Federal Reserve Monetary Policy Decision: May 2025

The Federal Reserve kept rates unchanged for the third consecutive meeting today as it continues to avoid rate cuts and assess the developing economic impacts of the newly implemented and threatened tariffs. The key difference between this month’s meeting and the March meeting is several new data points to contend with, including a negative Q1 GDP print.

Statement

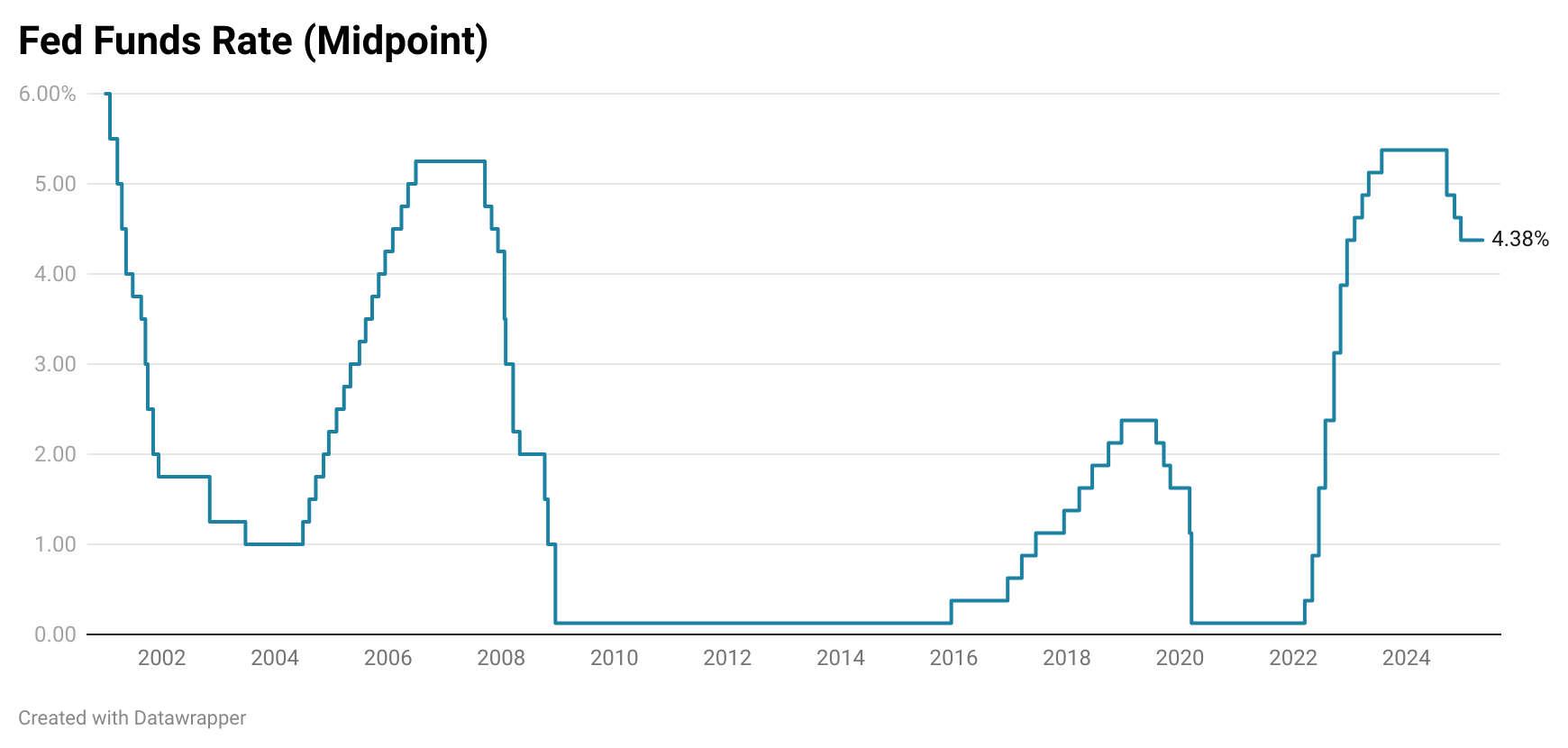

The Federal Reserve kept the target rate of the Fed Funds rate unchanged at 4.25% to 4.50% in the announcement today. This is the third straight pause since the last rate cut in December. The FOMC also made no changes to its quantitative tightening (QT) measures, which were updated in the previous announcement in mid-March. The actions were agreed upon unanimously, which is a slight difference from the last meeting when FOMC Governor Christopher Waller voted against easing up on QT.

Aside from these differences, there were no major changes to the statement, just minor changes that provided some nuance to the typical assessments in the press release.

- The change at the beginning of the release is an attempt to address the negative Q1 2025 GDP growth print, which was heavily impacted by trade dynamics. The FOMC members want to make it clear that it is looking through the recent surge in imports to other indicators that showed the economy was still growing like the real final sales to private domestic purchasers aggregate (sum of consumer spending and gross private fixed investment) which grew at a SAAR of 3.0%, slightly above the Q4 2024 2.9% gain. Powell actually points to this data point in his opening remarks of the press conference.

- The minor adjustments made to the second paragraph highlight the increasingly uncertain outlook that consumers and businesses are facing due to Trump’s new trade policy. It seems that now the FOMC members are making it clear that they see upside risks to unemployment and inflation, which were first communicated in the March SEP materials.

Overall, the statement was largely in line with prior communications, but it carried a more cautious tone reflecting the FOMC's growing awareness of a softening outlook. While hard data, such as labor market conditions and economic activity, continue to appear "solid," the Fed acknowledged more uncertainty stemming from soft indicators like consumer sentiment and regional Fed surveys. These subtle shifts suggest the Committee is more attuned to downside risks, even as headline figures remain resilient. At the same time, the Fed’s outlook for inflation has also firmed up as it sees tariffs forcing companies to increase selling prices.

Press Conference

The FOMC press conference continued with the theme of a weaker economic outlook and unique upside inflation risks from tariffs. Powell acknowledged downside risks have risen, especially from trade policy, but emphasized they have not yet materialized in official data. He pointed out particularly that soft data continued to deteriorate while hard data had remained solid. Overall, the outlook is still uncertain, and the FOMC could not make assumptions about the timing and magnitude of the effects of tariffs on the outlook.

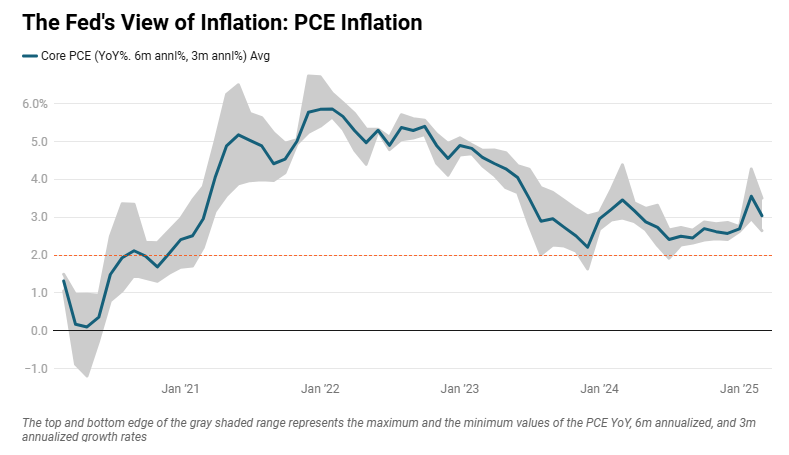

Regarding inflation, the Fed still sees inflation as above target, but Powell noted that it had eased significantly since mid-2022. While inflation has fallen, short-term inflation expectations have started to rise in response to tariff policy changes, but the FOMC still sees long-term inflation expectations as anchored. The Fed has not determined whether it sees tariffs as a temporary driver of pricing or if it will become a more persistent problem. Despite early inflation signals, FOMC members have opted to keep policy as it is until more is known about how trade policy plays out.

While Powell made sure to highlight the uncertainty in the inflation outlook, one quote during the Q&A session sticks out: “the underlying inflation picture is good.” In my view, the Fed’s focus is a bit more on the growth and unemployment side of the mandate as opposed to the inflation side. Yes, tariffs are likely to be a supply shock that drives prices higher, but the deflationary pressures from a much softer consumer are a bit overlooked. I believe that firms will struggle to successfully pass through most of the tariff costs and that the Fed is tuned into this downside risk.

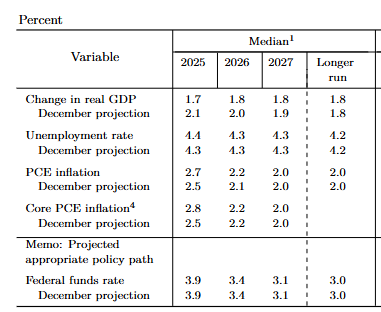

On the policy outlook, Powell made clear that the Committee is not currently committing to rate cuts and is comfortable maintaining the current stance for now. While the March Summary of Economic Projections included two cuts penciled in for 2025, Powell acknowledged that recent developments, particularly around trade policy, have introduced enough uncertainty to potentially change that path. Indeed, the Fed continues to be caught out by Trump’s policy announcements:

He emphasized that the Fed's policy rate is “moderately restrictive” and well-positioned to respond flexibly as more data comes in. Any shift in policy, whether a cut or an extended hold, will be determined by how the balance of risks evolves, and not made in anticipation of future developments. Indeed, Powell stuck with his favorite phrasing of this dynamic throughout the Q&A session: “We don’t have to be in a hurry [to cut].” Funnily enough, this is one of Trump’s main criticisms, calling him “Mr. Too Late” in a Truth Social post a few weeks ago.

On the topic of President Trump and the new administration, Powell was asked about the escalation in political pressure and criticism in the last few months. Once again, the Fed Chairman reaffirmed that Fed decisions are not influenced by political pressure. In fact, his position seemed firmer than ever. In response to a question about whether Powell had “asked for a meeting” with President Trump, he responded bluntly:

If Chair Powell did anything in the press conference, he reassured the markets that as long as he is leading the Fed, there will be no political interjections into monetary policy.