ISM Manufacturing PMI

About

-

July 1st, 2026 · 10:00 AM

-

August 3rd, 2026 · 10:00 AM

-

September 1st, 2026 · 10:00 AM

-

October 1st, 2026 · 10:00 AM

-

November 2nd, 2026 · 10:00 AM

-

December 1st, 2026 · 10:00 AM

-

January 4th, 2027 · 10:00 AM

-

February 1st, 2027 · 10:00 AM

-

March 1st, 2027 · 10:00 AM

-

April 1st, 2027 · 10:00 AM

-

May 3rd, 2027 · 10:00 AM

Charts & Data

Latest Releases

12

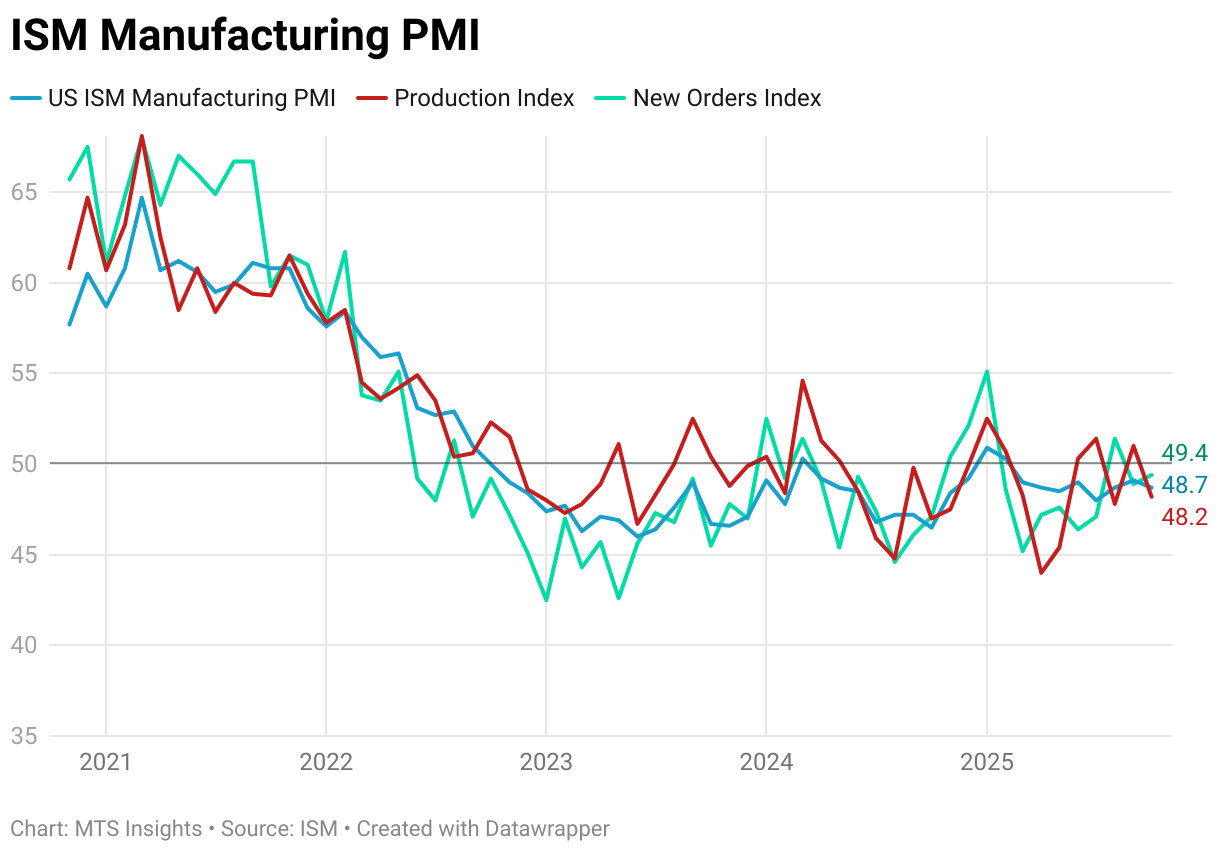

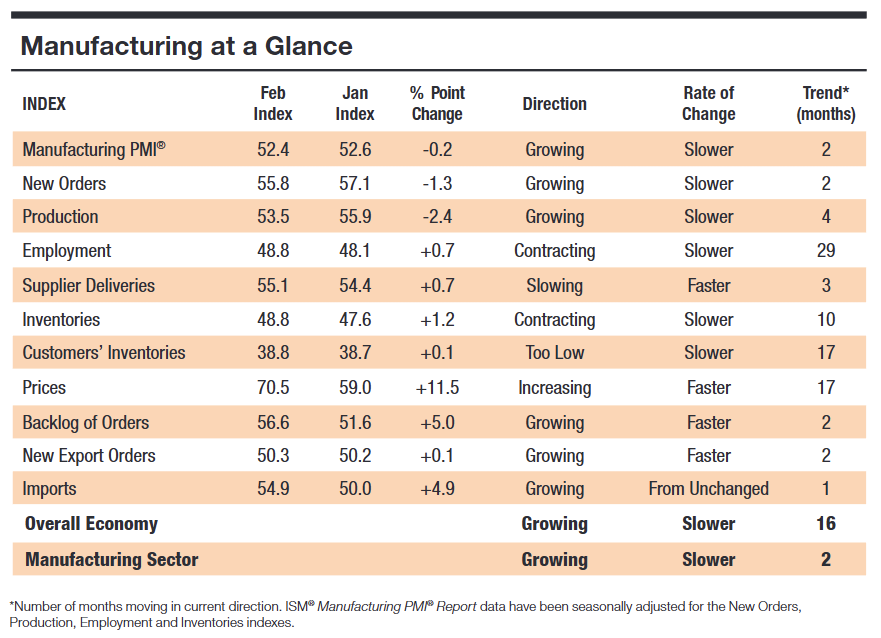

The ISM Manufacturing PMI registered 52.4 in February, down -0.2 percentage point MoM from 52.6 in January, remaining in expansion and reflecting moderate growth in production and new orders alongside sharply higher input prices and rising backlogs.

-

The New Orders Index stood at 55.8, down -1.3 pts MoM, indicating continued demand growth that has recovered after prior weakness and remains a key driver of production prospects for several large industries.

-

The Production Index was 53.5, down -2.4 pts MoM, marking a fourth consecutive month in expansion but at a slower pace than January and consistent with mixed firm-level comments on output.

-

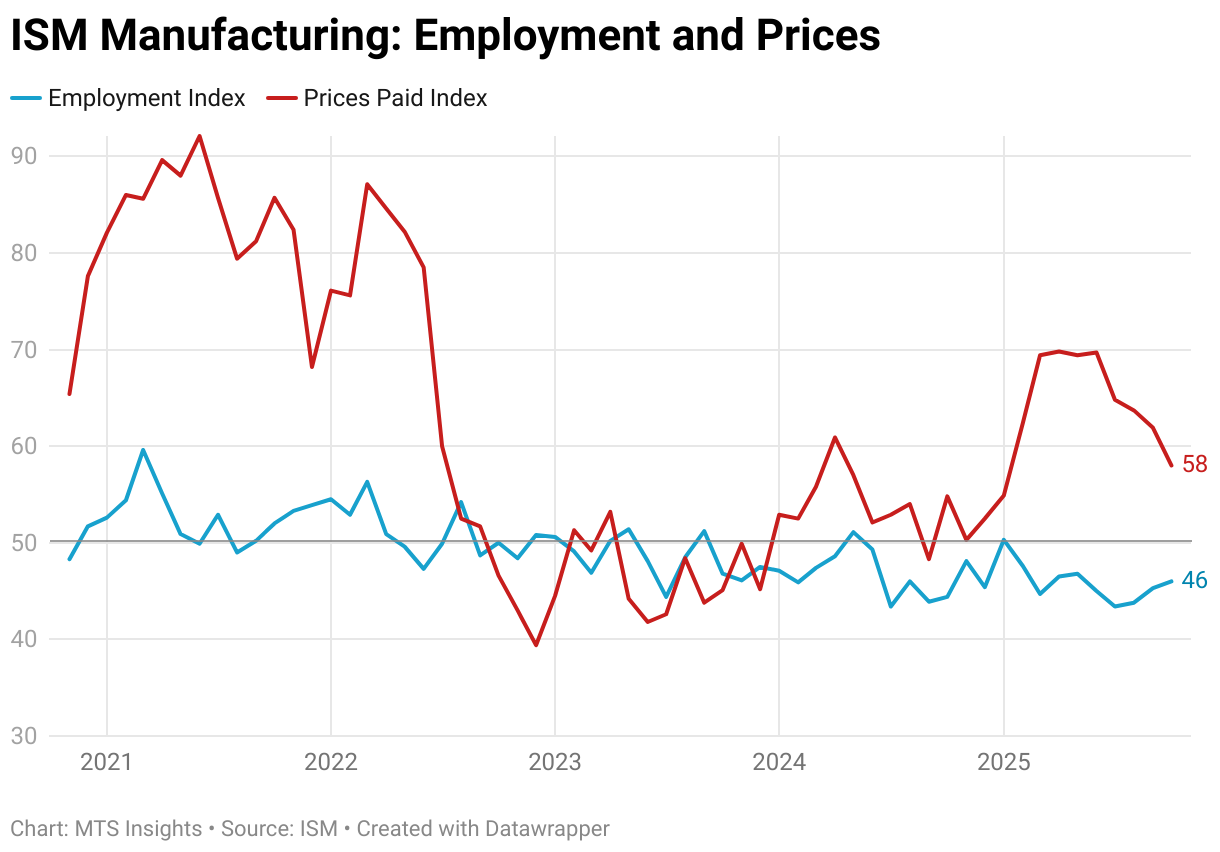

The Prices Index surged to 70.5, up +11.5 pts MoM and the highest since June 2022, signaling widespread raw material cost increases driven notably by steel and aluminum prices and tariffs, and implying stronger near-term cost pressure for manufacturers.

-

The Backlog of Orders Index rose to 56.6, up +5.0 pts MoM and the strongest since May 2022, showing that outstanding work has grown meaningfully and that order accumulation is supporting forward production plans.

-

The Employment Index remained in contraction at 48.8 but improved +0.7 pts MoM, reflecting modest rehiring in some industries even as many firms continue to manage head counts cautiously amid demand uncertainty.

-

Supplier Deliveries slowed further, with the Supplier Deliveries Index at 55.1, up +0.7 pts MoM, while the Inventories Index moved to 48.8, up +1.2 pts MoM, together showing slower vendor performance alongside only a tentative rebuilding of manufacturing stock positions.

-

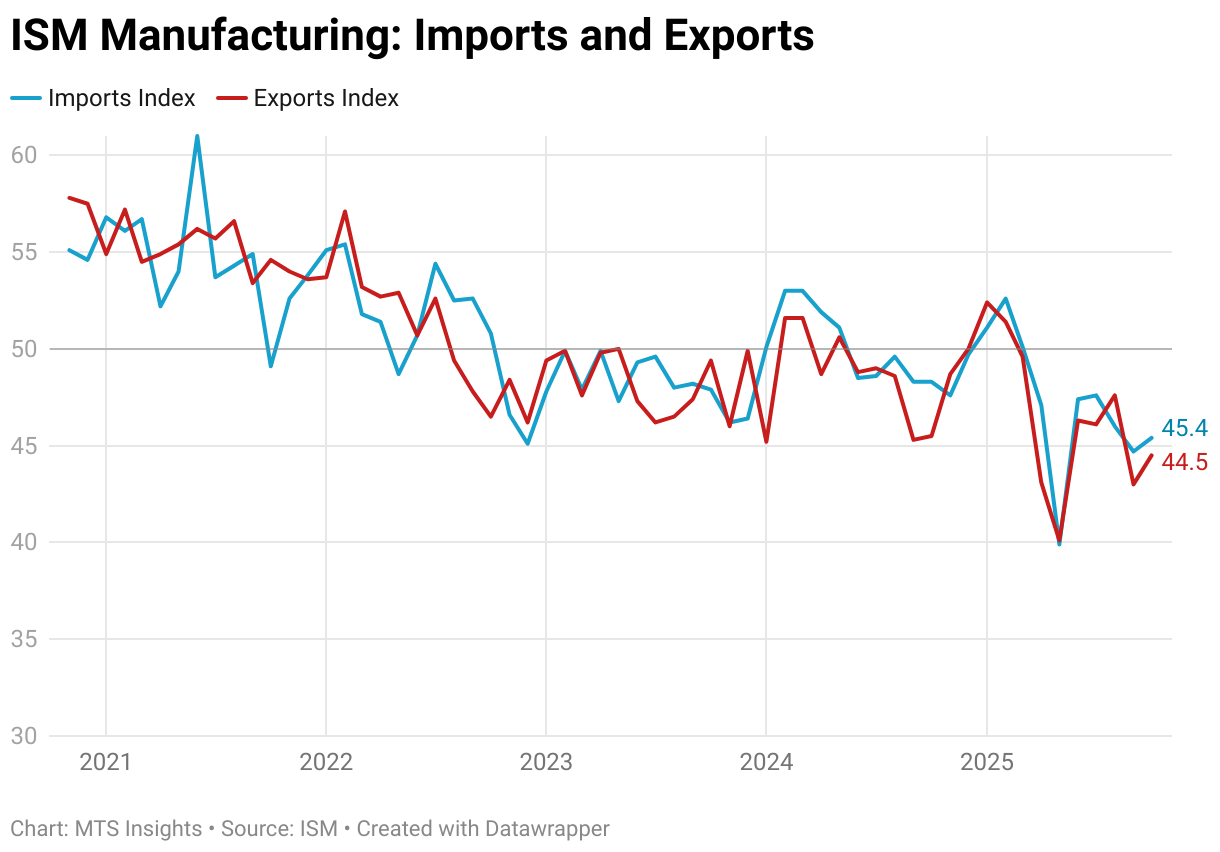

New Export Orders were marginally expansionary at 50.3, up +0.1 pts MoM, while the Imports Index jumped to 54.9, up +4.9 pts MoM and the highest since February 2022, indicating increased reliance on imported inputs even as export gains remain modest.

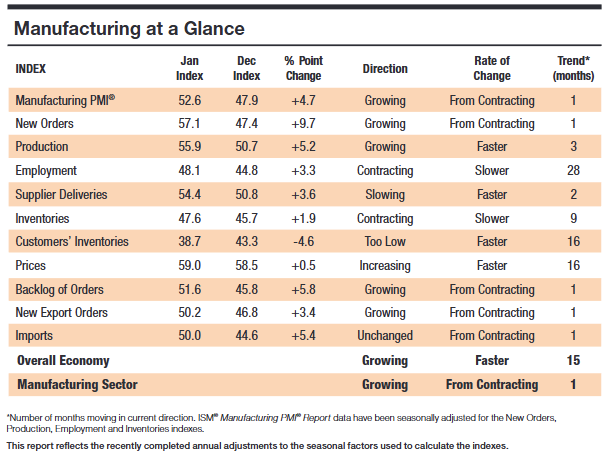

The ISM Manufacturing PMI rose to 52.6 in January from 47.9 in December (+4.7 pts MoM), ending a year-long contraction and indicating faster overall improvement in factory conditions.

-

The New Orders Index surged to 57.1 from 47.4 (+9.7 pts MoM), the highest since February 2022, showing demand turned expansionary, with the report noting post-holiday reordering and some buying ahead of expected tariff-related price increases.

-

The Production Index increased to 55.9 from 50.7 (+5.2 pts MoM), the strongest reading since February 2022 and a third straight month of expansion, reflecting stronger output growth.

-

The Employment Index improved to 48.1 from 44.8 (+3.3 pts MoM) but remained in contraction for a 28th month, indicating headcount reductions are still more common than hiring.

-

The Supplier Deliveries Index rose to 54.4 from 50.8 (+3.6 pts MoM), signaling slower deliveries for a second consecutive month, consistent with tightening supply performance as activity improves.

-

Inventories edged up to 47.6 from 45.7 (+1.9 pts MoM) but stayed in contraction, while Customers’ Inventories fell to 38.7 from 43.3 (-4.6 pts MoM) and remained “too low,” which the report links to the rebound in new orders and backlogs.

-

The Prices Index increased to 59.0 from 58.5 (+0.5 pts MoM), extending rising input costs to 16 straight months, while New Export Orders returned to expansion at 50.2 (+3.4 pts MoM) and Imports rebounded to 50.0 (+5.4 pts MoM), ending a prolonged contraction phase.

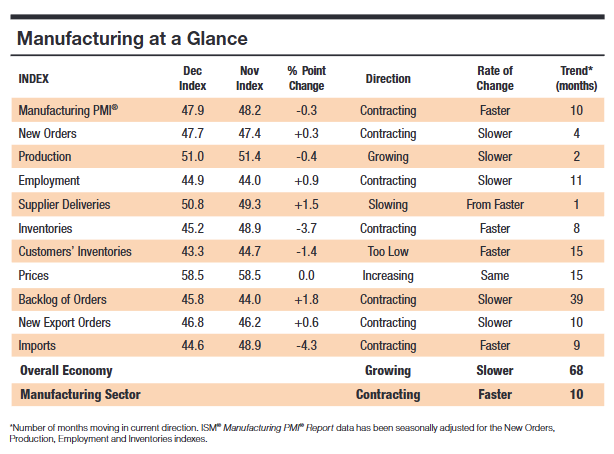

The US ISM Manufacturing PMI fell -0.3 pts MoM to 47.9 in December 2025, marking a tenth consecutive month of contraction while the broader economy remained in expansion.

-

Manufacturing PMI at 47.9 (Nov: 48.2) stayed below the 50 threshold, extending the contraction streak to 10 months, though the level remained above 42.3, which ISM associates with continued overall economic growth.

-

New Orders rose modestly to 47.7 (+0.3 pts MoM) but remained in contraction for a fourth straight month and below the 12-month average of 48.5, indicating persistently soft demand conditions.

-

The Production Index held in expansion at 51.0 (Nov: 51.4), showing output continued to grow, albeit at a slower pace, with only two of six large industries reporting higher production.

-

Employment increased to 44.9 (+0.9 pts MoM) but remained deeply contractionary for the 11th consecutive month, reflecting ongoing headcount reductions driven by uncertain near- to mid-term demand.

-

Supplier Deliveries moved back into slowing territory at 50.8 (Nov: 49.3), indicating deliveries became slower after one month of improvement, consistent with renewed supply-side frictions in some industries.

-

Inventories fell sharply to 45.2 (-3.7 pts MoM), signaling faster inventory contraction, while Customers’ Inventories declined to 43.3 (-1.4 pts MoM) and remained firmly in “too low” territory.

-

Prices held steady at 58.5 (unchanged MoM), marking the 15th consecutive month of rising input costs, with respondents continuing to cite steel, aluminum, and tariff-related pressures.

-

Backlogs of Orders rose to 45.8 (+1.8 pts MoM) but contracted for a 39th straight month, while New Export Orders improved slightly to 46.8 (+0.6 pts MoM) and Imports dropped sharply to 44.6 (-4.3 pts MoM), underscoring continued weakness in trade-related demand.

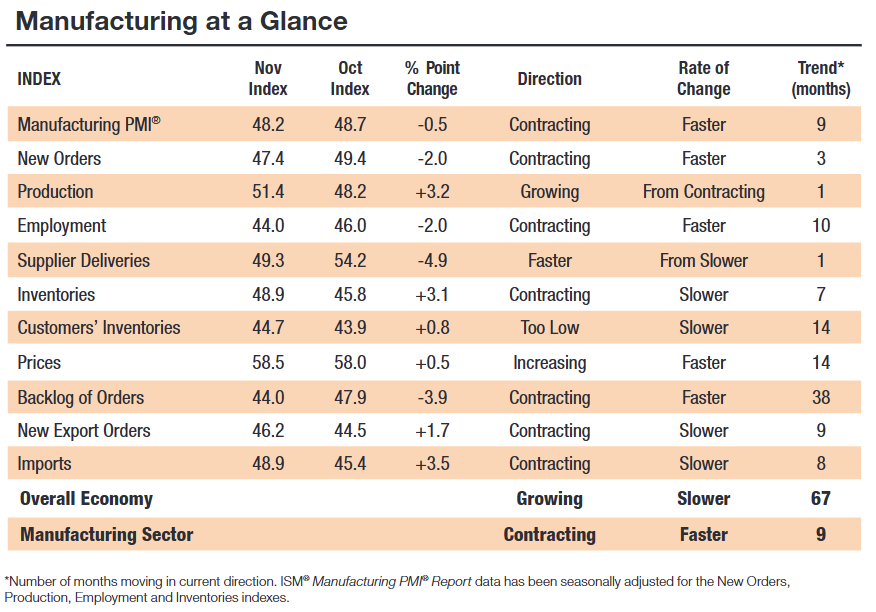

The US ISM Manufacturing PMI fell -0.5 pts to 48.2 in November 2025 (from 48.7 in October), indicating a faster contraction in factory activity even as the broader economy continued to expand.

-

The Manufacturing PMI has now been below 50 for 9 straight months (after two months of expansion), but at 48.2 it is still consistent with roughly +1.7 percent annualized growth in real GDP, so overall economic activity remains in expansion.

-

The New Orders Index fell to 47.4 (from 49.4), contracting for a third consecutive month and sitting below its 12-month average of 48.9, highlighting soft demand and ongoing concerns about tariffs and near-term demand among respondents.

-

The Production Index rose back into expansion at 51.4 (from 48.2), with 3 of the 6 largest industries reporting higher output, showing that firms are still able to lift production even as new orders soften.

-

The Employment Index declined to 44.0 (from 46.0), its 10th straight month of contraction, as companies continued to reduce headcount via layoffs and not filling open positions in response to uncertain demand.

-

The Supplier Deliveries Index dropped to 49.3 (from 54.2), indicating faster deliveries for the first time in four months, while the Inventories Index rose to 48.9 (from 45.8), suggesting stock levels are still contracting but at a slower pace.

-

Customers’ Inventories remained “too low” at 44.7 (up slightly from 43.9), meaning clients’ stock levels are still below desired levels, a configuration that is usually supportive for future production.

-

The Prices Index increased to 58.5 (from 58.0), its 14th consecutive month in expansion, with respondents citing higher steel, aluminum, and tariff-related costs as key drivers of elevated input price inflation.

-

The Backlog of Orders Index fell to 44.0 (from 47.9), contracting for the 38th straight month, while the New Export Orders (46.2) and Imports (48.9) indexes remained in contraction but improved versus October, indicating external trade remains a drag even as the pace of decline eases.

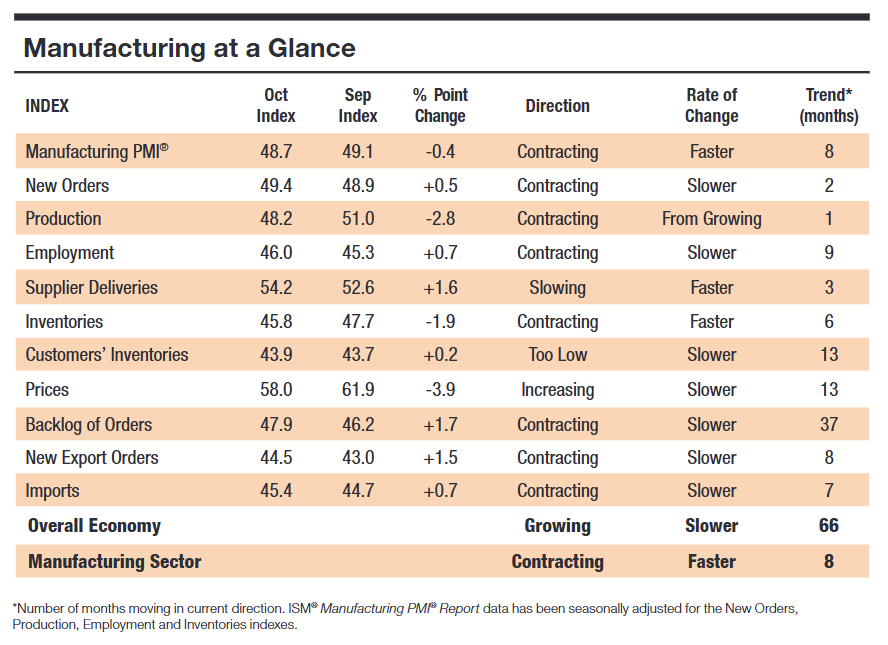

The US ISM Manufacturing PMI fell -0.4 pts to 48.7 in October 2025, marking a faster contraction while the broader economy continued to expand.

-

New Orders rose to 49.4 from 48.9 but stayed in contraction, indicating demand remains soft despite a slight improvement.

-

Production dropped to 48.2 from 51.0, pointing to a return to declining output after one month of growth.

-

Employment edged up to 46.0 from 45.3 yet remained below 50, showing continued head count reductions.

-

Prices eased to 58.0 from 61.9 but still indicated rising input costs for a 13th straight month.

-

Supplier Deliveries lengthened to 54.2 from 52.6, the third month of slower deliveries, consistent with ongoing supply frictions.

-

Inventories fell to 45.8 from 47.7, signaling a faster pace of stock drawdown at manufacturers.

-

Backlog of Orders improved to 47.9 from 46.2 but stayed in contraction, suggesting brief gains have not translated into sustained growth.

-

New Export Orders rose to 44.5 from 43.0 and Imports to 45.4 from 44.7, both still contracting, reflecting weak external trade flows.

-

Customers’ Inventories were 43.9, little changed from 43.7, remaining in too low territory, which can be supportive for future production.

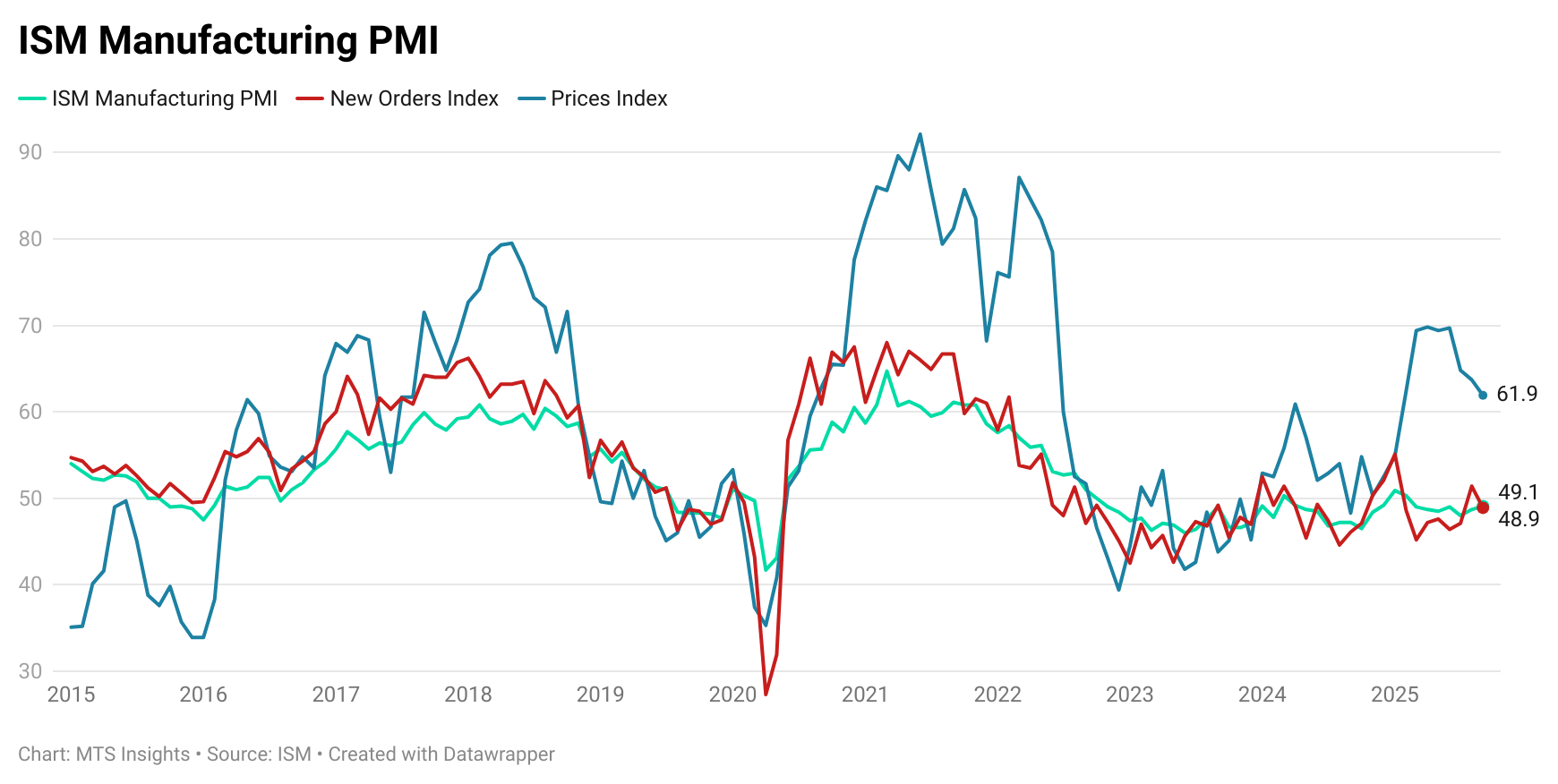

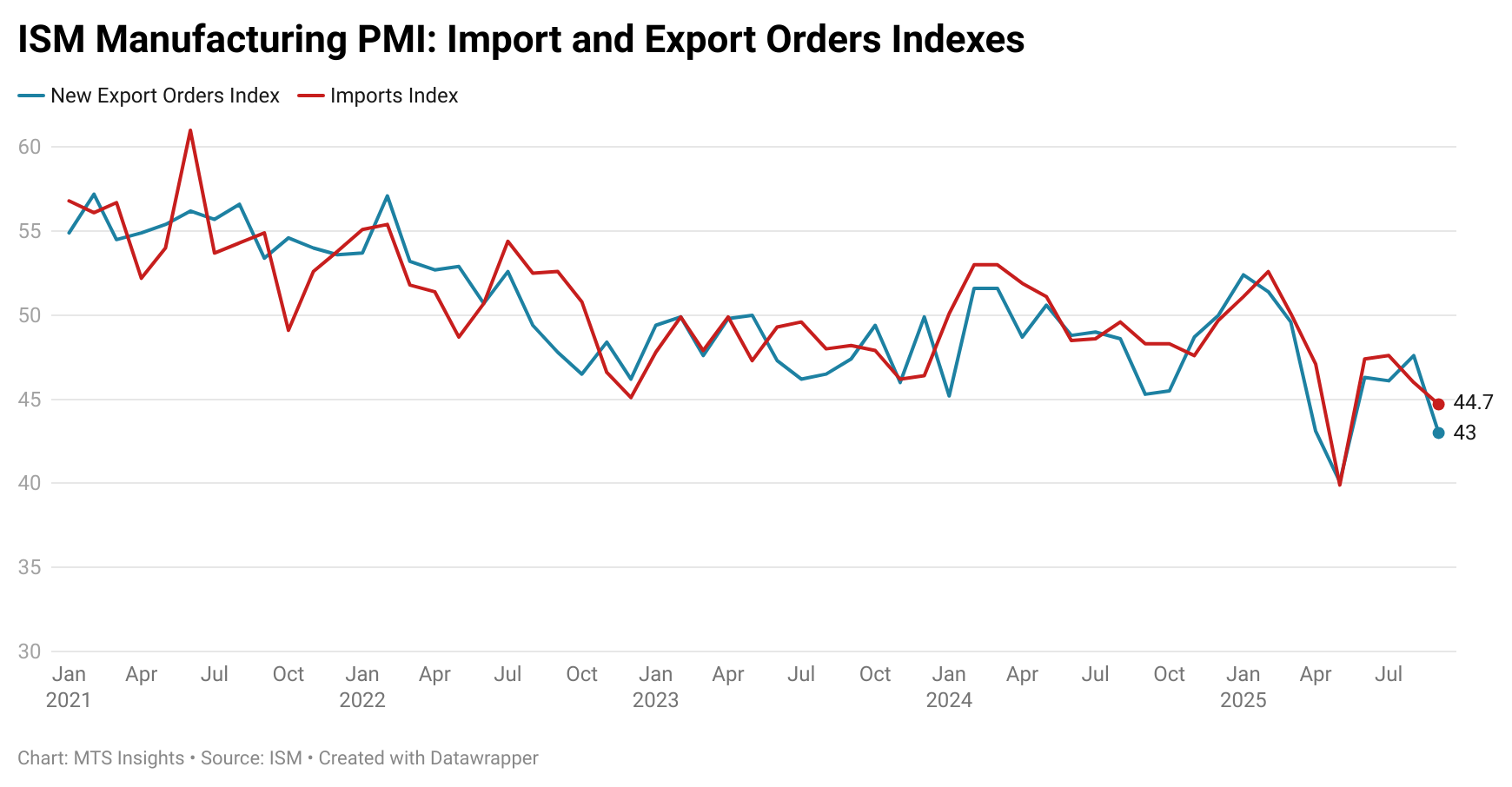

The US ISM Manufacturing PMI rose by 0.4 points to 49.1 in September 2025, remaining in contraction for a seventh straight month but signaling a slightly slower pace of decline.

-

New orders fell by 2.5 points to 48.9, returning to contraction after one month of expansion and pointing to weaker near-term demand.

-

Production increased by 3.2 points to 51.0, moving back into growth and marking one of the few areas of strength.

-

Employment rose by 1.5 points to 45.3, but it continued to contract for the eighth consecutive month as firms reduced head counts.

-

Supplier deliveries rose by 1.3 points to 52.6, indicating that delivery times lengthened for the second month in a row.

-

Inventories decreased by 1.7 points to 47.7, showing a faster pace of contraction, while customers’ inventories slipped by 0.9 points to 43.7 and remained in “too low” territory for the twelfth straight month.

-

Prices fell by 1.8 points to 61.9, but they continued to increase overall for a twelfth consecutive month, led by metals and tariff-related cost pressures.

-

Backlogs of orders rose by 1.5 points to 46.2, yet they contracted for the thirty-sixth straight month.

-

New export orders dropped sharply by 4.6 points to 43.0, marking a seventh consecutive contraction and reflecting weaker overseas demand.

-

Imports fell by 1.3 points to 44.7, extending their contraction for a sixth month in line with softer demand.

-

Overall, the PMI result suggests that the manufacturing sector remains under pressure, but the report also noted that the broader US economy continued to grow for a sixty-fifth straight month.

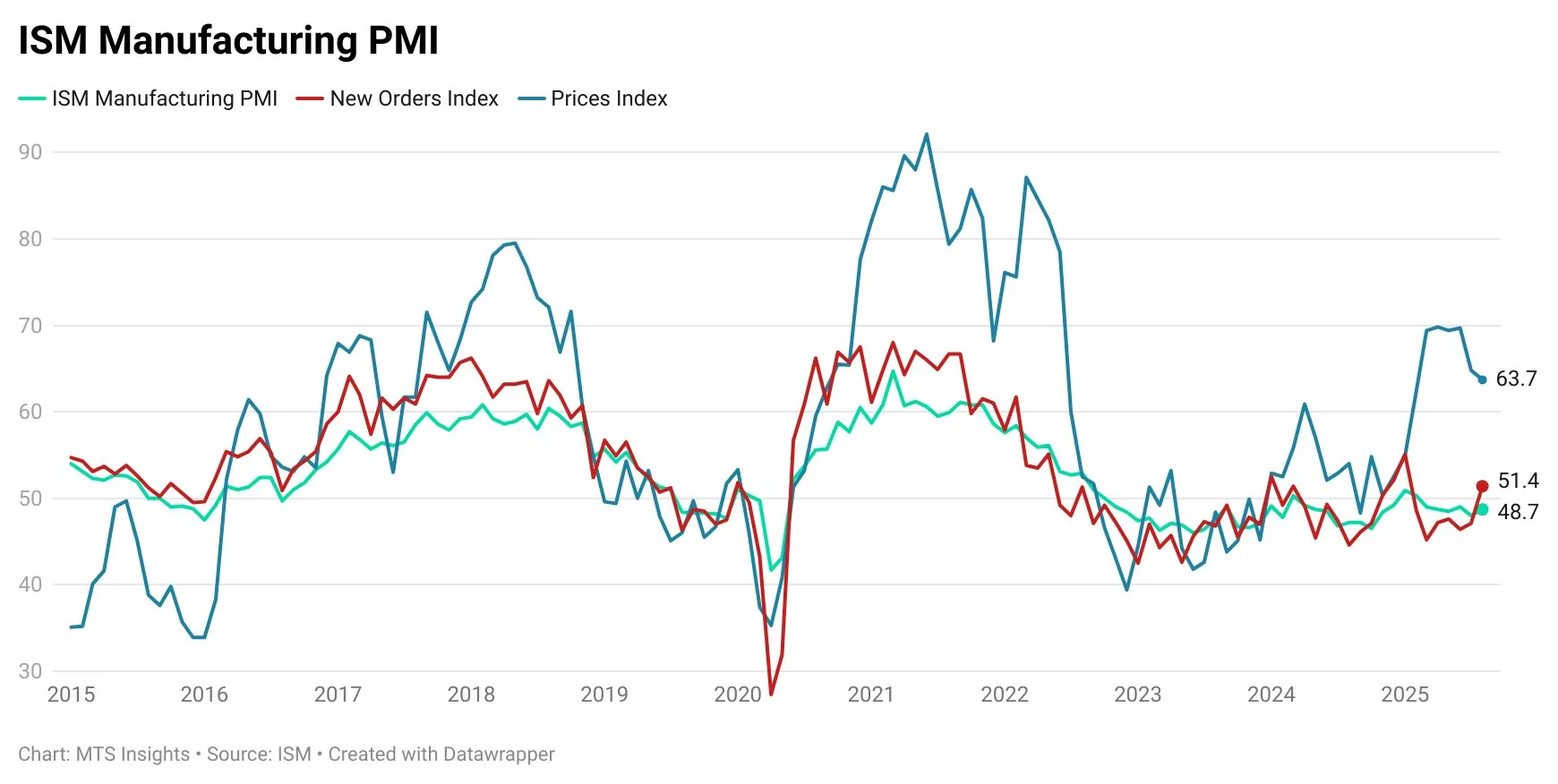

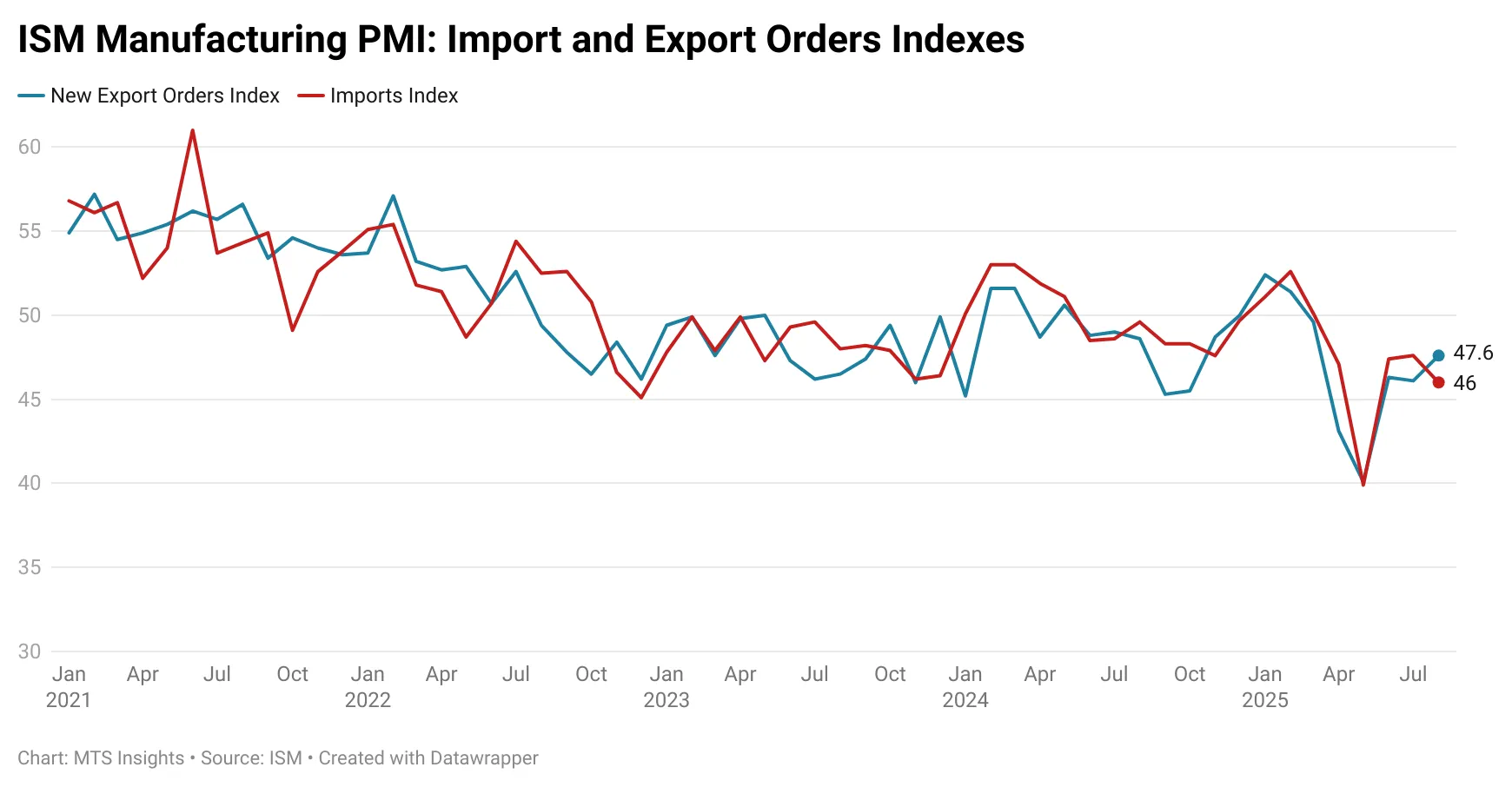

The ISM Manufacturing PMI presented a more negative view of the US manufacturing sector in August. The headline index increased 0.7 pts but remained in contraction territory for the 6th straight month at 48.7. This was slightly below consensus expectations of 49.0. Like the S&P data, the ISM data pointed to a sector heavily impacted by tariffs, with diverging performance between local and foreign markets.

The two biggest movers in August were the New Orders index, up 4.3 pts to 51.4, and the Production index, down -3.6 pts to 47.8. Interestingly, the indexes appeared to have flipped such that demand went from a moderate contraction to a slight gain, and supply flipped from a marginal gain to a decline. The New Export Orders index increased 1.5 pts in August, but remained in a moderate decline, suggesting that the noted improvement in demand is primarily related to domestic markets.

The tariff impacts show in the indexes tracking imports and prices. The Import index declined -1.6 pts to 46.0 as the subindex gave back some of the post “Liberation Day” rebound gains. In fact, with the exception of the May reading of 39.9, the August import indicator is the lowest since December 2022. It is very possible that the Import index will continue to decline as tariff policy becomes more entrenched and firms move past the inventory-building phase. The Price index has also reacted sharply to tariffs. While it did drop -1.1 pts in August, it remains elevated at 63.7, reflecting price pressures seen during the supply chain crunch of 2022-2023. In this subindex measuring inflationary pressures, the ISM survey is very similar to the S&P survey, such that both are pointing to a highly inflationary environment.

While there are similarities between the two surveys, there are some notable differences. The S&P survey showed evidence of inventory building by manufacturing firms in August, such that it was a major component of the strength in operating conditions. The ISM survey pointed to the opposite trend: the Inventories index was at 49.4, a slight contraction, and the Customers’ Inventories index eased to 44.6, an even deeper deterioration. Another key difference was in the employment measures. While the S&P PMI pointed to strong hiring trends, the ISM Employment index remained at a low 43.8, demonstrating a solid contraction in the manufacturing workforce not seen since Q3 2024 (when the Fed cut by 50 bps).

Overall, the ISM data is a more pessimistic view of the US manufacturing sector, even though the primary indicator of demand flipped from contraction to expansion. Besides that, the subindexes pointed to a continued weakening in trade, both imports and exports, shrinking inventories, and a significant decline in the manufacturing workforce. While this is all developing, tariffs are keeping price pressures high to make for a complicated environment for manufacturers.

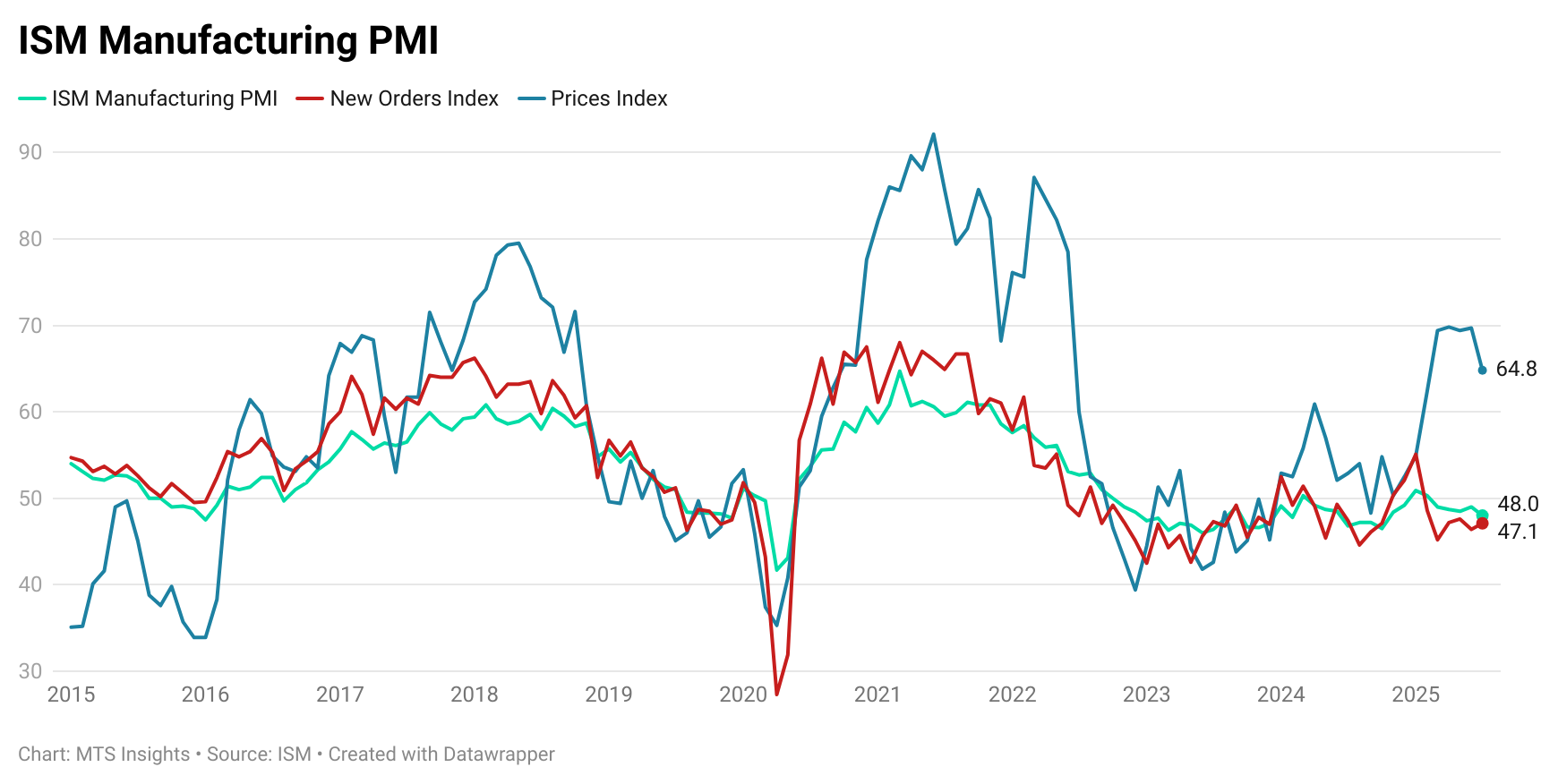

The US ISM Manufacturing PMI fell -1.0 pt to 48.0 in July, marking a fifth straight month of contraction and highlighting broad weakness across the sector.

- Production rose +1.1 pts to 51.4, extending its modest expansion despite weak demand.

- Employment dropped -1.6 pts to 43.4, a sixth consecutive contraction and reflecting ongoing layoffs.

- Supplier Deliveries fell sharply by -4.9 pts to 49.3, signaling faster deliveries amid easing supply chain strain and weaker demand.

- Prices decreased -4.9 pts to 64.8, though still in expansion, as input cost inflation moderated but remained elevated due to aluminum and tariff effects.

- New Orders edged up +0.7 pts to 47.1, still in contraction for a sixth month, reflecting continued uncertainty from tariffs and weak buyer confidence.

- The Import and Export indexes were both mostly unchanged, remaining in contraction at 47.6 and 46.1, respectively.

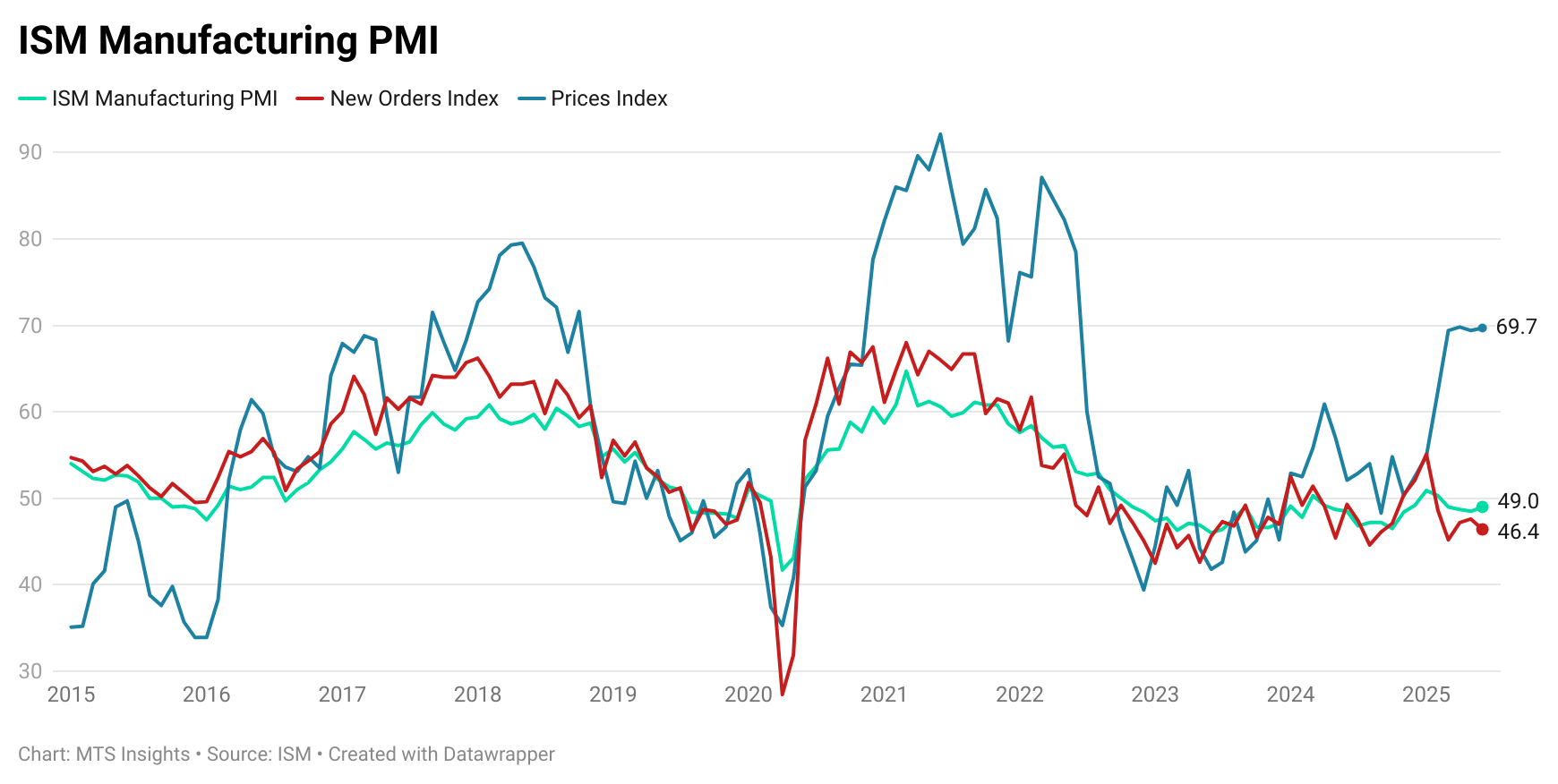

The US ISM Manufacturing PMI rose 0.5 pts to 49.0 in June, remaining in contraction for a fourth consecutive month, though signaling slower deterioration and a continued expansion of the broader economy.

- Production jumped 4.9 pts to 50.3, returning to expansion for the first time in four months.

- New Orders declined -1.2 pts to 46.4, marking a fifth straight month of contraction and ongoing weak demand.

- Employment fell -1.8 pts to 45.0, deepening contraction as layoffs accelerate.

- The Prices Index remained elevated, rising 0.3 pts to 69.7, with 45.6% of firms reporting higher prices.

- Supplier Deliveries fell -1.9 pts to 54.2, indicating slower but improving delivery performance amid easing port congestion.

- Inventories rose 2.5 pts to 49.2, contracting at a slower pace after tariff-related drawdowns.

- The New Export Orders (up 6.2 pts to 46.3) and Imports (up 7.5 pts to 47.4) indexes bounced back as trade dynamics improved while tariffs were paused.

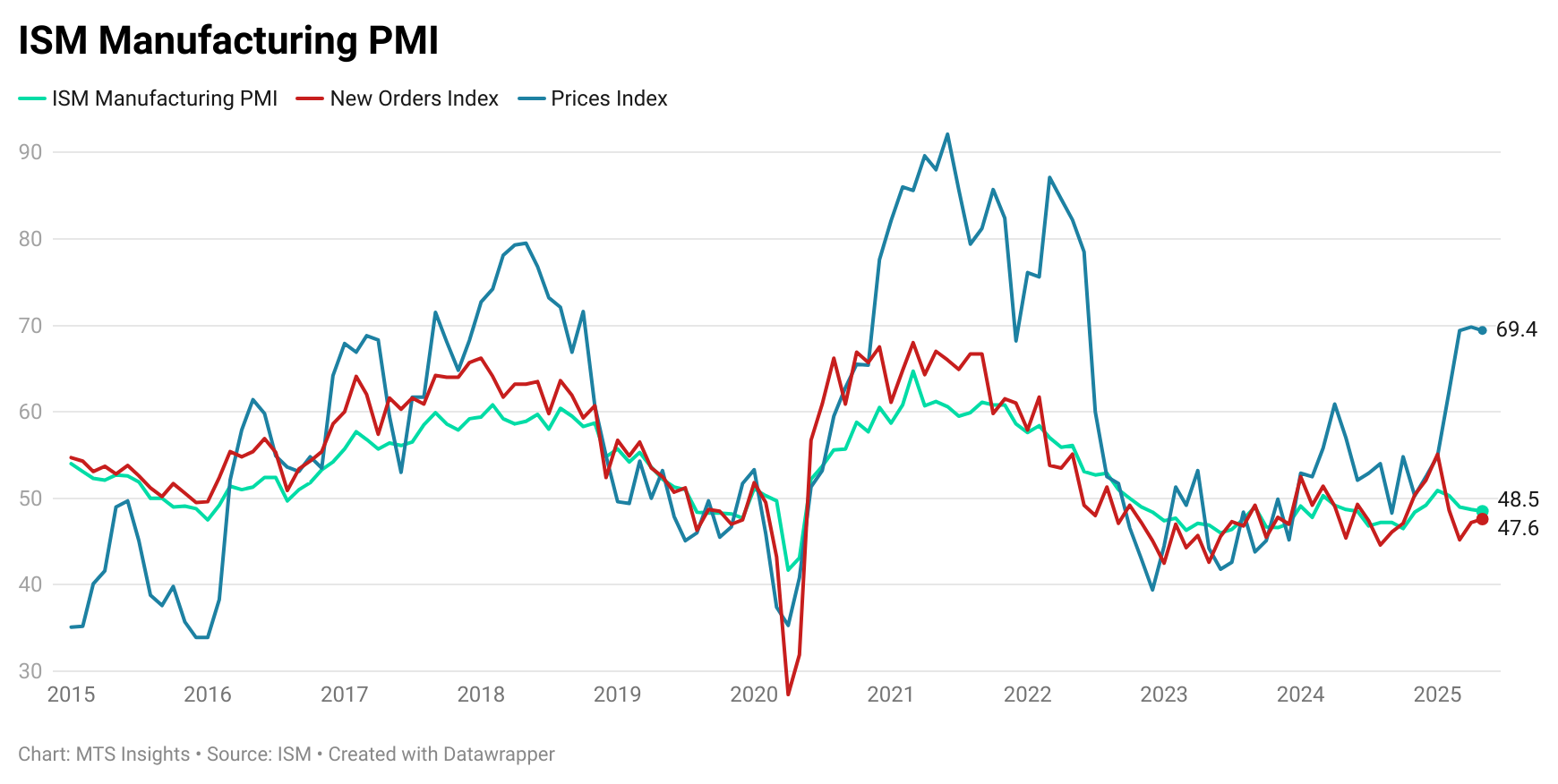

The US ISM Manufacturing PMI fell -0.2 pts to 48.5 (vs 49.5 expected) in May, remaining in contraction for a third straight month and marking the lowest reading since November 2024.

- Production rose 1.4 pts to 45.4 but remained in contraction, while New Orders improved 0.4 pts to 47.6 with ongoing weakness in demand.

- Inventories fell sharply, down -4.1 pts to 46.7, as companies completed tariff-driven stockpiling.

- New Export Orders dropped -3.0 pts to 40.1, the lowest since the pandemic excluding COVID-19, due to weak overseas demand and retaliatory tariffs.

- The Imports Index crashed -7.2 pts to 39.9, the lowest reading since the Global Financial Crisis.

- The Prices Index eased slightly to 69.4 (-0.4 pts), but remains elevated amid higher steel, aluminum, and tariff-related input costs.

- Supplier Deliveries increased to 56.1 (+0.9 pts), indicating slower deliveries amid strained logistics and pricing disputes.

- Despite manufacturing contraction, the overall economy was estimated to be growing for the 61st consecutive month.