FOMC Minutes: September 2025 Meeting

Key takeaways from the FOMC Minutes for the September 16-17, 2025 meeting:

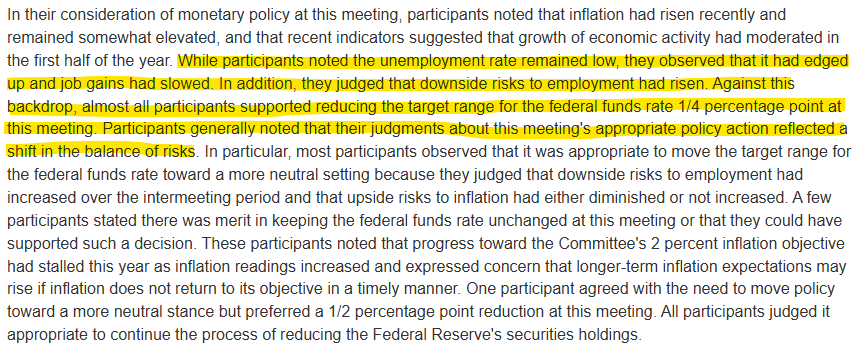

- The FOMC cut the federal funds rate -25 bps to 4.00–4.25% at the Sept 16–17, 2025 meeting, citing softer labor markets and still-elevated inflation, and emphasized a shift toward balanced risks with policy “not on a preset course.”

-

Markets & expectations: Following weaker July–Aug jobs data, survey and market pricing pointed to ~2–3 additional -25 bp cuts by year-end; Treasury yields fell 20–40 bps (bigger at the front end), the curve steepened slightly, and equity indexes moved near record highs while credit spreads stayed tight.

-

Money markets & balance sheet: Repo rates firmed amid higher TGA balances; SRF take-up hit $1.5B on Sept 15. If runoff continues, the SOMA portfolio is seen just over $6T by end-March, with reserves near ~$2.8T by end-Q1.

-

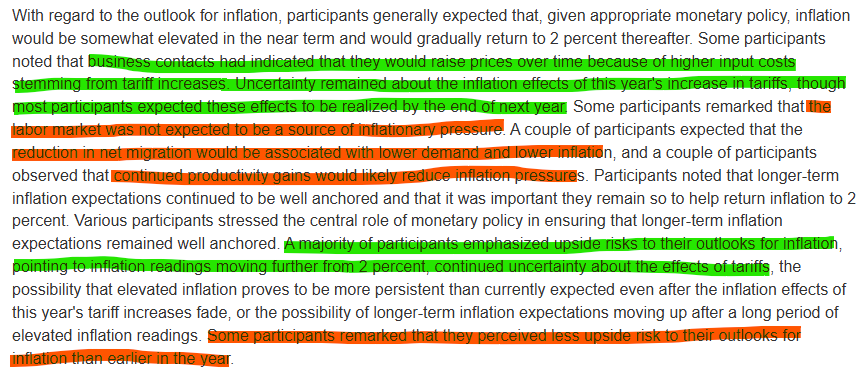

Inflation: PCE 2.7% YoY (Aug) and core PCE 2.9% YoY were at the upper end of this year’s range; participants saw tariff effects lifting prices near term but expected a gradual return to 2% over time.

- Most of the division in the Fed seems to be centered on the inflation outlook. Inflation hawks are worried about tariff price pressures and how long they could last. Inflation doves point to lower net migration, a weak labor market, and productivity gains.

-

Labor market: Conditions softened: unemployment 4.3% (Aug); payroll gains weak with a preliminary -900k benchmark revision to March levels; vacancies/unemployed ≈ 1.0; wage growth slowed (ECI +3.5% YoY; AHE +3.7% YoY).

-

Growth: Real GDP moderated in H1; staff revised up GDP a bit for 2025–2028 on firmer consumption/investment and easier financial conditions, but housing remained weak; high-tech capex was a relative bright spot.

-

Risk assessment: Participants judged downside risks to employment had risen; upside inflation risks remained but had diminished or not increased for many. Most anticipated further easing later in 2025, data-dependently.

-

Credit conditions: Borrowing costs fell but stayed elevated vs post-GFC norms; credit broadly available for larger firms and prime households, tighter for small businesses and lower-score borrowers; CMBS delinquencies elevated; card/auto delinquencies elevated but little changed.

- The September minutes confirm that the labor market was at the center of the cut, and that virtually all FOMC members saw a "shift in the balance of risks" in the weak employment data that had come out before the meeting.

-

Vote & dissent: Decision passed with one dissent—Governor Miran preferred -50 bps, citing further labor softening, inflation nearer 2%, and a lower neutral rate given tariff revenues and lower immigration.