Bank of England Monetary Policy Decision: March 2025

The Bank of England opted to keep its policy interest rate unchanged following its March meeting with a solid majority voting for the action. This pause appears to be in line with the Bank of England’s cadence of cuts that started when the central bank first cut rates in August 2024. Since then, the policy rate is down 75 bps, but a cautious outlook clouded by uncertainty kept the Bank of England on the sideline today.

Decision

By a vote of 8 to 1, the Bank of England opted to keep the Bank Rate unchanged at 4.5% in March 2025. The sole dissenter, Swati Dhingra, voted for a 25 bps cuts after disagreeing with the February decision as well, voting for a larger 50 bps cut. The pause confirms that the Bank of England wants to move forward with its cutting cycle gradually, and it appears to be doing that through a pattern of rate cuts every other meeting. So far three cuts have followed this pattern: 25 bps cut in August, pause in September, 25 bps cut in November, pause in December, 25 bps cut in February, pause in March. This suggests that the Bank of England will be considering a cut in the next meeting in May if disinflation continues as the it expects.

Inflation Outlook

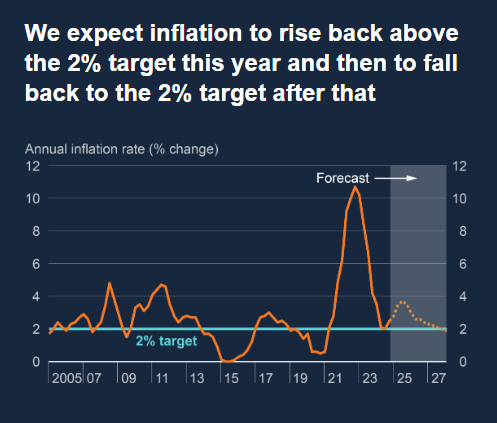

The BoE remains fixated on the goal of combatting inflation which is the main reason why we are seeing pauses every other meeting. The inflation situation has improved significantly since 2023, but the BoE still wants to maintain the Bank Rate “in restrictive territory so as to continue to squeeze out persistent inflationary pressures.” That hawkish sentiment is tempered by the fact that the Bank admits that “there has been substantial progress on disinflation” which has allowed them to ease monetary policy in the last six months.

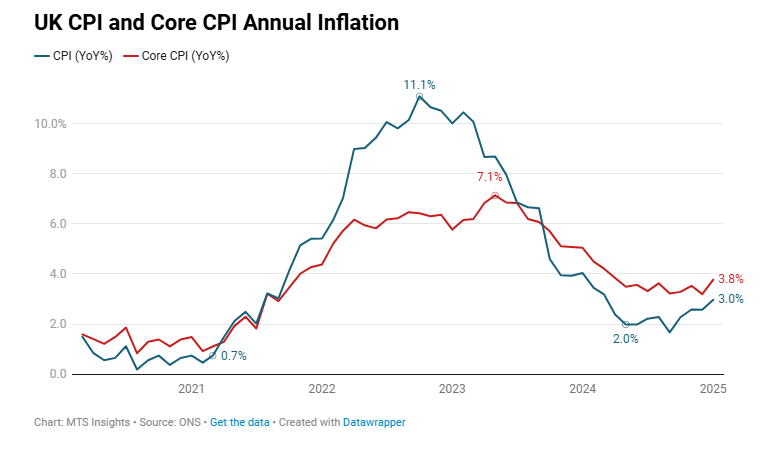

Unfortunately, recent data has started to run against the Bank of England. The annual increase in CPI inflation increased to 3.0% in January which was above the BoE’s forecast in the February Monetary Policy Report. Core inflation ticked up as well, rising to 3.8% YoY, the highest since April 2024. The inflation forecast did account for a rebound in energy prices in the first half of the year, but that rebound might be happening faster than expected. With trade uncertainty on the rise and threatening to become a new inflationary pressure in supply chains, the BoE was probably correct to pause today and may be likely to break its rate cut cadence in the next meeting.

Growth Outlook

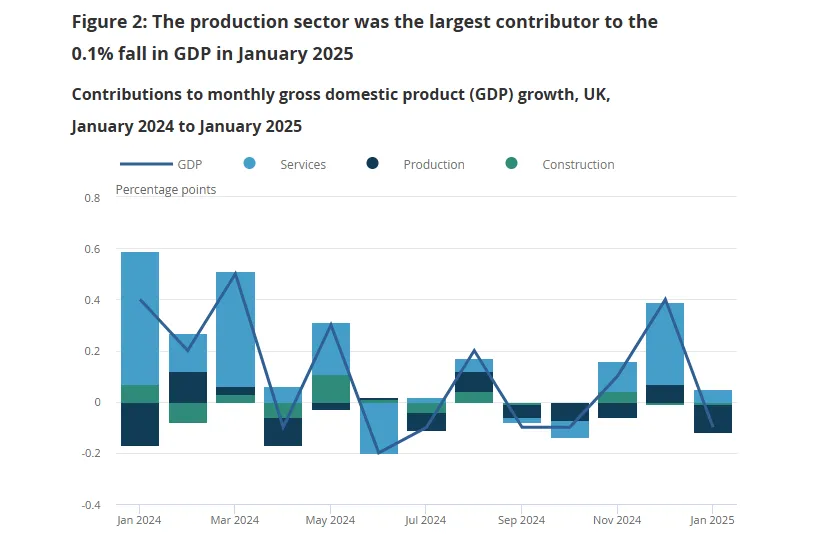

A key downside risk to the inflation outlook is a slowdown in growth that would create some downside pressure on prices from the demand side. The Bank of England likely scrutinized the GDP report in January which revealed that the UK economy contracted to start the year to decipher whether or not a new downtrend in growth is coming. Its growth outlook appears to be a bit dim as in the BoE’s Minutes it noted that “growth was expected to slow on the back of tariff and wider policy uncertainty, among other factors” and that indicators for Q1 2025 growth reflected “a weakening in household consumption growth” and that “firms’ output and investment expectations had also fallen.”

Despite hard data signaling some weakness, the outlook is still for slight growth in Q1 2025. The BoE makes it clear in its statement that growth is an important consideration in its inflation outlook: “Should there be greater or longer-lasting weakness in demand relative to supply, this could push down on inflationary pressures, warranting a less restrictive path of Bank Rate.” This balance of inflation and growth is key in the BoE’s decision-making.

Monetary Policy Outlook

While the March decision was relatively settled and a pause was largely expected, the next May decision to cut will be more uncertain. The BoE has not given any direct guidance on next month’s decision, but instead, it reaffirmed its intention to maintain “a gradual and careful approach to the further withdrawal of monetary policy restraint.” Guidance leaves open two paths that are will be determined by the balance between supply and demand pressures. If demand sees a “longer-lasting weakness” relative to supply, the BoE might opt for a less restrictive Bank Rate. If supply is more constrained relative to demand, putting upward pressure on inflation, the BoE might opt for a tighter monetary policy path.

While it seems like both paths are weighted similarly, the Bank of England does appear to be leaning in one direction. Based on its forecasts and language, it likely sees more upside risk to the inflation outlook than downside risks to the growth outlook. The March deliberations ended with a clear hawkish tilt: “Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further.” With that being said, I believe that the BoE is more likely to pause in May unless data changes the outlook significantly.