NY Fed Business Leaders Survey

About

-

August 18th, 2026 · 8:30 AM

-

September 16th, 2026 · 8:30 AM

-

October 16th, 2026 · 8:30 AM

-

November 17th, 2026 · 8:30 AM

-

December 16th, 2026 · 8:30 AM

Latest Releases

12

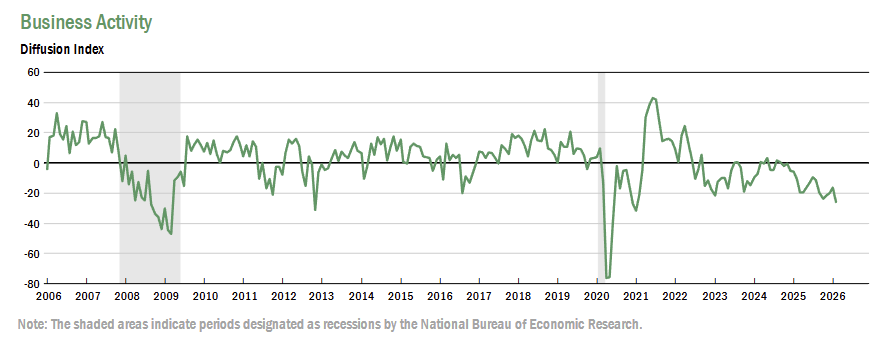

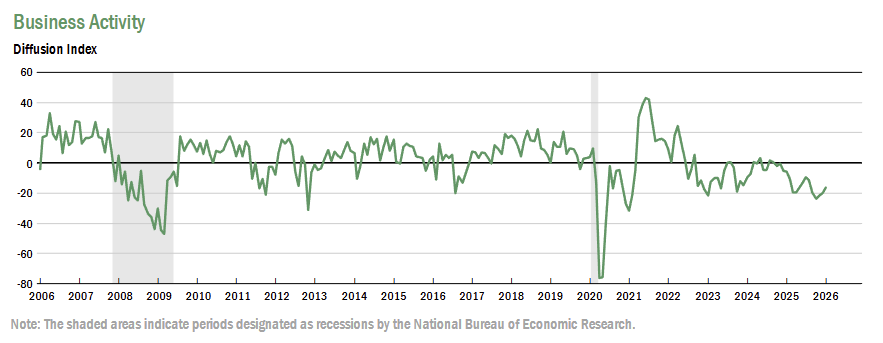

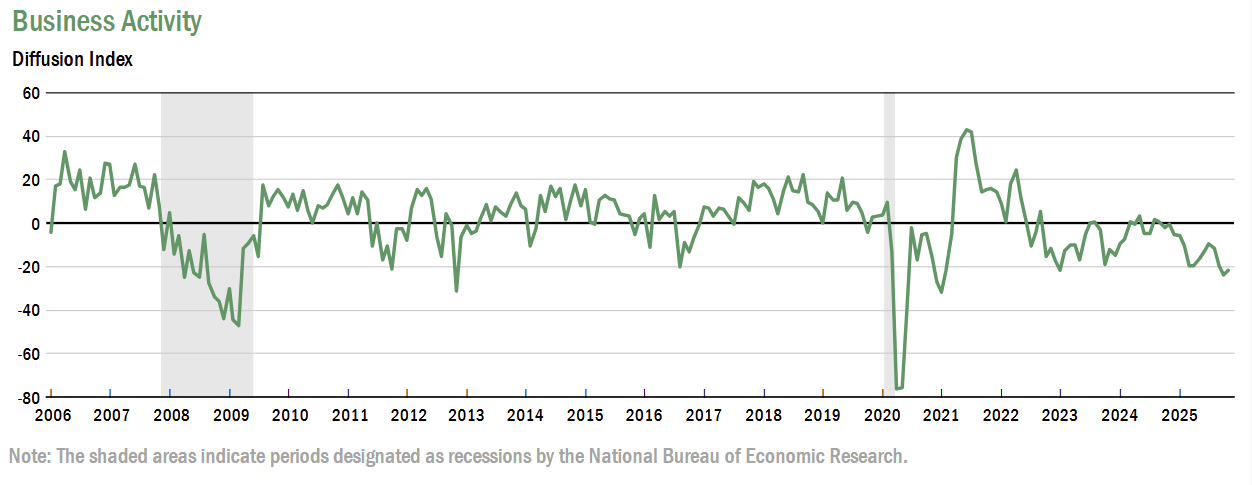

New York service sector activity fell to -25.7 in February (-10 pts MoM), indicating deeper contraction across the region.

-

The Business Activity Index dropped to -25.7 (17% higher vs 43% lower), showing a substantial decline in overall conditions.

-

The Business Climate Index fell to -41.7 (-7 pts), with just over half reporting an unfavorable climate, indicating conditions remained much worse than normal.

-

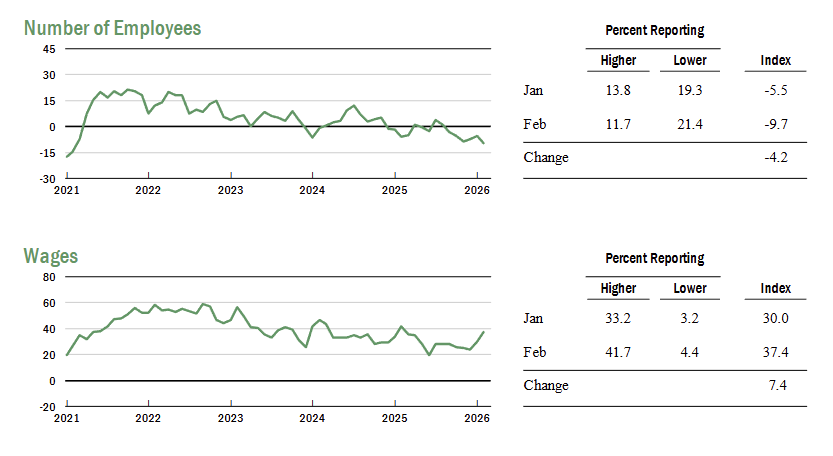

The Employment Index decreased to -9.7 (-4 pts), its sixth straight negative reading, suggesting ongoing job losses.

-

The Wages Index rose to 37.4 (+7 pts), pointing to faster wage growth even as employment declined.

-

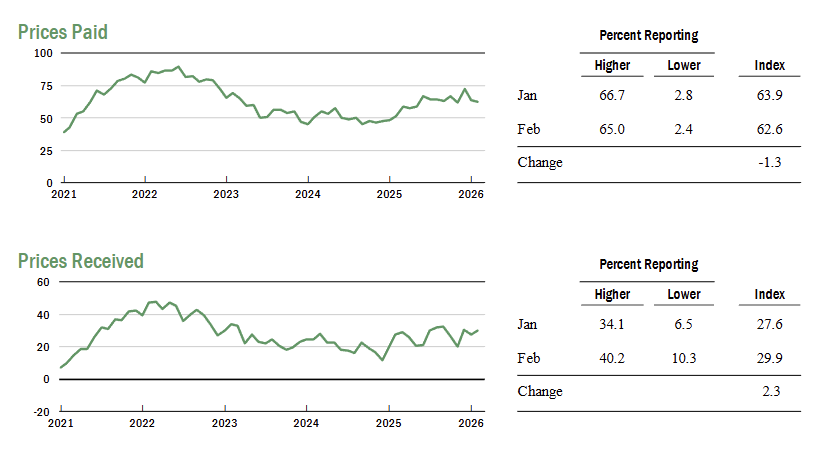

The Prices Paid Index held at 62.6 and Prices Received at 29.9 (both ~0 pts), indicating price pressures remained elevated but stable.

-

The Supply Availability Index fell to -9.2 (-6 pts), showing modest deterioration in supply conditions.

-

The Future Business Activity Index increased to 17.5 (+5 pts), with 40% expecting improvement, signaling modest optimism despite current contraction.

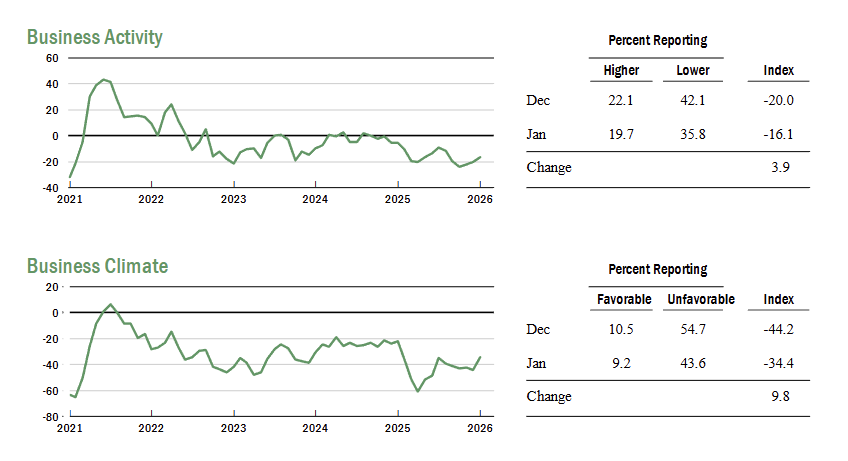

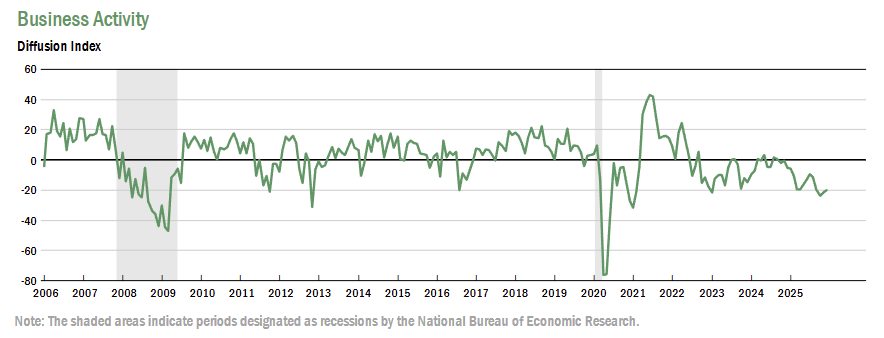

Business activity in the New York–Northern New Jersey service sector remained in contraction in January, with the Business Activity Index improving to -16.1.

-

The Business Activity Index rose to -16.1 in January (up 4 pts), with 20% of firms reporting improved conditions and 36% reporting worsening conditions, indicating contraction persisted despite modest improvement.

-

The Business Climate Index increased 10 pts to -34.4, with 44% reporting an unfavorable business climate, showing conditions remained broadly “worse than normal.”

-

The Employment Index was little changed at -5.5, its fifth consecutive negative reading, suggesting employment continued to decline modestly.

-

The Wages Index rose 6 pts to 30.0, pointing to somewhat faster wage growth, though still described as modest.

-

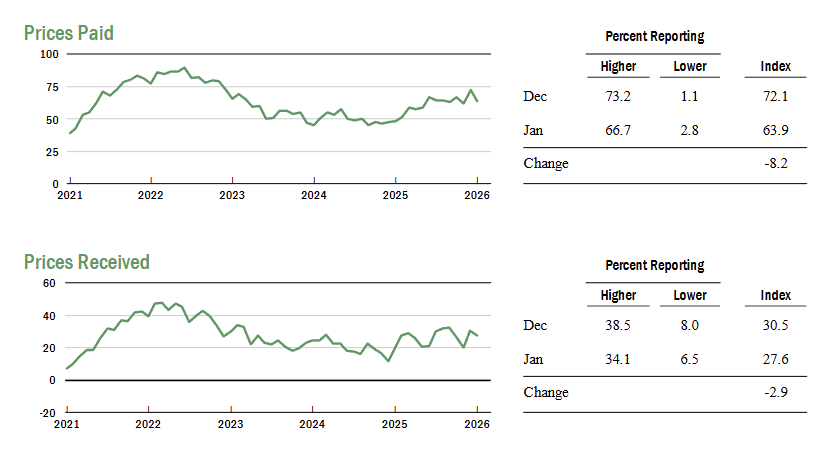

Input price pressures eased, with the Prices Paid Index falling 8 pts to 63.9 after reaching a three-year high in the prior month.

-

Selling price increases slowed slightly, with the Prices Received Index edging down 3 pts to 27.6, indicating reduced pricing momentum.

-

Supply availability was little changed, with the Supply Availability Index at -3.2, suggesting only a slight deterioration.

-

The Future Business Activity Index rose to 12.4 (first positive since July), signaling expectations for only modest improvement over the next six months, while capital spending plans remained soft.

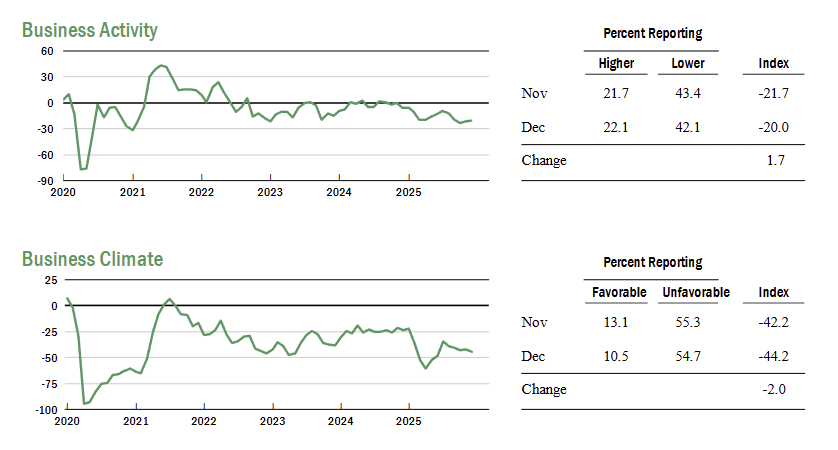

Business activity in the New York–Northern New Jersey service sector remained deeply negative in December, with the headline Business Activity Index unchanged at -20.0, reflecting continued contraction with little month-to-month improvement.

-

The Business Activity Index held at -20.0 in December (Nov: -21.7), with 22% of firms reporting improved conditions and 42% reporting worsening conditions, indicating contraction remained widespread.

-

The Business Climate Index slipped to -44.2 (from -42.2), showing a persistently unfavorable environment, with 55% of respondents describing conditions as worse than normal.

-

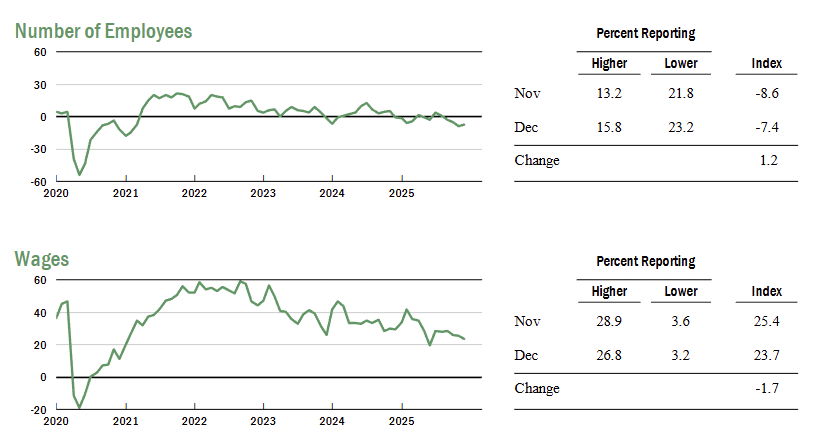

The Employment Index stayed negative at -7.4 (Nov: -8.6), marking a fourth consecutive month of declining employment, though the pace of contraction eased slightly.

-

The Wages Index edged down to 23.7 (from 25.4), suggesting wage growth remained positive but modest amid weak activity.

-

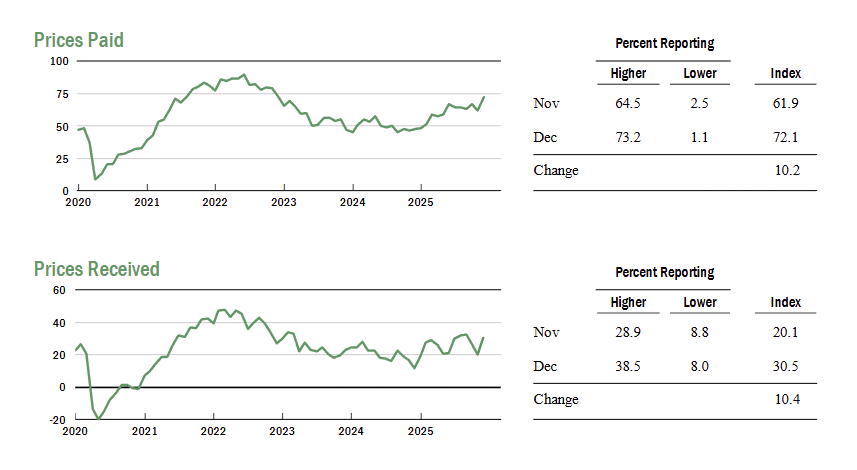

The Prices Paid Index jumped +10.2 pts to 72.1, its highest level in three years, indicating a renewed acceleration in input cost pressures after prior easing.

-

The Prices Received Index rose +10.4 pts to 30.5, pointing to firmer selling price increases following last month’s slowdown.

-

The Future Business Activity Index registered -1.1, showing firms generally did not expect meaningful improvement over the next six months, with only slight anticipated gains in employment and continued softness in capital spending plans.

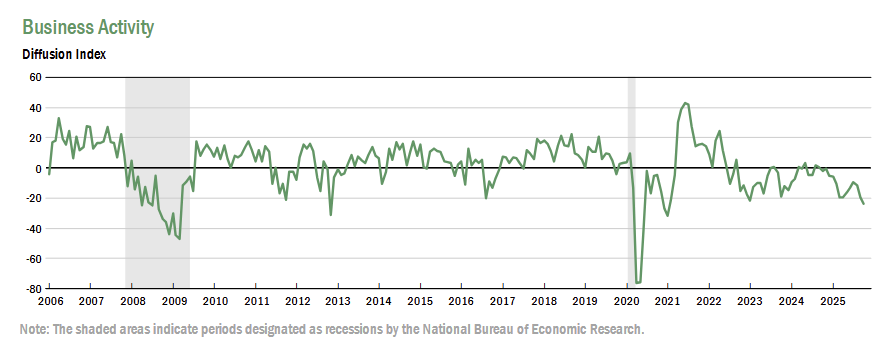

Business activity in the New York–Northern New Jersey service sector declined further in November, with the Business Activity Index edging up +1.9 pts MoM to -21.7, reflecting another month of substantial contraction.

-

The Business Climate Index was nearly unchanged at -42.2 (+0.7 pts MoM), indicating that a majority of firms continued to view conditions as worse than normal.

-

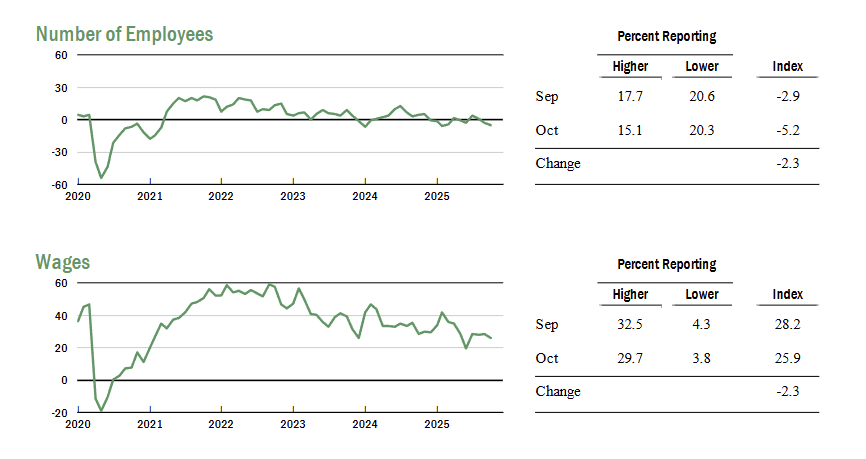

Employment fell for a third month, with the index dropping -3 pts to -8.6, marking a multiyear low and signaling continued job cuts across the region.

-

The Wages Index held steady at 25.4, showing modest but stable wage growth despite broader weakness in activity.

-

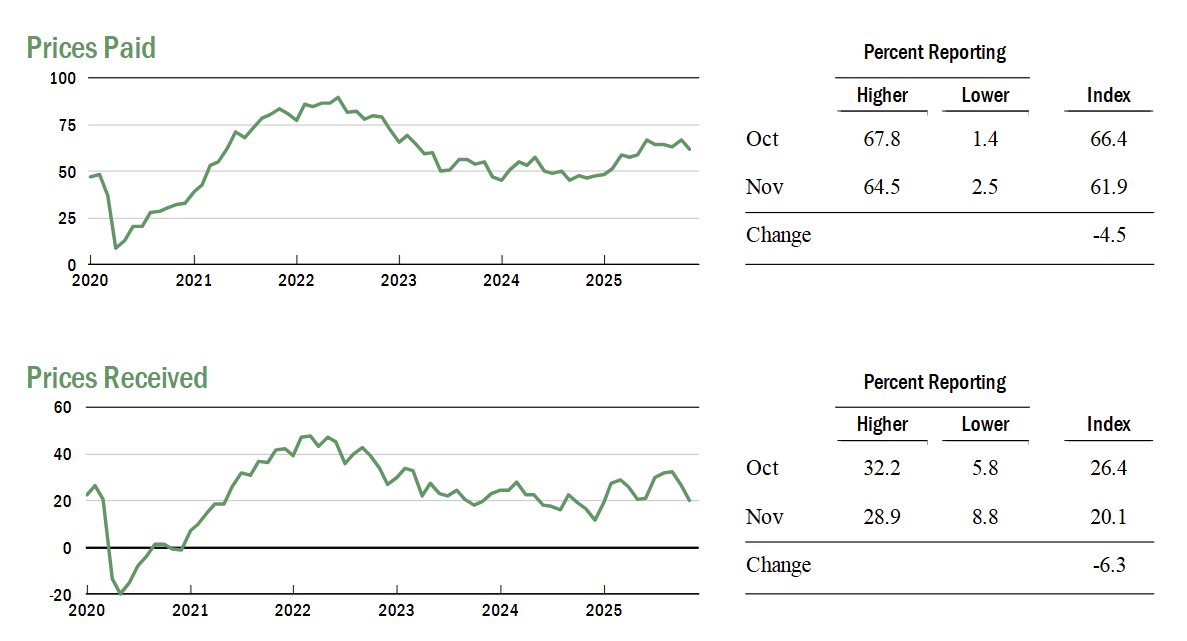

Prices Paid decreased -4.5 pts to 61.9, and Prices Received declined -6.3 pts to 20.1, pointing to slower increases in both input costs and selling prices.

-

The Supply Availability Index remained negative at -11.1, suggesting ongoing deterioration in the availability of inputs.

-

Firms remained cautious about the outlook, with the Future Business Activity Index at -4.6, and expectations for employment and capital spending staying soft.

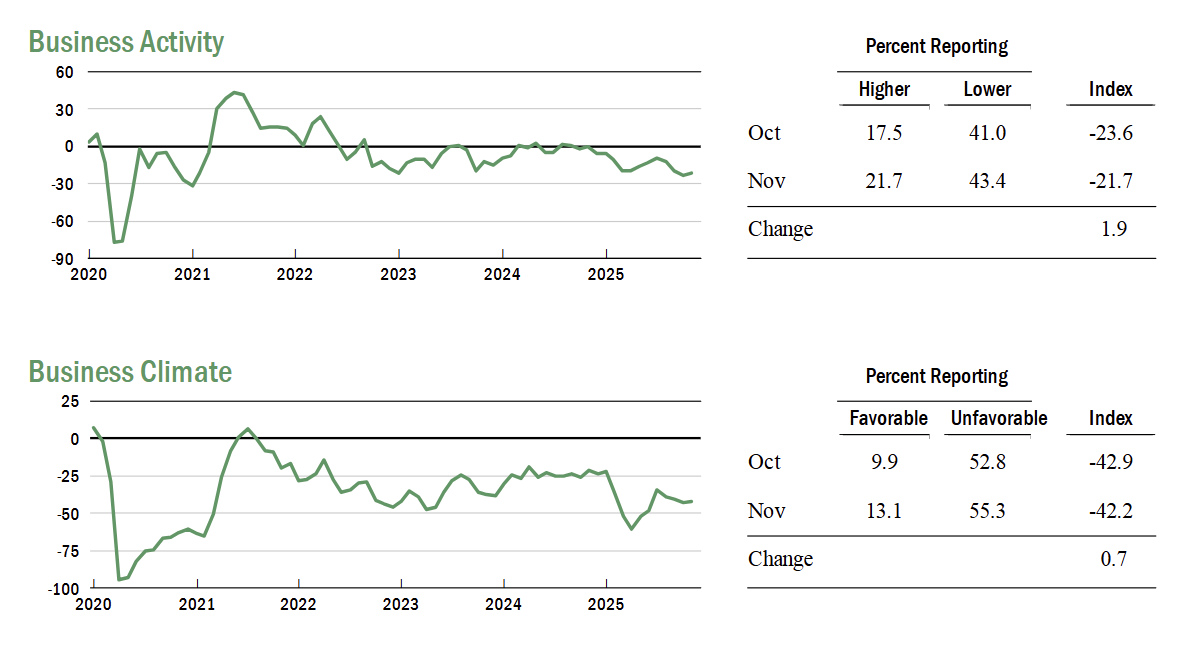

The NY Fed Business Leaders Survey showed a steeper contraction in October, with the Business Activity Index falling -4.2 pts to -23.6, its lowest in several years, underscoring persistent weakness in the regional service sector.

-

The Business Climate Index declined to -42.9 (from -40.7), as 53% of firms reported conditions worse than normal, indicating continued pessimism.

-

Employment softened further, with the index slipping -2.3 pts to -5.2, marking a second straight negative reading and signaling ongoing job losses.

-

The Wages Index edged down to 25.9 (from 28.2), showing modest but slightly slower wage growth compared with September.

-

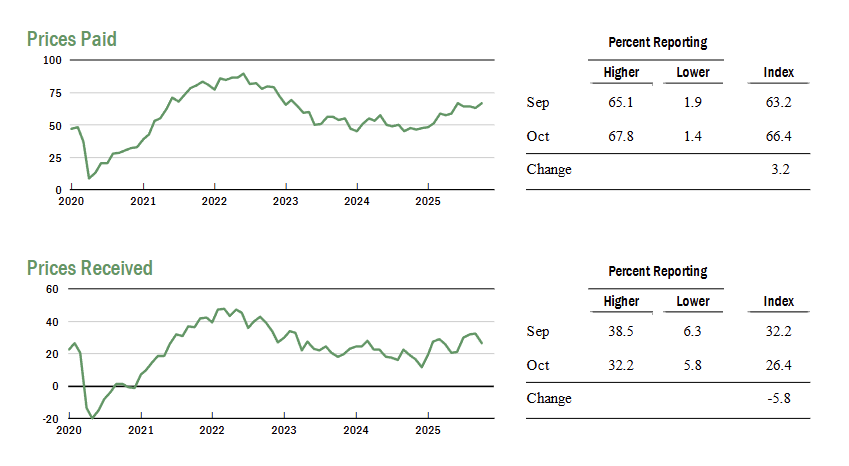

Input cost pressures intensified, as the Prices Paid Index rose to 66.4 (from 63.2), while the Prices Received Index fell -5.8 pts to 26.4, suggesting weaker pricing power.

-

Capital Spending weakened notably, dropping -8.1 pts to -6.7, pointing to a pullback in investment plans.

-

Firms remained downbeat on the outlook, with the Future Business Activity Index at -3.4 and half of respondents expecting the business climate to worsen over the next six months.

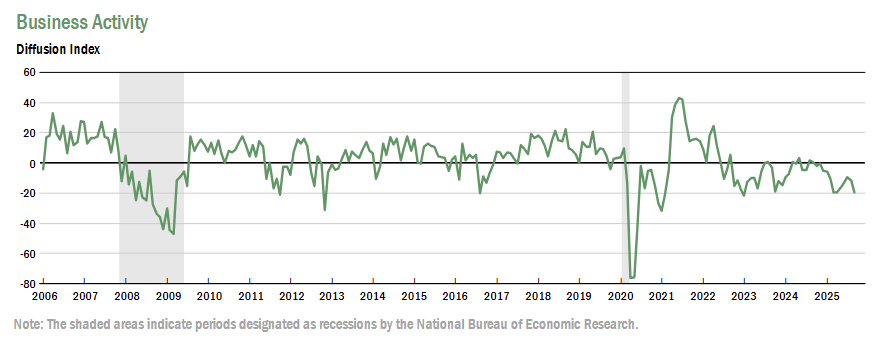

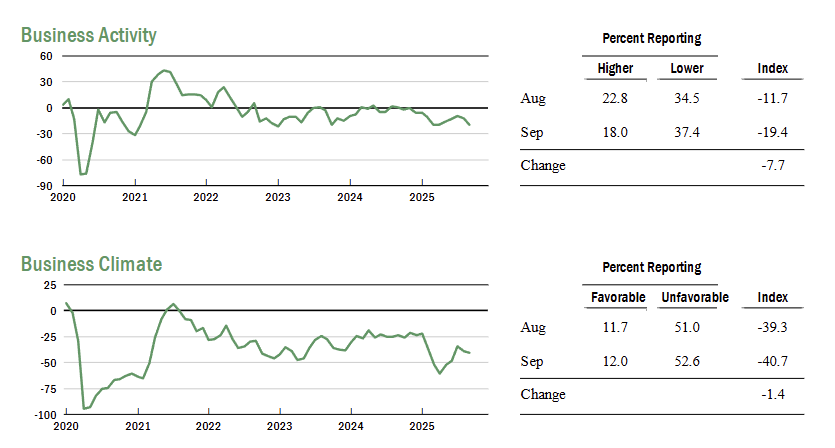

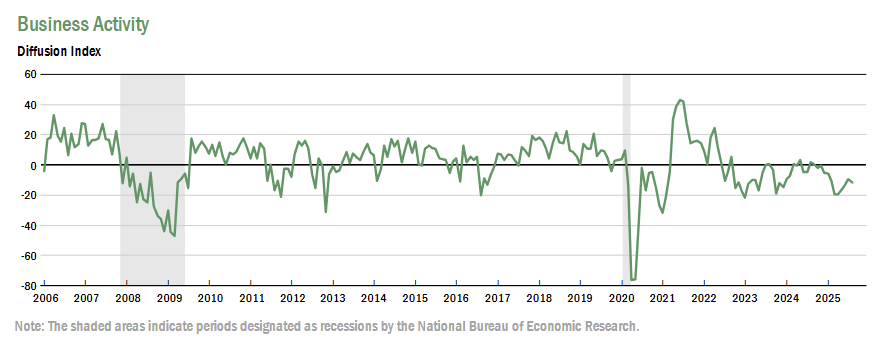

The NY Fed Business Leaders Survey showed a sharp deterioration in September, with the Business Activity Index dropping -7.7 pts to -19.4, its lowest since April, reflecting ongoing weakness in the regional service sector.

-

The Business Climate Index slipped further to -40.7 (from -39.3), with over half of firms reporting conditions worse than normal.

-

Employment edged lower as the index fell -3.9 pts to -2.9, while the Wages Index held steady at 28.2, suggesting wage growth was modest but unchanged.

-

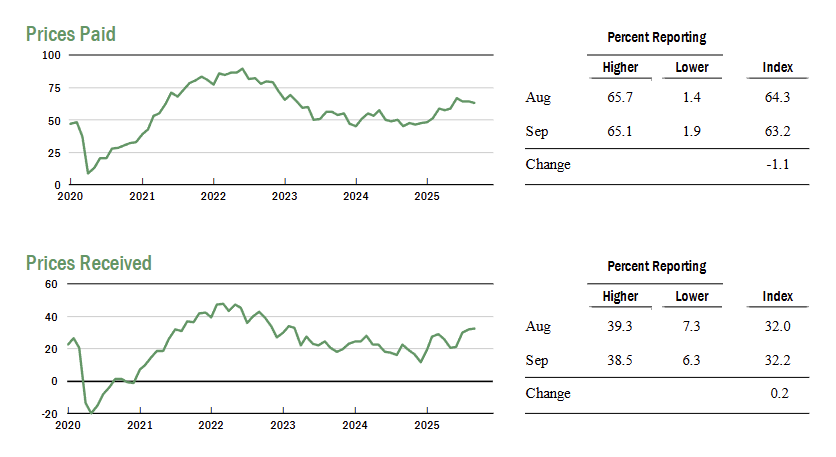

The Prices Paid Index eased slightly to 63.2 (from 64.3) but remained elevated, while the Prices Received Index was stable at 32.2, indicating continued widespread selling price increases.

-

Supply availability worsened, with the index at -9.6, consistent with persistent constraints in inputs.

-

Capital Spending improved to 1.4 (from -2.9), moving back into positive territory but still soft by historical standards.

-

Firms’ expectations stayed negative, with the Future Business Activity Index at -5.8 and the Future Business Climate Index well below zero, reflecting ongoing pessimism.

-

Notably, the Future Prices Received Index rose to its highest in more than three years, pointing to expectations of stronger selling price increases ahead.

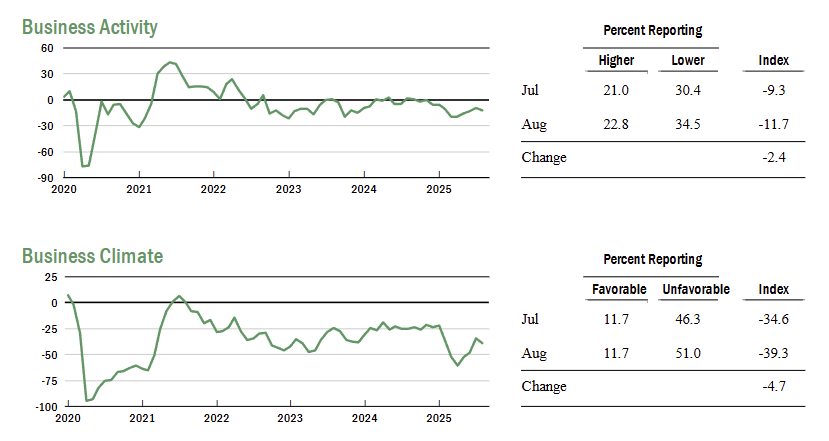

The NY Fed Business Leaders Survey showed another contraction in August, with the Business Activity Index slipping to -11.7 (from -9.3 in July), marking the sixth straight monthly decline and indicating ongoing weakness in the region’s service sector.

-

The Business Climate Index fell to -39.3 (from -34.6), signaling that conditions remain significantly worse than normal for most firms.

-

The Employment Index edged down to 1.0 (from 3.8), suggesting headcount was broadly unchanged, while wage growth held roughly steady (Wages Index at 28.0).

-

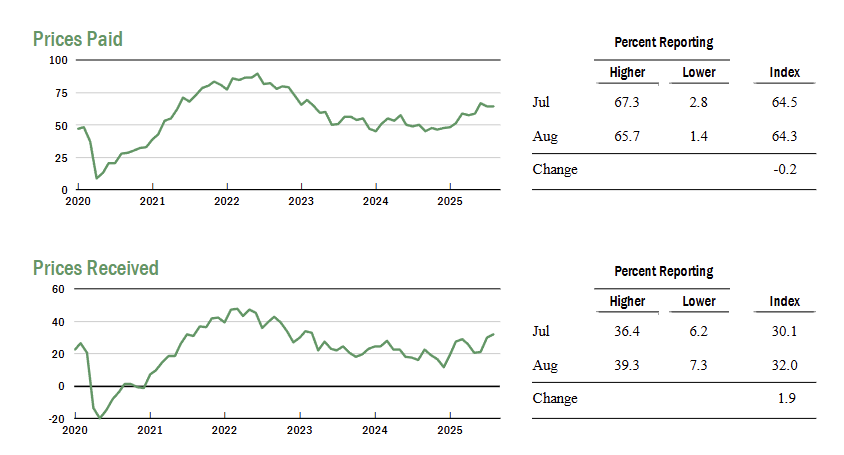

The Prices Paid Index remained high at 64.3, indicating continued input cost pressures, and the Prices Received Index rose to 32.0, the highest since March 2023, pointing to stronger selling price increases.

-

The Capital Spending Index improved to -2.9 (from -8.5), remaining in negative territory but indicating a slower pace of decline in investment plans.

-

Firms’ future outlook deteriorated, with the index for future business activity falling to -6.8, reflecting renewed pessimism about conditions ahead.

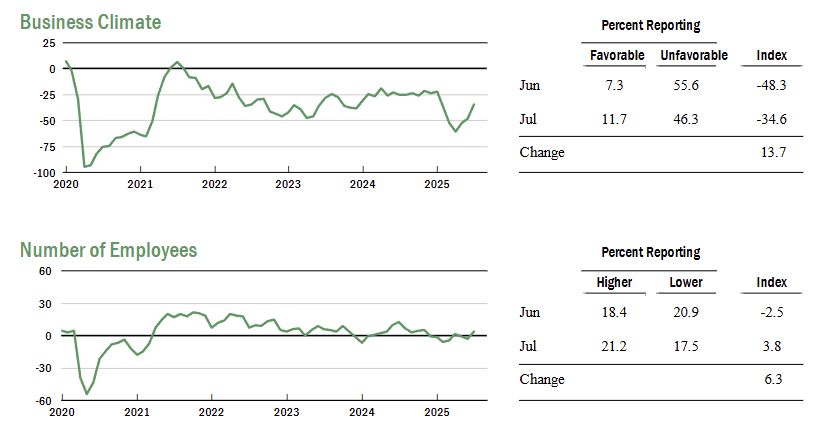

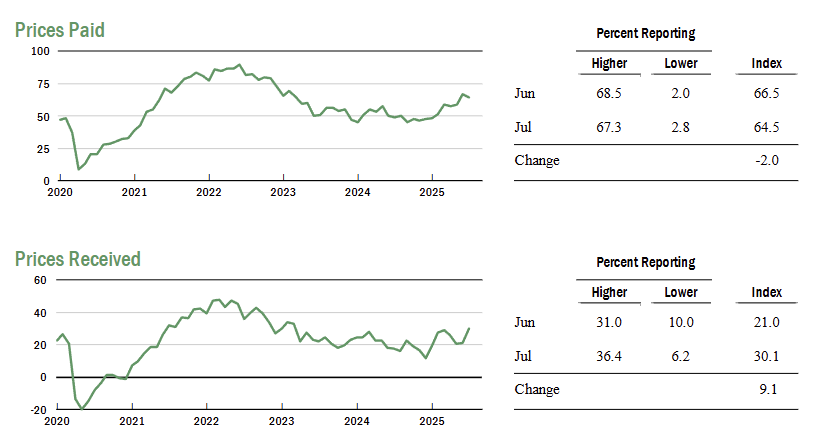

The NY Fed Business Leaders Survey Business Activity Index remained negative in July, with the headline index rising 3.9 pts to -9.3, marking the fifth straight monthly contraction.

- The Business Climate index improved by 13.7 pts to -34.6, though still signaling conditions worse than normal for most firms.

- The Employment index rose 6.3 pts to 3.8, suggesting modest job growth; wage pressures also picked up, with the Wages index jumping 9.0 pts to 28.3.

- Prices Paid edged down -2.0 pts to 64.5 but remained elevated, while Prices Received surged 9.1 pts to 30.1, the highest since March 2023.

- Capital Spending rose slightly, up 4.1 pts to -8.5, still negative but improving from June.

- Supply availability remained a constraint with its index at -7.1, though less severe than in the prior month.