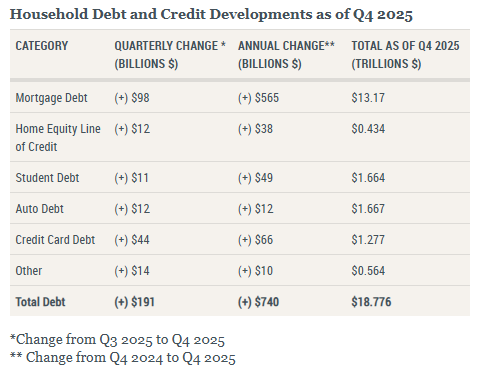

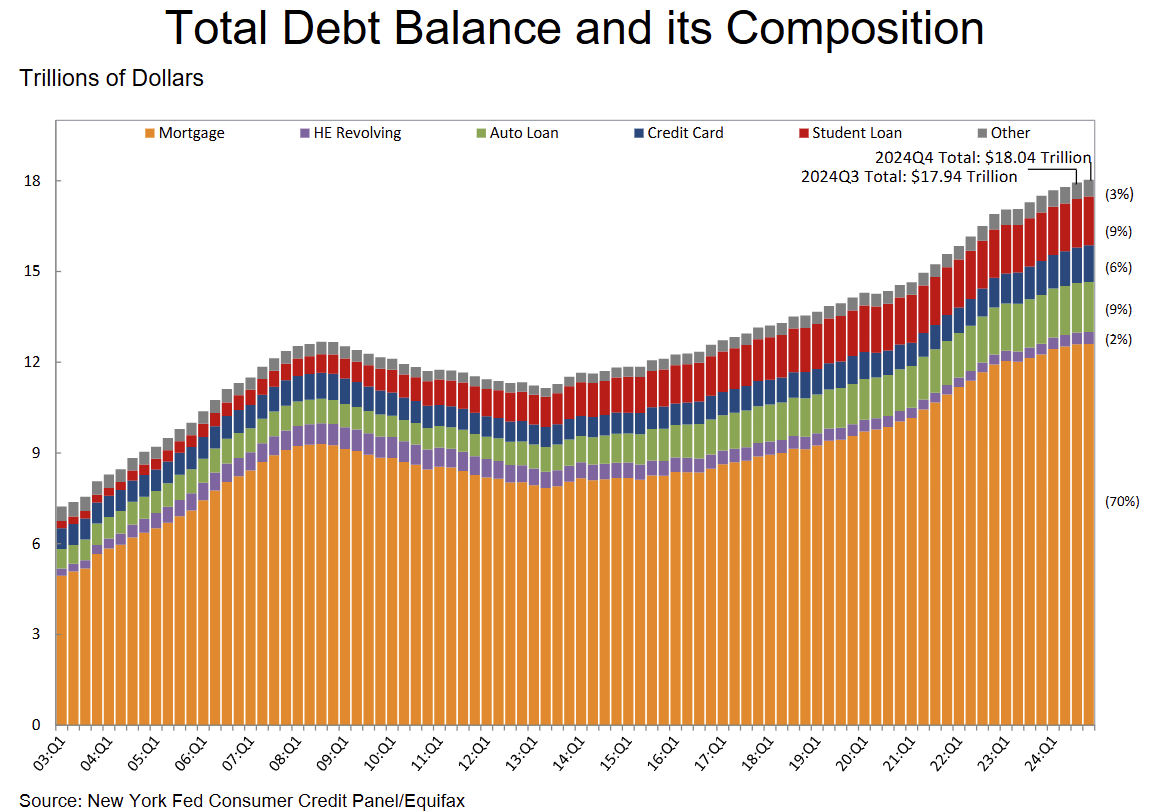

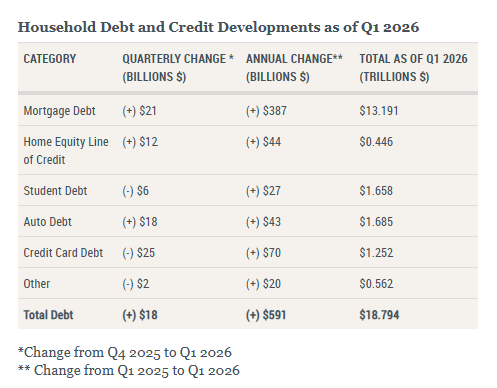

Total household debt rose +$191B QoQ (+1.0% QoQ, +$740B YoY) to $18.78T in Q4 2025, reflecting continued balance growth alongside rising delinquencies.

- Total household debt increased to $18.78T (+$191B QoQ; +$740B YoY), indicating steady expansion in aggregate borrowing levels compared with both the prior quarter and year.

- Mortgage balances rose +$98B QoQ (+$565B YoY) to $13.17T, remaining the primary driver of overall debt growth and the largest component of household liabilities.

- Credit card balances increased +$44B QoQ (+$66B YoY) to $1.28T, while aggregate credit limits expanded +$95B, pointing to continued availability and usage of revolving credit.

- Auto loan balances grew +$12B QoQ (+$12B YoY) to $1.67T, while new originations declined slightly to $181B (Q3: $184B), suggesting softer lending flow despite higher outstanding balances.

- HELOC balances increased +$11.6B QoQ (+$38B YoY) to $434B, with credit limits rising +$25B (+2.5%), extending the ongoing expansion in home equity borrowing.

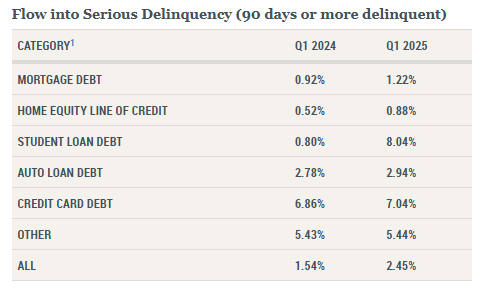

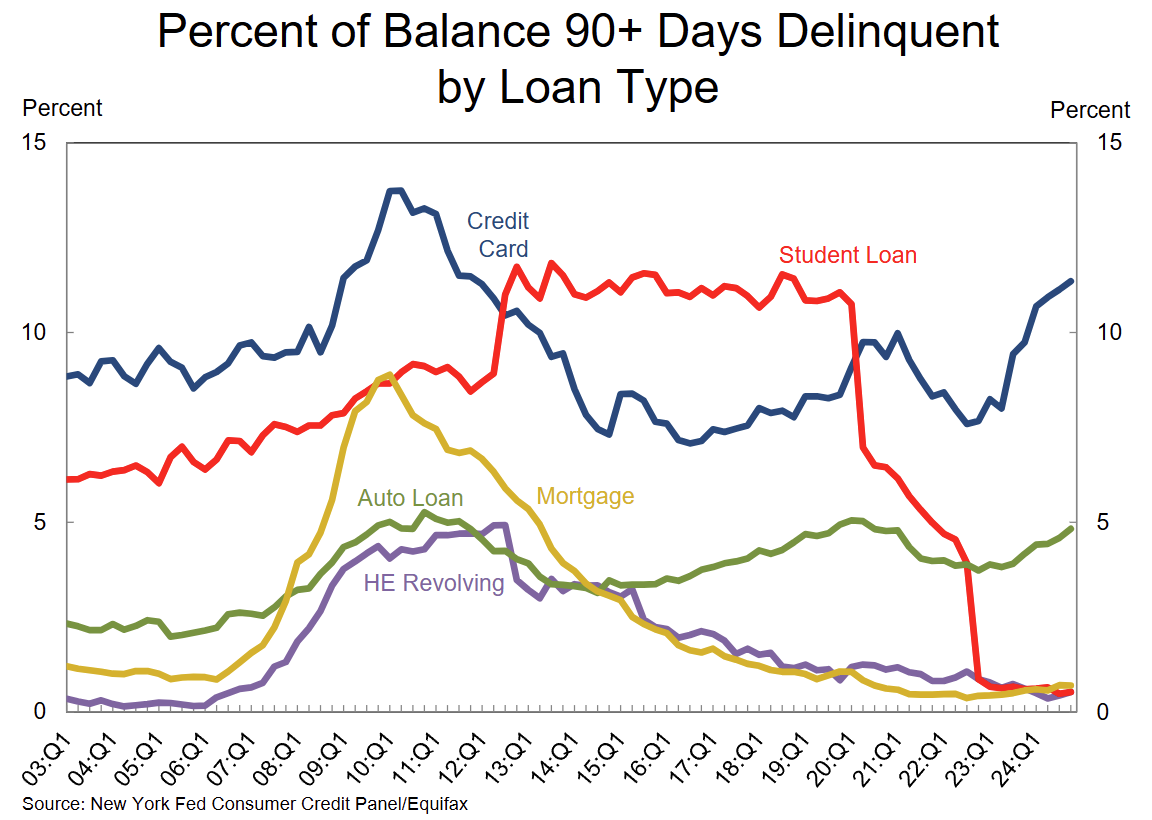

- Student loan balances rose +$11B QoQ (+$49B YoY) to $1.66T, with the 90+ day delinquency rate holding at 9.6%, indicating elevated repayment stress as reporting resumed.

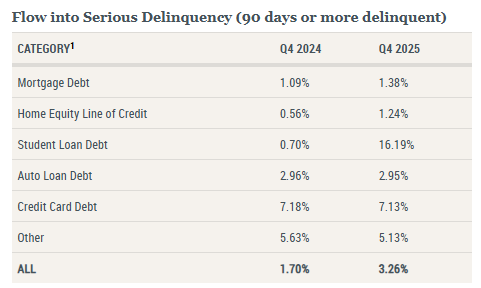

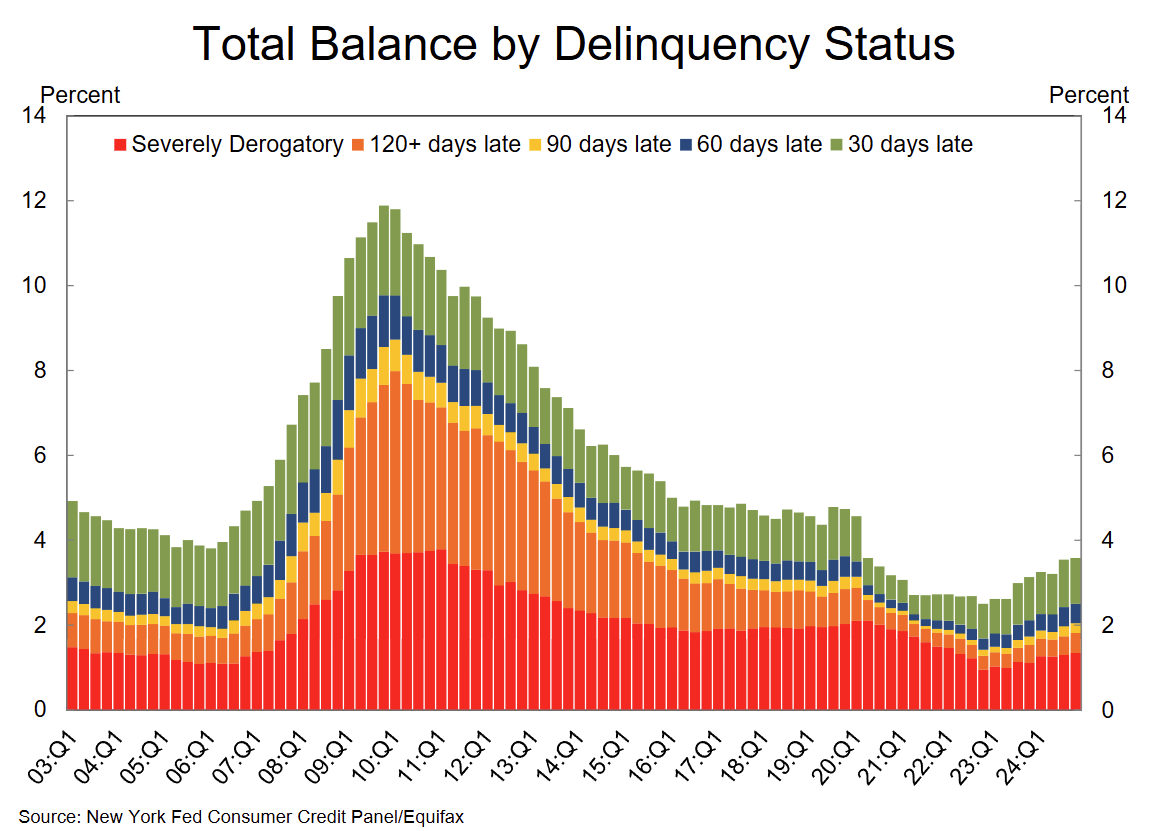

- Aggregate delinquency increased to 4.8% of outstanding debt, with early delinquency transitions mixed and serious delinquency rising across mortgages, credit cards, and student loans, pointing to a gradual deterioration in credit quality.