ISM Manufacturing PMI: November 2025

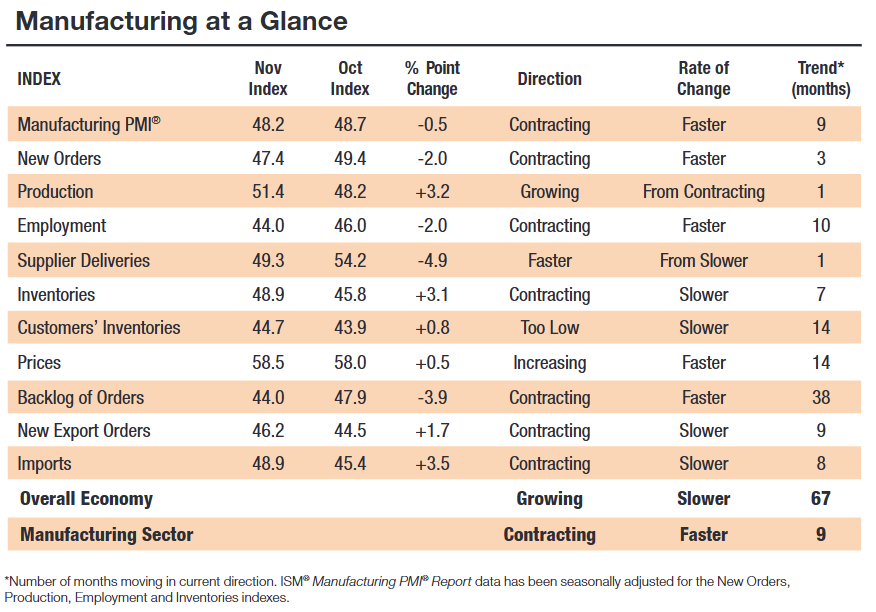

The US ISM Manufacturing PMI fell -0.5 pts to 48.2 in November 2025 (from 48.7 in October), indicating a faster contraction in factory activity even as the broader economy continued to expand.

-

The Manufacturing PMI has now been below 50 for 9 straight months (after two months of expansion), but at 48.2 it is still consistent with roughly +1.7 percent annualized growth in real GDP, so overall economic activity remains in expansion.

-

The New Orders Index fell to 47.4 (from 49.4), contracting for a third consecutive month and sitting below its 12-month average of 48.9, highlighting soft demand and ongoing concerns about tariffs and near-term demand among respondents.

-

The Production Index rose back into expansion at 51.4 (from 48.2), with 3 of the 6 largest industries reporting higher output, showing that firms are still able to lift production even as new orders soften.

-

The Employment Index declined to 44.0 (from 46.0), its 10th straight month of contraction, as companies continued to reduce headcount via layoffs and not filling open positions in response to uncertain demand.

-

The Supplier Deliveries Index dropped to 49.3 (from 54.2), indicating faster deliveries for the first time in four months, while the Inventories Index rose to 48.9 (from 45.8), suggesting stock levels are still contracting but at a slower pace.

-

Customers’ Inventories remained “too low” at 44.7 (up slightly from 43.9), meaning clients’ stock levels are still below desired levels, a configuration that is usually supportive for future production.

-

The Prices Index increased to 58.5 (from 58.0), its 14th consecutive month in expansion, with respondents citing higher steel, aluminum, and tariff-related costs as key drivers of elevated input price inflation.

-

The Backlog of Orders Index fell to 44.0 (from 47.9), contracting for the 38th straight month, while the New Export Orders (46.2) and Imports (48.9) indexes remained in contraction but improved versus October, indicating external trade remains a drag even as the pace of decline eases.