Federal Reserve Monetary Policy Decision: March 2025

In the second meeting of 2025, the Federal Reserve kept the target range of the Fed Funds rate at 4.25% to 4.50% meeting expectations that the US monetary authority would remain in a wait and see mode. While rate policy was unchanged, the Fed did decide to make some adjustments to its quantitative tightening (QT) policies in order to ease financial conditions in a particularly volatile period for financial markets.

Statement

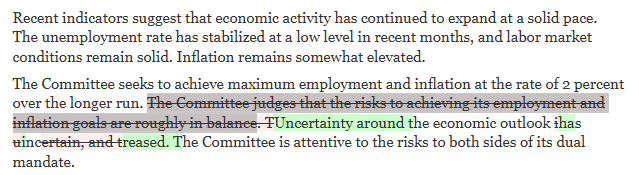

In its main statement, the Federal Reserve indicated its intention keep rates the same as it tries to look through the new rise in uncertainty that has come in the Trump administration’s first two months in power. There were not many changes to the press release’s assessment of the economic situation. The Fed still sees economic activity expanding at a “solid pace” and “solid” labor market conditions while inflation is described as “somewhat elevated.”

The first change came in the second paragraph as the FOMC decided to communicate its sense that uncertainty was clouding the outlook. It removed the sentence “The Committee judges that the risks to achieving its employment and inflation goals are roughly in balance,” and updated the next sentence to point out that “uncertainty around the economic outlook has increased.” Essentially, if the Fed had any kind of clarity on the inflation and employment situation in January, it no longer has that due to the seismic shifts in government policy.

This frames the March pause in a very different way than the January pause. The January pause was a break from cuts to let inflation data confirm a downtrend. The pause today is done out of a necessity to reassess the economic outlook in the face of the new reality of widespread tariffs and the potential for a large decline in government spending. Going into the new year, it felt like the Fed was only looking to move rates in one direction in 2025, but now it seems like all directions are in play.

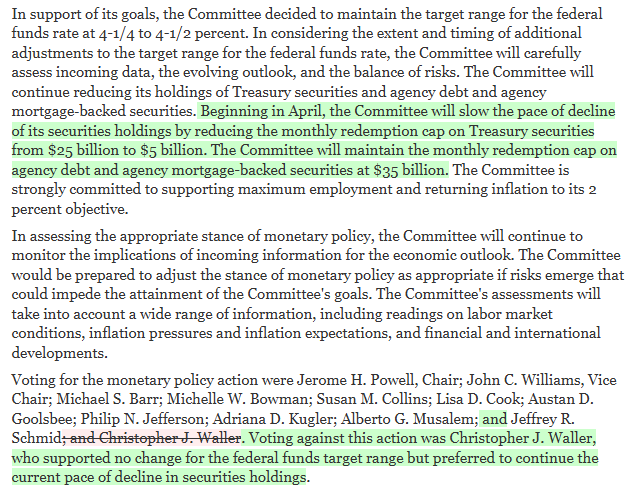

The second and third changes in the statement are related to the shift in quantitative tightening that had been suggested by some analysts as a possible policy adjustment in the face of financial market turbulence. Indeed, the FOMC opted to reduce the pace of quantitative tightening by reducing the drawdown of Treasury securities on its balance sheet from $25 billion a month to just $5 billion a month. The final change relates to Governor Waller voting against this new pace of balance sheet run off but not voting against the pause on rates. A reduction in quantitative tightening should allow for some easing in financial conditions to improve liquidity during volatility.

Summary of Economic Projections

This FOMC meeting was accompanied by an update in its Summary of Economic Projections (SEP) which was last adjusted in its December FOMC meeting that preceded the inauguration of President Trump. Thus, this first attempt by members to try and digest how the economy changes under new leadership.

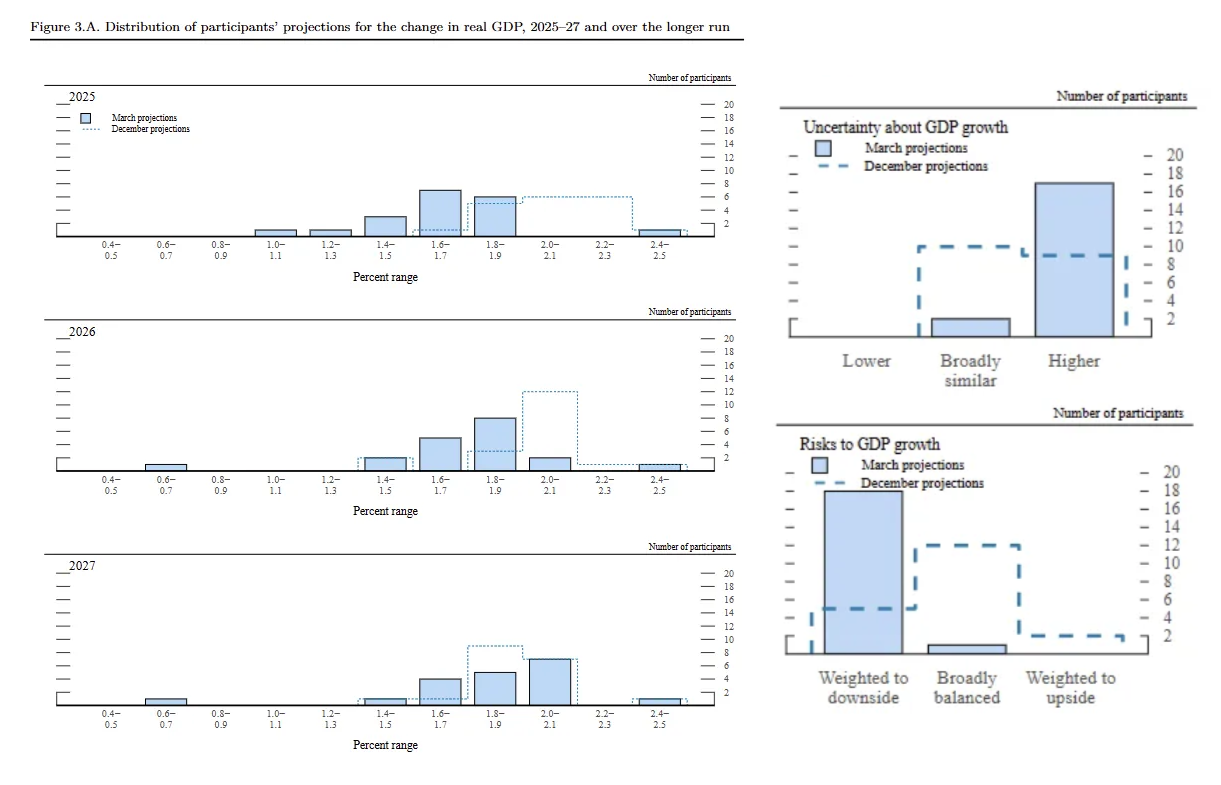

- The projections with the most changes were in GDP growth over the next three years. The median projection was revised down in each of those three years with the largest downward revision being the -0.4 ppts downgrade to 2.1% for 2025. The change in the 2025 median came from 12 members abandoning their projections of 2% or higher growth this year with just one member at 2.4% to 2.5%. The downgrade was accompanied by a major shift upward in uncertainty and risk assessment that is now heavily weighted to the downside.

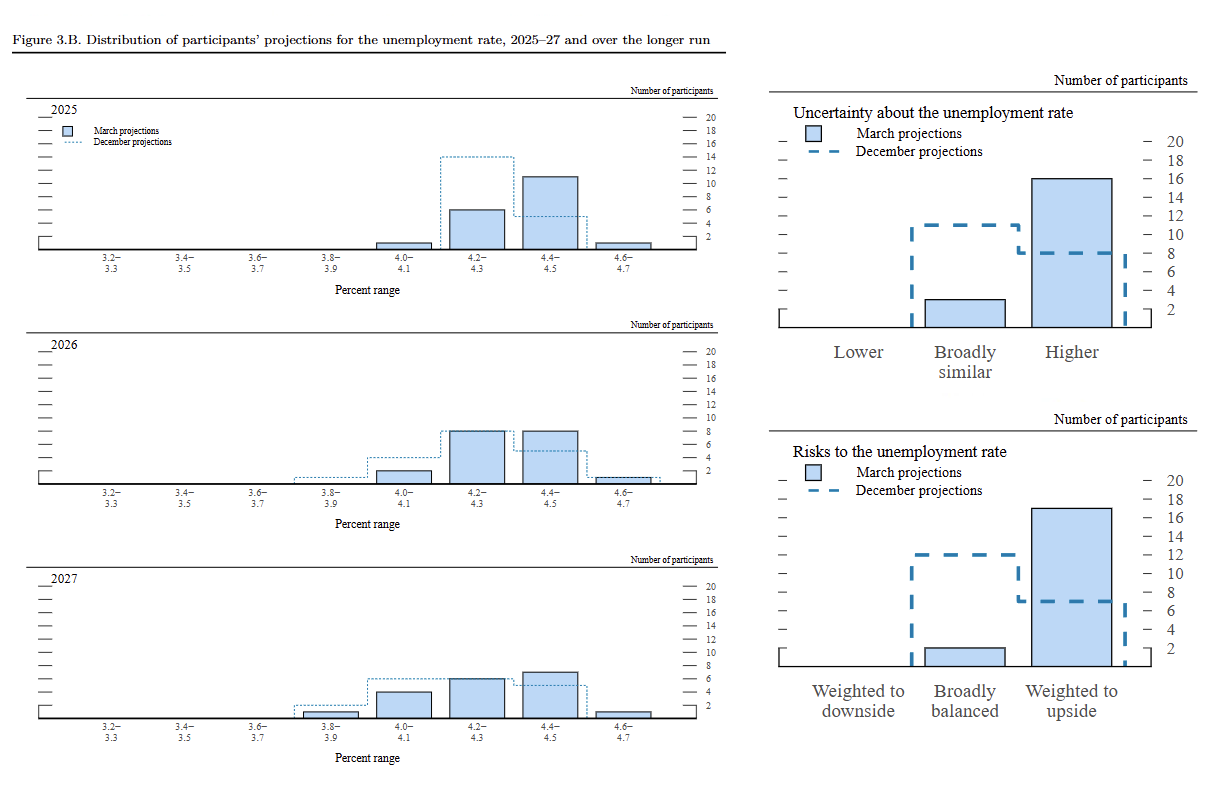

- FOMC members appear to be confident that the labor market will remain strong as it mostly confirms its forecasts for the unemployment rate. The only change was a minor upward revision of 0.1 ppts in the median projection of the 2025 unemployment rate. However, FOMC members agreed broadly that the risks to unemployment were weighted to the upside and shrouded in uncertainty.

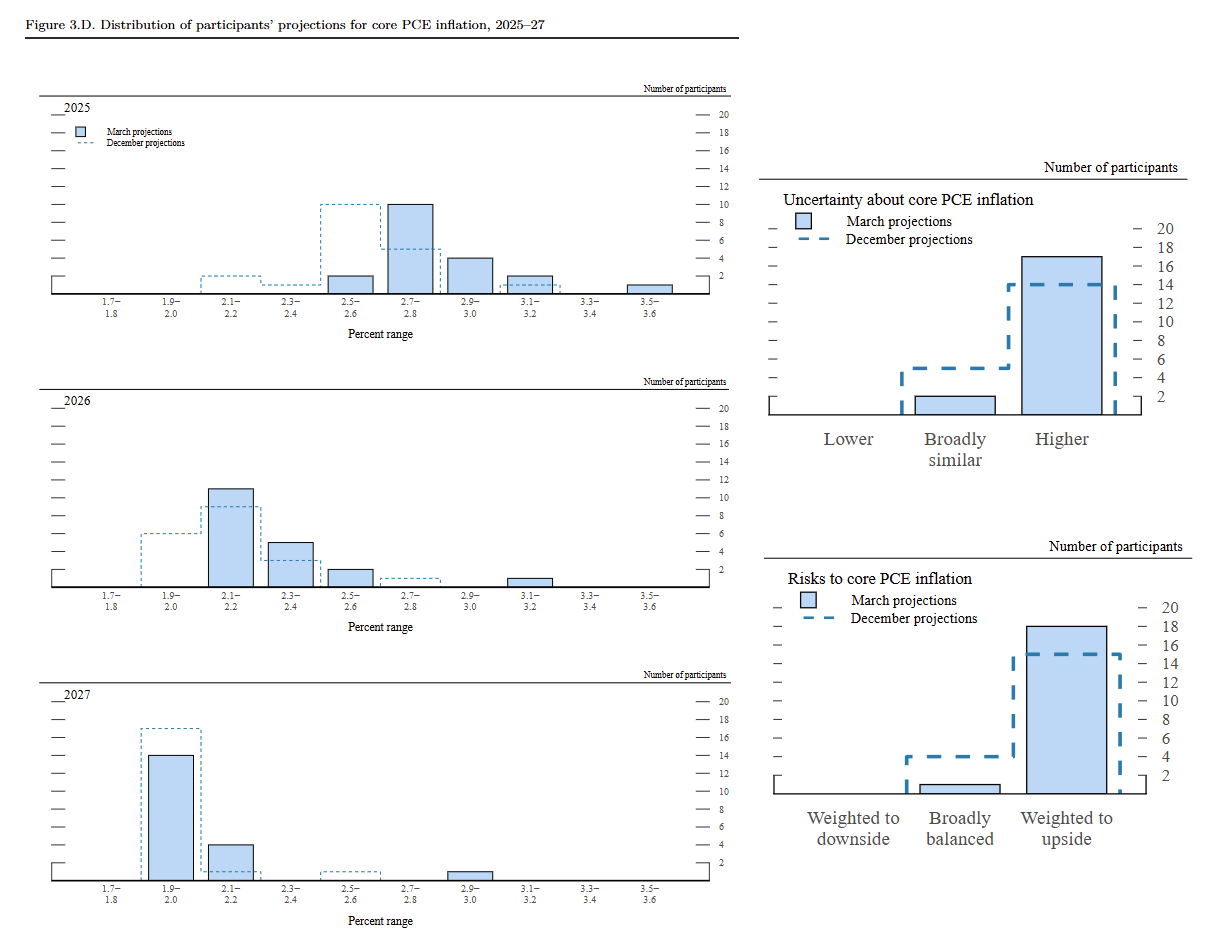

- The updated inflation projections likely do include some thoughts on how tariffs will flow through to prices as that is one of the early Trump policies that has been put in place. FOMC members project a pick up in inflation this year with the median PCE inflation forecast up 0.2 ppts to 2.7% and the median core PCE inflation forecast up 0.3 ppts in 2025. This suggests that the initial assessment of the impact of tariffs on inflation is that the increase could be transitory or that weaker growth could offset the potential for higher inflation. Like other projections, there was an increase in uncertainty and a strong weight placed on upside risks.

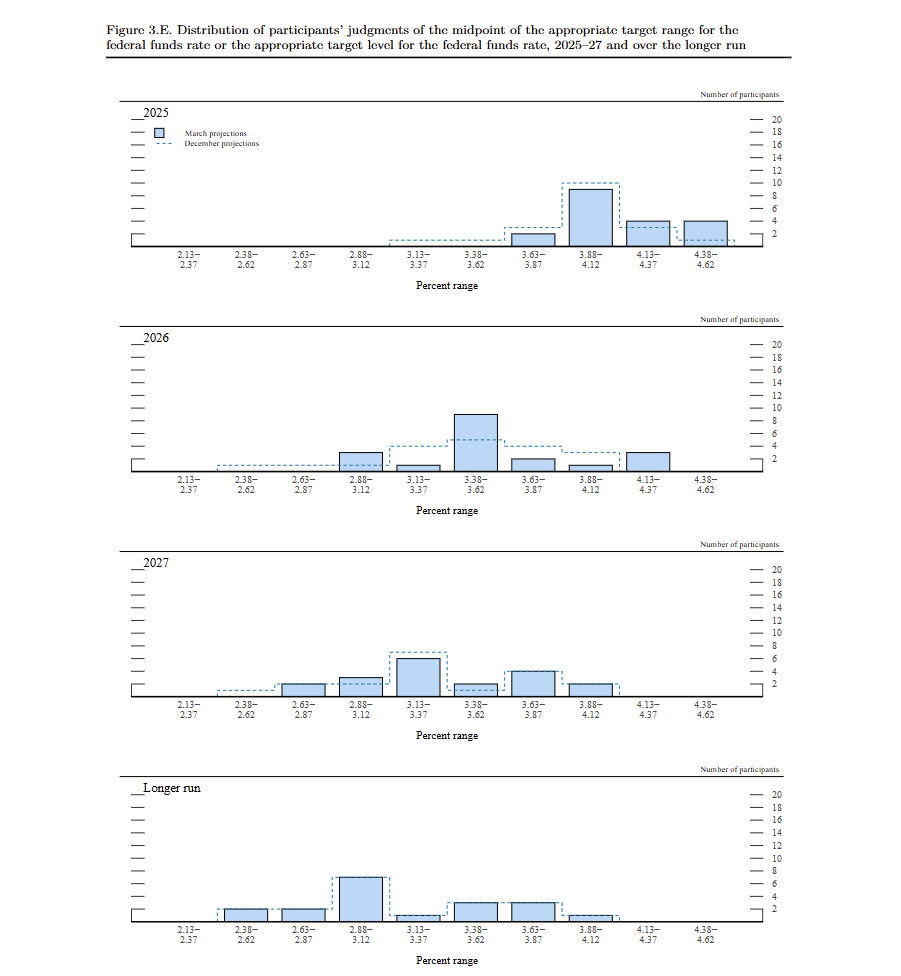

- Through it all, the median projections for the Fed Funds rate were kept the same from December to March. The 2025 distribution was basically unchanged with most FOMC members looking for 1-2 cuts this year. The 2026 distribution shifted a lot with some members moving towards the extremes while most landed on the target range of 3.25% to 3.50% which would be about 100 bps of cuts in two years. With the inflation forecast revised up and the general consensus being that tariffs will be inflationary, an unchanged policy path projection looks dovish.

Press Conference

In the post-FOMC meeting press conference, Chair Powell remained set on communicating that the Fed is in a wait-and-see mode as it wants to gain clarity on the economic outlook. He was not shy in pointing out that trade policy had been a major source of uncertainty. Powell made several references to “separating the signal from the noise” in distilling the impacts of new policies.

Additionally, he wanted to make the case that the Fed did not have to be in a hurry to change policy and that the economy was in a good state and could handle the current level of interest rates. The quote that sticks out was near the end of Powell’s opening remarks: “We do not need to be to be in a hurry to adjust our policy rates and we are in great position to wait for clarity.”

In the question and answer session, Powell was pressed on his and other members’ assessment of how tariffs had been factored into the economic outlook, especially the inflation outlook. He was questioned on the shift in core PCE inflation projections (2025 up, no change in 2026 and 2027 forecasts) meant that the Fed sees tariffs as a “transitory” inflationary pressure. His answer was the following

“I think that's the base case. But as I said we really can't know that. We are going to have to see how things actually work out. And the fact that there wasn't much change, I think that's partly because you see weaker growth but higher inflation.”

So it does seem like the Fed wants to look through the tariff inflation impulse as a temporary force. or at the very least, it sees the drag on growth offsetting the upward pressure on prices. Again, uncertainty is high, so it is hard to distill meaning from this, as it’s possible that FOMC members still believe that Trump is bluffing with tariffs. This appeared to be a key message for markets that made equities and rates react dovishly.

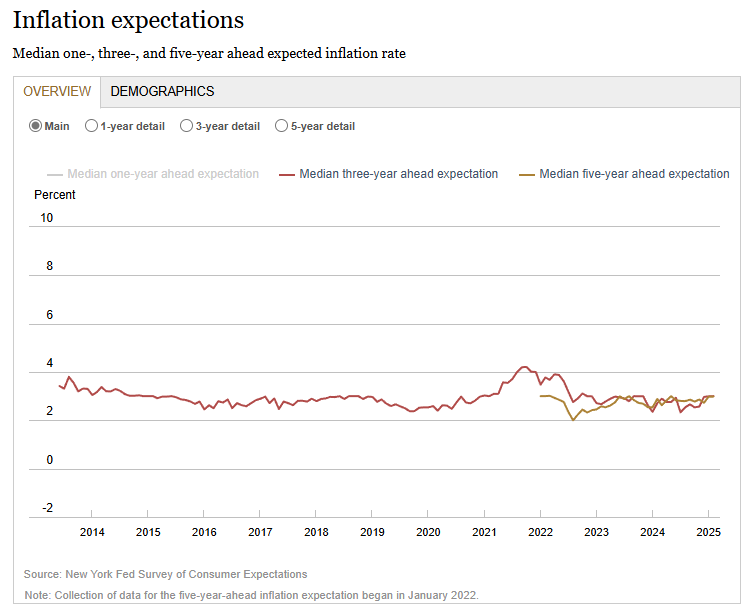

There were also several questions about inflation expectations, and whether or not the recent data in surveys (specifically the UMich consumer sentiment survey) was evidence of “de-anchoring” in inflation expectations. Powell was quick to blame tariffs for the rise in short-term expectations and pointed to long-term economic expectations remaining low and stable. He specifically points to the data in the NY Fed Survey of Consumer Expectations and market-based measures as evidence for his case.

Two of his statements stick out to me about the labor market and inflation:

- On the labor market: “What we have had is a low firing and low hiring situation. And it seems to be in balance now for - you know for the last six, seven, eight months.” This statement is a good overview of the current state of hiring. Unemployment remains low as there has been no major uptick in layoffs, but hiring has also slowed as demand for new workers gradually declines.

- On inflation: “We have had two very strong goods inflation readings in the last two months which is very unexpected.” The inflation outlook is extremely uncertain with tariffs and the Fed is looking at goods inflation as a signal. Powell mentioned these two monthly surprises in goods inflation twice in the Q&A session, and it sticks out to me as the upside risk that the Fed is watching out for on the price front.