NY Fed Empire State Manufacturing Survey

About

-

July 15th, 2026 · 8:30 AM

-

August 17th, 2026 · 8:30 AM

-

September 15th, 2026 · 8:30 AM

-

October 15th, 2026 · 8:30 AM

-

November 16th, 2026 · 8:30 AM

-

December 15th, 2026 · 8:30 AM

Latest Releases

12

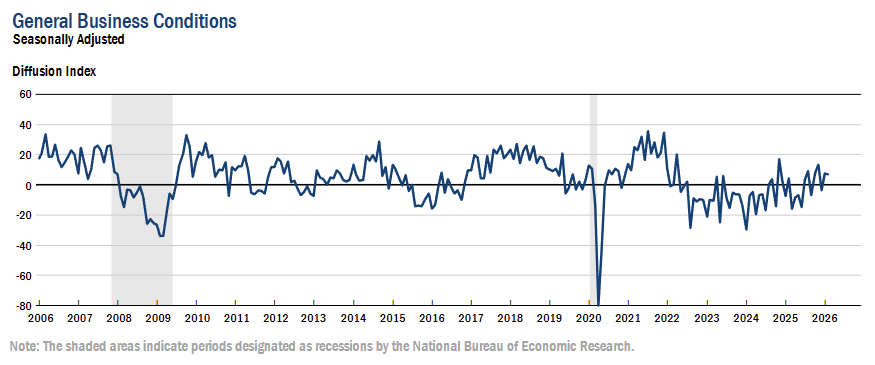

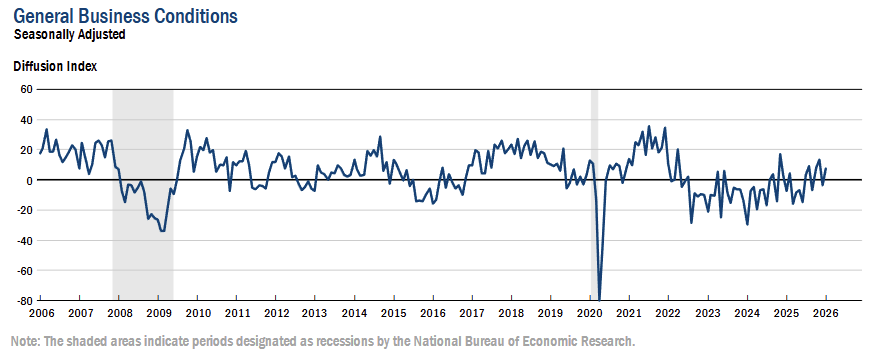

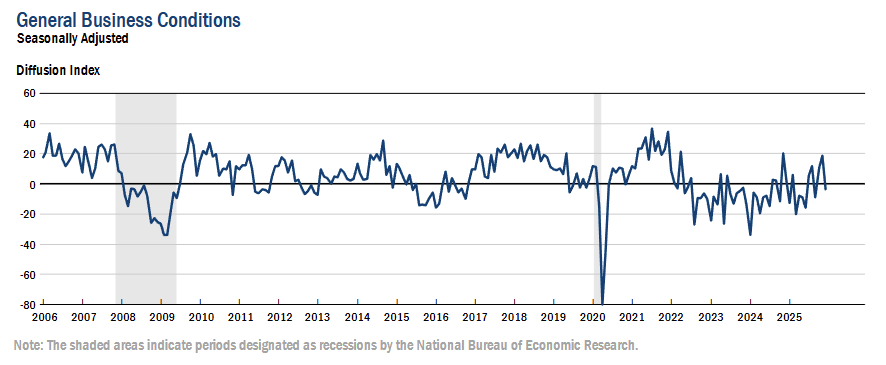

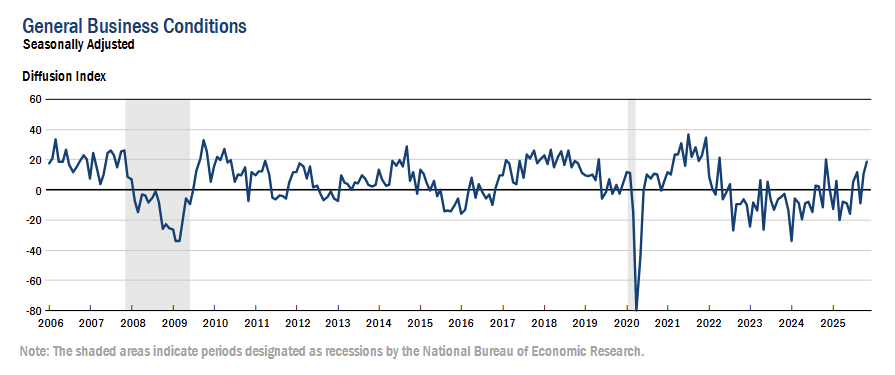

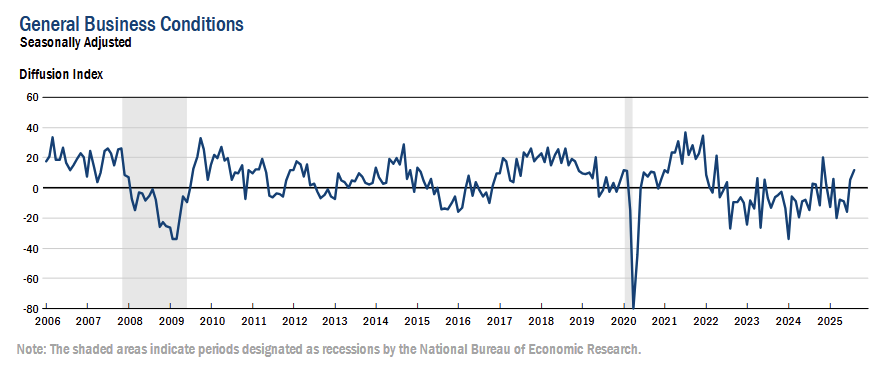

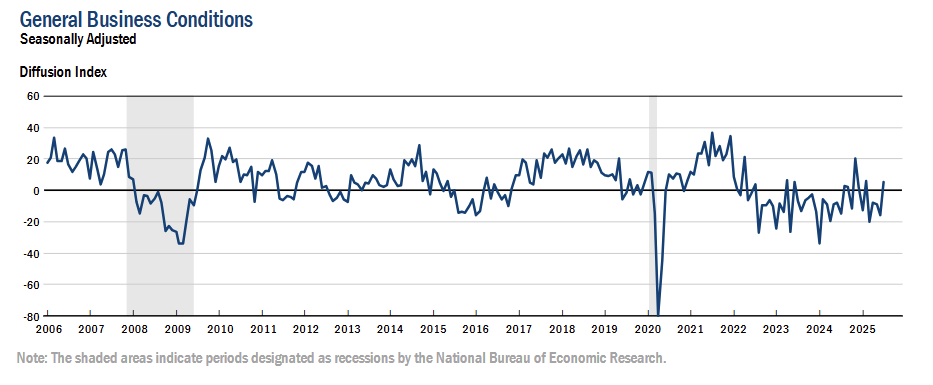

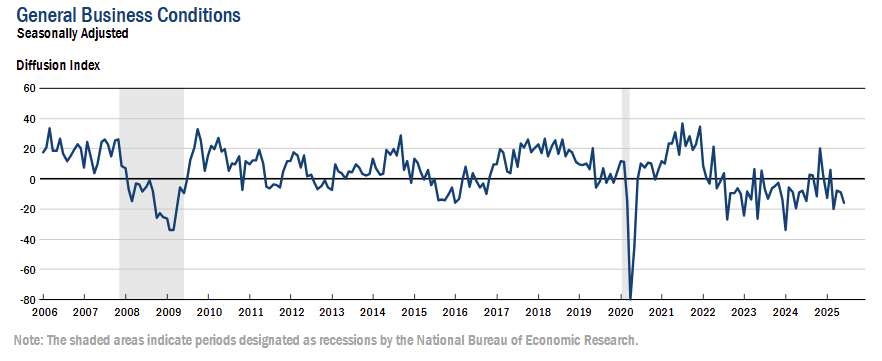

The Empire State Manufacturing Survey showed business conditions at 7.1 in February (unchanged MoM), indicating modest ongoing regional factory expansion.

-

The general business conditions index held at 7.1 (0.0 pts MoM), marking the fourth positive reading in five months and signaling continued modest growth in activity.

-

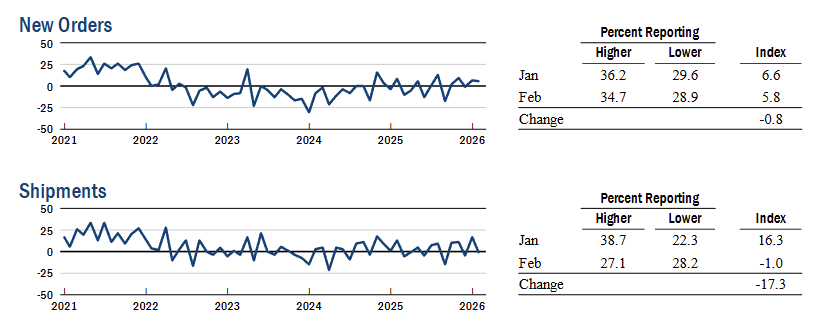

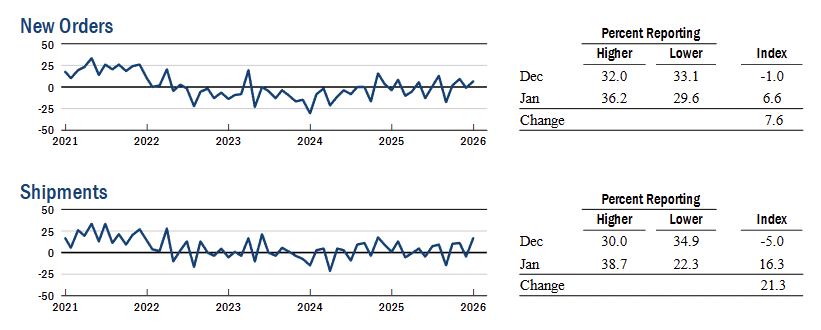

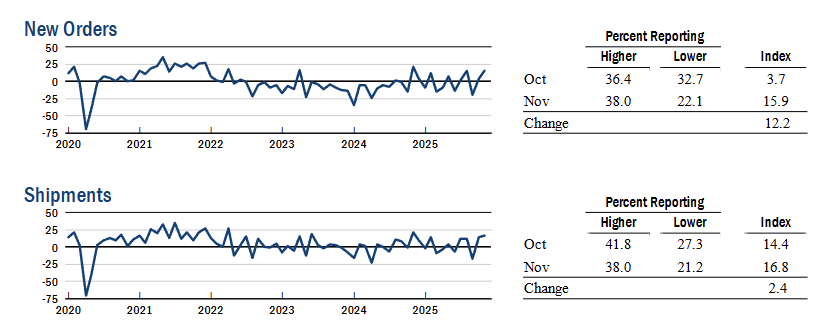

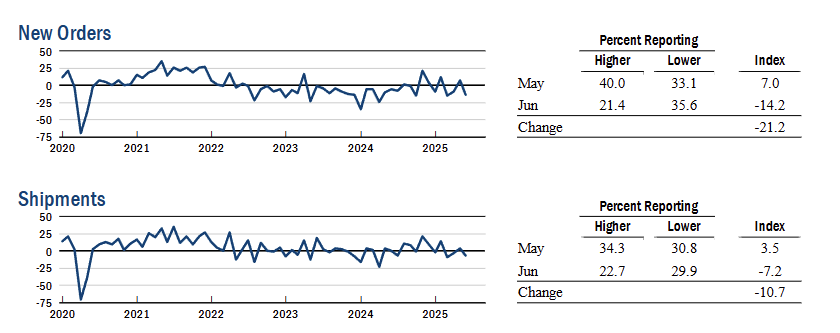

New orders registered 5.8 while shipments fell to -1.0 (-17.3 pts MoM), indicating demand expanded but output flow was essentially flat.

-

Unfilled orders rose to 9.1 (+17.0 pts MoM) and delivery times lengthened slightly, suggesting a growing backlog alongside mild supply frictions.

-

Employment increased to 4.0 (+13 pts MoM) and the average workweek to 2.1 (+8 pts), pointing to a small rebound in labor utilization after the prior month’s decline.

-

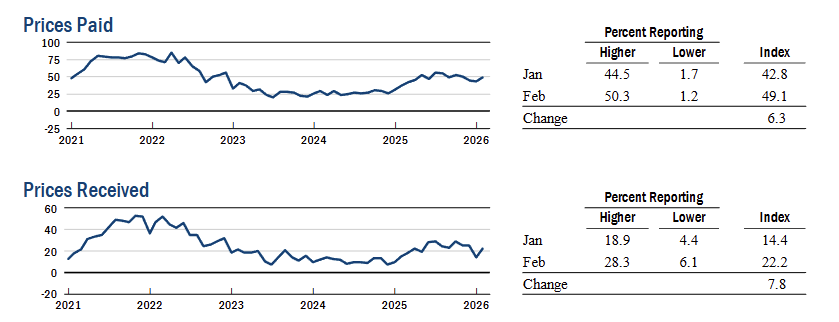

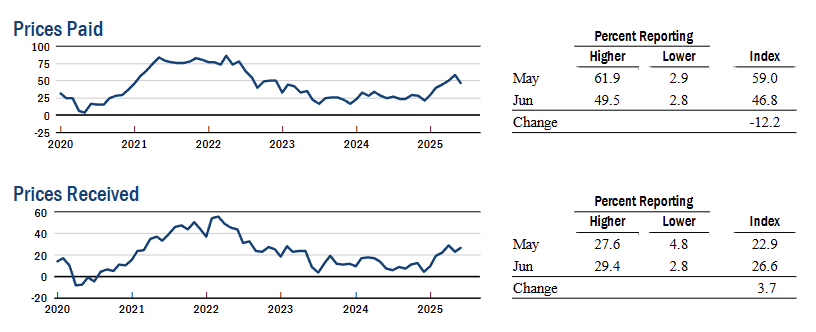

Price pressures strengthened: prices paid rose to 49.1 (+6.3 pts MoM) and prices received to 22.2 (+7.8 pts MoM), indicating faster input and selling price increases.

-

Firms’ outlook improved, with the future business conditions index at 34.7 (+4 pts) and the capital expenditures index at 18.2 (+8 pts, multi year high), showing stronger expectations for activity and investment.

The Empire State Manufacturing Survey showed business activity rising modestly in January, with the headline general business conditions index up +11.4 pts to 7.7 after dipping slightly below zero in December.

-

General business conditions increased to 7.7 (+11 pts), returning the index to positive territory after a small December decline.

-

New orders improved to 6.6 (+8 pts), indicating more firms reported higher demand than lower demand.

-

Shipments climbed to 16.3 (+21 pts), the strongest reading in more than a year, pointing to a solid pickup in output flow.

-

Unfilled orders decreased and inventories edged down, while delivery times were unchanged, consistent with limited supply-chain pressure.

-

Supply availability slipped, with the index at -4.1, suggesting slightly worse availability than the prior month.

-

Employment weakened, with the number of employees index falling -17 pts to -9.0 (lowest in two years) and the average workweek down -8 pts to -5.4, indicating fewer workers and fewer hours worked.

-

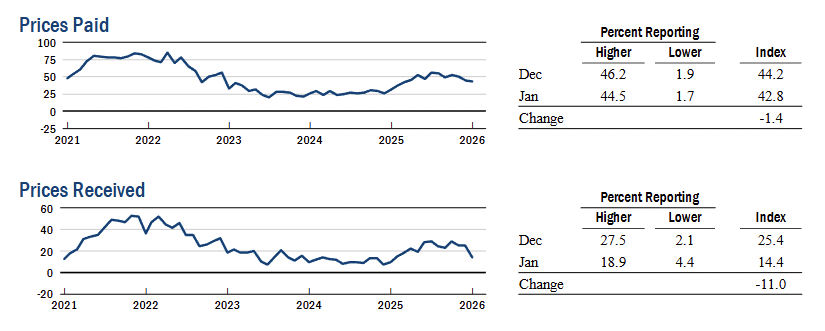

Price pressures were mixed: prices paid held at 42.8 (still elevated), while prices received dropped -11 pts to 14.4 (lowest since Feb 2025), signaling slowing selling price increases.

-

Firms remained optimistic, with the future business conditions index at 30.3 and about half of respondents expecting conditions to improve over the next six months; capital spending plans rose modestly (capex index +3 pts to 10.3).

The Empire State Manufacturing Survey showed activity slipping in December, with the General Business Conditions index falling from 18.7 to -3.9, marking a sharp pullback after November’s surge.

-

General Business Conditions dropped -22.6 pts MoM to -3.9, turning negative after reaching a one-year high in November, indicating slightly weaker overall activity.

-

New Orders held steady, with the index easing -15.9 pts to 0.0, as roughly equal shares of firms reported increases and decreases in demand.

-

Shipments declined modestly, with the index falling -22.5 pts to -5.7, pointing to softer output following recent gains.

-

Inventories increased slightly, with the index at 4.0, suggesting continued stock accumulation despite slower shipments.

-

Delivery Times quickened, with the index at -5.9, and Unfilled Orders fell to -14.9, the lowest since January 2024, indicating faster fulfillment and fewer backlogs.

-

Prices Paid fell -11.4 pts to 37.6 and Prices Received declined -4.2 pts to 19.8, showing moderating but still elevated input and selling price pressures.

-

Employment edged higher, with the Number of Employees index rising to 7.3, while the Average Workweek eased to 3.5, signaling modest job growth with slightly shorter hours.

-

The Future General Business Conditions index rose +17 pts to 35.7, its highest since January, indicating increased optimism for improvement over the next six months.

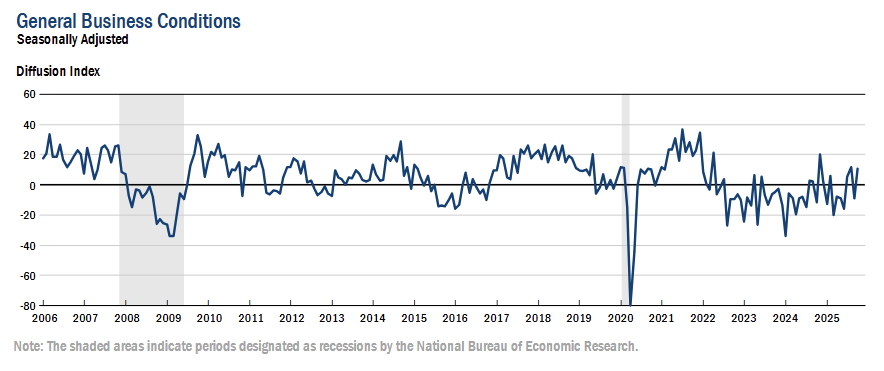

The Empire State Manufacturing Survey showed a solid pickup in activity in November, with the General Business Conditions index rising +8 pts to 18.7, its strongest reading since late last year.

-

New Orders jumped +12.2 pts to 15.9, indicating a clear rebound in demand after a softer October.

-

Shipments increased +2.4 pts to 16.8, pointing to continued gains in output alongside stronger orders.

-

Inventories rose +8.0 pts to 6.7, the first positive reading in several months, suggesting firms are rebuilding stock.

-

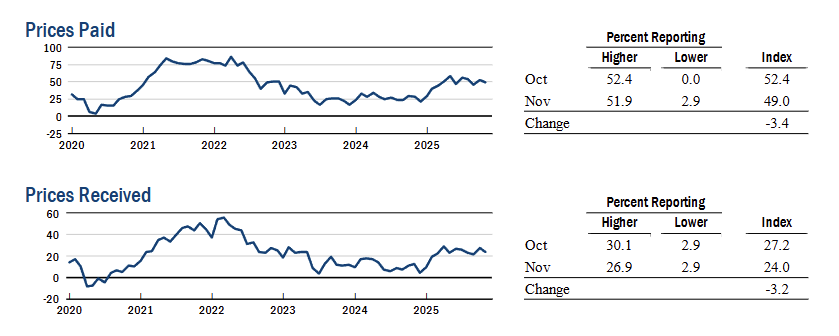

Prices Paid declined -3.4 pts to 49.0, and Prices Received fell -3.2 pts to 24.0, showing slightly slower but still elevated cost and selling price increases.

-

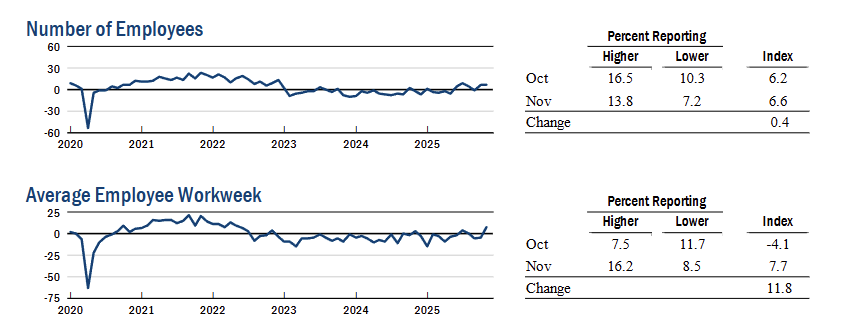

Employment edged up +0.4 pts to 6.6, and the Average Workweek rose +11.8 pts to 7.7, signaling modest hiring and longer hours worked.

-

Delivery Times ticked up and supply availability worsened, consistent with mildly tighter supply conditions.

-

Looking ahead, the Future General Business Conditions index fell to 19.1, indicating firms still expect improvement, though with less optimism than last month.

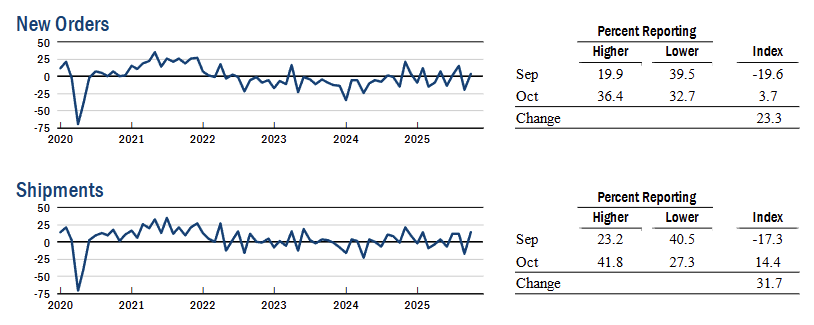

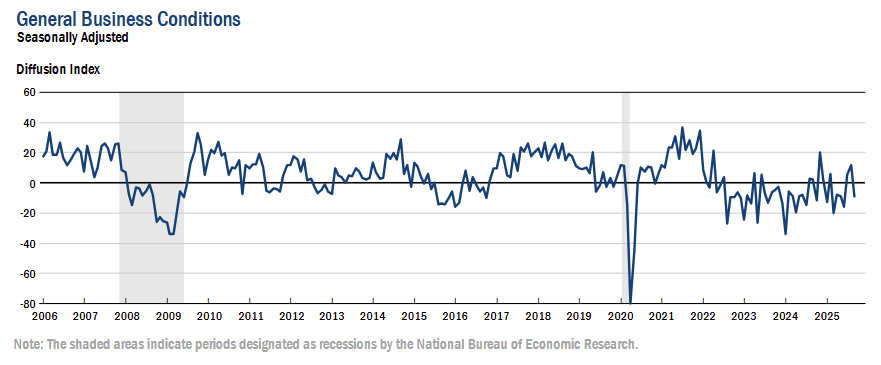

The Empire State Manufacturing Survey reported a modest rebound in business activity in October, with the General Business Conditions index rising +19.4 pts to 10.7, its third positive reading in four months.

-

New Orders recovered sharply, up +23.3 pts to 3.7, indicating a pickup in demand following September’s steep drop.

-

Shipments increased +31.7 pts to 14.4, reflecting a rebound in deliveries after a weak prior month.

-

Employment improved modestly, with the index rising +7.4 pts to 6.2, while the Average Workweek remained negative at -4.1, suggesting slightly shorter hours worked.

-

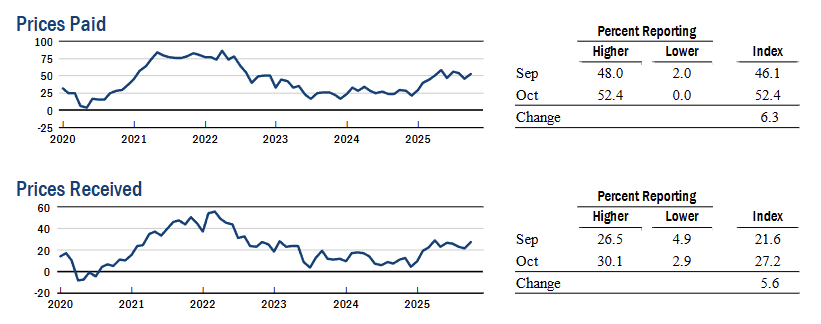

Prices Paid rose +6.3 pts to 52.4, signaling faster growth in input costs, and Prices Received climbed +5.6 pts to 27.2, pointing to stronger selling price gains.

-

Delivery Times lengthened slightly (+3.9), while the Supply Availability Index stayed negative (-10.7), suggesting ongoing supply constraints.

-

Inventories were largely unchanged (-1.0), consistent with stable stock levels.

-

Firms grew more optimistic about future conditions, with nearly half expecting improvement ahead, though capital spending plans remained subdued.

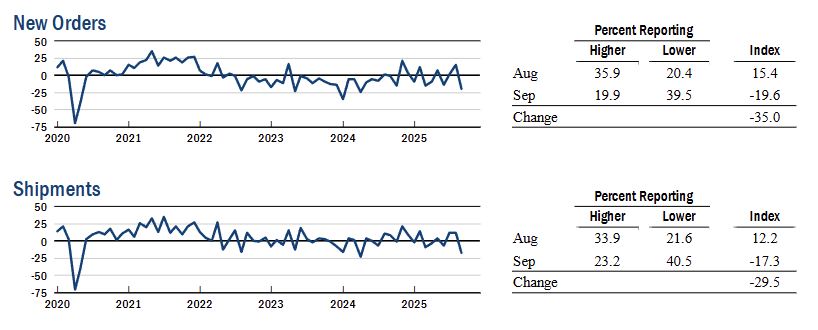

The Empire State Manufacturing Survey’s General Business Conditions index fell -20.6 pts to -8.7 in September, the first negative reading since June, reflecting a sharp pullback in activity.

-

New Orders plunged -35 pts to -19.6, the lowest since April 2024, signaling a significant drop in demand.

-

Shipments dropped -30 pts to -17.3, also the lowest since April 2024, pointing to broad weakness in deliveries.

-

Inventories edged down to -4.9, showing continued modest reductions in stock levels.

-

Supply availability deteriorated further, with the index falling to -8.8, while delivery times were unchanged.

-

Employment was flat around 0, but the Average Workweek declined -5.1, indicating fewer hours worked.

-

Prices Paid fell 8 pts to 46.1, suggesting slower but still elevated input cost pressures, while Prices Received held near 21.6, reflecting moderate selling price increases.

-

The Future General Business Conditions index eased to 14.8, showing firms expect some improvement but with subdued optimism, while the Future Employment index fell near zero, pointing to expectations of flat hiring.

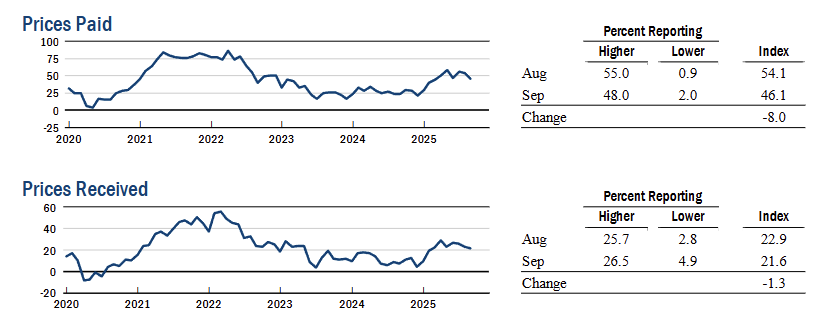

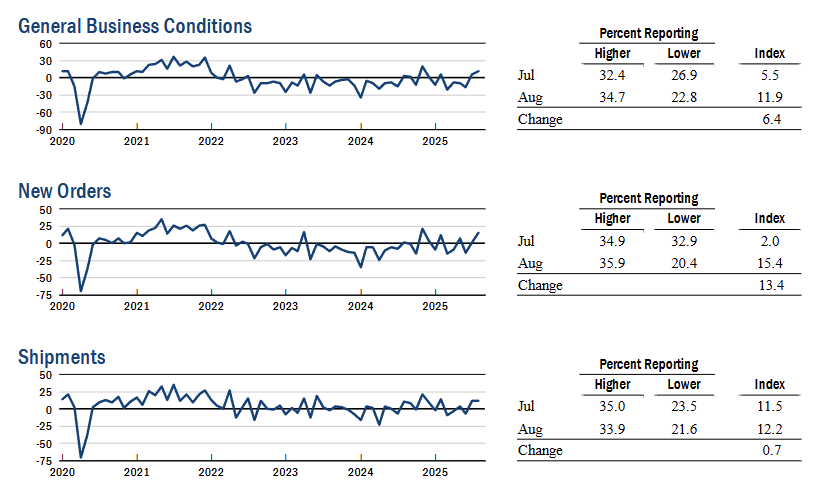

The Empire State Manufacturing Survey’s General Business Conditions index rose 6 pts to 11.9 in August, the highest since November 2024, marking a second consecutive month of expansion.

- New Orders climbed 13.4 pts to 15.4, indicating a solid pickup in demand.

- Shipments held steady at 12.2, pointing to continued growth in deliveries.

- Inventories fell sharply, with the index dropping -22.0 pts to -6.4 after last month’s strong rise.

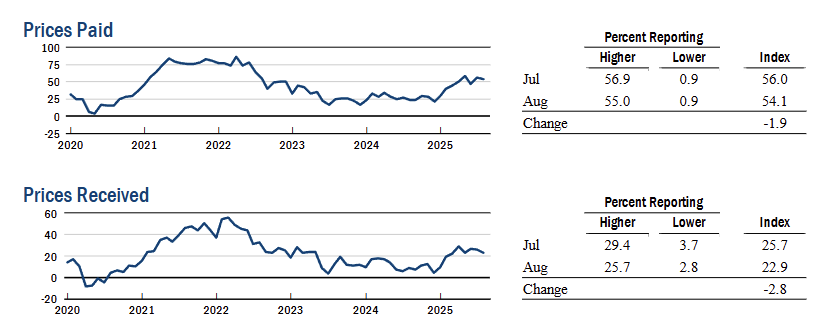

- Prices Paid fell -1.9 pts to 54.1, showing input cost pressures remain steep, while Prices Received eased -2.8 pts to 22.9, indicating more moderate selling price increases.

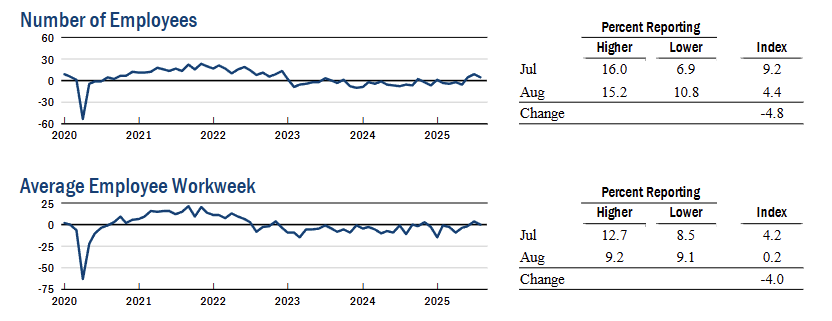

- The Employment index fell -4.8 pts to 4.4, and the Average Employee Workweek index dropped -4.0 pts to 0.2.

- The Future General Business Conditions index fell 8 pts to 16.0, showing firms expect growth ahead but with less optimism than last month.

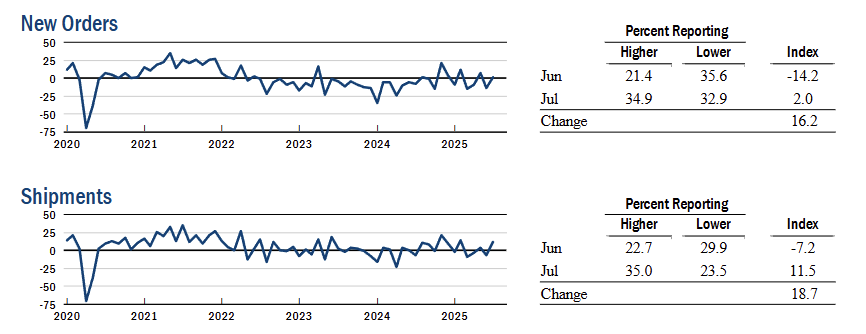

The Empire State Manufacturing Survey’s General Business Conditions index rose 21.5 pts to 5.5 in July, rebounding from -16.0 in June and marking the first positive reading since March.

- New Orders rose 16.2 pts to 2.0 (from -14.2), returning to expansion territory.

- Shipments jumped 18.7 pts to 11.5 (from -7.2), the strongest reading since early 2024.

- The share of firms reporting higher General Business Conditions more than doubled to 32.4% (from 16.9%).

- Despite the improvement, only modest gains were reported across key components, indicating a tentative rebound rather than strong growth.

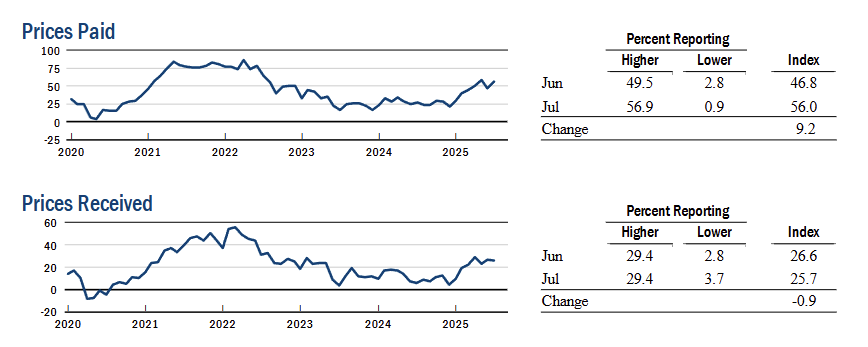

- Prices Received dipped slightly by -0.9 pts to 25.7, while Prices Paid jumped 9.2 pts to 56.0. This divergence points to margin compression in June.

- 56.9% of firms reported paying higher prices, up from 49.5% in June.

- Only 0.9% of firms reported lower input prices, while no change was reported in those receiving higher selling prices (29.4%).

- The Number of Employees index increased 4.5 pts to 9.2, continuing a gradual hiring trend.

The Empire State Manufacturing Survey’s General Business Conditions index fell -6.8 pts to -16.0 in June, the fourth consecutive month of contraction and the lowest since January.

- New Orders dropped -21.2 pts to -14.2, and Shipments fell -10.7 pts to -7.2, both reversing last month’s gains.

- Prices Paid fell -12.2 pts to 46.8, while Prices Received rose 3.7 pts to 26.6, showing a mixed picture for inflation pressures.

- Employment rose for the first time since January, with the index up 9.8 pts to 4.7, while the Average Workweek held nearly flat at -1.5.

- Supply availability remained tight with the index at -8.3, slightly better than May’s -11.4.

- Future General Business Conditions surged 23.2 pts to 21.2, marking the first optimistic outlook since March.