Philadelphia Fed Manufacturing Business Outlook Survey: January 2026

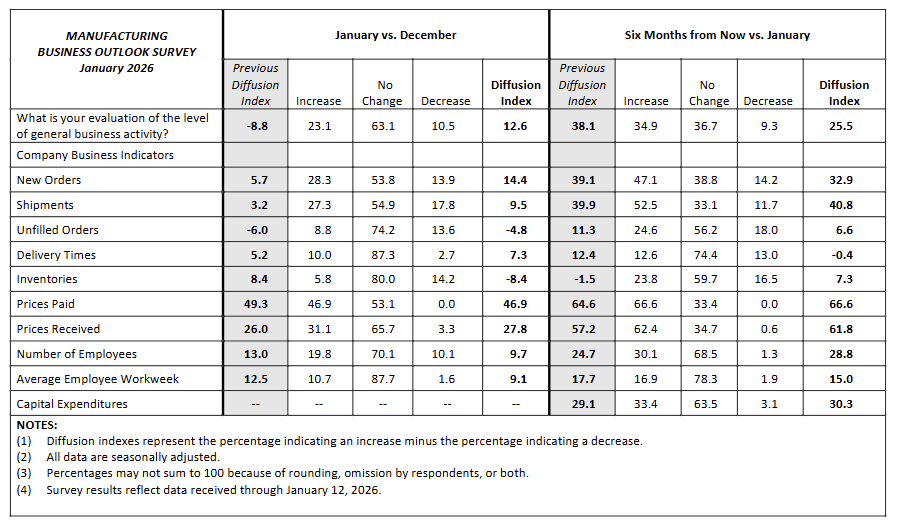

Manufacturing activity improved in January, with the general activity index jumping +21.4 pts to 12.6 and turning positive, alongside firmer demand and shipment growth.

-

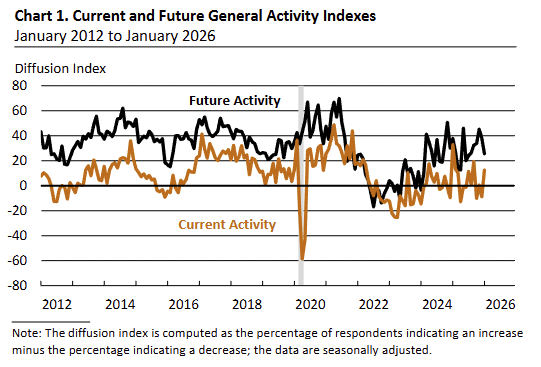

The diffusion index for current general activity rose to 12.6 in January (from -8.8 in December), the highest reading since September, with 23.1% of firms reporting increases vs 10.5% reporting decreases (63.1% no change).

-

Demand indicators strengthened: the current new orders index increased +8.7 pts to 14.4, and the current shipments index rose +6.3 pts to 9.5, signaling broader improvement in near-term activity.

-

Inventories moved lower, with the inventories index falling -16.8 pts to -8.4 (lowest since July 2024), indicating more firms reported inventory declines than builds.

-

Employment conditions remained positive but cooled slightly, with the number of employees index down -3.3 pts to 9.7; nearly 19.8% reported higher employment vs 10.1% reporting declines (70.1% unchanged).

-

The average workweek index declined from 12.5 to 9.1, suggesting a slower pace of hours growth even as the survey still pointed to expansion.

-

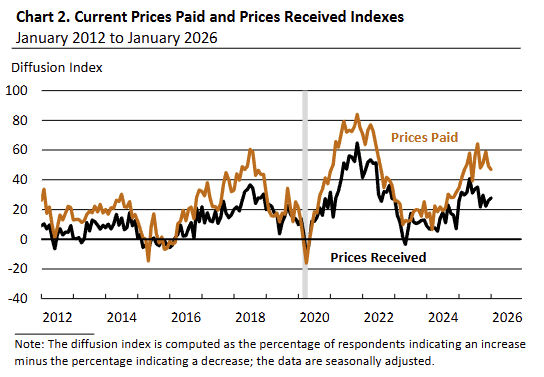

Price pressures stayed elevated: prices paid edged down -2.4 pts to 46.9 (second consecutive decline, lowest since June), while prices received ticked up +1.8 pts to 27.8, indicating ongoing input inflation with continued (but uneven) selling-price increases.

-

Forward-looking activity expectations softened but remained expansionary, with the future general activity index falling from 38.1 to 25.5 (lowest since July); future new orders slipped to 32.9 (-6.2 pts) while future shipments increasedIse edged up to 40.8 (+0.9 pt).

-

Firms continued to anticipate inflationary pressure ahead, with future prices paid at 66.6 and future prices received at 61.8, and the future capital expenditures index edging up to 30.3 (+1.2 pts), signaling modest capex plans.