Atlanta Fed Business Inflation Expectations

About

-

July 22nd, 2026 · 11:00 AM

-

August 19th, 2026 · 11:00 AM

-

September 23rd, 2026 · 11:00 AM

-

October 21st, 2026 · 11:00 AM

-

November 18th, 2026 · 11:00 AM

-

December 23rd, 2026 · 11:00 AM

Latest Releases

12

According to the Atlanta Fed, firms’ year-ahead unit cost expectations declined to 1.9% in February, continuing a gradual normalization in cost outlook.

-

Year-ahead unit cost expectations fell to 1.9% in February (from a 3.8% peak in Apr 2022) but remained slightly above the 2017–19 average of 2.0%, indicating easing yet still elevated expectations.

-

Unit cost uncertainty declined after peaking in July, suggesting reduced dispersion around firms’ cost outlooks.

-

Year-over-year unit cost growth averaged 2.0%, showing moderation in realized cost pressures compared with earlier periods.

-

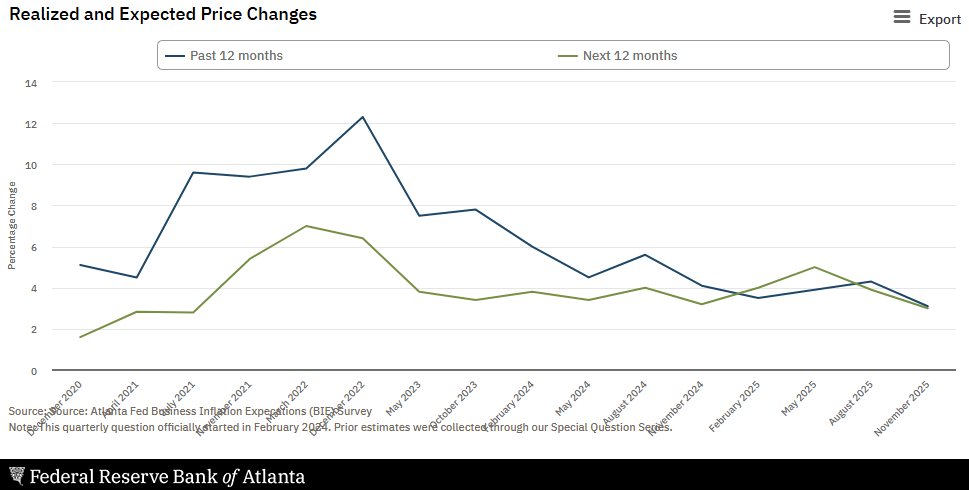

Firms reported a median +3.0% price increase over the past 12 months and expect +3.0% over the next 12 months (means 3.7% and 3.1%), indicating stable pricing behavior.

-

Both realized and expected prices increased relative to November, pointing to slightly firmer pricing dynamics.

-

Sales levels and profit margins compared to normal increased, signaling improved current business conditions.

-

About three-quarters of firms said the One Big Beautiful Bill would have no impact on employment, investment, sales, or profits in 2026, with manufacturing and construction showing the strongest reactions, while retail reported minimal effects.

Firms’ year-ahead unit cost expectations fell to 2.0% in January, returning to the prepandemic average and signaling further easing in expected cost growth.

-

Year-ahead unit cost expectations declined to 2.0% (from 2.2% previously), marking a continued downshift from the 3.8% peak in April 2022 and bringing expectations back to the 2017–19 average.

-

Year-ahead unit cost uncertainty has eased since peaking in July, indicating reduced dispersion around firms’ cost outlooks.

-

Firms’ sales levels increased compared with October 2025, driven by gains in medium firms (+0.6 ppt) and large firms (+2.8 ppt), while small firms saw a slight decline (-0.5 ppt).

-

Roughly two-thirds of firms reported having active job openings they are trying to fill, described as the lowest share since the postpandemic job market expansion.

-

Most firms reported the labor market is about the same as 12 months ago, consistent with a general view of stabilization rather than renewed tightening or loosening.

-

Among firms with job openings, most vacancies were attributed to normal turnover, while roughly one-third were tied to expansion efforts, indicating hiring demand remains partly growth-driven.

-

Small firms were closer to evenly split between turnover and expansion-driven openings, while about 70% of medium and large firms’ openings were attributed to normal turnover, pointing to more replacement hiring among larger employers.

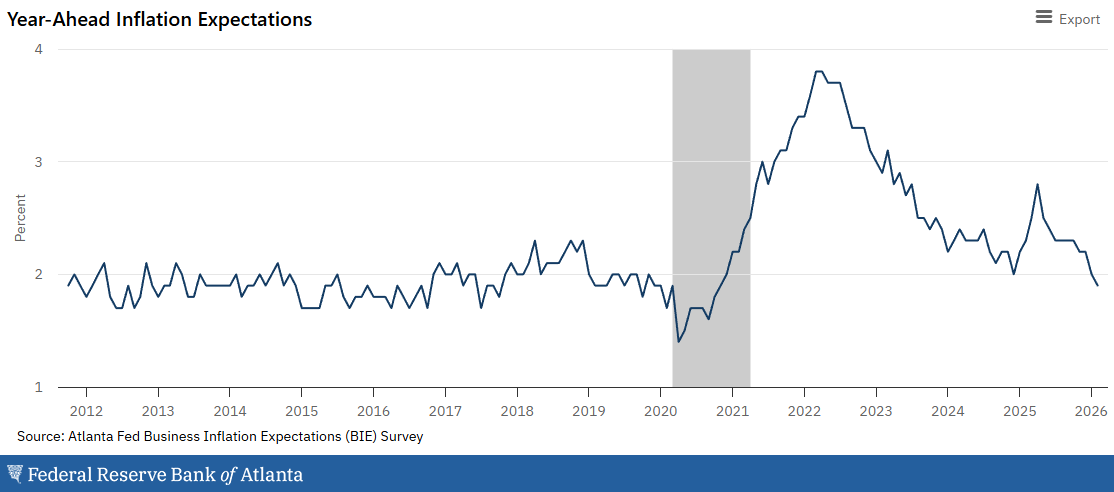

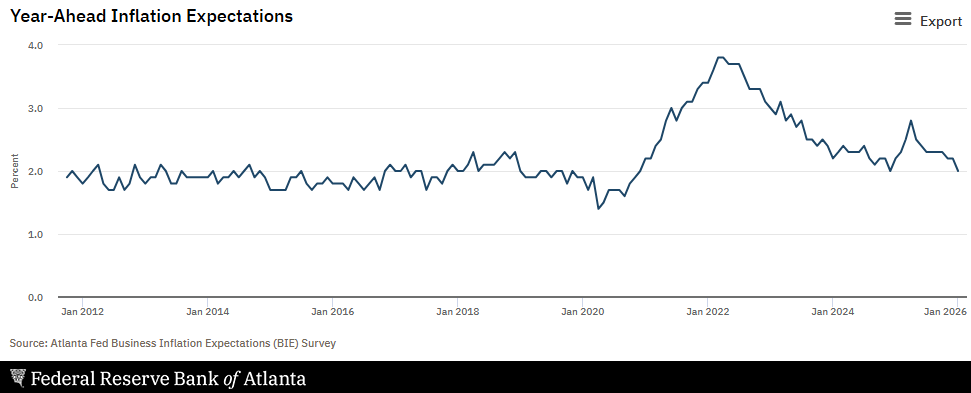

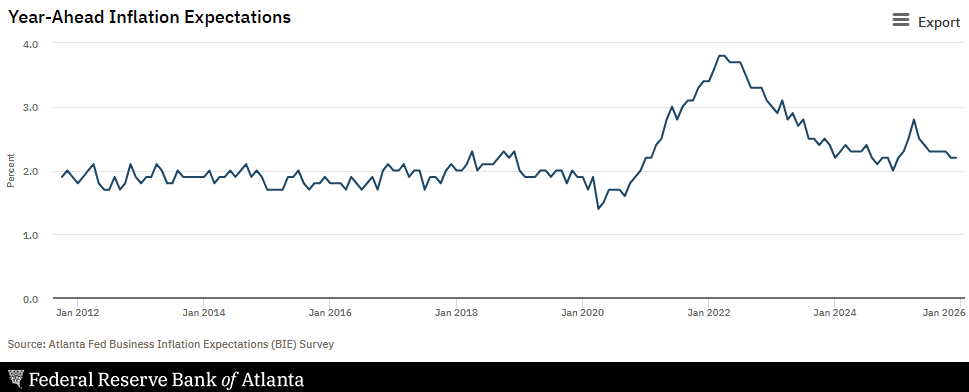

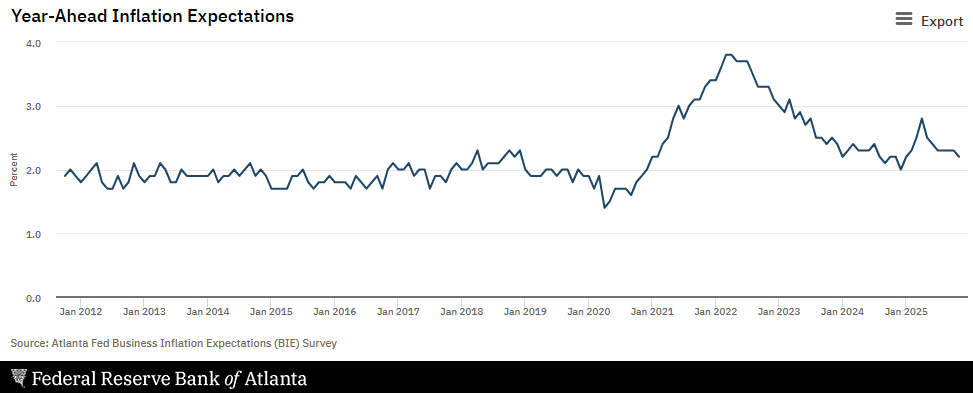

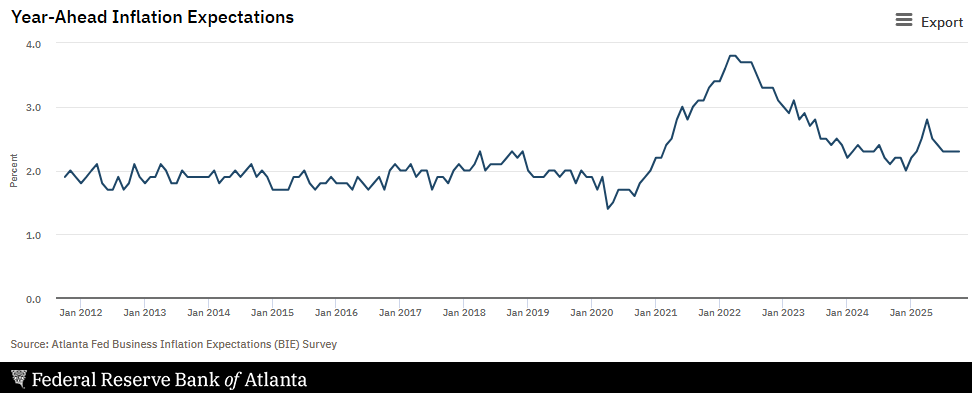

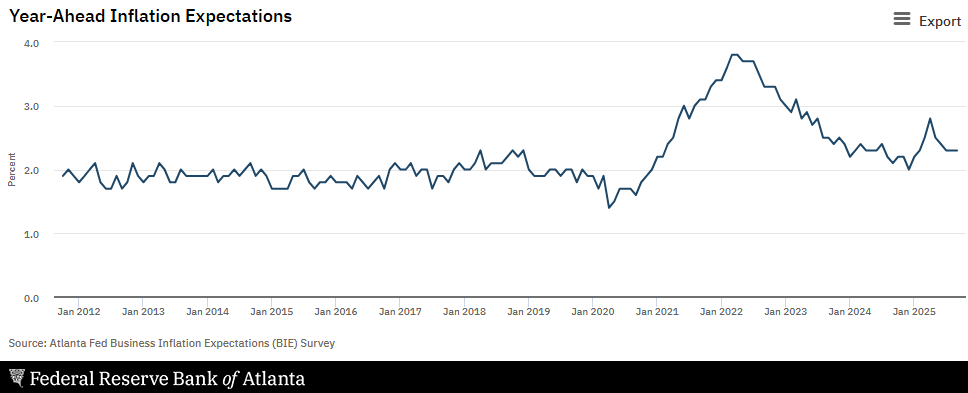

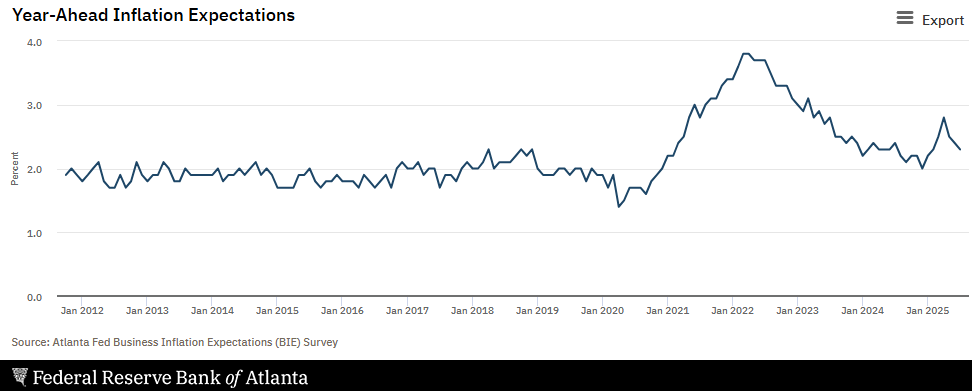

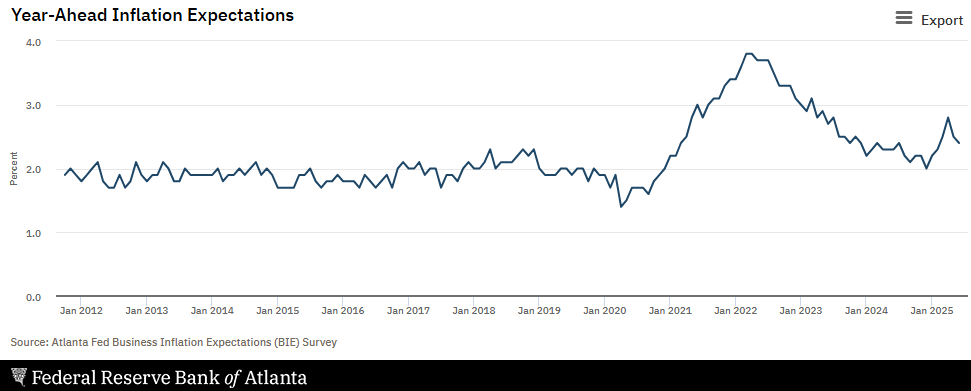

The Atlanta Fed Business Inflation Expectations Survey found firms’ year-ahead inflation and unit cost expectations held at 2.2% in December, remaining at the lowest level since January.

-

Year-ahead unit cost expectations remained unchanged at 2.2%, staying well below the April 2022 peak of 3.8% but still slightly above the 2.0% prepandemic average.

-

Firms’ year-ahead unit cost uncertainty declined further after peaking in July, indicating reduced dispersion around cost expectations.

-

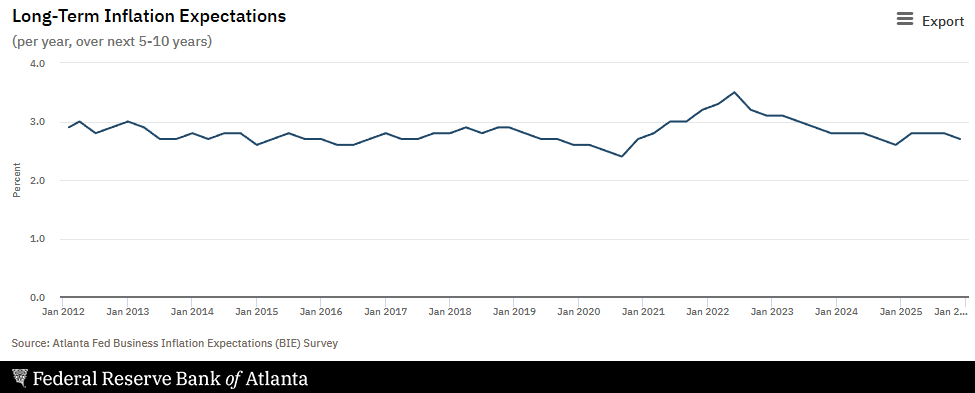

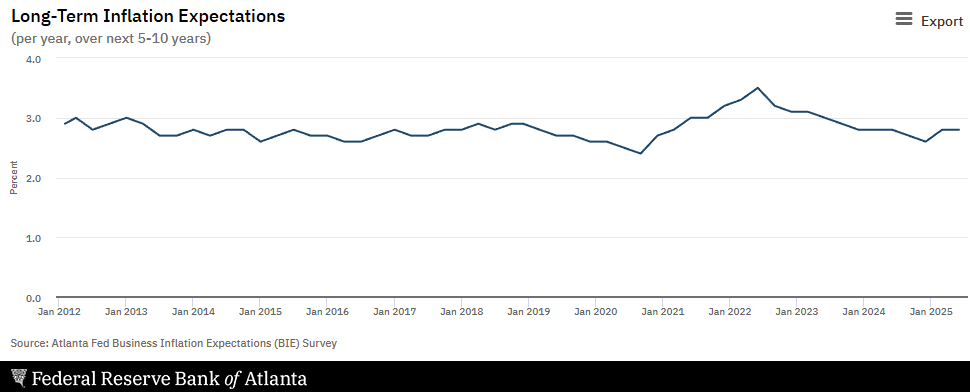

Long-run (five to ten year-ahead) unit cost expectations edged down from 2.7% in September 2025, pointing to a softer longer-term cost outlook.

-

Year-over-year unit cost growth rose to 2.4%, suggesting a modest pickup in realized cost pressures relative to prior readings.

-

Firms reported improvements in sales levels and profit margins “compared to normal,” indicating slightly better current business conditions.

-

Special-question results showed firms were equally confident in expectations for average prices and core product prices, though responses differed when costs rose sharply due to labor-driven increases.

Business inflation expectations declined to 2.2% in November (from 2.3% in October), marking the lowest reading since January 2025 and signaling further easing in firms’ price outlooks.

-

Year-over-year unit cost growth fell to 2.3% (down from 2.4% previously), indicating slightly slower realized cost pressures compared with prior months.

-

Firms reported a median 3.0% price increase over the past 12 months and a median 3.0% expected price increase over the next 12 months, with both realized and expected price growth edging lower from August.

-

Year-ahead unit cost expectations decreased to 2.2%, continuing a notable decline from the 3.8% peak in April 2022, though still somewhat above the 2.0% prepandemic average.

-

Sales levels and profit margins “compared to normal” improved, suggesting slightly better business conditions.

-

Firms’ unit cost uncertainty continued to ease, reflecting greater clarity around cost trends relative to midyear.

-

Special-question results showed that productivity concerns were a primary reason dismissals were not classified as temporary, and smaller firms were more likely than larger firms to use temporary dismissals.

Business inflation expectations held steady at 2.3% in October 2025, marking the fourth consecutive month of stability and reflecting continued moderation in firms’ price outlooks.

-

Firms’ year-ahead inflation expectations remained unchanged at 2.3%, consistent with recent readings since July.

-

Year-over-year unit cost growth edged up slightly to 2.4%, continuing a stable range observed through Q2.

-

Sales levels and profit margins “compared to normal” improved, suggesting modest strengthening in business conditions.

-

Sales levels rose across firm sizes, increasing +1.3 ppt for small firms and +4 ppt for medium firms, while large firms reported stable sales.

The Atlanta Fed Business Inflation Expectations survey showed year-ahead unit cost expectations unchanged at 2.3% in September 2025, reflecting stability after a notable decline from the 2022 peak.

-

Year-ahead unit cost expectations remain above the 2017–2019 pre-pandemic average of 2.0%, though uncertainty around these expectations has eased since peaking in July.

-

Long-run unit cost expectations (5–10 years ahead) were steady at 2.8%, showing little change from earlier in 2025.

-

Reported sales levels and profit margins “compared to normal” both declined, suggesting softer business conditions.

-

Year-over-year unit cost growth was stable at 2.3%, indicating no significant change in realized cost pressures.

-

Around half of firms indicated they would raise prices if competitors increased theirs, regardless of context.

-

When competitor pricing was linked to cost increases, about 7 percentage points more firms reported they would also raise prices, highlighting sensitivity to cost-driven dynamics.

The Atlanta Fed Business Inflation Expectations survey showed year-ahead inflation expectations unchanged at 2.3% in August 2025, indicating that firms’ price outlook remains anchored.

-

Sales levels and profit margins “compared to normal” improved, suggesting some recovery in current business conditions.

-

Year-over-year unit cost growth held steady at 2.3%, showing no pick-up in cost pressures.

-

Firms reported a median 4.0% realized price increase over the past 12 months (up from May), but expect a smaller 3.0% price increase over the next 12 months.

-

A special question highlighted that firms continue to rely on a mix of domestic and imported inputs, while reported demand and revenue levels were generally higher than a year earlier.

The Atlanta Fed Business Inflation Expectations measure fell -0.1 ppt to 2.3% in July, the lowest since February 2025.

- Sales levels and profit margins "compared to normal" declined slightly.

- Year-over-year unit cost growth remained steady at 2.3% for the third straight month.

- Large firms reported a -2.4 ppt drop in sales levels QoQ, while sales for small and medium firms were unchanged.

- Firms cited trade policy changes as a factor in 2025 price decisions.

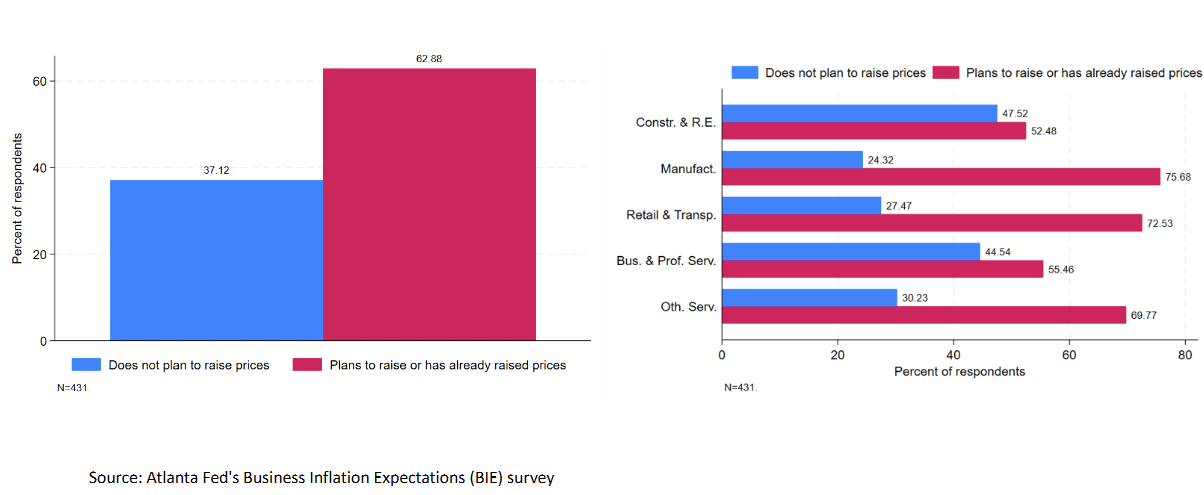

- In our sample around 60 percent of firms have increased prices or plan to do so within the current year. This result holds true across firms of different sizes.

- We see that firms who raised or plan to raise prices feel that their competitors are doing the same thing. The inverse is also true: firms that did not raise and do not plan to raise prices do not expect others in their industry to do so, either.

The Atlanta Fed Business Inflation Expectations measure ticked down -0.1 ppt to 2.4% in June, the lowest since February of this year.

- Sales levels and profit margins "compared to normal" increased with margin rebounding off of a 1.5 year low established in May.

- Year-over-year unit cost growth remained unchanged at 2.3%.

- Firms’ long-run (5-10 years ahead) unit cost expectations remained relatively unchanged from March 2025 at 2.8%.