Federal Reserve Monetary Policy Decision: March 2026

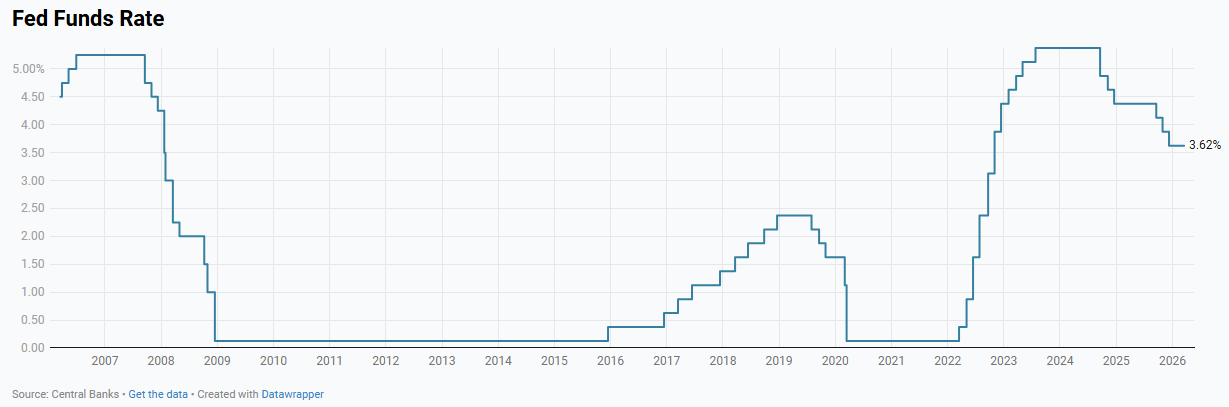

The Federal Reserve held the federal funds rate unchanged at 3.50%–3.75% in March 2026, while revising growth and inflation projections higher and signaling increased concern about persistent price pressures.

-

The FOMC left the policy rate unchanged at 3.50%–3.75%, with an 11–1 vote (Miran dissenting for a -25 bp cut), indicating a continued pause but with less support for easing compared to January when multiple members favored cuts.

-

Statement changes were minimal, with unemployment described as “little changed” rather than stabilizing, suggesting no meaningful shift in the Fed’s assessment of labor market conditions.

-

Growth projections were revised higher across 2025–2027 and the longer run, reflecting stronger productivity and demand dynamics, though risks to growth were viewed as more skewed to the downside.

-

Unemployment projections were largely unchanged, with only a small upward revision to the 2027 estimate (+0.1 ppt to 4.2%), indicating limited reassessment of labor market conditions despite increased uncertainty.

-

Headline PCE inflation projections were revised higher, with the 2026 median rising to 2.7% (Dec: 2.4%), reflecting the impact of higher energy prices, while risks to inflation were assessed as tilted to the upside.

-

Core PCE inflation projections also increased, with 2026 and 2027 medians revised up to 2.7% and 2.2%, respectively, indicating firmer underlying inflation pressures beyond energy-related effects.

-

Despite higher growth and inflation projections, the median expected rate path remained largely unchanged, with only a +0.1 ppt increase in the long-run rate to 3.1%, suggesting some hesitation to adjust policy expectations more aggressively.

-

Market reactions reflected a more hawkish interpretation, with equities declining (S&P 500 -1.36%), Treasury yields rising (2-year +10 bps), and the USD strengthening, consistent with reduced expectations for rate cuts.