NY Fed Household Debt and Credit Report: Q3 2025

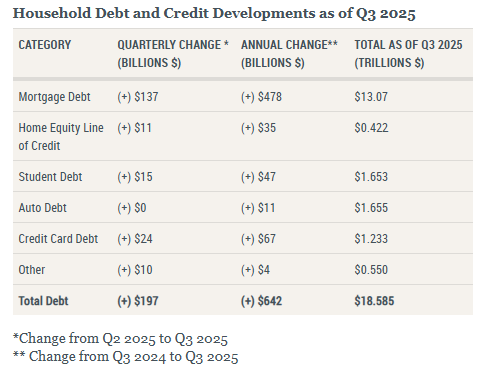

Total household debt rose $197B (+1.0% QoQ, +$642B YoY) to $18.59T in Q3 2025, marking continued moderate growth as delinquency rates stabilized and mortgage performance remained resilient.

-

Mortgage balances increased $137B QoQ (+$478B YoY) to $13.07T, supported by strong housing fundamentals and low delinquency amid tight underwriting and high home equity.

-

Credit card balances rose $24B QoQ (+$67B YoY) to $1.23T, while aggregate credit limits expanded $94B (+1.8% QoQ), indicating steady consumer credit growth.

-

Auto loan balances were unchanged at $1.66T, while new auto originations dipped slightly to $184B (from $188B in Q2).

-

HELOC balances increased $11B QoQ (+$35B YoY) to $422B, extending a growth trend that began in 2022.

-

Student loan balances rose $15B QoQ (+$47B YoY) to $1.65T; the delinquency rate remained elevated at 9.4% as previously unreported missed payments reappeared on credit reports.

-

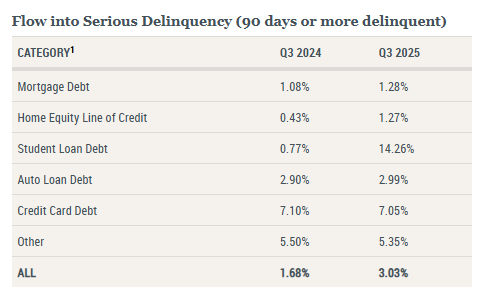

Overall delinquency stood at 4.5%, with early delinquencies mixed, credit card and student loans rising while other categories declined.

-

Serious delinquency (90+ days) increased across most debt types, reaching 3.03% overall (vs. 1.68% YoY), led by student loans (14.26%, up sharply YoY), while mortgage serious delinquency edged down slightly to 1.28%.

-

Mortgage originations rose to $512B, the highest since early 2024, pointing to renewed activity in the housing market despite elevated borrowing costs.