Federal Reserve Monetary Policy Decision: October 2025

The October FOMC meeting offered little in the way of new information, yet managed to send a clear message: the Fed isn’t ready to promise more cuts. A 25 bp cut was widely expected, but Powell’s tone reminded markets that further easing is not necessarily a guarantee, especially when the Fed is dealing with a lack of data. With the labor market softening and inflation still sticky, the Committee is increasingly divided on how close policy is to neutral and how far it should go. The result was a “hawkish cut,” one that signaled flexibility rather than commitment, and left December’s decision very much in play.

Fed Statement

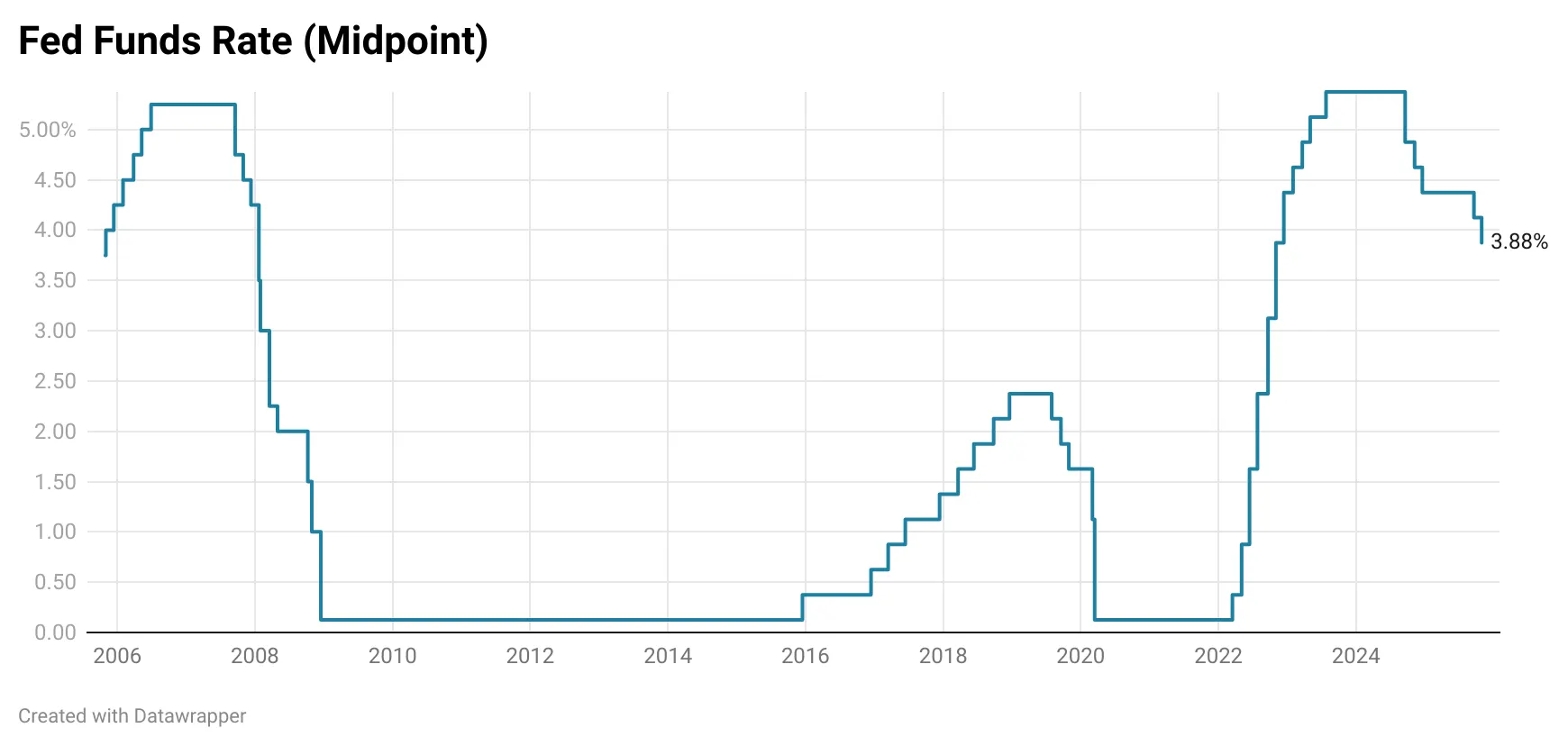

The Federal Reserve decided to cut the federal funds rate by 25 bps at the conclusion of the October FOMC meeting, bringing the target range down to 3.75% to 4.00%. The last time the federal funds rate was set this low was almost three years ago, after the December 2022 meeting. While this is just the second cut so far this year, it is the fifth cut since the Fed started its cutting cycle in September 2024 that has led to a cumulative reduction in the federal funds rate of 150 bps. The decision was not unanimous and included two dissenters: the new FOMC member, Stephen Miran, preferred a 50 bps cut, and Kansas City Federal Reserve President Jeffrey Schmid voted for no change in the rate.

In addition to the decision to cut, the FOMC decided to conclude its quantitative tightening (QT) measures on December 1st. Beginning that date, the Fed will fully reinvest all principal payments from its Treasury and agency securities holdings rather than allowing them to roll off its balance sheet. Until then, the runoff caps of $5 billion for Treasuries and $35 billion for agency MBS will remain in place for October and November. The shift marks the end of the balance sheet reduction program that was first announced after the May 2022 FOMC meeting.

Here are the notable changes in the press release from September:

- The first paragraph saw substantial changes, but the underlying message has not really changed much. Most of the edits were to acknowledge that the Fed is dealing with a lack of data (”recent indicators” became “available indicators”, reference to “August” unemployment data since September has been delayed). In general, the Fed hasn’t changed its assessment on the economy and suggests that the available indicators are mostly consistent with the last meeting’s assessment.

- The next paragraph only featured one change. This change does feel slightly relevant in that the Fed intends to keep current its view that there are downside risks to employment in saying that those risks remain visible “in recent months.”

- The changes in the rest of the statement just include edits to reflect the most recent decisions: a 25 bps cut to a target range of 3.75% to 4.00% and the end of QT measures.

With really no new data to look at and no change in how the Fed is looking at the economy, one can assume two things about today’s decision. First, the decision for a 25 bps cut was likely already largely determined during the September meeting. Labor market data available at that time had already shown enough weakening to justify at least one cut, and possibly two, depending on how conditions evolved. Second, today’s move can be viewed as a “risk management” cut. The balance of risks had tilted toward the labor market, with downside risks to employment outweighing the potential for renewed inflation pressures. In that context, holding rates steady risked tightening policy too much, whereas delivering a small, precautionary cut carried less downside if the economy proved more resilient than expected.

Press Conference

Opening Remarks

The opening remarks of the post-meeting press conference reflected the tone of the September meeting, likely a result of the dearth of data that has plagued the Fed during the government shutdown:

- Powell noted that “economic activity has been expanding at a moderate pace” according to “available indicators,” even going so far as to admit that economic activity was “on a somewhat firmer trajectory than expected.” This suggests that tariffs were having a smaller impact on growth than the Fed initially thought. Powell also notes that the shutdown will weigh on economic growth, but also that these effects are temporary and will reverse when the government reopens.

- On the labor market, Powell noted that the unemployment rate remains low (as of August data), and job gains have slowed, an assessment similar to his September remarks. Once again, he points out that both labor supply and labor demand have eased, leading to a “less dynamic and somewhat softer labor market.” Again, this language is not new and is similar to Powell’s tone since the weak July jobs report.

- On inflation, Powell notes that current inflation rates have fallen but remain “somewhat elevated” as goods inflation has “picked up” and services disinflation has continued. He points out that tariffs have increased prices, but it remains “a reasonable base case” that this rise will be “relatively short-lived.”

With the labor market softening and inflation still elevated, Powell highlights that the Fed continues to try and balance the risks to its dual mandate, calling it a “challenging situation.” But in recent months, since the labor market downside risks have become heavier, a reduction in the policy rate “toward a more neutral policy stance” has been warranted. But Powell was very clear to indicate that risks were coming more into balance, and he struck a much more hawkish tone, talking about the December meeting. The following statement was one that stuck out in his remarks and led to a significant response in markets:

In the Committee’s discussions at this meeting, there were strongly differing views about how to proceed in December. A further reduction in the policy rate at the December meeting is not a forgone conclusion—far from it. Policy is not on a preset course.

Powell ended his opening remarks explaining the decision to end the Fed’s quantitative tightening measures. Specifically, the condition to end balance sheet runoff where “reserves are somewhat above the level [the Fed] judge[s] consistent with ample reserve conditions” has been met.

Q&A

Here are some questions of note in the Q&A portion of the conference:

- Are you uncomfortable with how market pricing has assumed a rate cut is a foregone conclusion in the December meeting? - The first question was a heavy one, and it allowed Powell to continue to echo the hawkishness that came from the key quote that I highlighted from his opening remarks. He reasserted that a cut in December is “not a foregone conclusion,” given that there was a broad array of views being represented by all of the members of the FOMC in deliberations. Specifically, he said that “they hadn’t made a decision on December,” countering the market’s pricing in of a cut in the next meeting. A follow-up question from another reporter asks again about the December decision, to which he responds, “December is not a foregone conclusion. In fact, far from it.”

- When is “enough insurance,” and are you setting up a sequence of cuts like last year (risk management cuts)? - Powell reiterates that the balance of risks has shifted from inflation to the labor market since the post-July data revisions. Policy has been modestly to moderately restrictive and is moving toward neutral when risks are balanced. Today’s cut fits that risk-management logic, but crucially, the path ahead (”going forward”) is a separate decision.

- If the labor market stabilizes or strengthens, how would that change the rate path, especially with tariff risks? What if a shutdown limits data into December? - Powell notes that stronger labor data would matter for the path, but of course, without data, it is hard to get a full picture. But even without full federal data, the Fed will see initial claims, openings, surveys, and the Beige Book. With these data points, Powell says that “if there were a significant or material change in the economy one way or another, I think we would pick that up.” At the end of the answer, however, Powell highlights the “high level of uncertainty” the Fed is facing.

- How are officials reading the latest CPI, with core still near 3 percent, and where are the bigger policy risks? - Powell mostly repeats his notes from the opening remarks. Goods inflation is up mostly due to tariffs versus a long-run trend of mild goods deflation; housing services inflation is declining as expected; other services have moved sideways, with a sizable non-market component. He does point out that ex-tariffs, underlying inflation, “ is actually not so far from our 2% goal.”

- Is the government shutdown making it more difficult to move in December? Will it make you more cautious? - Powell: “…could it affect the December meeting, I am not saying it is going to, but yeah, you could imagine -- what do you do if you are driving in the fog? You slow down. So, that could or could not. I don't know how that will play into things.” We get more of that hawkish tone, suggesting that a December cut is not guaranteed.

- If December is not a foregone conclusion, what else besides missing data could hold you back? - Powell points out that after 150 bps of cuts, policy is near many of the FOMC members’ estimates of a neutral federal funds rate (between 3% to 4%). Some members may prefer to pause to assess labor market risks and whether growth strength is persistent, reflecting different estimates of neutral and risk tolerance.

- Are equities overvalued, and how do you balance labor support with asset prices and AI-linked job cuts? - An interesting question about the equity market leads to a typical non-answer from Powell. The Fed does not set or judge individual asset prices. It focuses on system stability, which currently looks mixed but not overly troubling. “We don't set asset prices. Markets do that.”