Philadelphia Fed Manufacturing Business Outlook Survey: November 2025

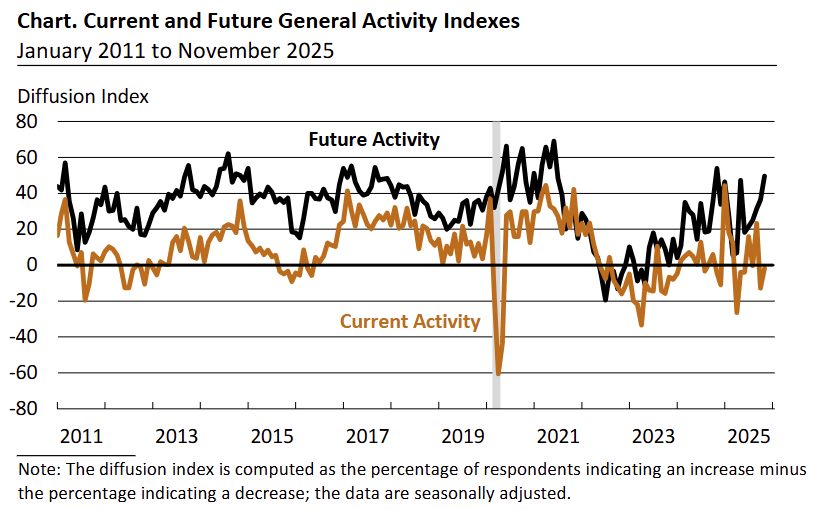

The Philadelphia Fed’s Manufacturing Business Outlook Survey showed the General Activity Index rising +11.1 pts to -1.7 in November, still negative and reflecting ongoing softness in regional manufacturing.

-

New Orders fell -27 pts to -8.6, the lowest since April, indicating a notable pullback in demand after last month’s positive reading.

-

Shipments dropped -15 pts to -8.7, the first negative print since May, signaling weaker output momentum.

-

Employment ticked up to 6.0 (+1 pt), with most firms reporting unchanged staffing, suggesting modest net hiring despite softer activity.

-

The Average Workweek Index fell sharply to 3.7 (from 12.8), implying a reduction in hours worked even as employment increased.

-

Prices Paid rose to 56.1 (+7 pts), remaining well above the long-run average and showing continued input cost pressures.

-

Prices Received declined to 17.7 (-9 pts), more than reversing last month’s gain and indicating softer pricing power.

-

The Future General Activity Index jumped to 49.6 (+13.4 pts), its strongest in a year, with firms expecting better orders, shipments, and continued price increases over the next six months.