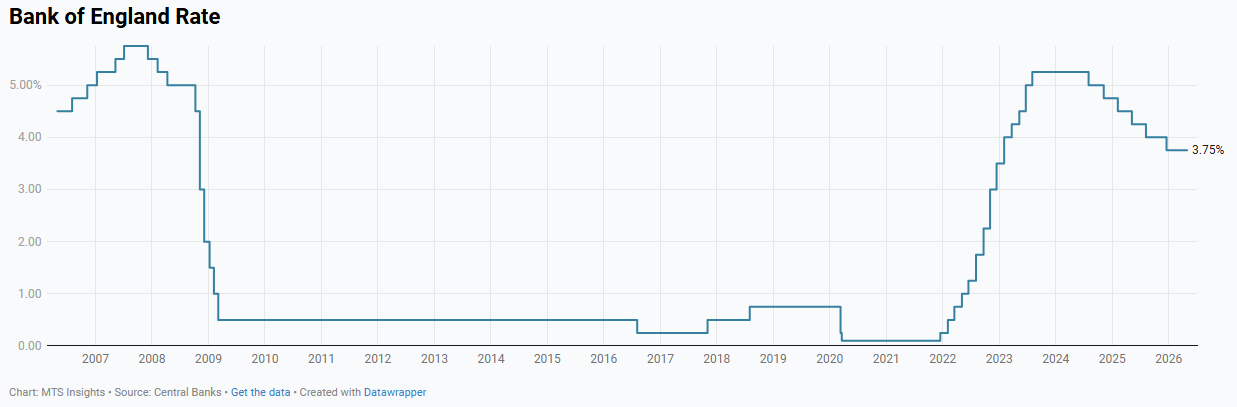

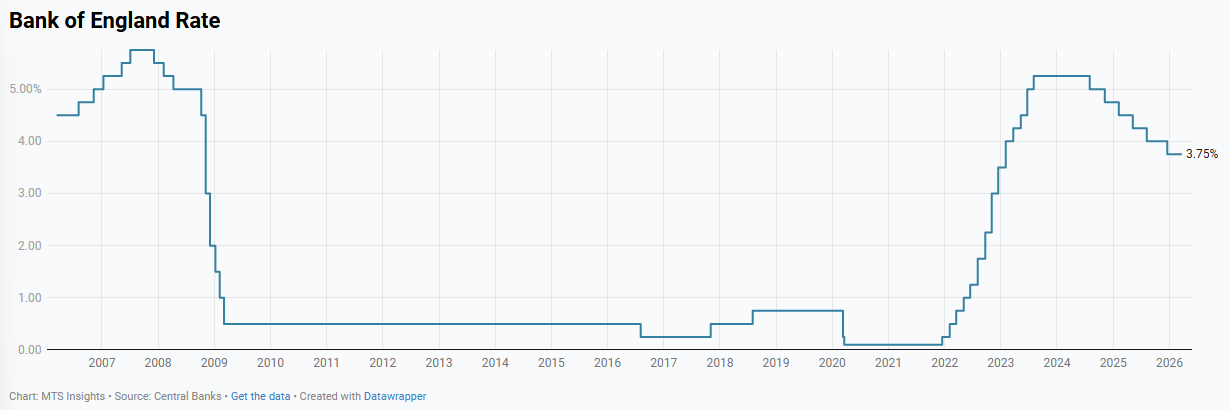

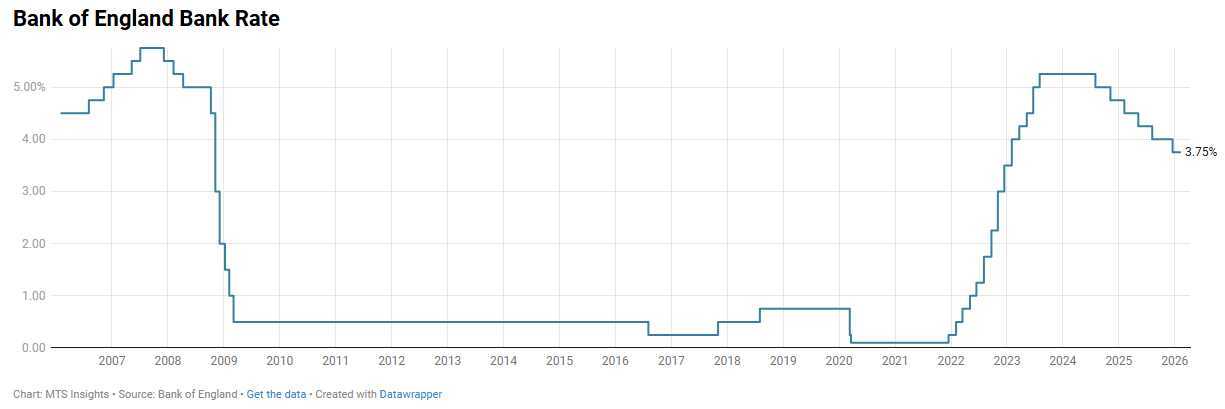

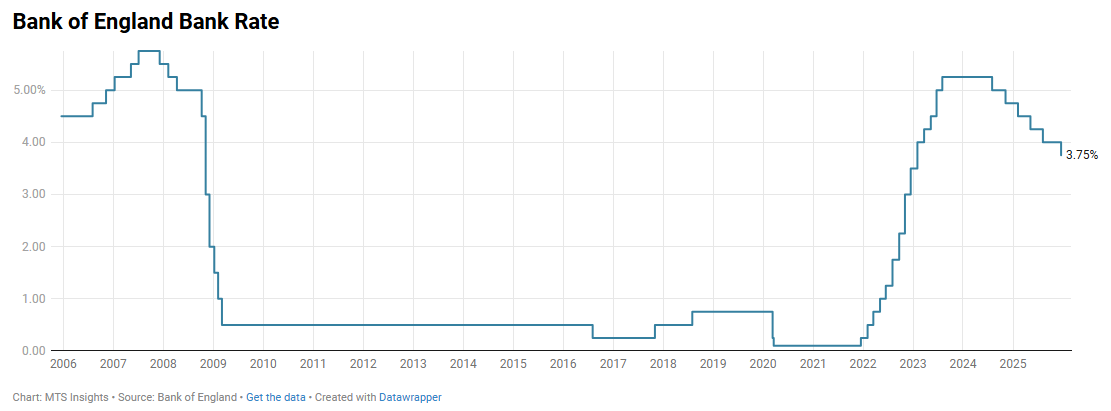

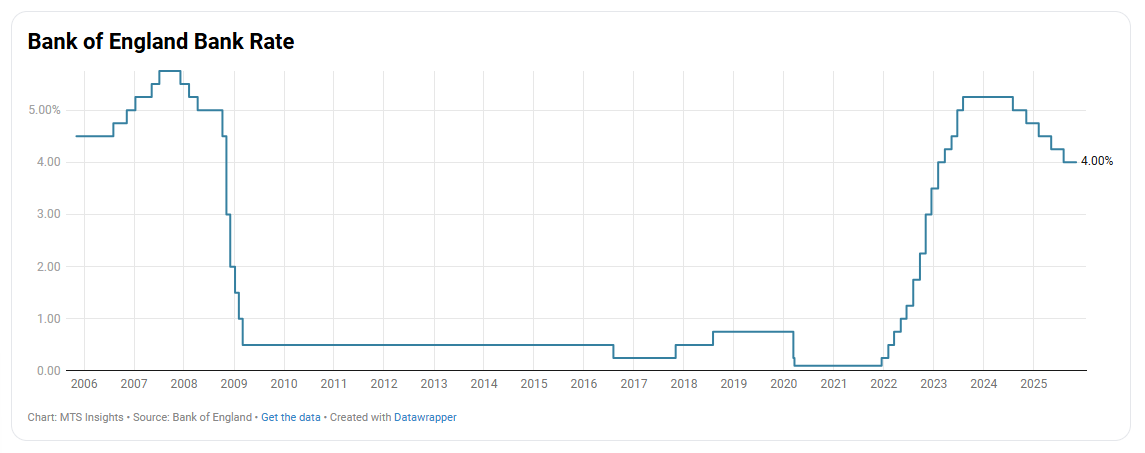

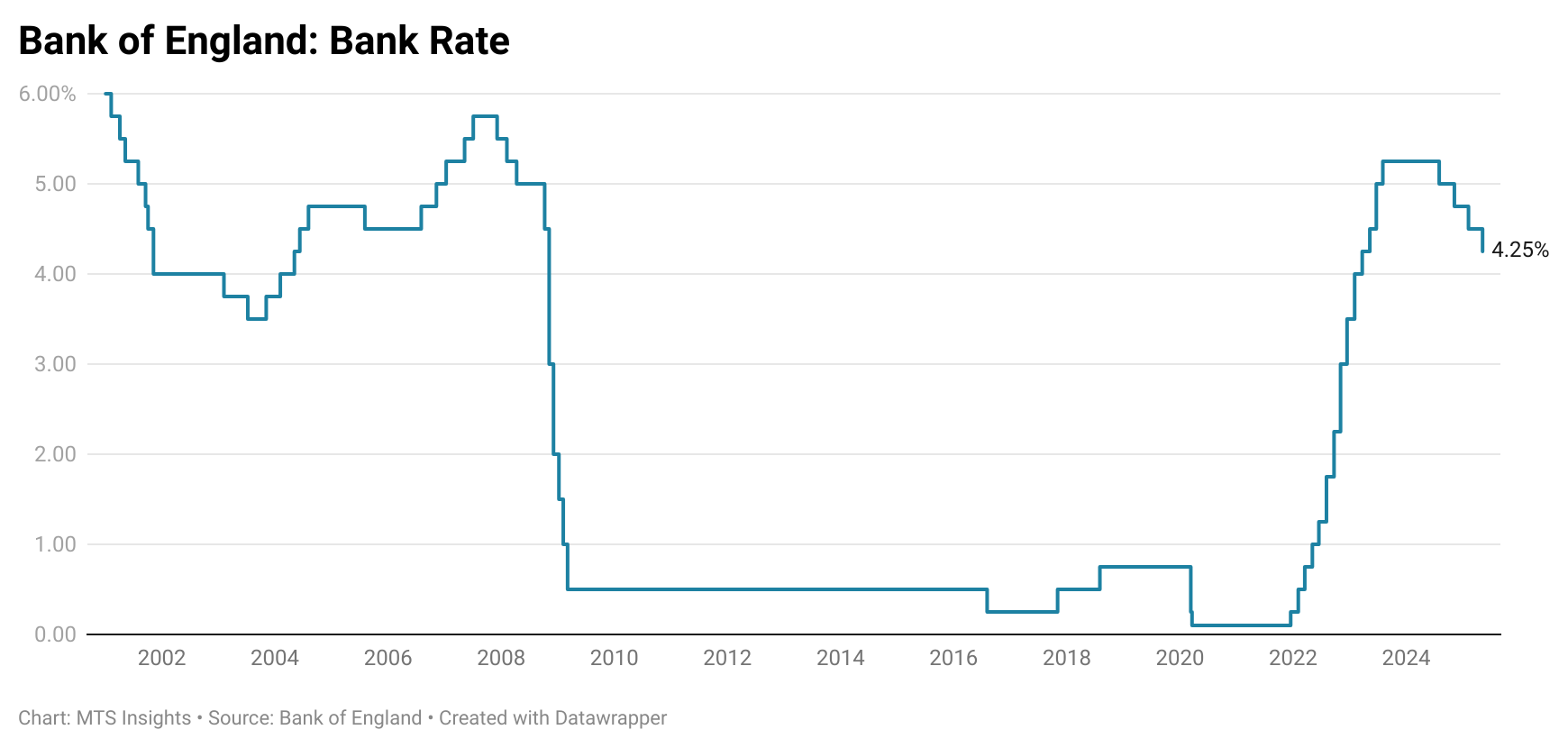

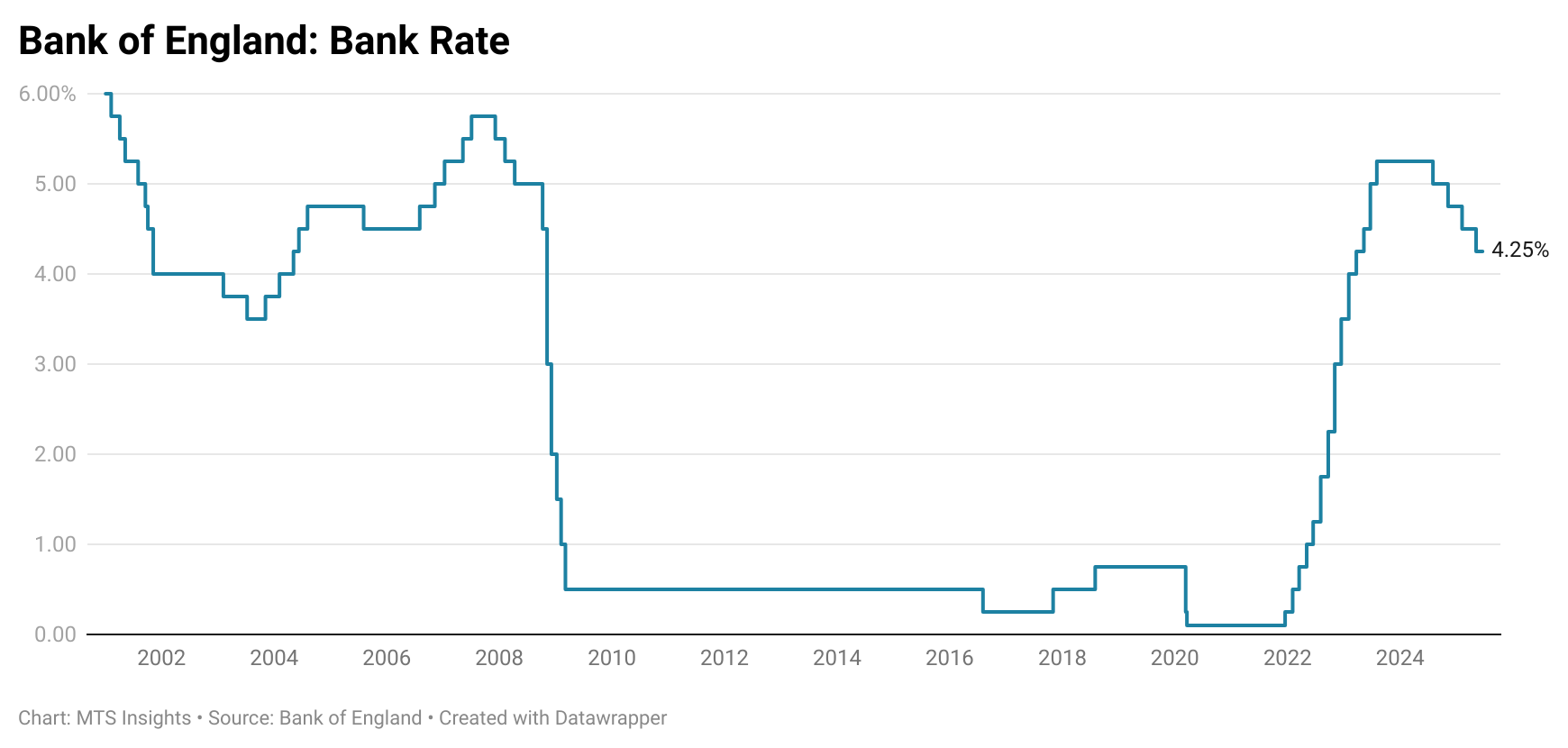

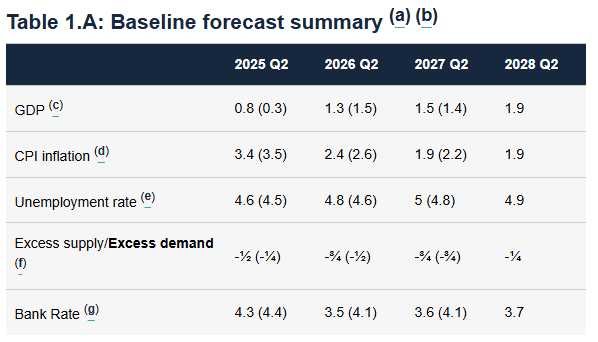

The Bank of England kept its main policy rate, the Bank Rate, unchanged at 4.25% following the June 2025 meeting. The decision to pause maintains the cadence of interest rate cuts that has led to a gradual easing in monetary policy since August 2024. While there was a pause today, recent growth and employment data have tilted the Monetary Policy Committee members to be a bit more dovish as it appears that the economy could be weakening more than they expect.

Decision

The Bank of England (BoE) opted to leave the Bank Rate unchanged at 4.25%. Six members voted for a pause and outnumbered the three members who voted for a 25 bps cut. Of the three members voting for a cut, two of those members had voted for a 50 bps cut in the May meeting (Dhingra and Taylor), and one voted for the 25 bps cut that occurred (Ramsden). The other four members who voted for a cut in the May meeting (Bailey, Breeden, Greene, Lombardelli) joined the two who voted for a pause (Mann, Pill) to create the majority that decided on no change in June.

The decision maintains the pattern of alternating between a pause and a cut that was set after the first quarter point cut in August 2024. Since then, we have had 25 bps cuts in November 2024, February 2025, and May 2025 and pauses in September 2024, December 2024, March 2025, and now June 2025. In total, the Bank of England has cut rates by 100 bps over that timeframe.

Minutes

Throughout its rate-cutting cycle, the Bank of England has been navigating a balance between a gradual weakening in UK economic growth and employment and expectations of a resurgence in inflation this year. So far, the data points have drifted around the forecasts of the Monetary Policy Committee (MPC) members such that a gradual easing of the Bank Rate was possible. In the June meeting, the MPC members paused to reassess the developments in the global economy and recent UK data points to decide what the decision in early August will be.

Inflation

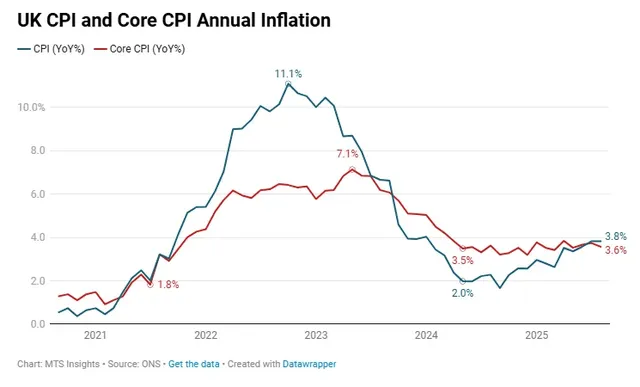

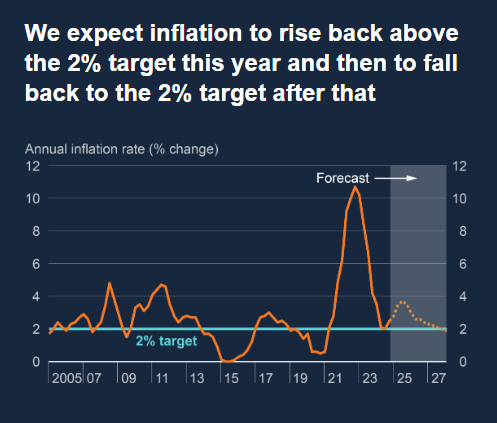

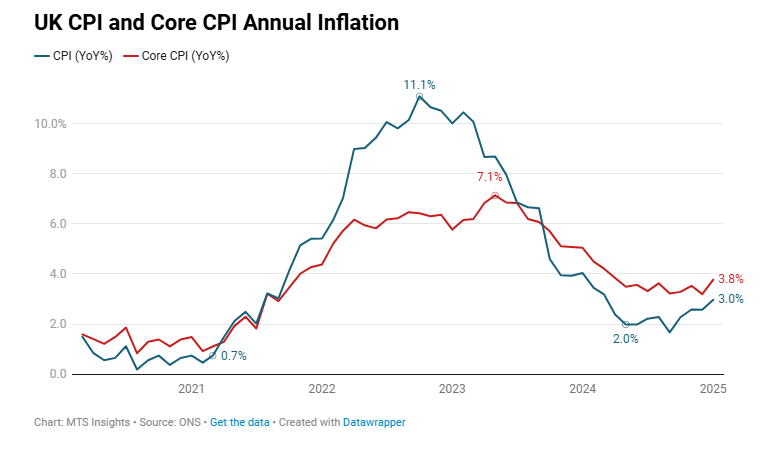

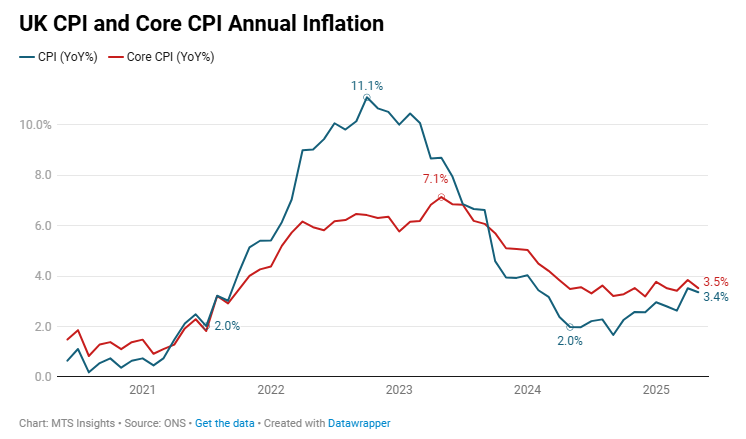

Inflation data for May was released the day before the Bank of England’s decision on June 18th, so the MPC had plenty to discuss ahead of the decision today. The UK CPI inflation rate ended up at 3.4% YoY in May with core CPI inflation coming in at 3.5% YoY (below analyst expectations). The details of the report showed goods CPI inflation on the rise, up to the highest since November 2023 at 2.0% YoY. About 0.2 ppts of the acceleration in the headline rate came from three goods categories: food & non-alcoholic beverages (+0.11 ppts), furniture & household goods (+0.07 ppts), and miscellaneous goods & services (+0.03 ppts). The energy aggregate, which the BoE expects will become an upward pressure on inflation, fell -0.8% MoM and -1.7% YoY.

In a nod towards the new data, the Bank of England points out that CPI inflation of 3.4% in May is “in line with expectations in the May Monetary Policy Report.” This recent rise is expected to be the peak for inflation in 2025 before it flattens out and starts to ease before “falling back towards the target next year.” The Bank of England’s tone on inflation in the June statement and minutes suggests that prices are developing largely as expected, but members will be monitoring the persistence of these current inflation rates. Notably, it also shares that the MPC members see “two-sided risks to inflation.”

Growth and Employment

The downside risk to inflation comes from the Bank of England’s view that UK growth has “remained weak” and the labor market has “continued to loosen” which suggests that economic slack has increased since the cutting cycle began.

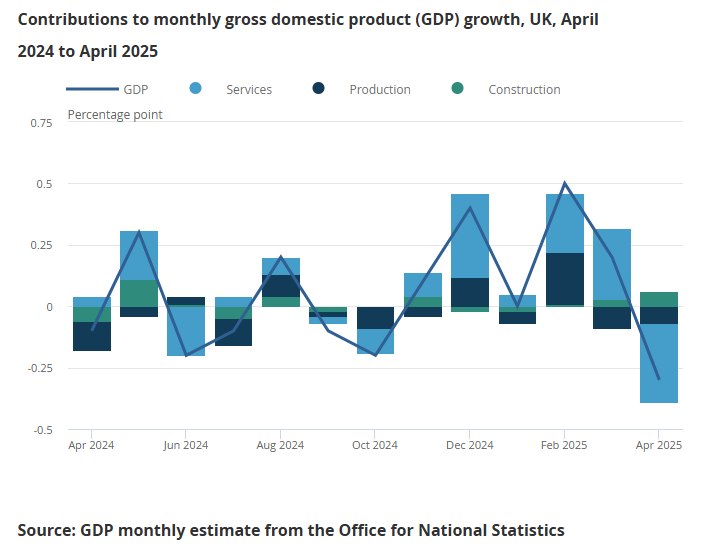

- GDP data has been volatile over the last few months, with strong monthly reports in February and March to cap off a strong Q1, but the most recent April data point revealed a drop of -0.3% MoM, led by weak services. The BoE also points out that the strong readings in February and March “could have been affected by a front-loading of activity ahead of the imposition of new tariffs by the United States and related trade policy developments.” On an annual basis, GDP growth slowed to 0.9% YoY, which is slightly ahead of the May forecast for Q2 2025. Economic activity is expected to continue to soften in May and June, especially with US trade policy continuing to create growth headwinds in the broader global economy.

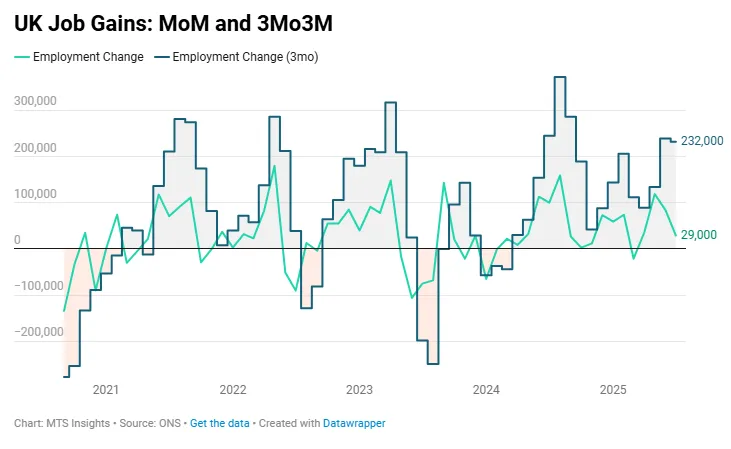

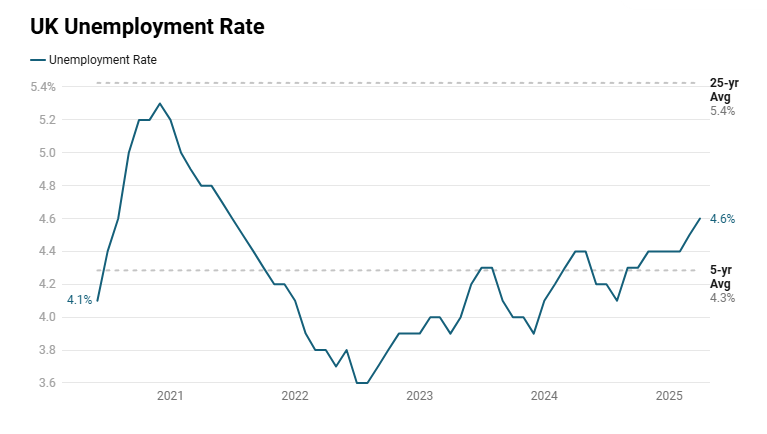

- The labor market report for April was also weak as it showed the unemployment rate ticked up 0.2 ppts to 4.6%, the highest since July 2021. This rise has been a little bit ahead of schedule as the Bank of England forecasted in the May meeting that it would reach that level by the end of Q2 2024, and in fact, the flash estimate of May payrolls, a drop of -274k in employment, suggests the unemployment rate might overshoot the projection. The easing in the labor market has led to a not insignificant decline in wage growth that has contributed to the disinflationary trend. The MPC members are confident that the still “elevated” wage growth will see “a significant slowing over the rest of the year.”

The growth and employment data were the main arguments wielded by the three MPC members who voted for a quarter-point rate cut today. Alongside the progress on inflation, the members assessed that “the cumulative evidence from a range of labour market data pointed to a material further loosening in labour market conditions.” Compared to other central banks, the Bank of England does appear to be facing more loosening in the labor market, so these arguments are not invalid and would probably become the basis of a cut in August.

In my opinion, unless data suddenly shifts before the next meeting, GDP growth easing at the BoE’s expected pace and a faster-than-expected increase in the unemployment rate will lead to a quarter point cut in August. The trend in hiring is especially concerning given the flash figures and the fact that UK firms have faced broadly weaker global economic conditions in Q2 2025 due to US tariffs. The Bank of England briefly mentions a potential spike in energy prices due to the Middle East, but the inflationary pressures from this will almost certainly be transitory and something that the BoE can look through.