ISM Manufacturing PMI: February 2026

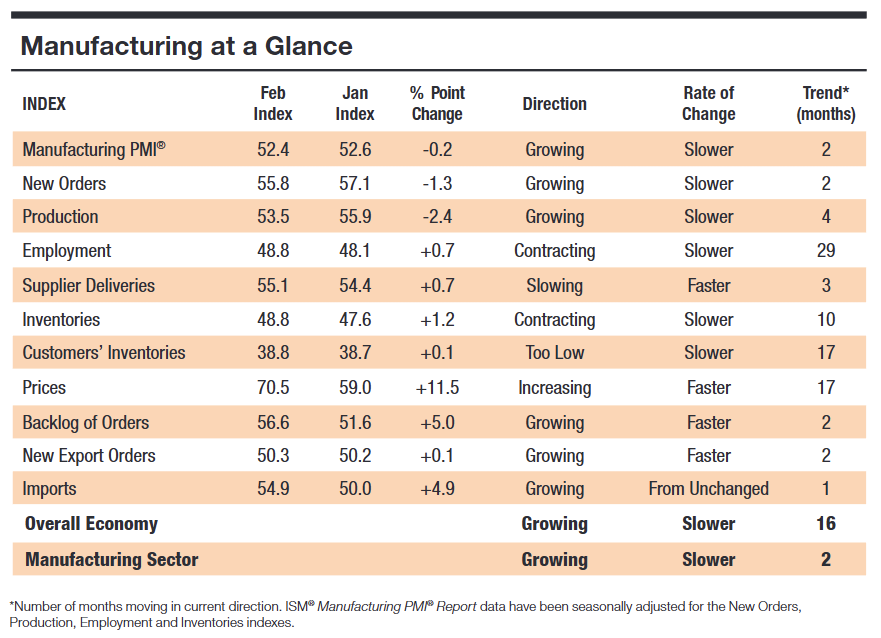

The ISM Manufacturing PMI registered 52.4 in February, down -0.2 percentage point MoM from 52.6 in January, remaining in expansion and reflecting moderate growth in production and new orders alongside sharply higher input prices and rising backlogs.

-

The New Orders Index stood at 55.8, down -1.3 pts MoM, indicating continued demand growth that has recovered after prior weakness and remains a key driver of production prospects for several large industries.

-

The Production Index was 53.5, down -2.4 pts MoM, marking a fourth consecutive month in expansion but at a slower pace than January and consistent with mixed firm-level comments on output.

-

The Prices Index surged to 70.5, up +11.5 pts MoM and the highest since June 2022, signaling widespread raw material cost increases driven notably by steel and aluminum prices and tariffs, and implying stronger near-term cost pressure for manufacturers.

-

The Backlog of Orders Index rose to 56.6, up +5.0 pts MoM and the strongest since May 2022, showing that outstanding work has grown meaningfully and that order accumulation is supporting forward production plans.

-

The Employment Index remained in contraction at 48.8 but improved +0.7 pts MoM, reflecting modest rehiring in some industries even as many firms continue to manage head counts cautiously amid demand uncertainty.

-

Supplier Deliveries slowed further, with the Supplier Deliveries Index at 55.1, up +0.7 pts MoM, while the Inventories Index moved to 48.8, up +1.2 pts MoM, together showing slower vendor performance alongside only a tentative rebuilding of manufacturing stock positions.

-

New Export Orders were marginally expansionary at 50.3, up +0.1 pts MoM, while the Imports Index jumped to 54.9, up +4.9 pts MoM and the highest since February 2022, indicating increased reliance on imported inputs even as export gains remain modest.