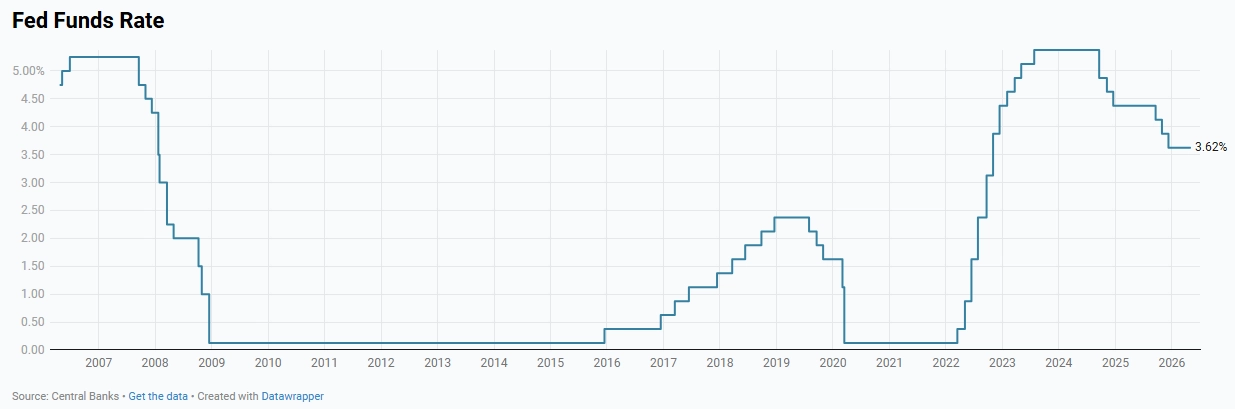

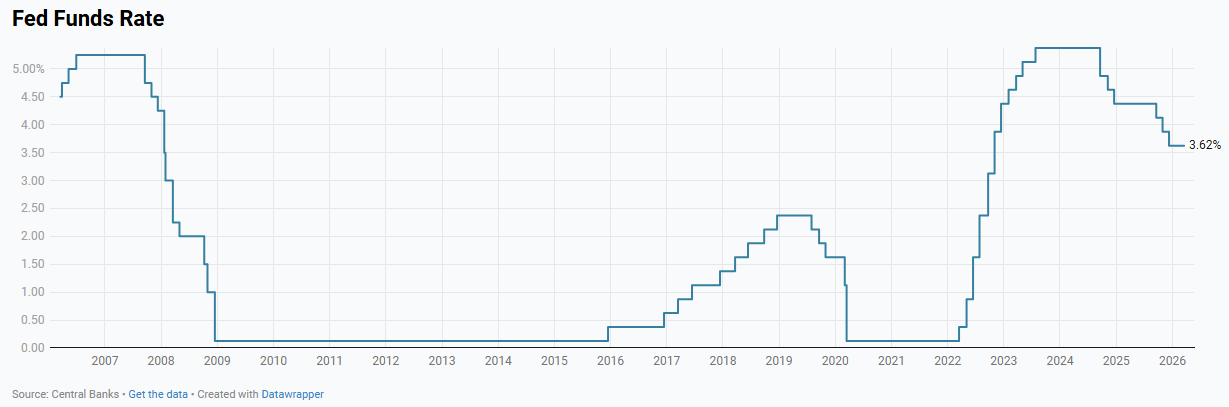

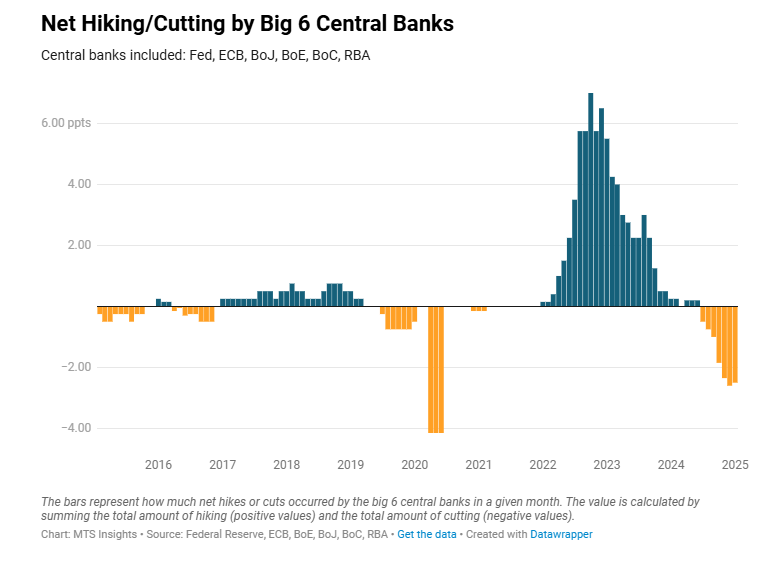

The long-awaited 2025 rate cut has finally come after six meetings. The Federal Reserve lowered its policy rate by a quarter point in September, marking the first reduction since December 2024. The decision reflects a significant shift in the Fed’s balancing act: labor market deterioration has become too evident to ignore, even as inflation remains elevated. September’s move also came alongside fresh projections and a carefully worded press conference, both of which carried a distinctly hawkish tone that underscored the Fed’s determination to guard against lingering price pressures while acknowledging softer labor conditions.

Statement

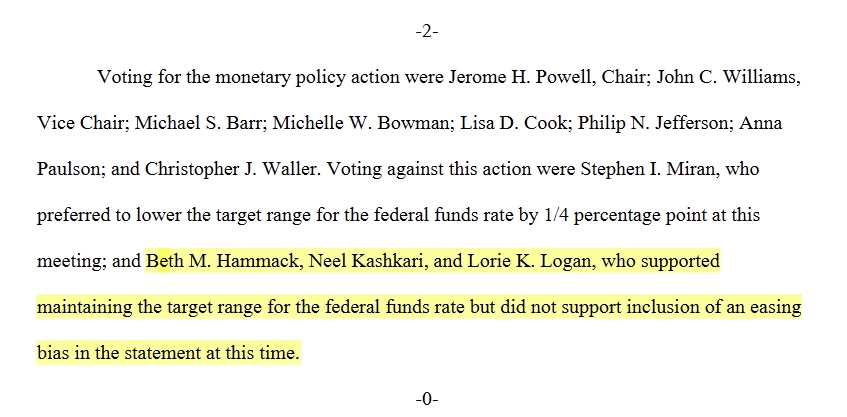

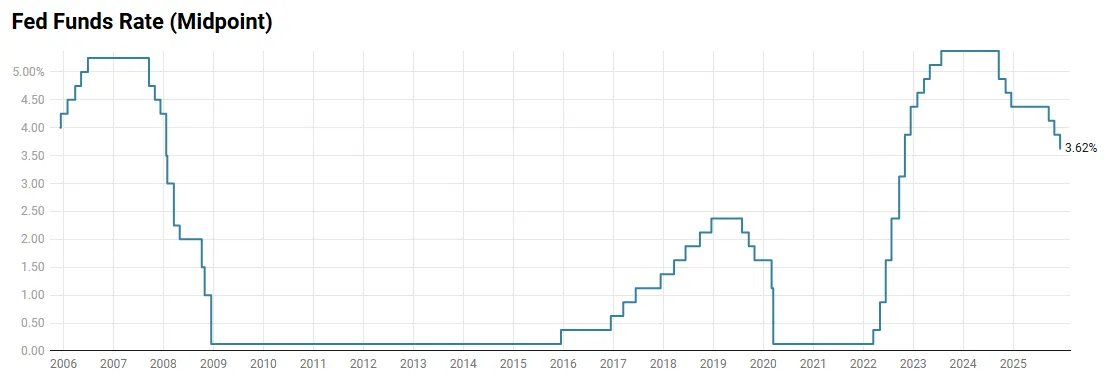

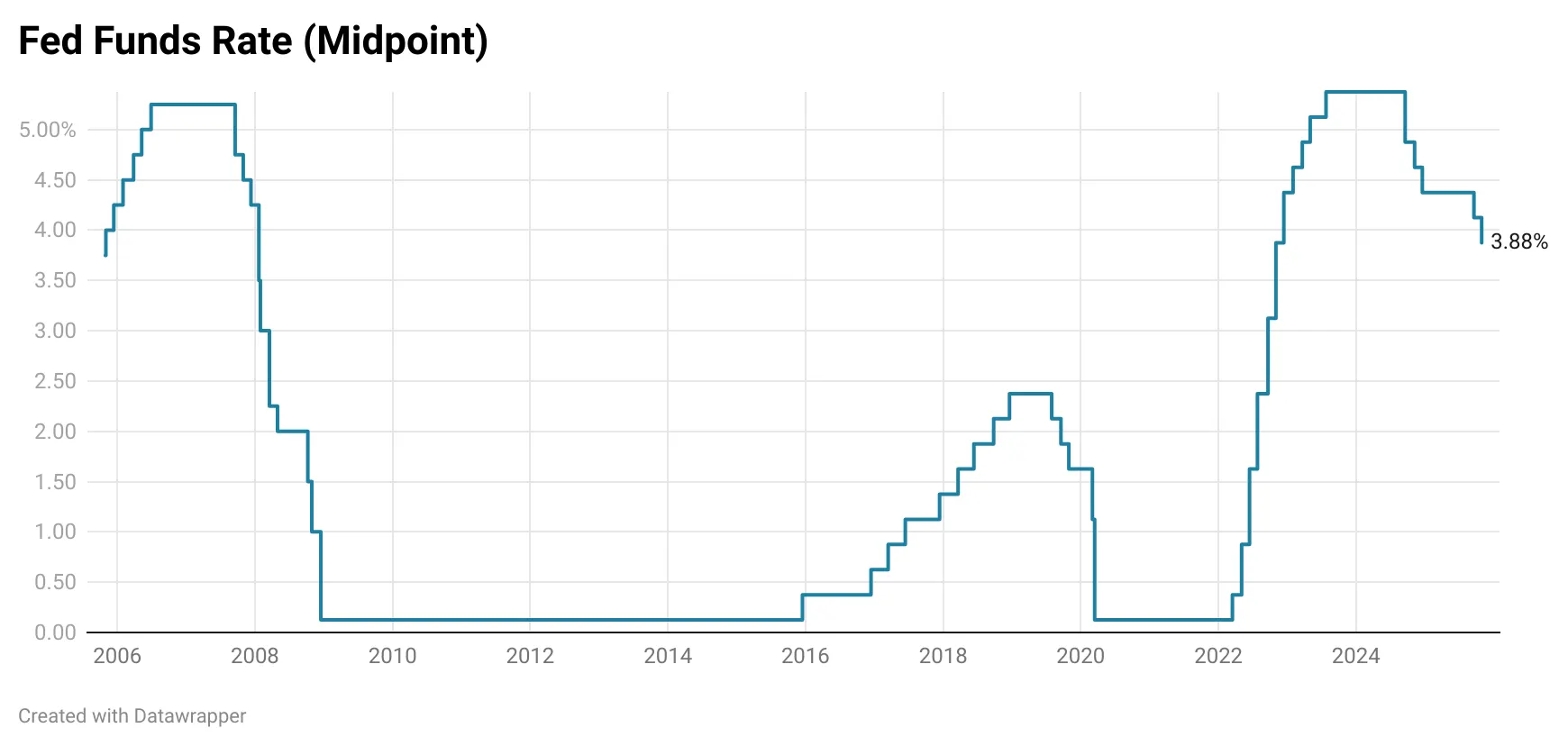

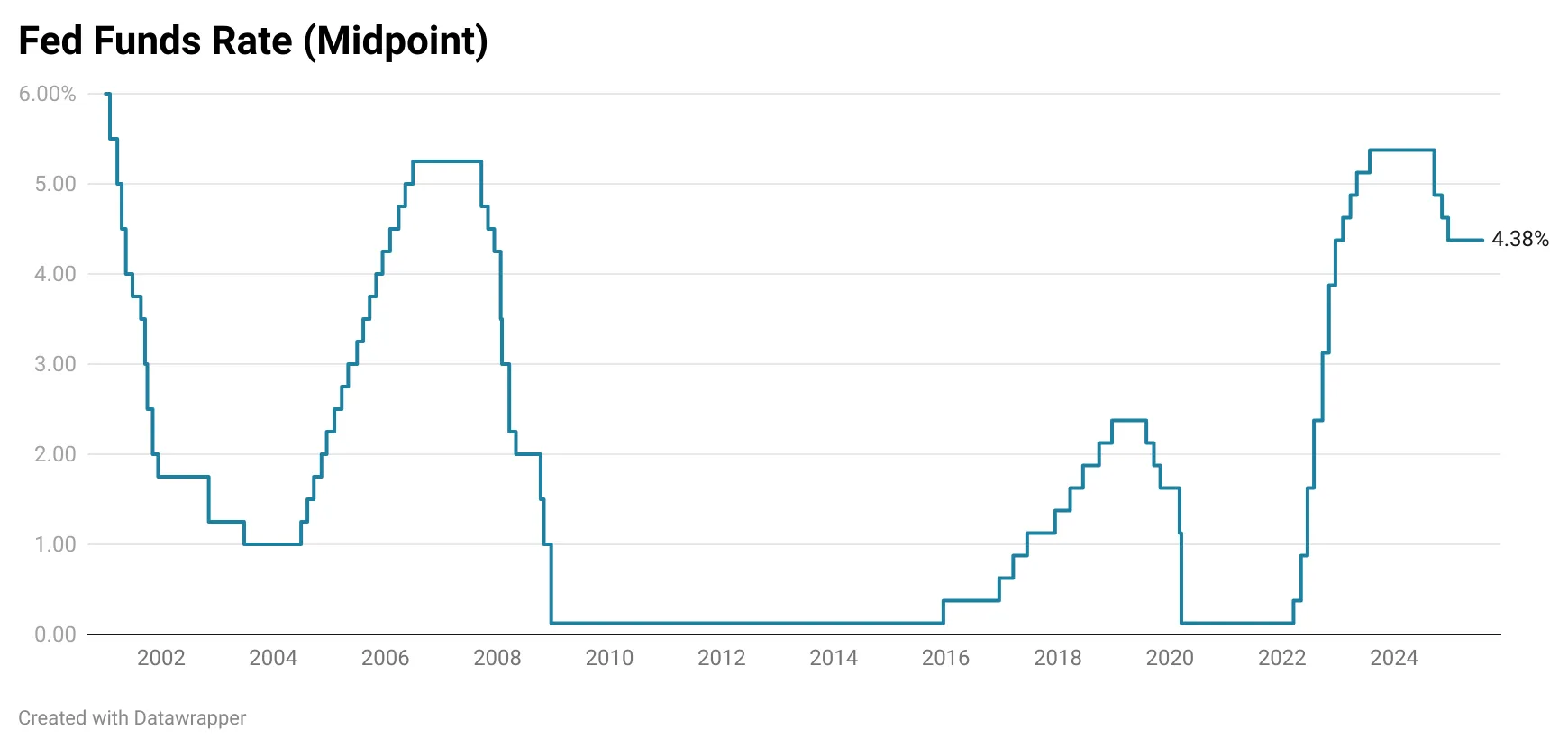

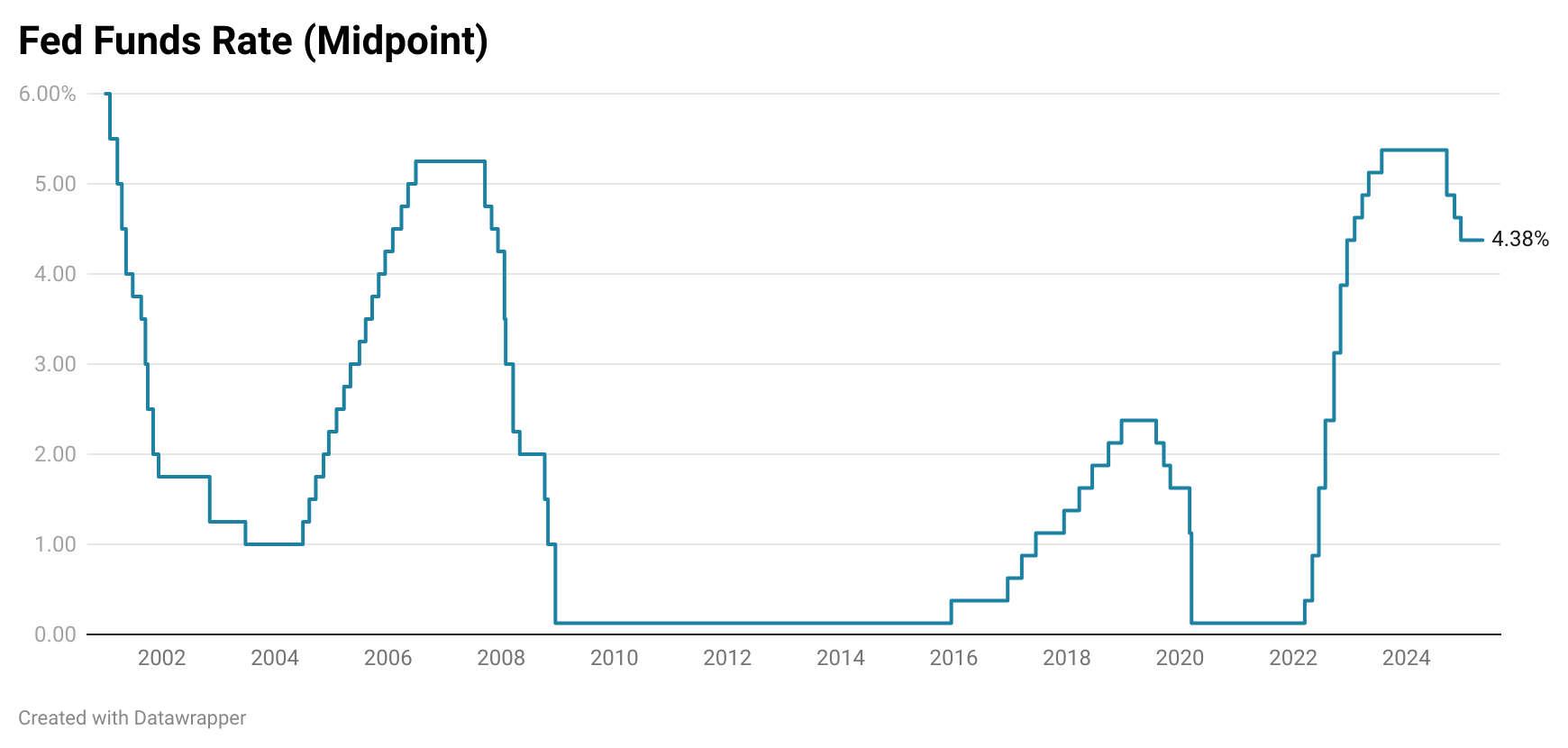

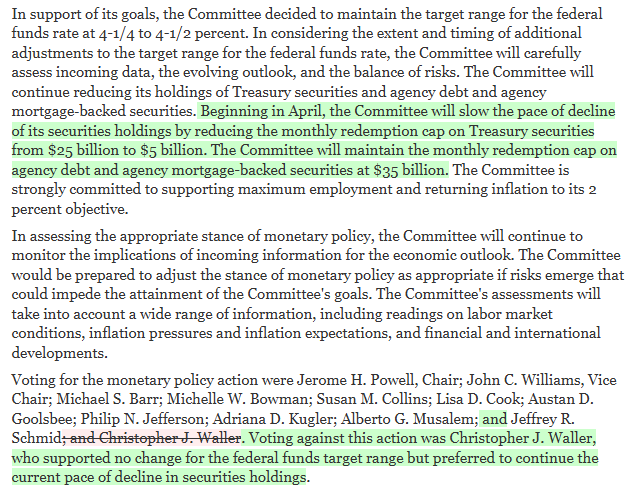

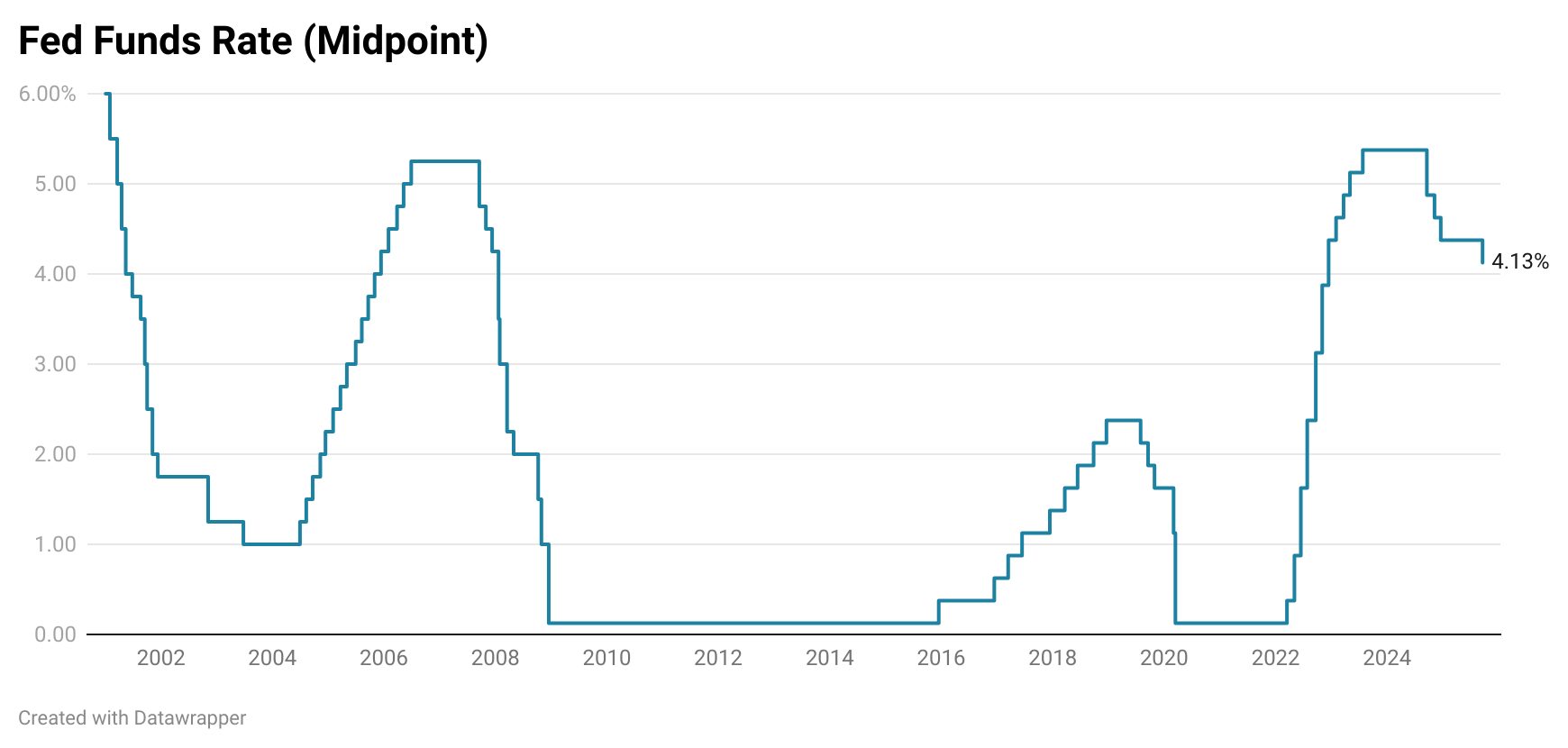

The Federal Reserve voted to reduce the target range for its federal funds rate by 25 bps to a range from 4.00% to 4.25% following the September FOMC meeting. This is the first time the rate has been cut since December 2024, and the new range is the lowest since December 2022 (right before the Fed hiked by 50 bps). The decision to cut by a quarter point was supported by all members except for one. The newly appointed Stephen Miran dissented in his first FOMC meeting, preferring to cut the federal funds rate by 50 bps to a range of 3.75% to 4.00%. The two dissenters from the July meeting, Michelle Bowman and Christopher Waller, both kept their votes for a quarter-point cut in this meeting.

The press release came with more changes than usual in September, briefly highlighting some of the shifts in the assessment of the US economy since the July meeting:

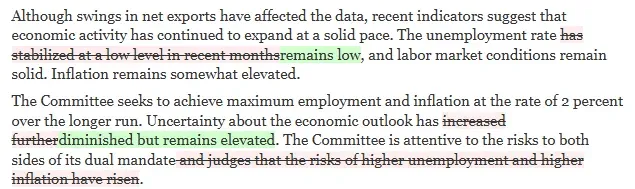

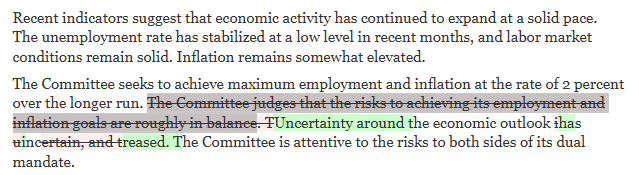

- The changes in the first paragraph are reflective of shifts in data that have occurred since the July meeting. The statement seeks to acknowledge the newfound weakness in the labor market that is evidenced by slower growth in job gains and a gradual, but significant rise in the unemployment rate. The Fed also removes its assertion that labor market conditions are “solid.” The shift away from this narrative underpins the FOMC’s decision to cut.

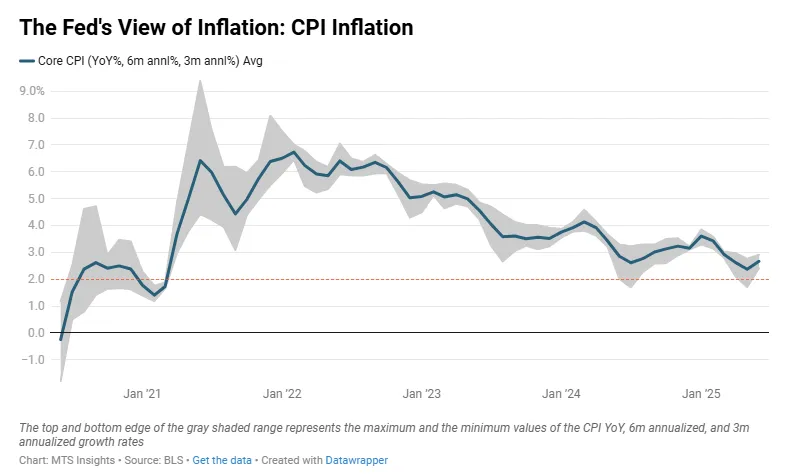

- In the same paragraph, it admits that inflation “has moved up” and confirms its assessment that inflation “remains somewhat elevated.” One might be surprised to find this change of wording in a Fed statement that later goes on to share the decision to cut rates, and they would usually be correct to be. There are only two ways to make sense of this: 1) the Fed is talking about inflation rising due to tariffs, which it sees as transitory, or 2) the labor market is deteriorating to such a degree that policymakers are ignoring a rise in inflation.

- The change in the second paragraph may provide an answer to that question on inflation. The statement contains a new line that communicates that the Fed now sees stronger “downside risks to employment” than they did in the last meeting. And since they did not mention a rise in the upside risks to inflation, the observed tick up in inflationary pressures is not leading to a more prolonged inflationary threat.

The changes in the statement lay out the reasoning for the rate cut today. Not only did the Fed see a significant deterioration in the labor market in the July and August jobs reports, but it sees a further rise in joblessness in the near future. More generally, the Fed is saying loud and clear that its focus has shifted away from the inflation mandate, even though inflation accelerated, towards the employment mandate.

Summary of Economic Projections

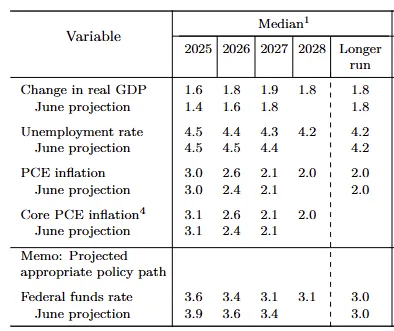

The significance of this meeting lies not only in being the first rate cut in nearly a year, but also in the release of a new set of projections in the September 2025 edition of the Summary of Economic Projections (SEP). This marked the first update since June, when policymakers presented a notably different view of the labor market. While the statement acknowledged a shift in labor market conditions, the September projections ultimately proved to be less convincing:

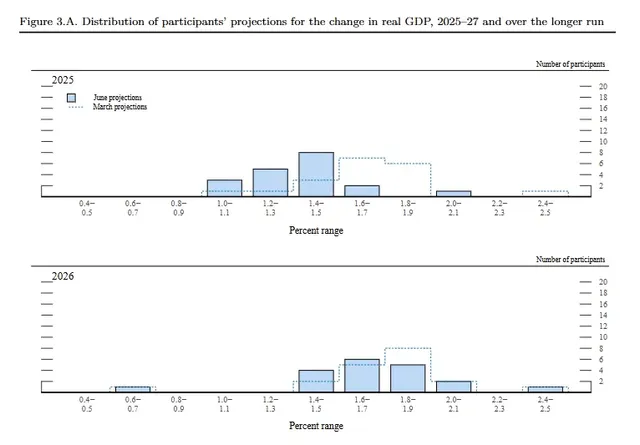

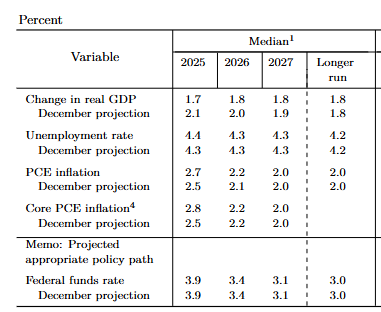

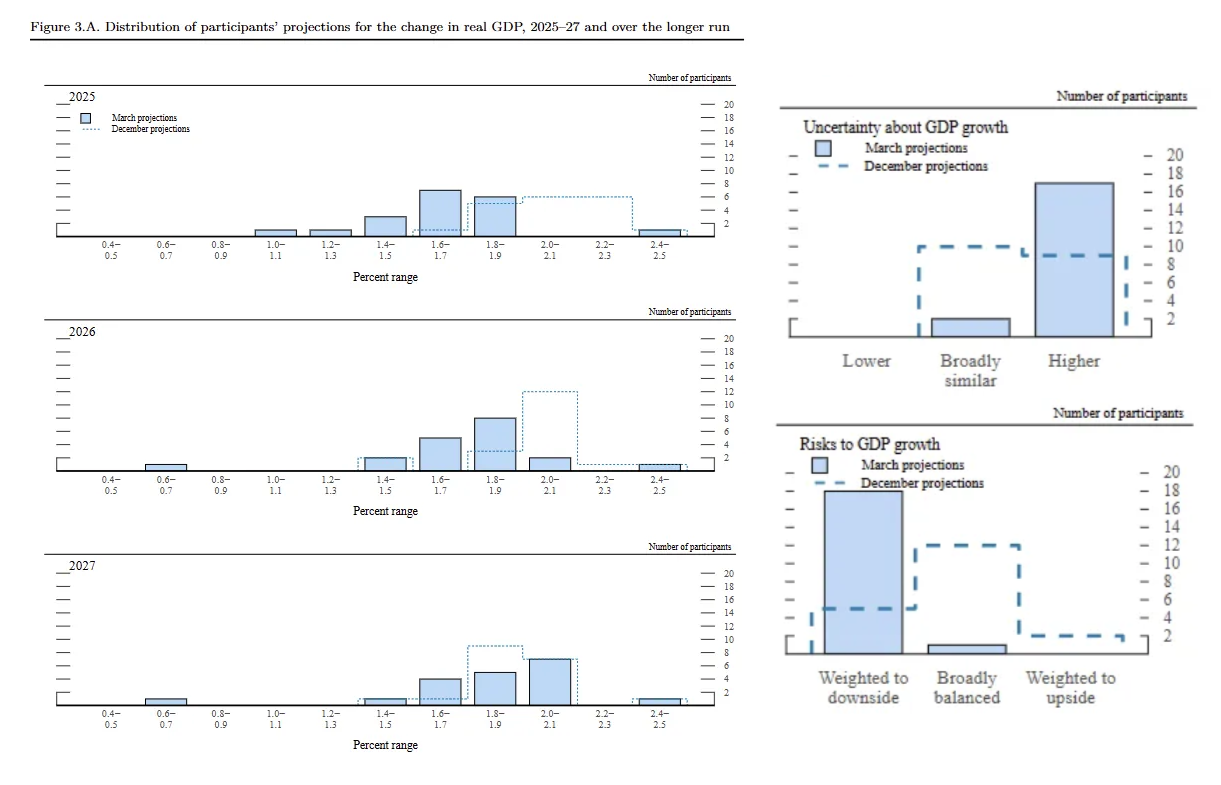

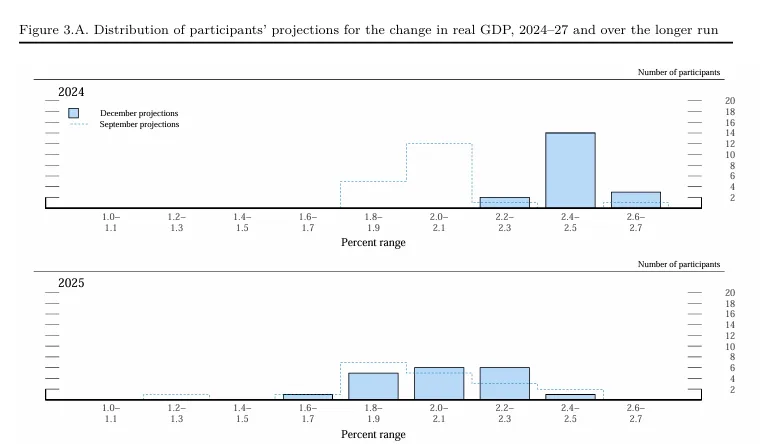

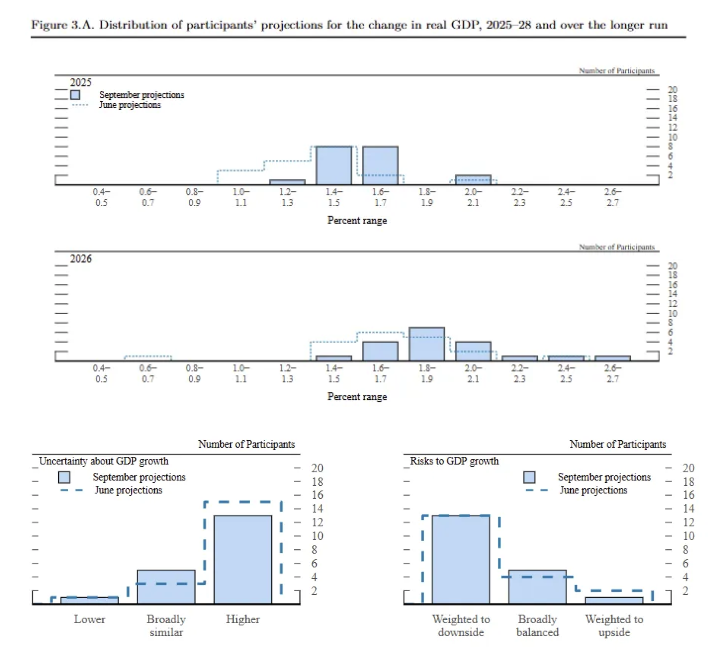

- FOMC members were broadly more optimistic about GDP growth in the September SEP compared to three months ago. The median projection of GDP growth was revised up across the next three years: up 0.2 ppts to 1.6% in 2025, up 0.2 ppts to 1.8% in 2026, and up 0.1 ppts to 1.9% in 2027. The bottom ends of the forecasts for all three years were also revised up, suggesting a broad-based assessment that the tariff worst-case scenario has been avoided. While these adjustments look optimistic, FOMC members did not shift their views on the risks to growth, as the same number of participants citing heavier downside risks in June said the same in September.

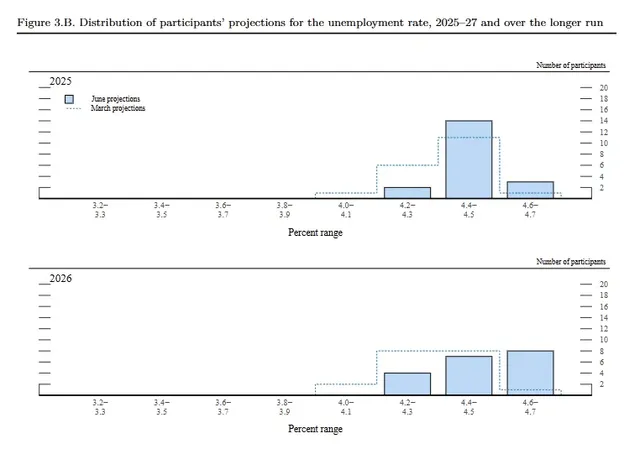

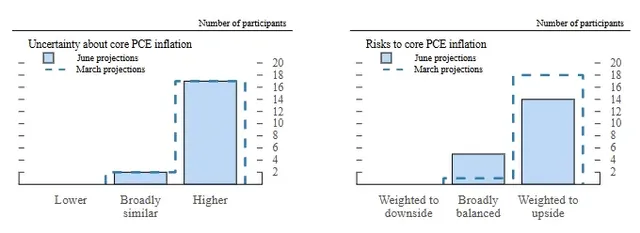

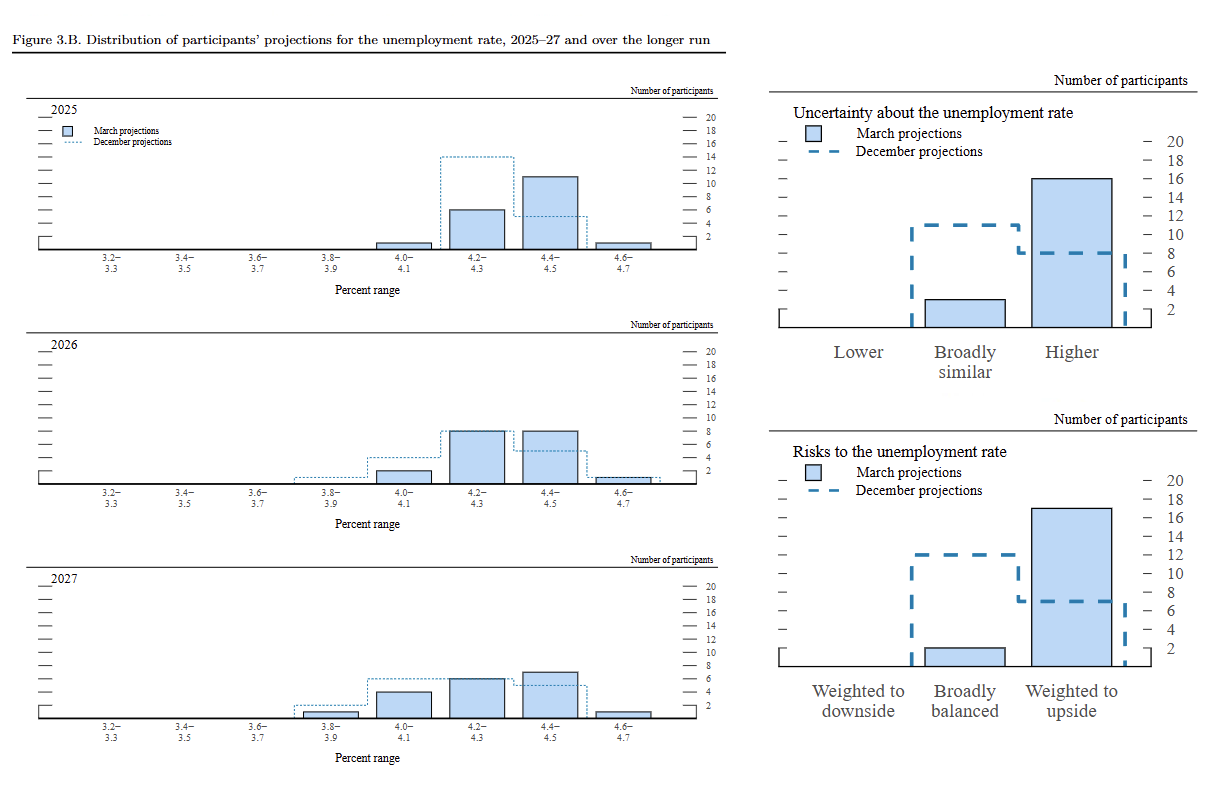

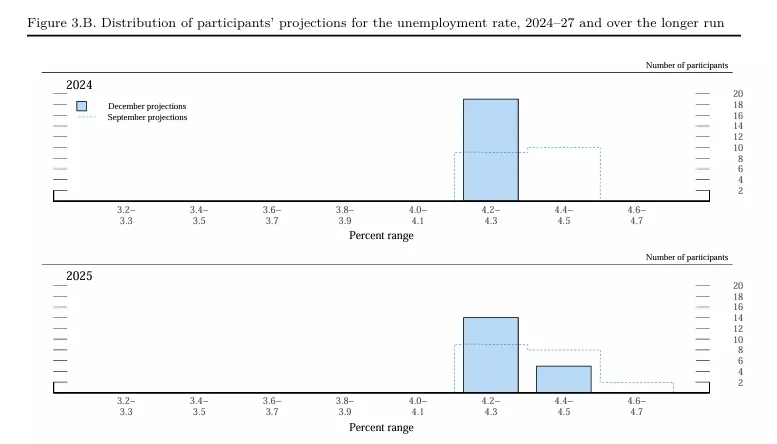

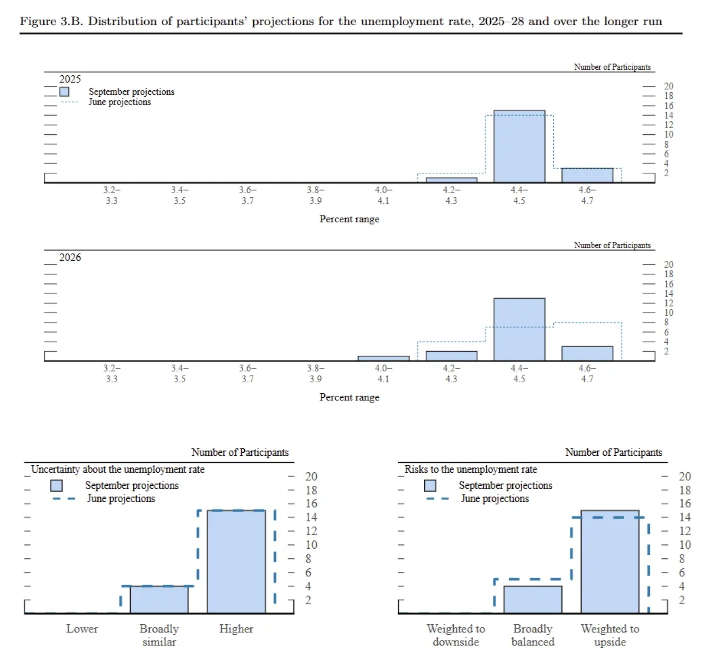

- The Fed just cut rates and pointed to weakness in the labor market as the main motivation for that cut, so one would assume that it would become more pessimistic in its unemployment rate forecast. Well, that is not the case. The September SEP revealed downward revisions to the projections of the unemployment rate in 2026 and 2027, each down -0.1 ppt to 4.4% and 4.3%, respectively, while the 2025 projection remained at 4.5%. The revisions in the next two years were caused by a tightening of the range of forecasts at both ends, driving a greater consensus in the middle. Despite projections moving lower and becoming tighter around the median, FOMC members still see risks entirely weighted to the upside, with only 4 members seeing risks “broadly balanced.”

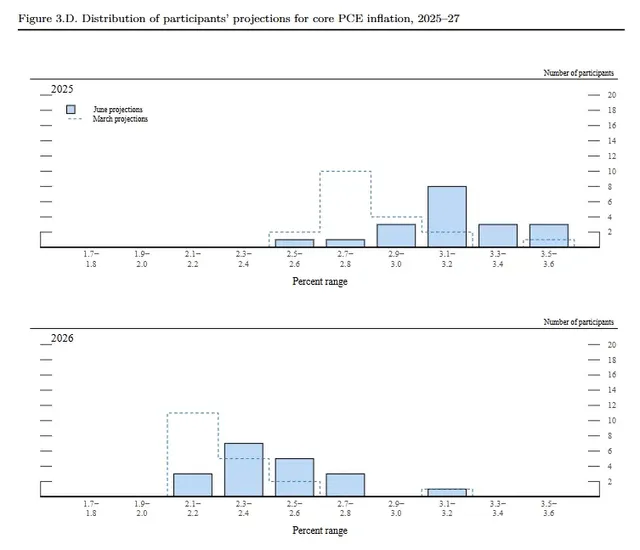

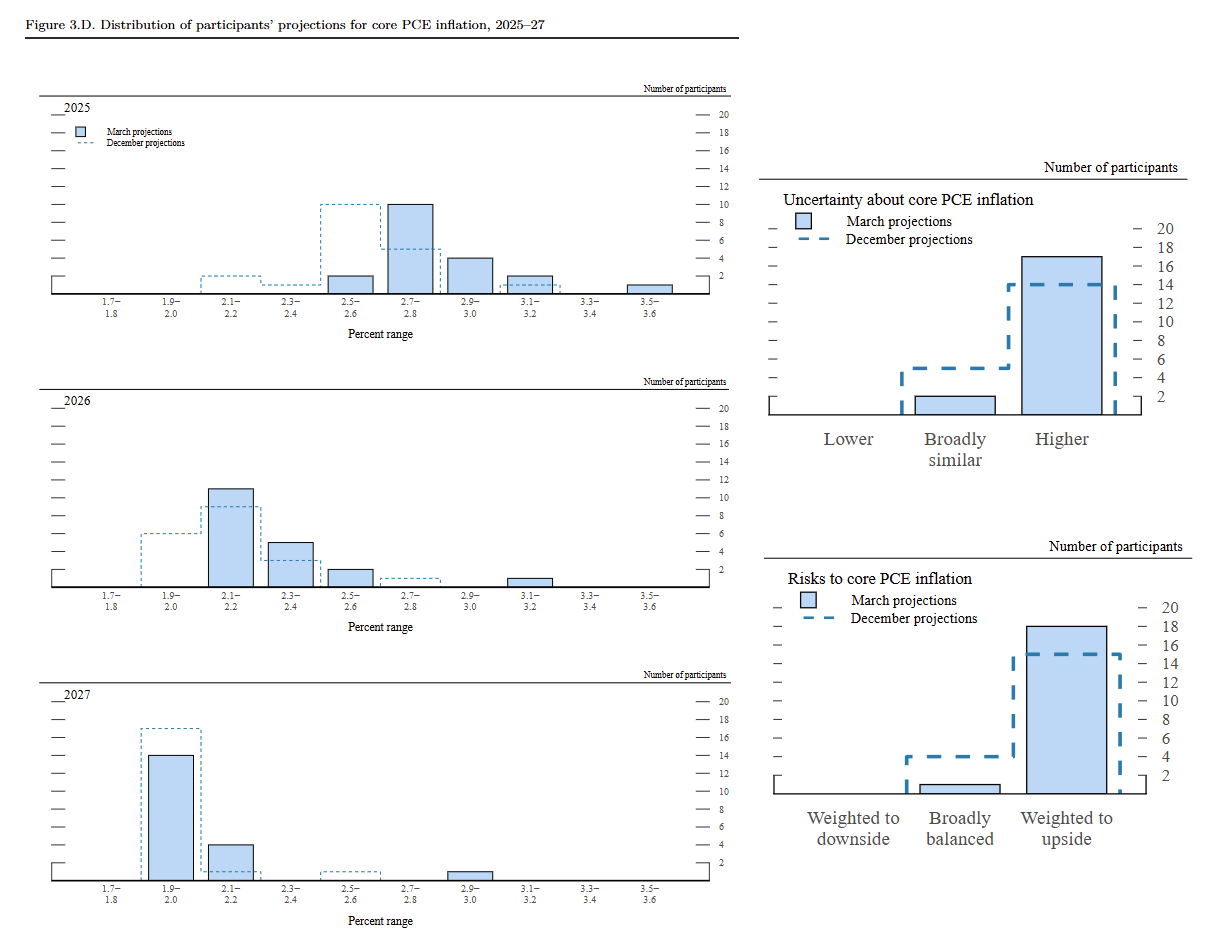

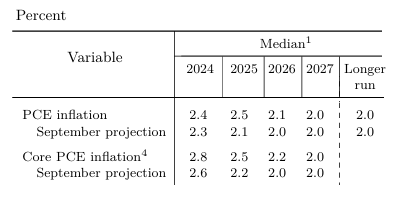

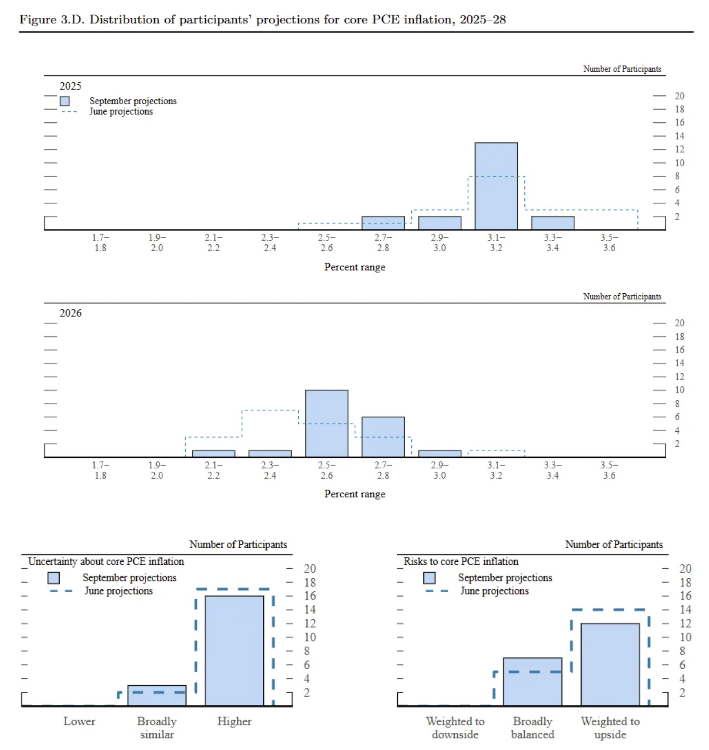

- The forecasts for PCE and core PCE inflation were the least unchanged out of all of the indicators in the SEP. Despite there being a shift in the intensity of tariff policy, the median projections of PCE and core PCE inflation in 2025 remained unchanged at 3.0% and 3.1%, respectively. The adjustments for each came in the 2026 forecast,s where both headline and core projections were revised up 0.2 ppts to 2.6%. This would suggest to me that the Fed sees the tariff inflation being less transitory than it may have thought before. In the assessment of risks, FOMC members were slightly less concerned about the upside risks to inflation than in June.

Overall, the September SEP does not seem to align neatly with the Fed’s decision to cut rates by a quarter point. The projections paint a more optimistic picture of the economy, with stronger GDP growth and a lower unemployment rate expected over the coming years, and inflation forecasts suggest policymakers now view tariff-related pressures as more persistent than previously assumed. These would be seen as hawkish shifts in the Fed’s views of the US economy. Despite the rosier projections, FOMC members placed greater weight on upside risks to unemployment and dialed back concerns about inflation, suggesting it was this shift in the balance of risks, rather than the projections themselves, that ultimately drove the rate cut.

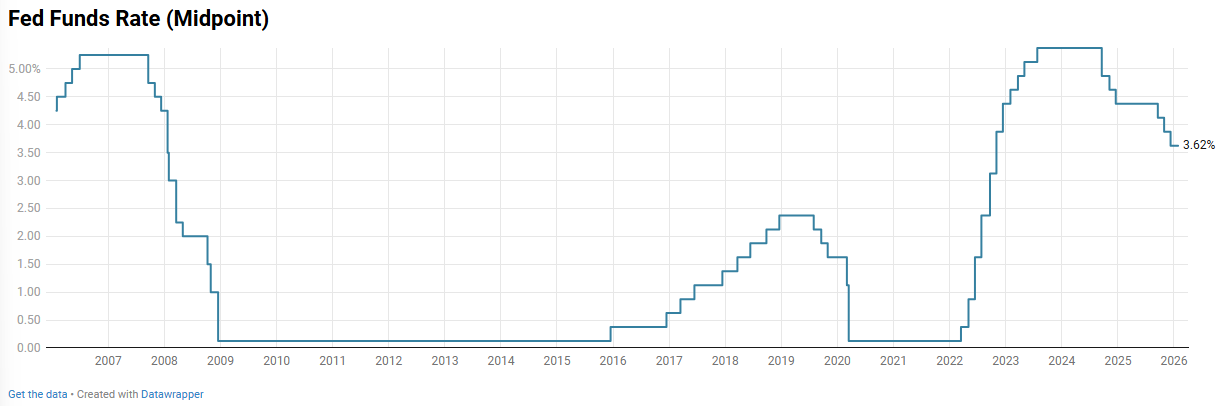

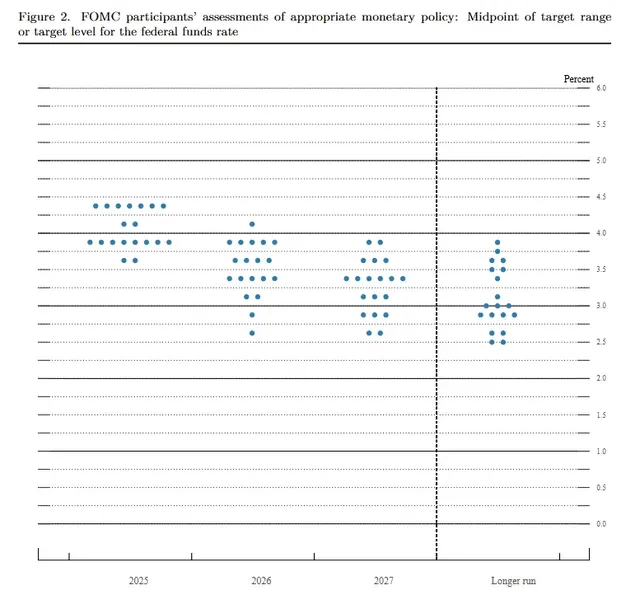

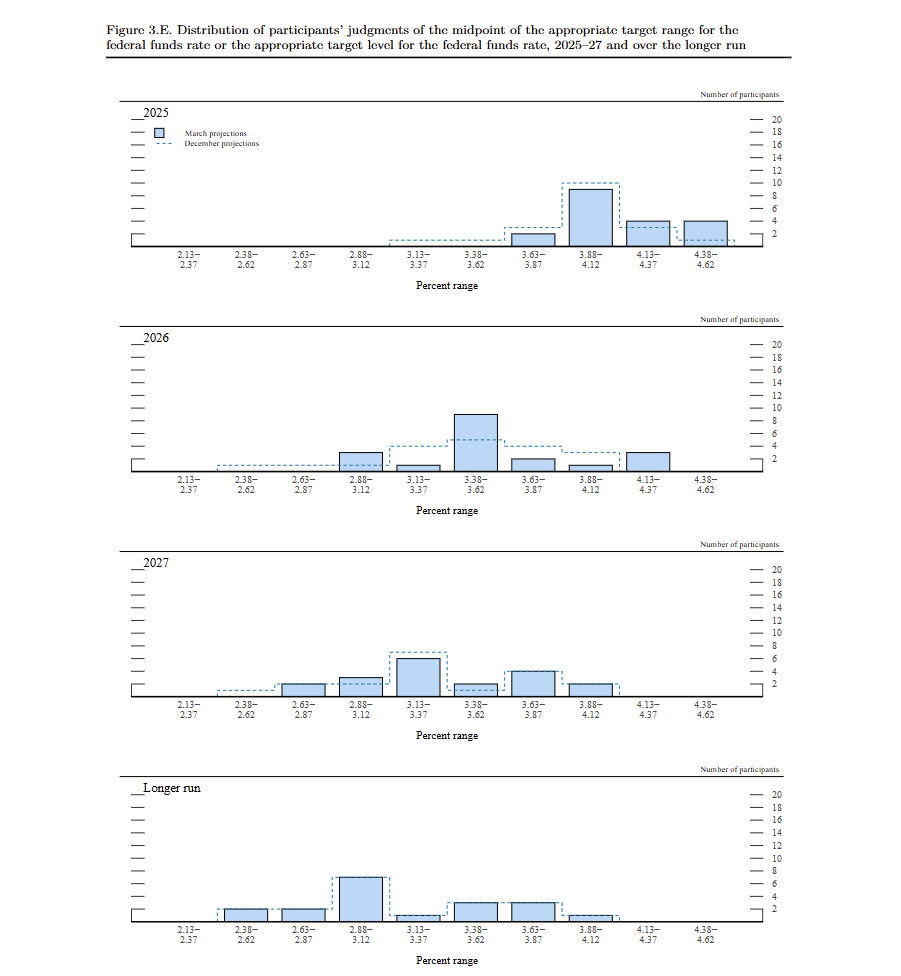

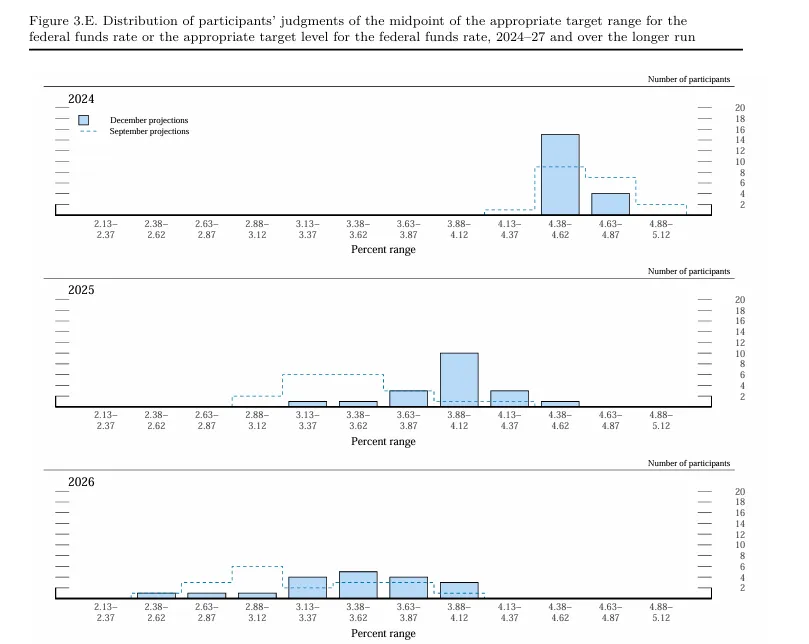

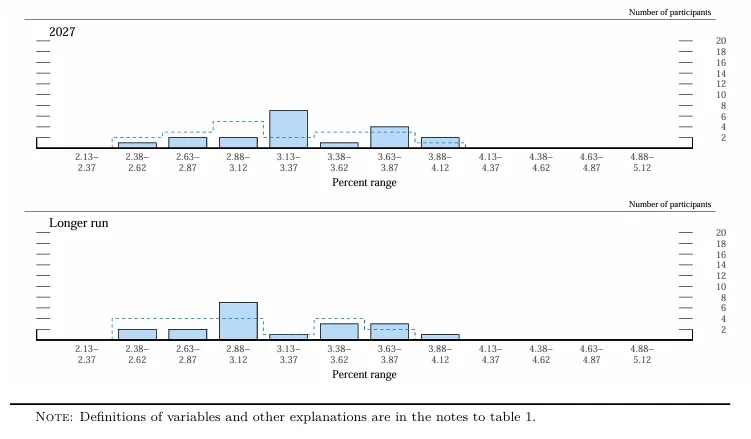

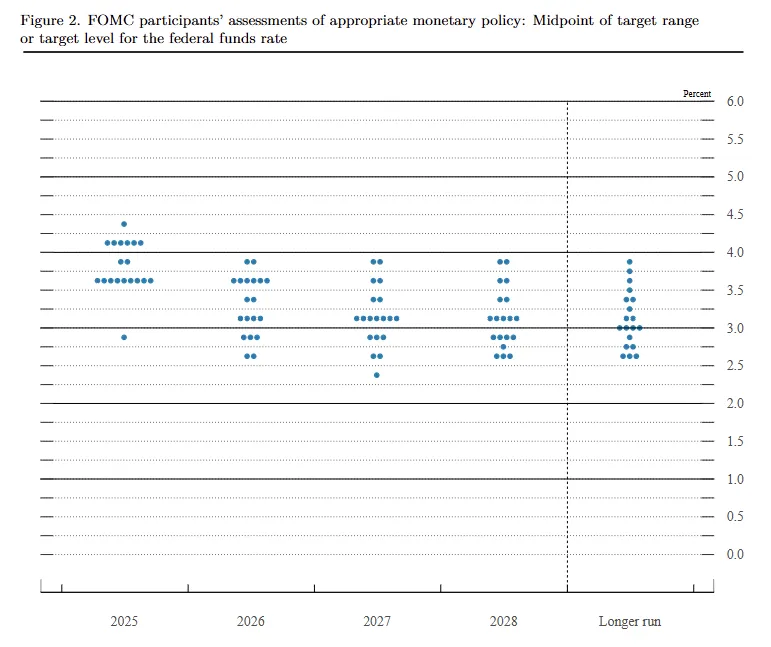

The shift in the balance of risks clearly drove the Fed’s decision to cut rates at this meeting, but the policy rate projections tell a slightly different story. The median forecast for the federal funds rate was revised down by about 25 bps in each of the next three years, placing the midpoints at 3.625% in 2025, 3.375% in 2026, and 3.125% in 2027. These uniform adjustments appear less about a new economic outlook and more about correcting the policy stance to reflect the weaker labor market revealed earlier this year. In other words, while the immediate cut was guided by risk assessments, the longer-term policy path remains largely consistent with June’s projections, with some optimistic revisions pointing to stronger growth, lower unemployment, and slightly higher inflation.

Press Conference

Opening Statement

Powell’s opening statement for the press conference laid out the thinking behind the Federal Reserve’s decision to cut before taking questions. His assessment of the economy was actually very similar to his address at Jackson Hole in August:

- Powell noted that the “growth of economic activity has moderated” so far this year. This includes a slowdown in consumer spending and weakness in the housing sector.

- In the labor market, Powell highlights a slowdown in the demand for hiring and a decline in the labor supply, both contributing to stagnation in the labor market. He describes this “less dynamic” labor market as “unusual,” reflecting language used in his Jackson Hole speech. Powell suggests that this stagnation has caused the “downside risks to employment to have risen.”

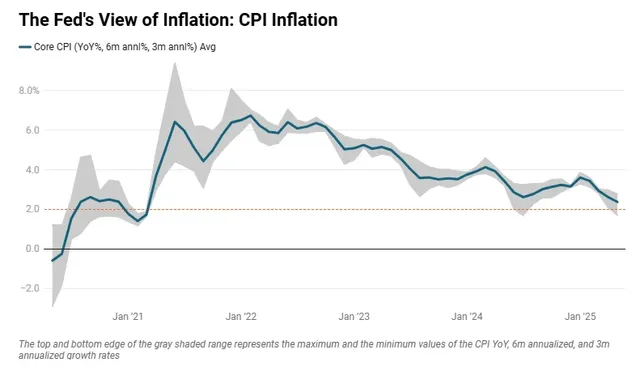

- While inflation has come down from its 2022 peaks, Powell continues to describe inflation as “somewhat elevated” relative to the Fed’s target. He specifically points to a pick-up in goods inflation as the reason for higher inflation readings earlier this year. It seems that for now, the Fed’s base case is that the effects of tariffs on inflation “will be relatively short-lived, a one-time shift in the price level.” However, Powell notes that there is still uncertainty surrounding the effects of tariffs and asserts that it is the Fed’s “obligation” to ensure that tariff inflation does not become entrenched.

He ended his opening statement discussing the September SEP and policy outlook. Powell noted that the Fed’s median projection for the federal funds rate was lowered by 25 bps across the forecast horizon, to 3.6% in 2025, 3.4% in 2026, and 3.1% in 2027. He stressed that this path is “not a preset course,” but rather reflects individual participants’ views under their most likely scenarios. The decision to cut rates now, he explained, stemmed from a shift in the balance of risks, with “downside risks to employment” rising and concerns over inflation pressures easing. Powell framed the move as another step toward a more neutral stance, leaving the Fed “well positioned to respond in a timely way to potential economic developments.”

Despite the quarter-point cut, Powell’s opening struck a distinctly hawkish tone. His language echoed closely from Jackson Hole, suggesting the decision to ease was already taking shape after the weak July jobs revisions, with the soft August payrolls simply reinforcing it. That context matters because Powell framed the move less as the start of an easing cycle and more as risk management, aimed at recalibrating policy closer to neutral. At the same time, he underscored that inflation remains “somewhat elevated,” highlighted upside risks to prices from tariffs, and stressed the Fed’s “obligation” to prevent temporary shocks from becoming entrenched. By pairing the modest cut, sparked by a newfound softness in the labor market, with firm inflation vigilance and continued balance-sheet runoff, Powell is keeping doves who are calling for consecutive rate cuts at bay.

Q&A

Here are some questions of note in the Q&A portion of the conference:

- Are tariffs slowing the labor market more than showing up in inflation? - Powell: “It’s certainly possible.” Goods prices are contributing “most of the increase in inflation” this year, effects are “not very large” yet but may “continue to build.” On jobs, he pointed to lower immigration and participation and softer demand: a “curious balance” where both supply and demand fell, with demand falling more as unemployment rises. At the very least, it seems the impact of inflation has been less than what the Fed expected.

- Do economic conditions and the balance of risks no longer warrant a “restrict” policy setting? - Powell: “I don't think we can say this.” Earlier this year, policy was clearly restrictive with a strong labor market. He suggests revised payrolls mean “I can no longer say" that the labor market is strong. Risks were tilted towards inflation and have moved “meaningfully toward greater equality.” Despite that balance, Powell notes that the Fed should be “moving in the direction of neutral” but not necessarily that monetary policy should not be restrictive. This is the tone of a hawkish cut.

- Is AI dampening labor demand already? And what policy implications does this have? - Powell says that effects are possible but “not the main thing” driving labor market dynamics and its “hard to say how big it is.” He points out that this trend may be more visible for new grads. In general, multiple forces are slowing job creation.

- What evidence shows tariffs in inflation?- Powell points to how goods inflation moved from negative last year to ~1.2% YoY this year. He estimates that tariffs may be contributing “0.3–0.4 ppts” to 2.9% inflation. Notably, Powell admits that consumer pass-through is “slower and smaller than we thought,” but “there’s some pass-through.”

- Why a strong consensus for a cut, yet scattered dots about the path? - Powell says that there was broad recognition that labor-market risks have risen from “downside risks” to a “reality.” Nearly everyone supported this cut (except for Mian), but views differ on what’s next given unusually challenging trade-offs. This gives me confidence on my thought that the cut today was an admission that they should’ve cut once in Q2, but employment data was unclear.

- Is there tension between strong Q3 activity and downside labor risks? - This question seems to try to get Powell to address the divergence between the optimism, the outlook, and the cut today. Powell first claims that there’s not really tension in these things, citing AI and business investment as driving activity. He clarifies that today’s decision to cut was focused on labor-market risks rather than big changes in inflation or labor projections.

- The Q&A session featured several questions about Federal Reserve independence in various forms (referencing Miran’s addition to the FOMC, Bessent’s suggestion of “mission creep” and a review). Powell remained diplomatic in these instances and declined to explicitly comment as he always has, and he consistently reasserted that the Fed would be “strongly committed to maintaining its independence.”