Philadelphia Fed Manufacturing Business Outlook Survey: December 2025

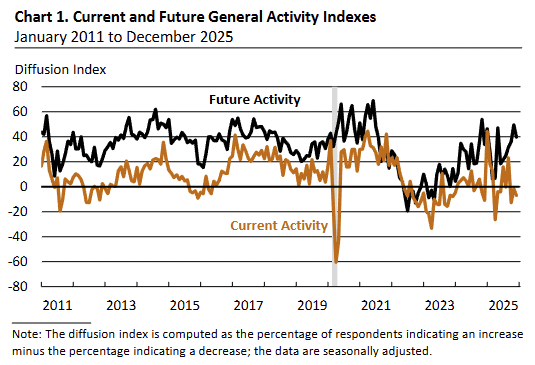

Manufacturing activity weakened in December, with the general activity index falling further into negative territory, reflecting continued softness despite improvements in some demand indicators.

-

The General Activity Index declined to -10.2 in December (from -1.7 in November), its third consecutive negative reading, as fewer firms reported increases and a larger share reported no change.

-

New orders turned positive, with the index rising to 5.0 (from -8.6), indicating a modest rebound in demand after last month’s contraction.

-

Shipments also moved back into positive territory at 3.2 (from -8.7), suggesting a partial recovery in output flows.

-

The employment index increased to 12.9 (from 6.0), its highest level since May, with most firms reporting unchanged headcounts but more increases than decreases.

-

The average workweek index rose to 14.7 (from 3.7), pointing to longer hours alongside reported gains in employment.

-

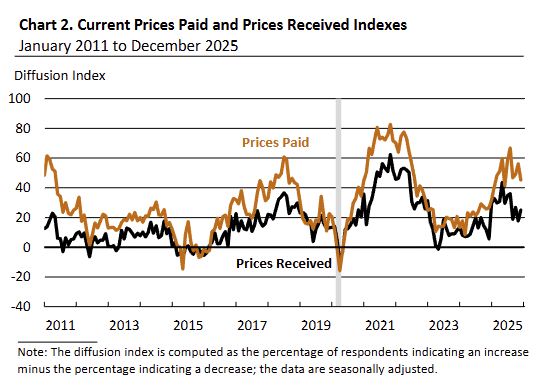

Input cost pressures eased, as the prices paid index fell to 43.6 (from 56.1), its lowest reading since June, though it remained elevated.

-

Pricing power improved modestly, with the prices received index rising to 24.3 (from 17.7), largely reversing the prior month’s decline.