GEP Global Supply Chain Volatility Index

About

Latest Releases

12

The GEP Global Supply Chain Volatility Index signaled a marked rebound in global manufacturing demand in January 2026, with Asia at 0.12 (from -0.20) and North America at 0.06 (from -0.37), indicating a shift from underutilized to stretched supply capacity in key regions.

-

Asia’s index rose to 0.12 (from -0.20), marking the busiest supply chain conditions since November 2024, as manufacturers in China, Japan, Korea, India, and across ASEAN increased purchasing volumes in response to improved order books.

-

North America’s index climbed to 0.06 (from -0.37), the most stretched supplier capacity in just over 18 months, reflecting renewed momentum in U.S. manufacturing and greater appetite for inventory building.

-

Europe’s index fell to -0.27 (from -0.17), signaling increased spare capacity and continued reluctance among firms to restock, though the downturn in purchasing showed tentative signs of easing.

-

The U.K. index declined to -0.17 (from 0.12), indicating a shift back to underutilized supply chains at the start of 2026 and a weakening in manufacturing conditions.

-

Globally, demand for commodities, raw materials, and intermediate goods rose by its strongest margin in almost four years, underscoring a broad-based pickup in procurement activity.

-

Inventory stockpiling tied to price or supply concerns remained muted globally, though inventory building increased in North America while Europe continued destocking, highlighting regional divergence.

-

The global items-in-short-supply indicator stayed below its long-run average for nearly two-and-a-half years, suggesting fewer-than-normal material shortages, while labor shortages also remained below typical levels, indicating staff constraints were not limiting production.

-

Transportation costs increased at the start of the year amid rising global oil prices, pointing to renewed cost pressures within logistics channels.

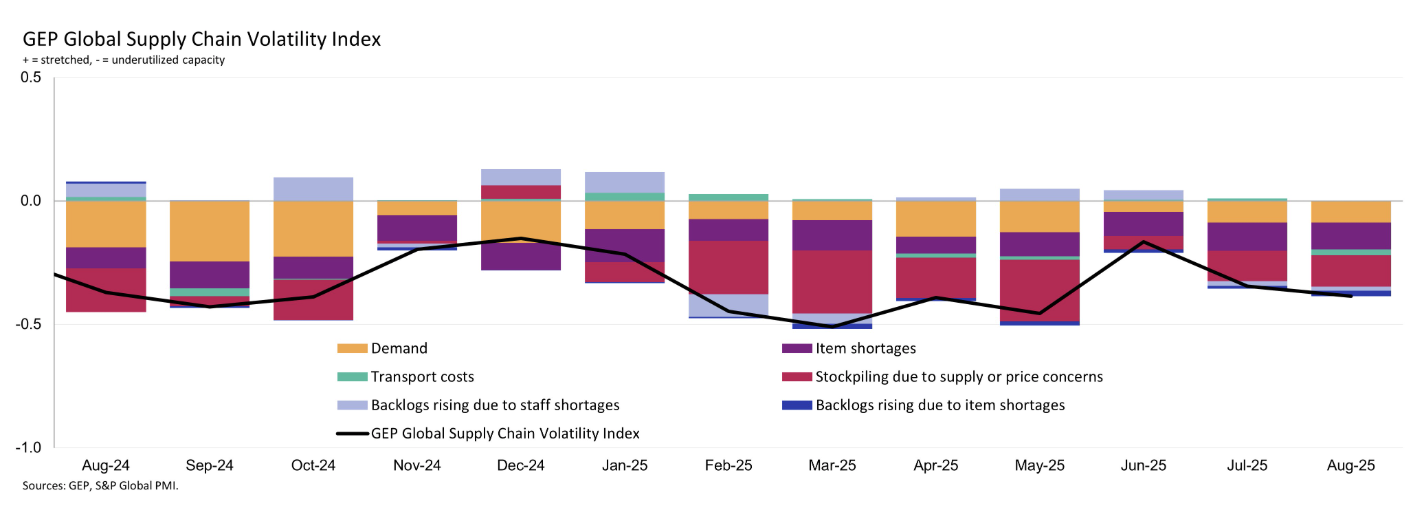

The GEP Global Supply Chain Volatility Index improved to -0.17 in December 2025 (highest since June 2025), but remained negative, signaling continued underutilized global supply capacity heading into 2026.

-

The global index edged up to -0.17, but underlying details continued to point to softening global manufacturing demand, especially across the Western economies.

-

North America’s index fell to -0.37, indicating underused supplier capacity, as manufacturers reduced procurement at the fastest pace since May 2025 and logged a sixth consecutive month of weakening input demand.

-

North American weakness was described as broad-based, with Mexico posting the steepest contraction, reinforcing the report’s message of regional manufacturing pullback.

-

Europe’s index rose to -0.17 (highest since June 2025), with the report attributing the improvement partly to labor-related constraints that impeded order completion, even as purchasing volumes continued to deteriorate.

-

European factory purchasing registered its sharpest decline in nine months, led by pronounced cutbacks in Germany, where weak demand pipelines continued to weigh on orders.

-

Asia’s index slipped to -0.20 from -0.16, but the report emphasized greater resilience in Asian factory purchasing, with improving input demand in South Korea, Vietnam, and Taiwan, and stabilizing buying activity in China.

-

The U.K. index rose to 0.12, signaling stretched supply chain capacity for the first time in almost a year and a half, making it the only region cited in expansionary territory.

-

Inventory stockpiling tied to supply or price concerns remained below average, with the report noting strong item availability, helping keep price pressures contained and limiting demand for buffer inventories.

-

Material shortages remained below the long-run average (continuing a pattern of more than two years), consistent with few shortage-related disruptions across supply chains.

-

Labor shortages rose to a 14-month high and were above the long-run average, with the report noting the pressure was centered on Europe, while global transportation costs remained in line with long-term averages.

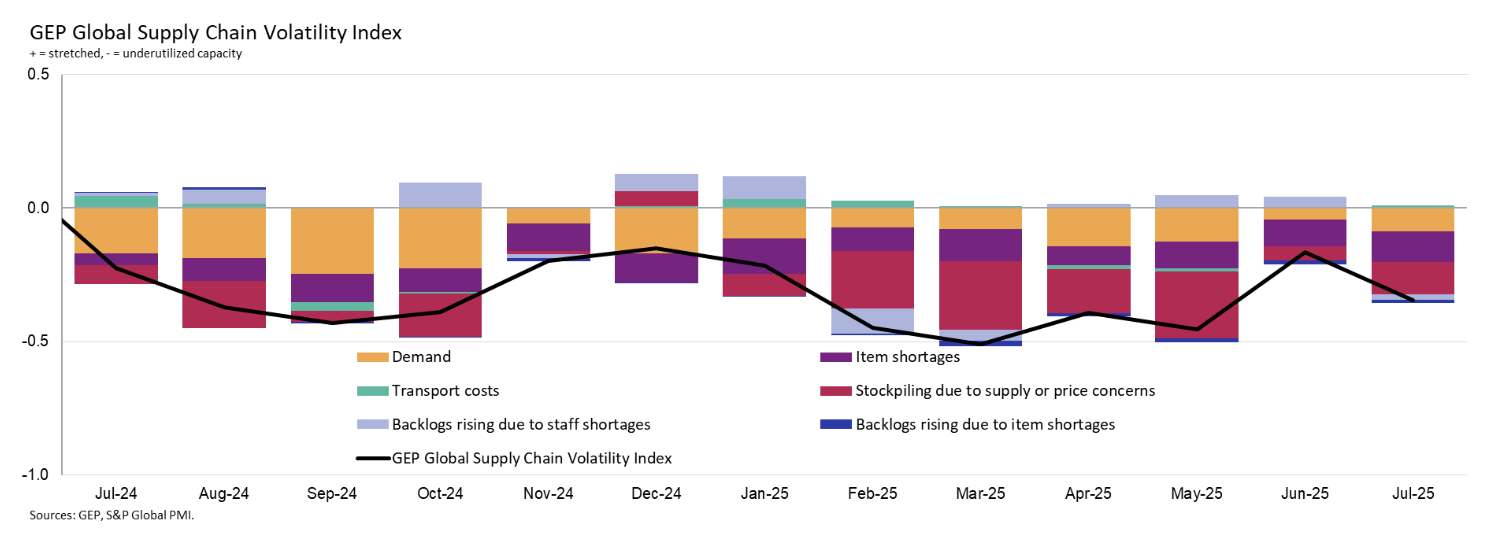

The GEP Global Supply Chain Volatility Index registered -0.29 in November 2025, up modestly from October but still indicating meaningful underutilization of global supply capacity as manufacturers cut back purchasing heading into 2026.

-

North America’s index fell to -0.53 (from -0.45), the sharpest regional deterioration, pointing to the weakest manufacturing demand since March as firms reduced input orders.

-

Asia’s index improved to -0.16 (from -0.30), reflecting slightly less spare capacity overall, though Chinese factory purchasing continued to decline and remained a major regional drag.

-

Europe’s index dipped to -0.33 (from -0.25), signaling persistent fragility across major industrial economies, particularly Germany and France, where firms made deeper purchasing cutbacks.

-

The U.K. index rose to -0.20 (from -0.80), marking its highest level in a year and suggesting early signs of stabilization after a prolonged manufacturing downturn.

-

Global factory demand weakened further, with slower purchasing of commodities and intermediate goods driven by softness in China, the U.S., and key European markets.

-

Inventory accumulation stayed historically low, indicating little concern about price spikes or supply risks and continued preference for lean stock strategies.

-

Material shortages remained well below trend, showing broad availability of goods and minimal sourcing challenges for manufacturers.

-

Labor shortages held only slightly above long-run norms, implying limited labor-related constraints on production capacity.

-

Transportation costs edged higher MoM, but remained broadly in line with historical averages, reinforcing the overall picture of slack rather than strain in global supply chains.

The GEP Global Supply Chain Volatility Index edged up slightly to -0.33 in October 2025 (from -0.39 in September), indicating continued underutilization of global supply capacity as manufacturers scaled back orders and inventories amid weak demand.

-

North America’s index dropped to -0.45 (from -0.25), the lowest since March, reflecting the steepest reduction in raw material purchases since May and signaling weaker production ahead.

-

Asia’s index declined sharply to -0.30 (from -0.06) as reduced factory buying in China offset strength in India, leaving the region with increased spare capacity.

-

Europe’s index improved to -0.25 (from -0.53), a three-month high, but still indicated subdued manufacturing activity as firms in Germany, France, Italy, and the U.K. limited material purchases.

-

The U.K. saw a notable pullback, with its index falling to -0.80 (from -0.57), pointing to a sharper contraction in supplier activity.

-

Global demand weakened as factory purchasing reversed September’s rebound, while inventory accumulation remained historically low, showing limited concern over shortages or price risks.

-

Material shortages stayed well below trend, suggesting ample product availability and minimal sourcing challenges across industries.

-

Labor-related capacity constraints rose slightly to a four-month high, though remained near long-run averages, while transportation costs edged down to just below historical norms.

-

GEP noted that with widespread spare capacity and reduced stockpiling, supply chains face little risk of goods price inflation outside of tariff impacts.

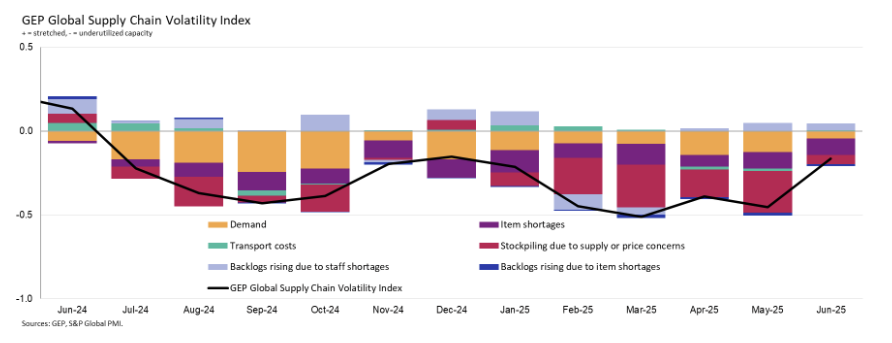

The GEP Global Supply Chain Volatility Index was virtually unchanged at -0.38 in September (vs -0.39 in August), signaling continued underutilization of global supply capacity despite a sharp rebound in China-led factory activity, marking the strongest global manufacturing expansion since mid-2022.

-

Chinese manufacturers significantly increased purchasing in September, driving Asia’s supply chains to near-full utilization — their busiest level since June 2022.

-

North American manufacturers pulled back from August’s strong stockpiling, as tariff disruptions and a softer outlook curbed purchasing and inventory accumulation.

-

Europe’s supply chains weakened further, with Germany, France, and Italy all reporting slower procurement, bringing the region’s index to its lowest since March.

-

The U.K. index improved to -0.57 (from -0.90) but still indicated considerable manufacturing weakness.

-

Global demand showed its strongest increase since June 2022, led by Asia, while North America and Europe saw limited improvement.

-

Material shortages eased, with GEP’s tracker showing robust product availability and minimal sourcing issues.

-

Global transportation costs remained stable and aligned with historical averages, and labor shortages were the lowest in six months, suggesting limited operational bottlenecks.

-

GEP noted that global manufacturers are adapting to a “new normal” of persistent tariffs, higher costs, and slower growth, prompting a strategic shift away from waiting for stability toward active adjustment.

The GEP Global Supply Chain Volatility Index slipped to -0.39 in August from -0.35 in July, signaling rising spare capacity globally and reflecting contrasting regional dynamics between U.S. stockpiling and weakening demand in Europe and Asia.

-

North America’s index showed supply chains running near full capacity as firms stockpiled raw materials and components, especially in U.S. consumer goods industries like food & beverages and household products.

-

Asia’s index dropped to a three-month low, with notable weakness in Japan and Taiwan, while China’s consumer non-cyclicals sector remained flat and India, Indonesia, and South Korea saw increased procurement.

-

Europe’s index fell further to -0.90, one of the steepest drops since 2024, as Germany’s basic materials sector softened and UK manufacturing contracted sharply.

-

The divergence highlights how tariff fears are driving precautionary stockpiling in North America, while weaker purchasing and destocking weigh on Asia and Europe.

-

GEP noted tariffs have become a structural feature of global supply chains, requiring companies to build resilience through supplier diversification and stronger demand sensing capabilities.

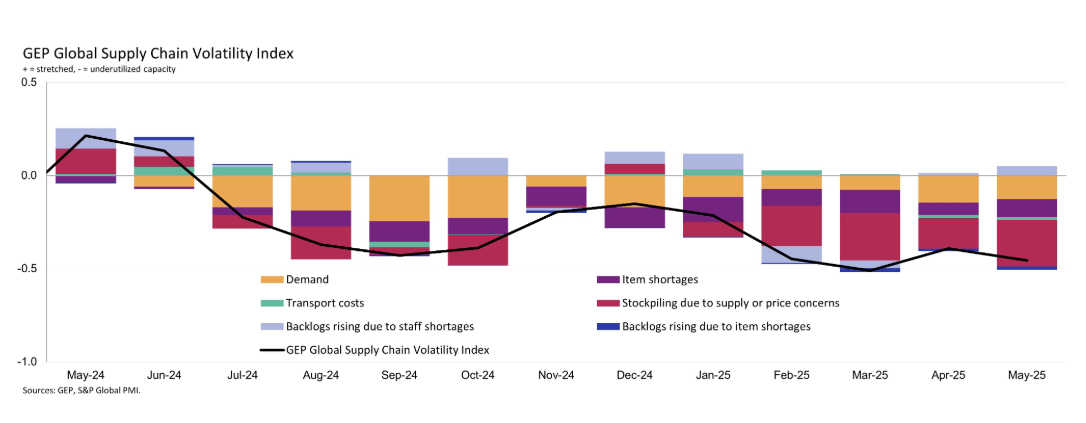

The GEP Global Supply Chain Volatility Index fell to -0.35 in July 2025 from -0.17 in June, signaling increased spare capacity as U.S. manufacturers sharply slowed purchases after front-loading inventories during the tariff pause.

- North America’s index dropped to -0.33 (from -0.06), driven by reduced U.S. factory orders for materials and components.

- Europe’s index declined to -0.30 (from 0.01) as Germany’s rebound lost momentum, stalling the region’s fragile recovery.

- Asia’s index remained below trend due to weakness in Japan, South Korea, and Taiwan, though China saw a rebound in factory buying.

- The U.K.’s index fell to -0.58 (from -0.41), indicating continued elevated spare capacity.

- Inventories eased from June’s stockpiling, while labor and transportation costs remained stable without inflationary pressure.

The GEP Global Supply Chain Volatility Index rose to -0.17 in June 2025 from -0.46 in May, the highest level this year, indicating global supply chains are operating near full capacity despite ongoing tariff concerns.

- Europe’s index climbed to 0.01 (from -0.30), signaling full capacity use for the first time in over two years, driven by German exports and domestic demand.

- North America’s index rose to -0.06 (from -0.24) as U.S. manufacturers accelerated purchases ahead of the tariff pause ending.

- Asia’s index increased to -0.27 (from -0.40), with stronger activity in India, Japan, and South Korea, though Southeast Asia remains underutilized.

- The U.K.’s index improved to -0.41 (from -0.97), the highest in 7 months but still indicates spare capacity.

- Despite a surge in procurement and stockpiling, global shortages, labor constraints, and transportation costs remain stable and historically typical.

The GEP Global Supply Chain Volatility Index fell to -0.46 in May 2025 from -0.39 in April, indicating a further rise in spare capacity globally amid weak demand and trade tensions.

- Asia’s index dropped to -0.40 (from -0.32), the lowest since Dec 2023, driven by sharp pullbacks in Chinese factory procurement.

- North America’s index improved to -0.24 (from -0.34) as U.S. manufacturers increased purchases to front-load inventories ahead of tariffs.

- Europe’s index was little changed at -0.30, with modest recovery aided by fiscal stimulus, especially in Germany.

- The U.K. index rose to -0.97 (from -1.12) but remains indicative of deep underutilization in supply chains.

- Global inventories diverged: safety stockpiling rose in North America but remained historically low in Europe, while global material shortages remained below average, signaling adequate supply.