Index declined to -10.2 in December (from -1.7 in November), its third consecutive negative reading, as fewer firms reported increases and a larger share reported no change.

-

New orders turned positive, with the index rising to 5.0 (from -8.6), indicating a modest rebound in demand after last month’s contraction.

-

Shipments also moved back into positive territory at 3.2 (from -8.7), suggesting a partial recovery in output flows.

-

The employment index increased to 12.9 (from 6.0), its highest level since May, with most firms reporting unchanged headcounts but more increases than decreases.

-

The average workweek index rose to 14.7 (from 3.7), pointing to longer hours alongside reported gains in employment.

-

Input cost pressures eased, as the prices paid index fell to 43.6 (from 56.1), its lowest reading since June, though it remained elevated.

-

Pricing power improved modestly, with the prices received index rising to 24.3 (from 17.7), largely reversing the prior month’s decline.

The Philadelphia Fed’s Manufacturing Business Outlook Survey showed the General Activity Index rising +11.1 pts to -1.7 in November, still negative and reflecting ongoing softness in regional manufacturing.

-

New Orders fell -27 pts to -8.6, the lowest since April, indicating a notable pullback in demand after last month’s positive reading.

-

Shipments dropped -15 pts to -8.7, the first negative print since May, signaling weaker output momentum.

-

Employment ticked up to 6.0 (+1 pt), with most firms reporting unchanged staffing, suggesting modest net hiring despite softer activity.

-

The Average Workweek Index fell sharply to 3.7 (from 12.8), implying a reduction in hours worked even as employment increased.

-

Prices Paid rose to 56.1 (+7 pts), remaining well above the long-run average and showing continued input cost pressures.

-

Prices Received declined to 17.7 (-9 pts), more than reversing last month’s gain and indicating softer pricing power.

-

The Future General Activity Index jumped to 49.6 (+13.4 pts), its strongest in a year, with firms expecting better orders, shipments, and continued price increases over the next six months.

The Philadelphia Fed Manufacturing Business Outlook Survey showed the General Activity Index dropped 36 pts to -12.8 in October, its lowest since April, signaling a pullback in regional manufacturing momentum.

-

Shipments fell 20 pts to 6.0, remaining positive but indicating weaker output growth compared with September.

-

New Orders rose 6 pts to 18.2, marking a second straight monthly gain and suggesting firmer demand conditions.

-

Employment edged down 1 pt to 4.6, showing slower but still positive job growth; 81% of firms reported no change in staffing.

-

The Average Workweek Index eased to 12.8 (from 14.9), implying a slight reduction in hours worked.

-

Prices Paid increased 3 pts to 49.2, and Prices Received rose 8 pts to 26.8, both staying above long-run averages and indicating continued price pressures.

-

The Future General Activity Index climbed 5 pts to 36.2, with expectations for New Orders (+7 pts to 49.8) and Shipments (+17 pts to 48.4) both strengthening.

-

Nearly 36% of firms plan to raise total capital expenditures next year, compared with 19% expecting declines, with spending increases most common in equipment and software.

The Philadelphia Fed Manufacturing Business Outlook Survey showed the General Activity Index rose 24 pts to 23.2 in September, its highest since January, with new orders and shipments returning to positive territory.

-

New Orders increased 14 pts to 12.4, marking the first positive reading since April, while Shipments surged 22 pts to 26.1, both indicating stronger demand momentum.

-

The Employment Index was little changed at 5.6, still reflecting modest job growth, while the Average Workweek rose 10 pts to 14.9.

-

Prices Paid fell 20 pts to 46.8, down from last month’s multiyear high, while Prices Received declined 17 pts to 18.8, signaling some easing in cost pressures though both remain elevated.

-

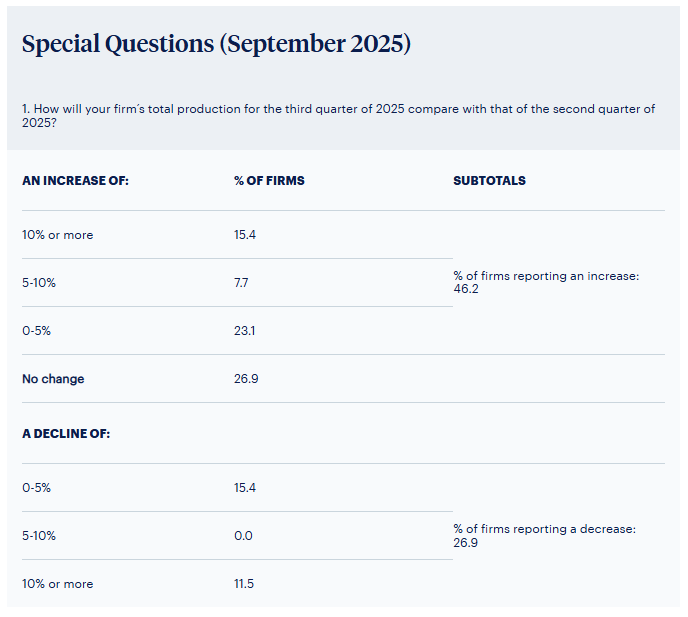

Special questions showed 46% of firms reported higher Q3 production versus Q2, with median capacity utilization steady at 70–80%. Uncertainty, labor supply, and supply chains remained key constraints.

-

The Future General Activity Index rose 7 pts to 31.5, with firms broadly expecting growth over the next six months; future employment expectations strengthened, but future capital expenditure plans fell sharply.

The Philadelphia Fed Manufacturing Business Outlook Survey’s General Activity Index dropped sharply to -0.3 in August from 15.9 in July, with new orders turning negative and shipments weakening, signaling a loss of momentum.

-

New Orders fell 20 pts to -1.9, the first negative reading since April, while Shipments dropped to 4.5, erasing last month’s gains.

-

The Employment Index eased to 5.9 (from 10.3) but still indicated modest job growth; the Average Workweek rose to 4.7.

-

Prices Paid surged 8 pts to 66.8, the highest since May 2022, while Prices Received edged up to 36.1, showing continued price pressures.

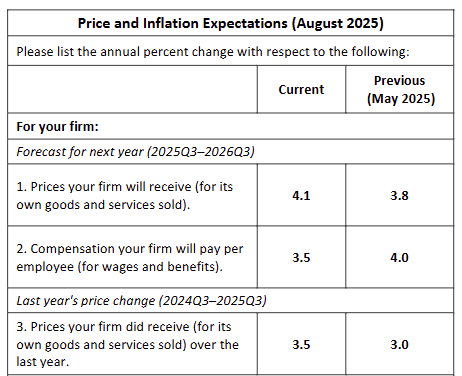

-

Firms expect their own prices to rise 4.1% over the next year (vs 3.8% in May), while wage/benefit costs are expected to grow 3.5% (down from 4.0%).

-

Future expectations strengthened, with the Future General Activity Index up to 25.0, and New Orders (39.2), Shipments (40.3), and Capital Expenditures (38.4) all at multi-month highs.

The Philadelphia Fed Manufacturing Business Outlook Survey’s General Activity Index rose to 15.9 in July from -4.0 in June, marking the first positive reading in four months and the highest since February.

- New Orders jumped to 18.4 (from 2.3) and Shipments rose to 23.7 (from 8.3), both reaching five-month highs.

- The Employment Index climbed to 10.3 (from -9.8), indicating firms are adding workers again, while the Average Workweek edged up to 0.4.

- Prices Paid surged to 58.8 (from 41.4), and Prices Received increased to 34.8 (from 29.5), showing a reacceleration in cost and selling price pressures.

- The Delivery Times Index fell to -4.7, suggesting faster delivery times, while Inventories dipped to -1.3.

- Future activity measures remained positive, with the Future General Activity Index up to 21.5, though expectations for future hiring moderated slightly.

- In general, firms revised down their expectations of cost growth for nonlabor inputs in 2025 except for energy from April to July. Labor cost growth was also revised down with wage growth expectations remaining about the same.

The Philadelphia Fed Manufacturing Business Outlook Survey’s General Activity Index was unchanged at -4.0 (vs -1.5 expected) in June, signaling continued contraction in regional factory activity.

- New Orders fell -5.2 pts to 2.3, while Shipments rose 21.3 pts to 8.3, its first positive reading since March.

- Employment dropped sharply, with the index falling -26.3 pts to -9.8, its lowest since May 2020. The Average Workweek index saw a smaller drop, slipping to -1.6 from 2.0 previously.

- Prices Paid fell -18.4 pts to 41.4, and the Prices Received index dropped -14.1 pts to 29.5, both still elevated but moderating.

- The Future Activity Index dropped -28.9 pts to 18.3, indicating less confidence in six-month growth; future new orders and shipments also declined.

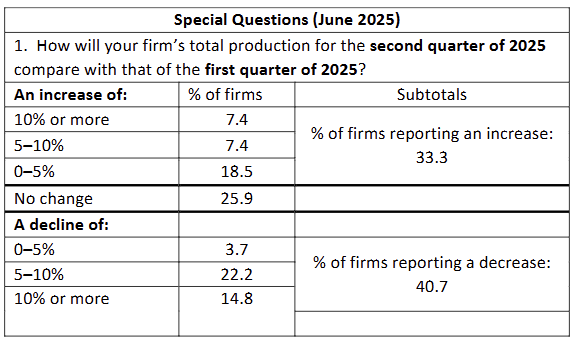

- In special questions, 40.7% of firms reported a drop in Q2 production vs Q1, and most firms continued operating at 70–80% capacity. Labor supply and uncertainty were cited as key constraints.