Bank of England Monetary Policy Decision: September 2025

The Bank of England held rates steady in September, extending its pattern of alternating between cuts and pauses while signaling a more unified stance than in recent months. The decision reflects a balance between acknowledging the progress made in bringing inflation lower and maintaining caution as price pressures remain elevated. With growth and employment proving more resilient than expected earlier in the year, the Committee’s attention is increasingly centered on inflation risks, which continue to play a decisive role in shaping policy.

Decision

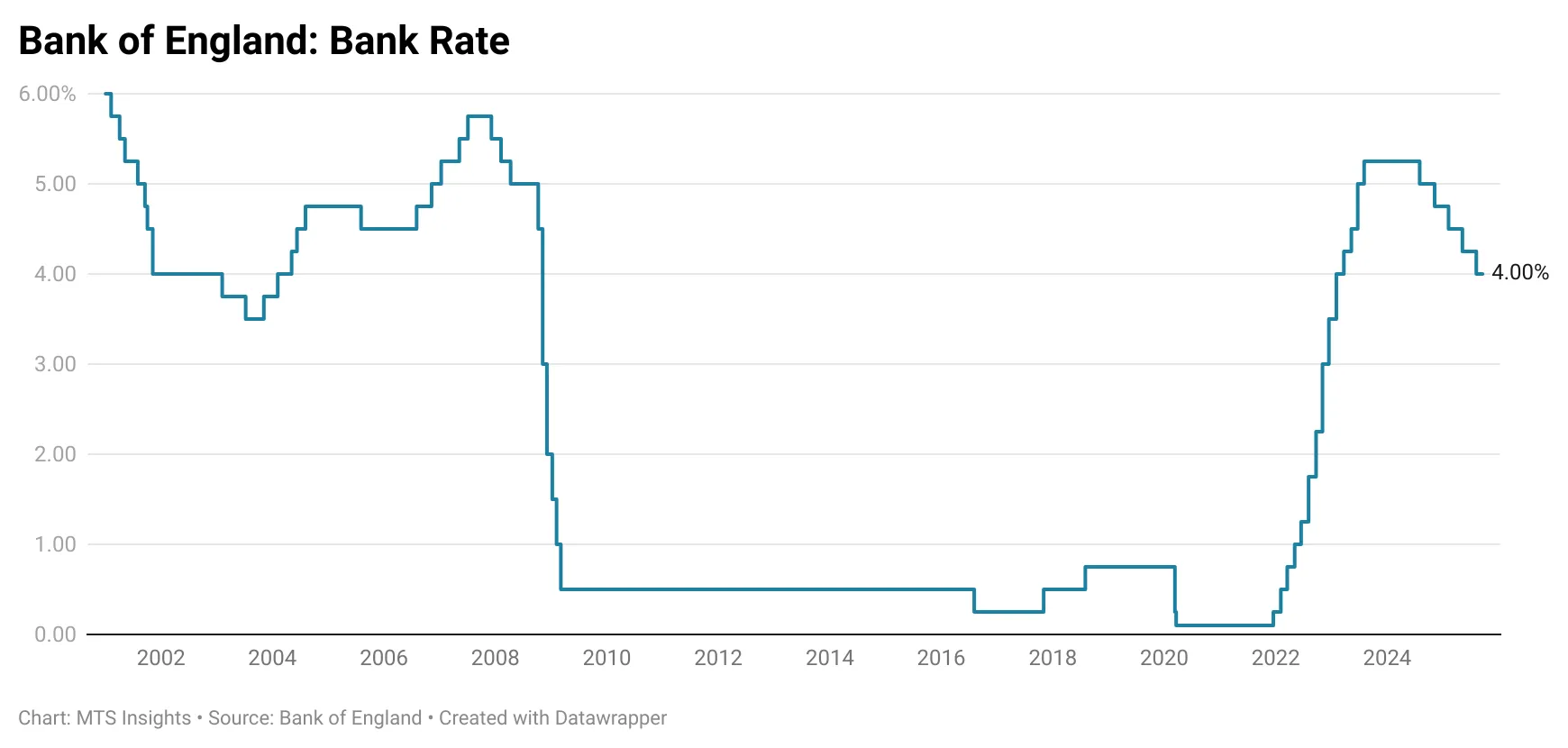

The Bank of England (BOE) decided to maintain its Bank Rate at 4.00% at the conclusion of the September meeting, continuing the pattern of alternating between cuts and pauses for the 10th straight meeting. The decision was less divided than the early August cut (which barely made it over the line), with 7 members voting for the pause and 2 members voting for a quarter-point cut. This vote was also more decisive than the June pause, which was decided with a 6-3 vote. Overall, the Bank of England’s pause today has the strongest majority since March.

In addition to the pause, the BoE’s Monetary Policy Committee (MPC) voted to reduce the stock of UK government bond purchases held for monetary policy purposes by £70 billion over the next twelve months, bringing the total to £488 billion, down from the total of £558 billion set in the September 2024 meeting. Seven members backed the £70 billion path, while Catherine Mann preferred a slightly smaller £62 billion reduction and Huw Pill a larger £100 billion reduction, and the Committee reaffirmed that any change to the pace outside the annual review would face a high bar. This decision represents the Bank of England’s continuation of quantitative tightening with most members aligned on the chosen pace, and only modest debate over whether the process should be somewhat slower or faster, reinforcing the Bank’s preference for a steady and predictable approach.

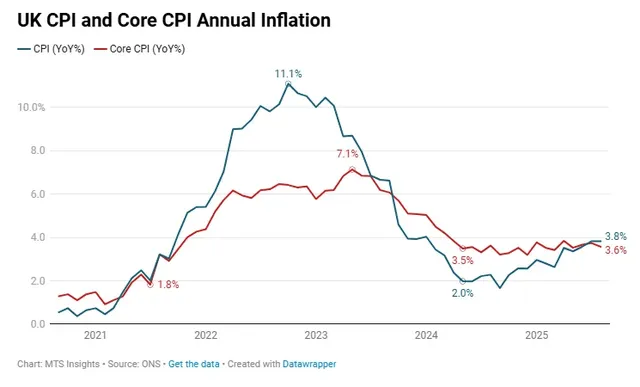

The focus of the statement given today is inflation as it appears to be the main thinking keeping the MPC from cutting rates further (coincidentally, this decision was immediately preceded by a UK CPI release). The MPC starts out by pointing out the “substantial disinflation” that has occurred over the past two and a half years and explains that this “progress has allowed for reductions in [the] Bank Rate over the past year.” While inflation has generally fallen, there is still work to be done with both CPI and core CPI annual inflation above 3.5%. The MPC continues to describe the stickiness in inflation this year as a “temporary increase,” but at the same time, it highlights that “upside risks” to inflationary pressures are a “prominent” part of the outlook.

The general stance on inflation is a bit mixed. The MPC wants to point to a trend of disinflation that “has generally continued,” but it also must voice a concern of upside risks in its economic outlook. This echoes the sentiment in the last few announcements, but interestingly, the assessment of upside inflation risks looks to be getting stronger. Specifically, we can see a difference in how it is referenced in the August statement and today’s statement:

- August: “The MPC judges that the upside risks around medium-term inflationary pressures have moved slightly higher since May.”

- September: “Upside risks around medium-term inflationary pressures remain prominent in the Committee’s assessment of the outlook.”

Using the word “prominent” does not feel like an accident. I believe that several members of the MPC have become very vigilant of inflationary pressures and are unlikely to vote for another cut unless inflation starts to come down again.

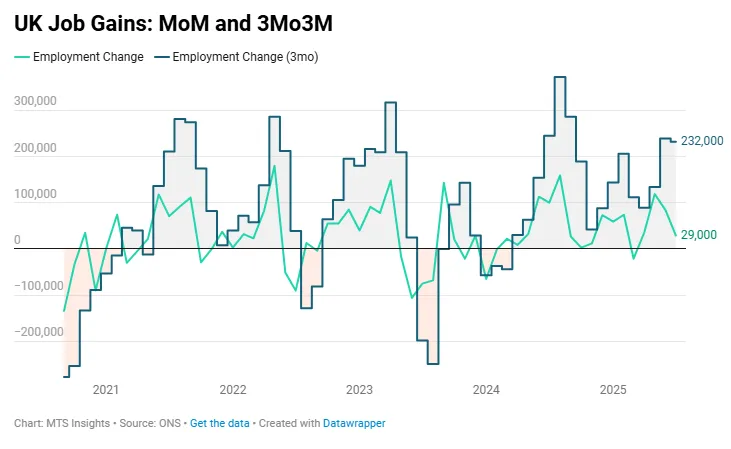

Why can the BoE move towards a more intense focus on inflation? A large part of it is because trends in growth and the labor market have been more resilient than the they were expected to be. In the first half of the year, US tariff policy and global trade uncertainty cast a shadow over the UK economic outlook, but those factors have not been as detrimental as previously thought. Employment gains have actually been pretty solid recently, increasing 232k in the three months to July and the unemployment rate at 4.7% is a tick below the Bank of England’s Q3 2025 forecast. GDP growth in Q2 2025 surprised to the upside, increasing 0.3% QoQ when growth was expected at 0.1% QoQ. This stronger data suggests that growth and employment are now less of a concern for the MPC than they appeared in Q1 and Q2, which is reflected in the September monetary policy statement, where the Committee devoted just three sentences to the topic.