IEA Oil Market Report: January 2026

Highlights

-

Global oil demand growth is forecast to average 930 kb/d in 2026, up from 850 kb/d in 2025, reflecting a normalisation of economic conditions after last year’s tariff turmoil and lower oil prices than a year ago. A recovery in petrochemical feedstocks demand will be partially offset by a continued slowdown in gasoline gains. Non-OECD countries will once again account for all of the growth in 2026.

-

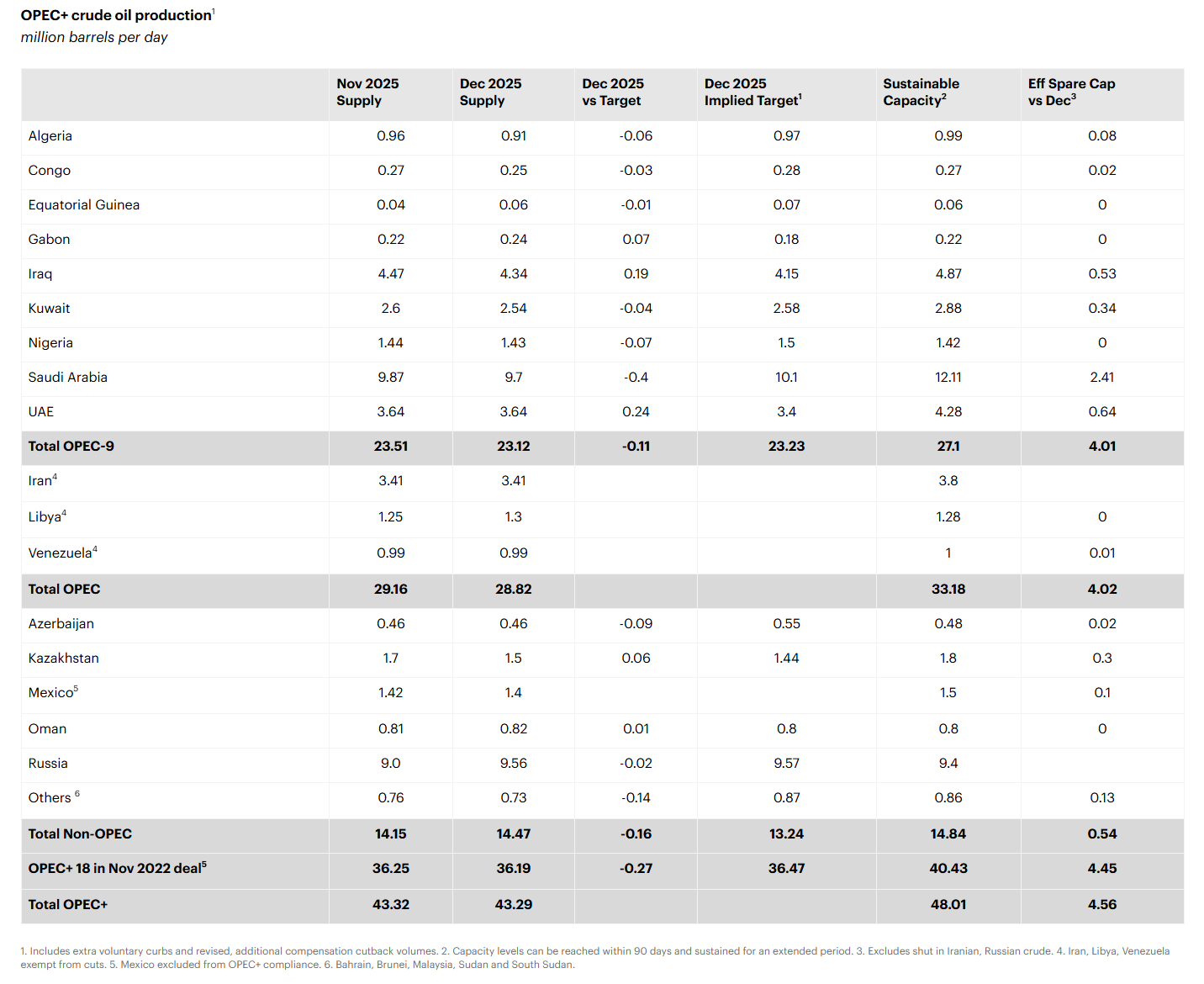

Global oil supply fell by 350 kb/d m-o-m to 107.4 mb/d in December, 1.6 mb/d below September’s record high. Lower output from Kazakhstan and a number of Middle Eastern OPEC producers was partly offset by a sharp rebound in Russian production. World oil supply is now projected to rise by 2.5 mb/d this year to 108.7 mb/d, following an increase of 3 mb/d in 2025. Non-OPEC+ accounts for 1.8 mb/d of the gains in 2025 and 1.3 mb/d in 2026.

-

Global refinery crude throughputs surged by 2 mb/d to 85.7 mb/d in December, ahead of 1Q26 seasonal maintenance in the United States, Europe, the Middle East and Asia. Crude runs are forecast to average 84.6 mb/d for 2026, with annual growth of 770 kb/d slightly below 2025’s 930 kb/d pace. Refining margins slumped over the course of December, led by weaker profitability in Europe as middle distillate cracks halved from November’s highs.

-

Global observed stocks surged by 75.3 mb in November 2025, or 2.5 mb/d, with crude oil accounting for 96% of the increase, mostly onshore. OECD industry stocks were up by 7.3 mb to 2 838 mb, largely in line with the five-year average level. Total observed oil inventories were 433 mb higher than at the start of 2025, increasing by 1.3 mb/d on average. Preliminary data showed global inventories rose further in December, led by builds in products.

-

Benchmark crude oil prices jumped by about $6/bbl at the start of the new year in the wake of geopolitical developments in Iran and Venezuela, but eased by mid-month as tensions moderated. North Sea Dated fell by $0.99/bbl m-o-m in December to an average $62.64/bbl, as markets remained well supplied. This was the benchmark’s sixth consecutive monthly decline, with prices hitting a low of $60.07/bbl mid-month – the weakest since early 2021.