Bank of England Monetary Policy Decision: May 2025

The Bank of England moved forward in a contested decision with a quarter point rate cut following its May meeting. There were supporters that were both more hawkish and more dovish in the deliberations, and ultimately, the more neutral position won out. The division is a good representation of the Bank of England walking a tightrope, trying to balance the hotter inflation outlook and cooler growth expectations.

Decision

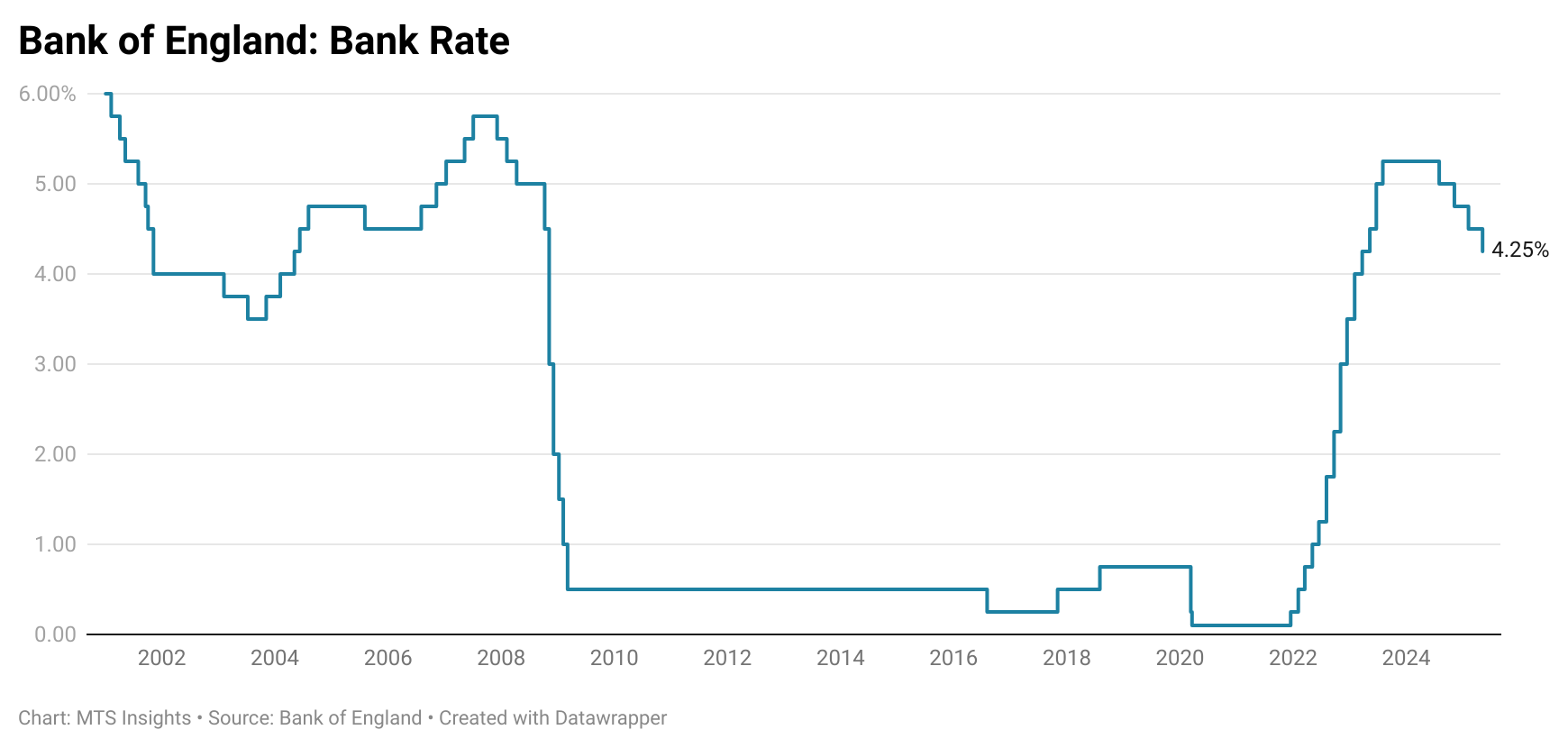

The Bank of England voted by a narrow 5–4 margin to lower its Bank Rate by 25 bps to 4.25% at its May meeting, marking the start of a gradual policy easing cycle. The decision was highly contested: two members pushed for a larger 50 bp cut, arguing that persistent disinflation and weak domestic demand justified more accommodation, while two others voted to hold rates steady, citing continued inflationary pressures and firming household inflation expectations. The majority ultimately favored a middle ground, judging that inflation progress had been sufficient to begin withdrawing some policy restraint without abandoning a restrictive stance altogether.

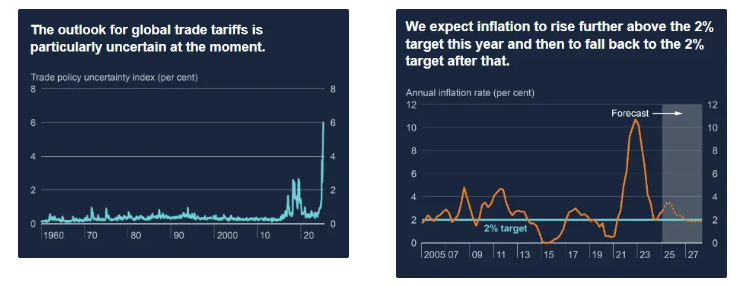

The decision reflects growing concern about weakening global growth and uncertainty surrounding new trade policies, as well as slowing domestic momentum. The Bank still expects headline inflation to temporarily rise in Q3 due to energy-related base effects, but sees that increase as transitory. Importantly, the MPC emphasized that monetary policy is not on a pre-set course and remains data-dependent. However, for those observing the trend, the cut today continues a pattern of alternating between a pause and a 25 bps cut that has been evident since August 2024.

Monetary Policy Report

The May policy announcement comes with an update to the Monetary Policy Report put together by the BoE members which features key forecasts updates and discussion about the economic and monetary policy outlooks. The key parts of the report are updates to the inflation and growth forecasts which reflect some shifts in data since the last Monetary Policy Report (MPR).

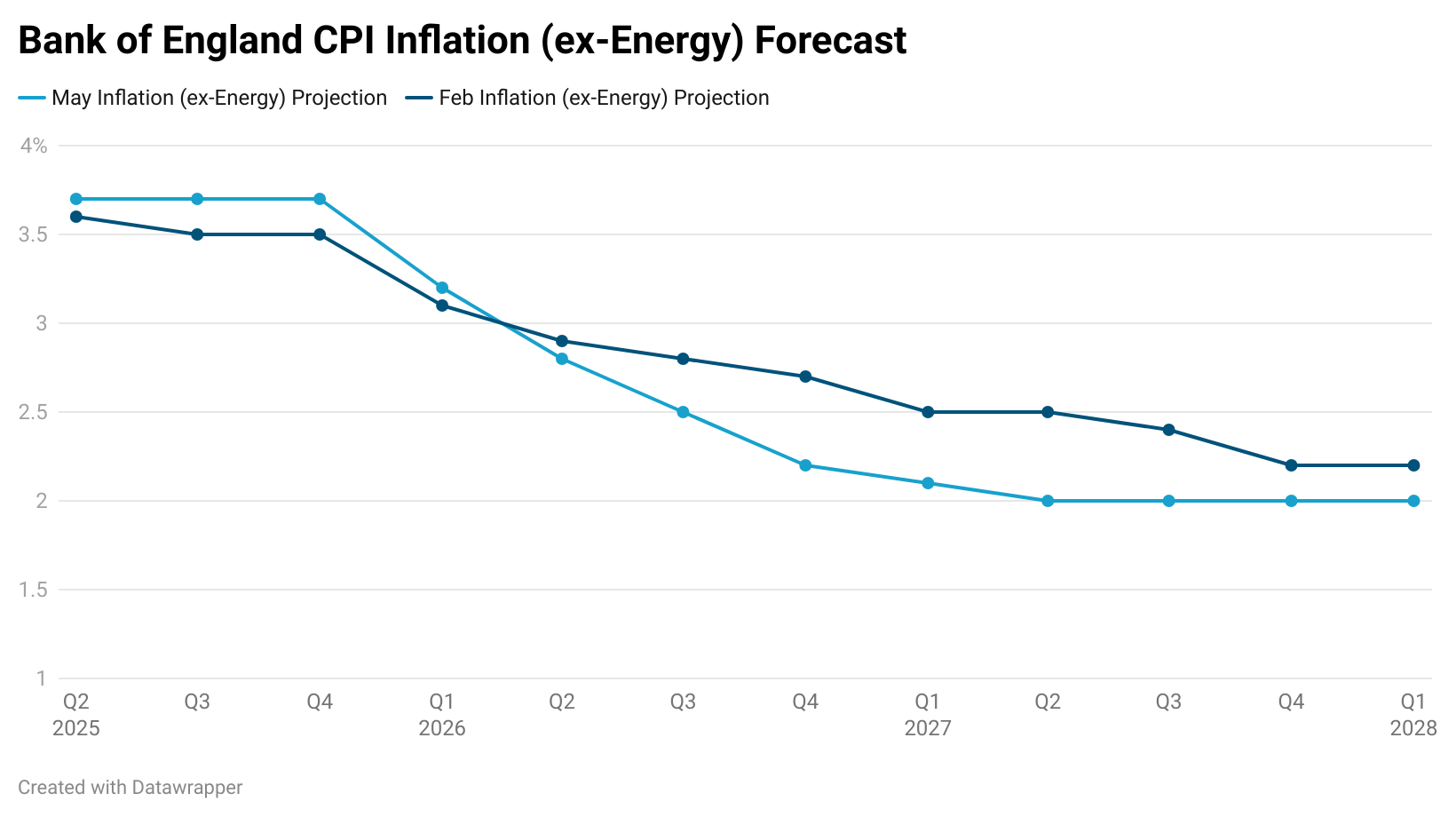

The BoE updated its forecast for inflation after price growth in the first quarter of the year was reported in line with expectations. The estimates for inflation in the next four quarters were raised in the May update, only slightly above the February estimates, but in the medium- to long-term, the BoE actually sees significant disinflation. It now projects CPI inflation (ex-energy) to fall to 2.0% by Q2 2027, while the February forecast did not reach that level. The BoE maintains its position that the increase in inflation in the near term is transitory and that inflationary pressures would dissipate due to “a period of excess economic slack” or weaker growth.

The BoE also updated its forecast for GDP growth, and it reflects some of the upside surprises that we have seen in the monthly data from the ONS. The February forecast for four-quarter GDP growth was well beaten at 1.2% vs the expected 0.4%. Because of that, the near-term estimates of GDP growth have been moved up to reflect a smoother path of real GDP growth over the next few quarters as the BoE still sees economic growth weakening in the short-term. This partly incorporates expectations that the volatile trade environment will cause excess supply to ”widen over the next couple of years, to just under 1% of potential GDP, before narrowing by the end of the forecast period.”

The May edition of the Monetary Policy Report made clear that the primary reason for today’s rate cut was the ongoing “progress in reducing domestic inflationary pressures,” which gave the Bank enough confidence to begin gradually withdrawing policy restraint. At the same time, the BoE flagged growing global trade uncertainty, particularly around US tariffs, as an additional downside risk to UK growth and a counterweight to any potential upside inflation risks. This caution comes despite stronger-than-expected GDP growth in late 2024 and early 2025. Still, the Bank did not commit to any future path of policy, noting that monetary policy would need to stay restrictive “until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further,” signaling a continued emphasis on a data-dependent approach.