Federal Reserve Monetary Policy Decision: June 2025

The Federal Reserve left its target range for the federal funds rate unchanged at 4.25% to 4.50% for the fourth meeting in a row. The non-event was largely expected, as futures markets more or less had priced in the move for the last two to three weeks. However, the Fed’s “wait and see” position in the face of cooling inflation data made this pause look hawkish, and the market responded in kind.

Fed Statement

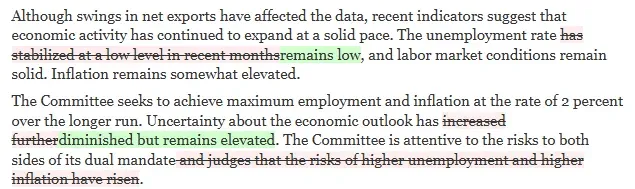

The Federal Reserve’s press release following the June meeting was left mostly the same as the last meeting in May. Only two minor changes were made:

- In the first paragraph, the description of the unemployment rate was simplified, and the underlying meaning remains the same. The Fed still assesses the labor market as strong, and the recent readings of the unemployment rate are low.

- In the second paragraph, the statement is adjusted to reflect an easing in the Fed’s uncertainty about the economic outlook. The FOMC is likely referring to some new clarity on trade policy, which has become less chaotic in the last two months with trade deals and pauses becoming the focus, and the worst of the China-US trade relationship likely behind us.

Overall, the official statement still communicates a “wait and see” position while policymakers attempt to look through uncertainty. This position is accompanied by the general assessment that the economy is in solid standing, even though Q1 GDP growth came in negative.

Summary of Economic Projections

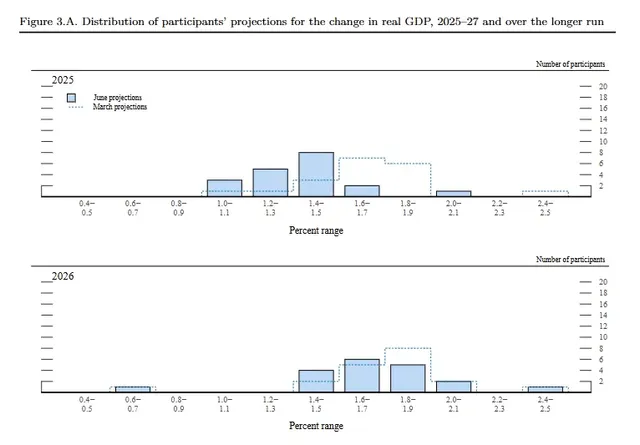

The conclusion of the June FOMC meeting comes with an update of the central bank’s economic projections that were last updated in March. Since then, we have had the “Liberation Day” tariff announcement and the aftermath, including the attempts to make trade deals with China and the UK. The Fed should have been able to produce projections with more confidence than three months ago. Here are the details of the projections:

- FOMC members have become more bearish on growth in the next two years, with the median projection of GDP growth in 2025 moving down -0.3 ppts to 1.4% and in 2026 moving down -0.2 ppts to 1.6%. The range of forecasted 2025 values fell from 1.4 ppts in March to 1.0 ppts in June. The general message is that the Fed has become more confident that growth will slow down and expects a stronger slowdown over the next two years than three months ago.

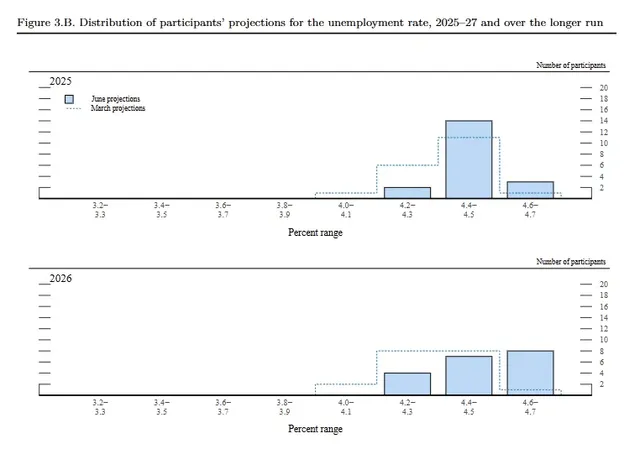

- The projections for the unemployment rate look similar to the GDP projections. Across all three years, the median projections in June increased compared to the March projections, with the forecast holding at 4.5% in both 2025 and 2026. The range of values for those two years also shrank, sending the same message that FOMC members are more confident that the labor market will loosen and expect more loosening in labor markets over the next two years than three months ago.

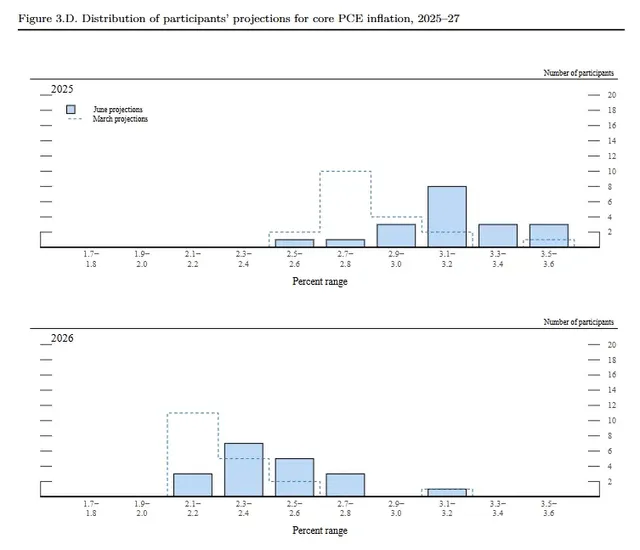

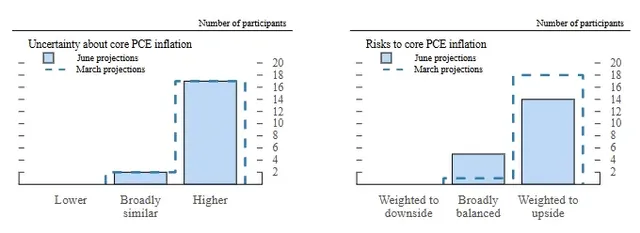

- The most surprising shift in the projections came in the PCE and core PCE forecast. FOMC members upgraded their forecasted values significantly for the next two years, with the median core PCE projection rising to 3.1% in 2025 and 2.8% in 2026, both upward revisions of 0.3 ppts. Unlike the GDP and unemployment rate ranges, the range of values for expected inflation remains about as wide in June as it was in March. But when looking at the spread of values in the center (excluding the three largest and three smallest), the range actually got wider. These changes suggest to me that the inflation outlook is still being clouded by uncertainty, but the Fed does still want to insist that it sees tariffs as inflationary.

- One more interesting thing to note on the inflation outlook is a shift in the risk assessment that didn’t align with the revisions to the projections. The right bar chart shows that 4 FOMC members shifted their view of risks to the inflation outlook from “weighted to upside” to “broadly balanced.” This detail is further evidence that there is a growing split in the inflation assessment that should be watched closely.

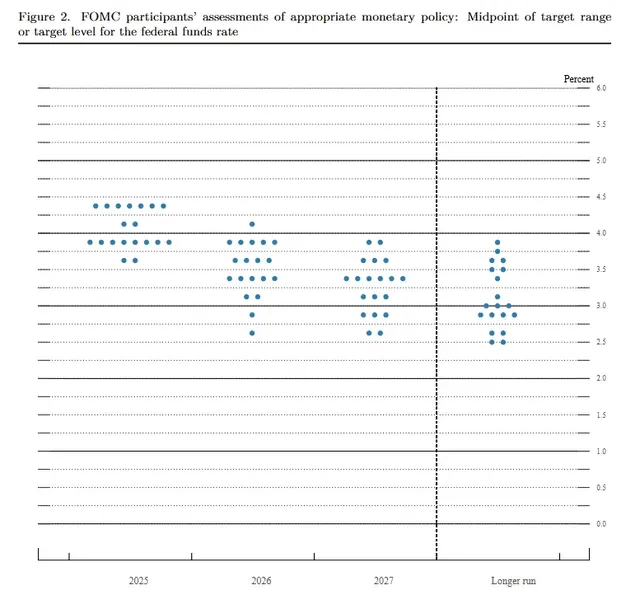

Overall, the economic projections pointed to weaker growth, a weaker labor market, but higher prices, a dynamic situation that suggests the Fed will have to find a delicate balance between its employment and inflation mandates. The balance in the forecast shift has caused the median projection for the federal funds rate target level to be unchanged for 2025 and shifted up slightly for 2026, from 3.375% to 3.625%. However, that balance comes as a result of an even split among policymakers. For 2025, there are nine FOMC participants who see 0-1 quarter-point cuts, and there are ten FOMC participants who see 2-3 quarter-point cuts. These dynamics make it hard to decipher any kind of policy rate path, and, in the end, maintain a similar level of uncertainty than was seen in the March projections.

In my opinion, these projections lean hawkish since they appear to disregard the progress in inflation that we have seen in the last few months despite tariffs. Near-term inflationary pressures have renewed the disinflationary trend that was lost in the first quarter (a main reason why the Fed turned more hawkish), and that doesn’t seem to have resonated with the Fed, or at least (roughly) half of the Fed that sees no rate cuts this year and core PCE inflation jumping back above 3%.

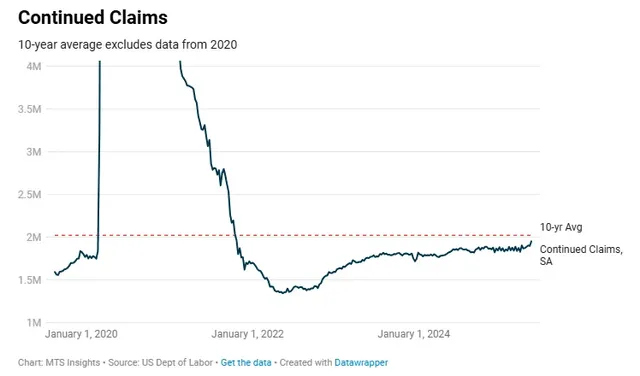

In terms of the outlook, I believe the Fed feels too secure about the labor market and economic activity as sources of strength in the demand side of pricing pressures. Just look at recent retail sales data (-0.9% MoM in May, below expectations) and rising continued claims data (highest since November 2021), and the cracks are showing. For these reasons, I see the June round of projections as more hawkish than expected, which should put upward pressure on short-term interest rates.

Fed Chair Powell Press Conference

In the post-meeting press conference, Chair Powell’s opening statement sought to reinforce the Fed’s “wait and see” position. The two main points underpinning the patience on policy changes were ones that we have heard before:

- Powell reasserts that the labor market remains solid and does not require any extra attention at this point, saying, “Overall, a wide set of indicators suggests that conditions in the labor market are broadly in balance and consistent with maximum employment.” This employment assessment has been the same in each 2025 meeting so far and is a key assumption in the “wait and see” position.

- Inflation has come down as seen in recent data, but Powell redirects from that to point out that tariffs complicate the future path of inflation. Because tariff effects are uncertain and perceived to be weighted to the upside (“Increases in tariffs this year are likely to push up prices… the effects could be short-lived or more persistent”), the motivation for a cut is dismissed.

At the end of the opening statement, we get a quote we’ve heard before, summing it all up.

“We are well-positioned to wait to learn more about the likely course of the economy before considering any adjustments.”

Powell was challenged on this position in the question-and-answer portion of the press conference. Multiple reporters pressed him on why the Fed chose not to cut rates in June despite cooling inflation, signs of economic softness, and consumer strain. Powell emphasized that while inflation has improved, the full impact of recently imposed tariffs remains unclear and is expected to show up over the coming months.

“Without tariffs, that confidence [in falling inflation] would be building… but we have to learn more.”

He reiterated that monetary policy must be forward-looking and cautioned against premature easing, noting that the Fed needs more data to understand whether the tariff-driven price increases will be temporary or more persistent. Despite acknowledging that inflation could remain contained, Powell reiterated that the Fed is “well-positioned to wait and learn,” underscoring the high degree of uncertainty and the need to avoid misreading a potentially transitory inflation bump as something more entrenched.