US Existing Home Sales: December 2025

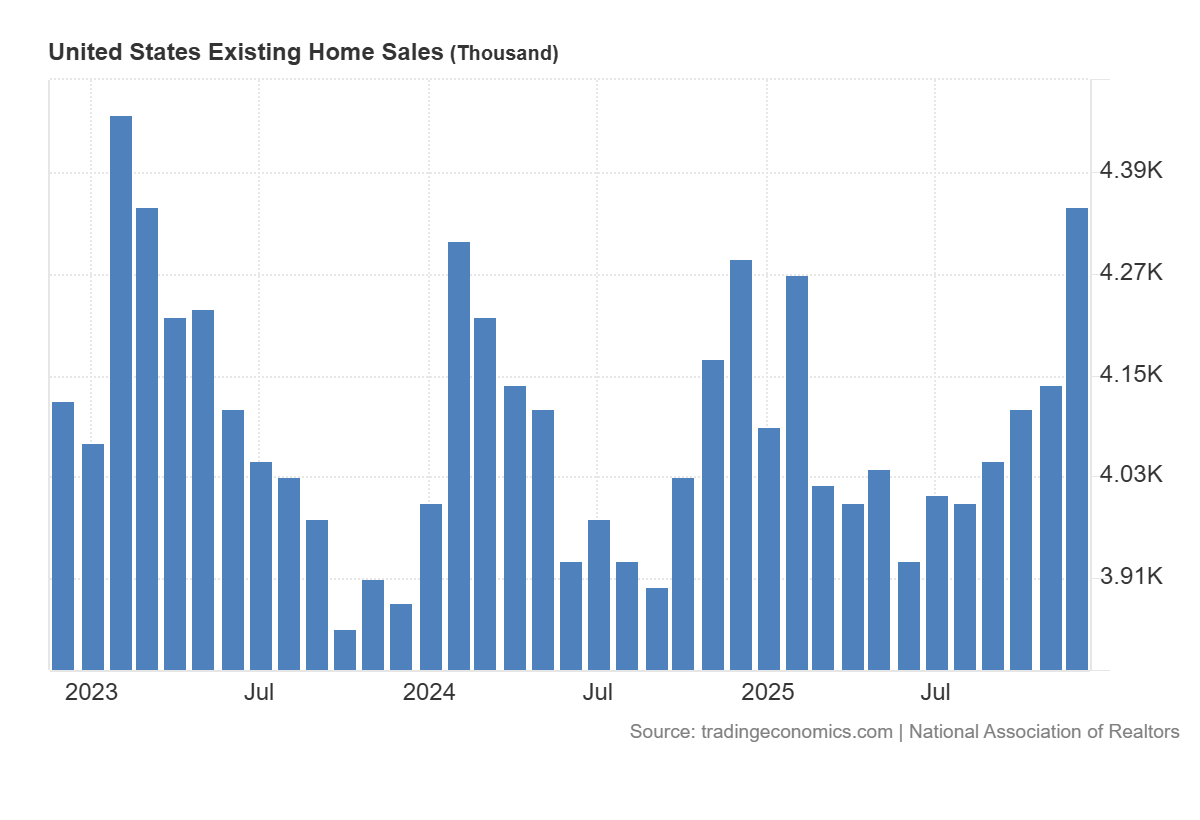

U.S. existing-home sales rose +5.1% MoM in December to a 4.35 million (vs 4.21 million) SAAR and increased +1.4% YoY, marking the strongest seasonally adjusted pace in nearly three years amid improving late-2025 conditions.

-

Total housing inventory fell to 1.18 million units (-18.1% MoM, +3.5% YoY), pushing months’ supply down to 3.3 months (from 4.2 in November), signaling tighter near-term availability despite slightly higher stock than a year ago.

-

The median existing-home price rose +0.4% YoY to $405,400, extending 30 consecutive months of YoY price gains, though the report noted slower home price growth in Q4.

-

Single-family sales increased +5.1% MoM to 3.95M SAAR and were up +1.8% YoY, while the median single-family price rose +0.2% YoY to $409,500, indicating modest price appreciation alongside stronger volumes.

-

Condo and co-op sales rose +5.3% MoM to 400k SAAR but were down -2.4% YoY; the median condo price increased +1.5% YoY to $364,400, showing firmer annual pricing than the single-family segment despite weaker YoY sales.

-

Regional performance was broadly positive MoM, with the Northeast +2.0%, South +6.9%, and West +6.6%, offset by a -2.0% MoM decline in the Midwest; YoY sales rose in the South (+3.6%), were flat in the Midwest and West, and fell in the Northeast (-1.9%).

-

Price trends varied by region, with median prices up +3.7% YoY in the Northeast ($496,700) and +3.1% YoY in the Midwest ($306,000), while the South fell -0.3% YoY ($360,200) and the West fell -1.4% YoY ($605,600).

-

The average 30-year fixed mortgage rate eased to 6.19% in December (from 6.24% in November and 6.72% a year earlier), consistent with the report’s view that lower mortgage rates helped support Q4 sales improvement.