FOMC Minutes

About

-

August 19th, 2026 · 2:00 PM

-

October 7th, 2026 · 2:00 PM

-

November 18th, 2026 · 2:00 PM

-

December 30th, 2026 · 2:00 PM

-

February 17th, 2027 · 2:00 PM

-

April 7th, 2027 · 2:00 PM

-

May 19th, 2027 · 2:00 PM

-

June 30th, 2027 · 2:00 PM

-

August 18th, 2027 · 2:00 PM

-

October 6th, 2027 · 2:00 PM

-

November 17th, 2027 · 2:00 PM

Latest Releases

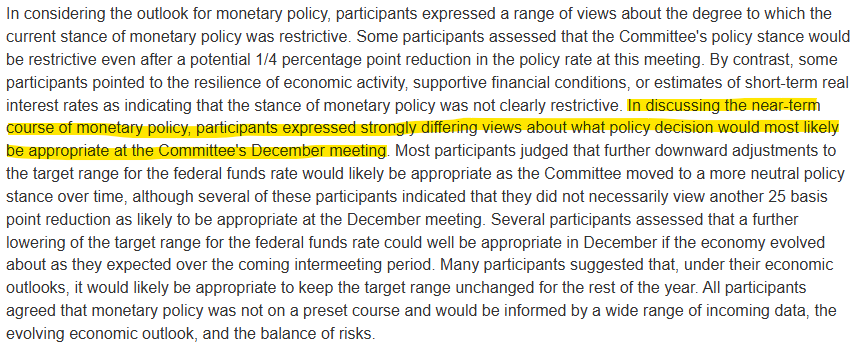

12Key takeaways from the FOMC Minutes for the January 27-28, 2026 meeting:

- The FOMC maintained the federal funds target range at 3.50% to 3.75%, citing solid growth but still-elevated inflation.

- Real GDP expanded in 2025 at a slightly slower pace than 2024, while consumer spending remained resilient and business investment robust, indicating continued economic expansion.

- The unemployment rate held at 4.4% in December and job gains remained low, suggesting labor market stabilization after gradual cooling.

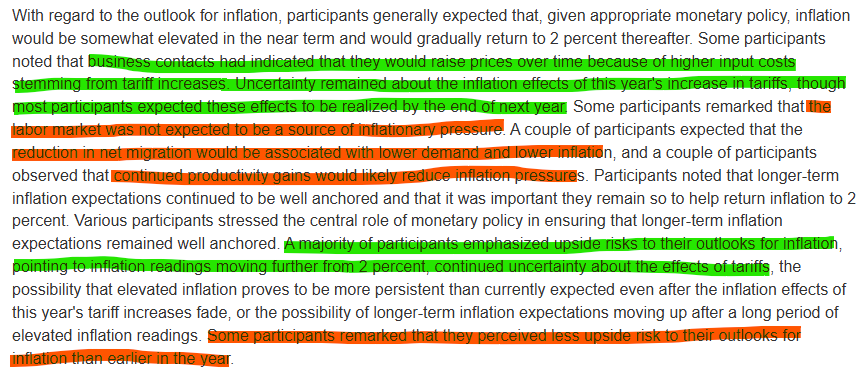

- Inflation stayed above target: PCE +2.8% YoY in November (prior year +2.6%), core PCE +2.8% YoY (prior year 3.0%), while CPI +2.7% YoY and core CPI +2.6% YoY in December, showing easing but still elevated price pressures.

- Participants noted core goods inflation was boosted by tariffs while core services inflation, particularly housing services, continued to decelerate, highlighting differing inflation drivers.

- Financial conditions were supportive: equity prices rose modestly, credit spreads remained low, and borrowing costs declined somewhat but stayed above post-GFC averages.

- Policy expectations were largely unchanged, with markets anticipating 1 to 2 rate cuts this year and the Committee emphasizing decisions would depend on incoming data and risk balance.

- The Committee voted to hold rates, with two members preferring a -25 bp cut, reflecting ongoing debate between inflation persistence risks and labor-market downside risks.

- The Fed also continued balance sheet operations, directing Treasury bill purchases and repo facilities to maintain ample reserves and stable money market functioning.

Key takeaways from the FOMC Minutes for the December 9-10, 2025 meeting:

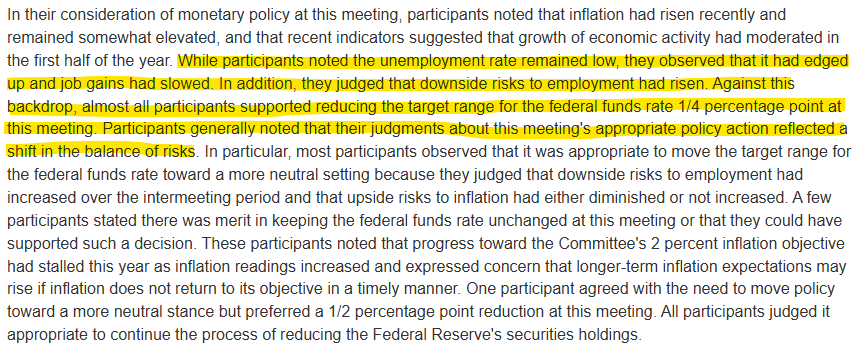

- The FOMC cut the fed funds target range -25 bps to 3.50% to 3.75% in December, reflecting elevated inflation but rising downside labor risks.

-

Investors generally expected a -25 bp cut at the December meeting, with the Desk survey modal outlook and options pricing implying two additional rate cuts next year, while macro outlooks were little changed over the intermeeting period.

-

Treasury yields edged higher but stayed within recent ranges, while inflation compensation moved lower, especially at shorter tenors, which the Desk manager attributed to lower energy prices and some reassessment of near-term tariff inflation effects.

-

Money market conditions tightened as repo rates stayed elevated and volatile, the EFFR spread to IORB faced upward pressure, and standing repo operations saw higher frequency and volume, consistent with reserves having declined into the ample range.

-

The manager flagged seasonal liability swings that could drive large reserve declines, especially around mid to late April via TGA tax inflows, and recommended starting reserve management purchases (RMPs) soon, with Desk survey respondents expecting about $220B in net purchases over the first 12 months on average.

-

Participants judged it appropriate to begin RMPs and to initiate purchases of shorter-term Treasuries, with many preferring Treasury bills to shift SOMA composition toward the Treasury universe, while emphasizing that RMPs are for rate control and market functioning rather than the policy stance.

-

The Committee voted to remove the aggregate limit on standing repo operations and directed the Desk to increase SOMA holdings via Treasury bill purchases and, if needed, other Treasuries with maturities of 3 years or less to maintain ample reserves.

-

Staff data through September showed total PCE inflation at 2.8% YoY and core PCE at 2.8% YoY, with core services inflation moving down but core goods inflation picking up, which staff largely attributed to higher tariffs.

-

Labor market conditions were described as gradually cooling: unemployment ticked up to 4.4% in September, payroll gains slowed, hiring remained subdued, and participants judged labor market risks tilted to the downside amid limited recent government data.

-

On the policy decision, nine members supported the -25 bp cut, while three dissented (two preferring no change and one preferring a -50 bp cut), with supporters citing increased downside employment risks and diminished or unchanged upside inflation risks, and opponents citing stalled progress toward 2% inflation and the value of additional incoming data.

-

Participants broadly agreed inflation remained somewhat elevated and risks to inflation were still tilted to the upside, while also judging downside employment risks had increased, reinforcing the emphasis that policy is not on a preset course and will be guided by incoming data and risk balancing.

-

Many participants "judged that the available evidence pointed to a reduced probability that tariffs would lead to persistent inflation pressures."

Key takeaways from the FOMC Minutes for the October 28-29, 2025 meeting:

-

Market expectations were stable, with investors pricing a -25 bp cut in October and another -25 bp in December, and Treasury yields holding little changed, reflecting an unchanged macro outlook.

-

Inflation compensation moved lower, especially at shorter maturities, as staff models attributed the decline to temporary factors, while broad equity indexes rose on continued optimism around AI-driven earnings.

-

Money markets tightened, with repo rates rising relative to IORB and SRF take-up occurring on several days, signaling reserves were moving closer to ample and prompting discussion about ending balance sheet runoff soon.

-

Participants agreed that reinvestments should shift toward Treasury bills once runoff stops, with many favoring a longer-run SOMA composition that more closely matches the distribution of Treasury securities outstanding.

-

Staff estimated September PCE and core PCE at 2.8% YoY, noting both remained somewhat elevated, with tariff-related pressures expected to push inflation higher in 2025–26 before returning to a disinflation trend.

-

GDP growth was moderate in H1, with indicators suggesting continued expansion but limited visibility due to the government shutdown; consumption was firming but increasingly dependent on higher-income households.

-

Labor market indicators pointed to gradual cooling, with job gains slowing, unemployment edging higher, and businesses showing hesitation to hire or fire; participants noted weaker labor demand but still limited layoffs.

-

Financial conditions remained supportive, with equity gains, tight credit spreads, and robust issuance, though vulnerabilities in private credit and elevated asset valuations were noted.

-

Participants were divided on inflation risks, with some citing tariff pass-through and sticky services inflation, while others pointed to weaker labor markets and productivity gains as moderating forces.

-

The Fed remained very divided on the December decision. Most participants judged further easing likely as policy moves toward neutral, though several cautioned that another cut in December was not guaranteed and emphasized the need for data-dependent decision-making.

-

Towards the end of the FOMC Minutes, we see two statements that highlight the division in the FOMC. We don't get exact numbers on each side, so "many" vs "most" is up to interpretation (in my opinion, "most" > "many").

-

Doves: "Many of these participants also judged that, with more evidence having accumulated that the effect on overall inflation of this year's higher tariffs would likely be limited, it was appropriate for the Committee to ease its policy stance in response to downside risks to employment."

-

Hawks: "Most participants noted that, against a backdrop of elevated inflation readings and a very gradual cooling of labor market conditions, further policy rate reductions could add to the risk of higher inflation becoming entrenched or could be misinterpreted as implying a lack of policymaker commitment to the 2% inflation objective."

-

Key takeaways from the FOMC Minutes for the September 16-17, 2025 meeting:

- The FOMC cut the federal funds rate -25 bps to 4.00–4.25% at the Sept 16–17, 2025 meeting, citing softer labor markets and still-elevated inflation, and emphasized a shift toward balanced risks with policy “not on a preset course.”

-

Markets & expectations: Following weaker July–Aug jobs data, survey and market pricing pointed to ~2–3 additional -25 bp cuts by year-end; Treasury yields fell 20–40 bps (bigger at the front end), the curve steepened slightly, and equity indexes moved near record highs while credit spreads stayed tight.

-

Money markets & balance sheet: Repo rates firmed amid higher TGA balances; SRF take-up hit $1.5B on Sept 15. If runoff continues, the SOMA portfolio is seen just over $6T by end-March, with reserves near ~$2.8T by end-Q1.

-

Inflation: PCE 2.7% YoY (Aug) and core PCE 2.9% YoY were at the upper end of this year’s range; participants saw tariff effects lifting prices near term but expected a gradual return to 2% over time.

- Most of the division in the Fed seems to be centered on the inflation outlook. Inflation hawks are worried about tariff price pressures and how long they could last. Inflation doves point to lower net migration, a weak labor market, and productivity gains.

-

Labor market: Conditions softened: unemployment 4.3% (Aug); payroll gains weak with a preliminary -900k benchmark revision to March levels; vacancies/unemployed ≈ 1.0; wage growth slowed (ECI +3.5% YoY; AHE +3.7% YoY).

-

Growth: Real GDP moderated in H1; staff revised up GDP a bit for 2025–2028 on firmer consumption/investment and easier financial conditions, but housing remained weak; high-tech capex was a relative bright spot.

-

Risk assessment: Participants judged downside risks to employment had risen; upside inflation risks remained but had diminished or not increased for many. Most anticipated further easing later in 2025, data-dependently.

-

Credit conditions: Borrowing costs fell but stayed elevated vs post-GFC norms; credit broadly available for larger firms and prime households, tighter for small businesses and lower-score borrowers; CMBS delinquencies elevated; card/auto delinquencies elevated but little changed.

- The September minutes confirm that the labor market was at the center of the cut, and that virtually all FOMC members saw a "shift in the balance of risks" in the weak employment data that had come out before the meeting.

-

Vote & dissent: Decision passed with one dissent—Governor Miran preferred -50 bps, citing further labor softening, inflation nearer 2%, and a lower neutral rate given tariff revenues and lower immigration.

Key takeaways from the FOMC Minutes for the July 29–30, 2025 meeting:

-

Economic Activity: Real GDP expanded modestly in H1 2025 after a Q1 contraction; growth in Q2 was driven by consumption and net exports, though investment slowed. Several participants expected subdued growth in H2. Housing demand showed weakness, while business investment was weighed down by policy uncertainty.

-

Inflation: Headline PCE inflation was 2.5% YoY in June; core PCE was 2.7%. Tariffs have put upward pressure on goods prices, while services inflation slowed. Many participants noted uncertainty about the timing and persistence of tariff effects, though longer-term inflation expectations remained anchored.

-

Labor Market: The unemployment rate stood at 4.1% in June, near maximum employment. Payroll gains were solid overall, though private sector hiring slowed. Some indicators suggested softer demand, including weaker wage gains and concentrated job growth, but participants emphasized stability in labor markets.

-

Monetary Policy Outlook: The Committee kept the federal funds rate at 4.25–4.50%. Almost all participants supported no change, citing inflation still above target; two members dissented in favor of a -25 bps cut, arguing that excluding tariffs, inflation is near 2% and growth has slowed. Policy remains data-dependent with attention to tariffs’ effects.

-

Risks and Financial Stability: Upside risks to inflation and downside risks to employment both seen as elevated, with the majority viewing inflation risks as greater. Participants flagged asset valuation pressures, tariff uncertainty, and vulnerabilities in nonbank finance and stablecoins. The Committee stressed the need to keep inflation expectations anchored amid tariff-related shocks.

-

Bowman and Waller's dissents did not include a weak labor market which suggests they might actually be in favor of a 50 bps cut in September given the bad July employment data.

Key takeaways from the FOMC Minutes for the June 17–18, 2025 meeting:

- Economic Activity: The economy expanded solidly in Q2 after a slight Q1 contraction. Consumer spending and business investment remained firm, though sentiment was subdued. Labor markets were stable with unemployment at 4.2%. Real GDP projections were revised higher, mainly due to lower assumed tariff rates.

- Inflation: Headline PCE inflation was 2.3% YoY in May; core PCE was 2.6%. Inflation has eased from 2022 peaks but remains somewhat elevated. Tariffs are expected to put modest upward pressure on inflation, though uncertainty surrounds their timing and magnitude.

- Monetary Policy Outlook:

- All participants supported keeping the federal funds rate at 4.25–4.50%.

- Most participants viewed some rate cuts in H2 2025 as likely appropriate if inflation continues to ease and labor markets remain stable.

- A minority favored no cuts in 2025, citing elevated inflation and upside risks.

- The Committee reaffirmed a data-dependent and cautious stance given persistent risks.

- Risks and Uncertainty:

- Uncertainty around tariffs, fiscal policy, and geopolitics remains elevated, though less so than in April.

- Inflation risks are still skewed to the upside; labor market risks are more balanced but could intensify if policy stays restrictive.

- Participants emphasized the need to keep inflation expectations anchored, especially amid recent price shocks.

- Balance Sheet and Market Functioning:

- SOMA runoff continued, with securities holdings down ~$2.25T since June 2022.

- Liquidity remains ample, but rebuilding of the Treasury General Account post-debt ceiling could drain reserves.

- Repo facility operations were expanded to include morning sessions.

- Overall, the FOMC is signaling patience with current policy while preparing to pivot if inflation continues to moderate and labor markets soften. The path of tariffs remains a key variable for future policy decisions.

Key takeaways from the FOMC Minutes for the May 2025 meeting:

- Economic Activity: Despite a small decline in Q1 GDP (likely due to measurement issues from import surges ahead of tariffs), underlying momentum (PDFP) remained solid. Labor markets stayed strong, with low unemployment and stable job gains.

- Inflation: Headline PCE inflation was 2.3% YoY (March); core was 2.6%. Inflation has eased since 2022 but remains "somewhat elevated." Tariffs are expected to add upward pressure to inflation, especially in 2025.

- Tariffs and Uncertainty: Participants flagged the larger-than-expected scope and scale of recent tariff increases, which were seen as raising upside inflation risk and downside growth risk. Business sentiment deteriorated, with some firms pausing investment.

- Inflation Strategy Review:

- Participants reaffirmed the 2% inflation target and discussed shifting away from flexible average inflation targeting toward flexible inflation targeting—viewed as more robust in today's environment.

- Market Expectations:

- Markets are pricing in 2–3 rate cuts by year-end, though participants gave no firm guidance.

- The Committee emphasized a "wait and see" approach given heightened uncertainty, especially around trade and fiscal policy.

Key notes on the Fed’s discussion of its policy stance and outlook:

- Policy Stance: The Fed is in a holding pattern, awaiting clearer signals on inflation and economic activity.

- Outlook for Rates:

- Policymakers see elevated risks of both higher inflation (due to tariffs) and higher unemployment (due to trade and business uncertainty).

- Most participants view persistent inflation as a key risk; some worry inflation expectations may drift upward.

- The FOMC will base future moves on incoming data, particularly around inflation, labor markets, and the net effects of government policy changes.

Key note for the FOMC members. Uncertainty around government policies will force the Fed to move with cation in the months ahead:

- "Participants remarked that uncertainty about the net effect of an array of government policies on the economic outlook was high, making it appropriate to take a cautious approach. Emphasizing that uncertainty, a majority of participants noted the potential for inflationary effects arising from various factors to be more persistent than they projected."

Minutes suggest the Fed is worried more about inflation than growth or employment.

- "Some participants observed, however, that the Committee may face difficult tradeoffs if inflation proved to be more persistent while the outlook for growth and employment weakened. Several participants emphasized that elevated inflation could prove to be more persistent than expected.”

The January FOMC Minutes suggests that FOMC members are shifting from its focus on the employment mandate to the inflation mandate.

- “…a couple commented that the risks to achieving the price stability mandate currently appeared to be greater than the risks to achieving the maximum employment mandate.”

- “The Committee was well positioned to take time to assess the evolving outlook for economic activity, the labor market, and inflation, with the vast majority pointing to a still-restrictive policy stance. Participants indicated that, provided the economy remained near maximum employment, they would want to see further progress on inflation before making additional adjustments to the target range for the federal funds rate.”

- “Participants generally pointed to upside risks to the inflation outlook. In particular, participants cited the possible effects of potential changes in trade and immigration policy, the potential for geopolitical developments to disrupt supply chains, or stronger-than-expected household spending.”