Federal Reserve Monetary Policy Decision: December 2024

The Fed cuts by 25 bps to a range of 4.25-4.50%. In the statement, the Fed moves into data dependence mode as it “will continue to monitor the implications of incoming information for the economic outlook.” The FOMC will adjust its monetary policy stance if “risks emerge that could impede the attainment of the Committee's goals.” There was one dissenter who opted to keep rates unchanged. The Fed also released its SEP.

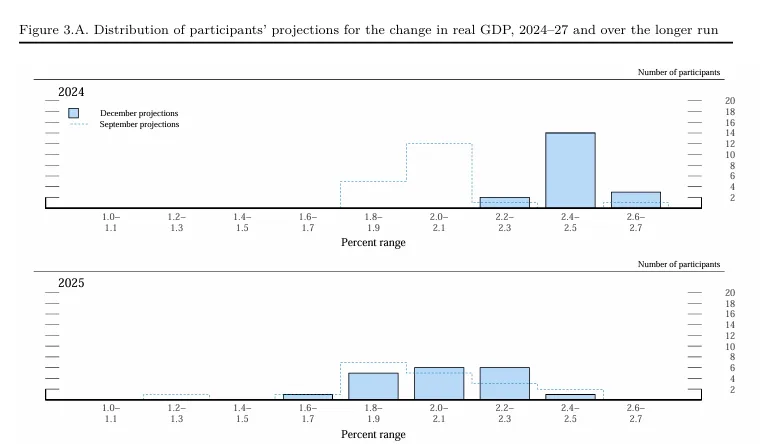

The Fed has upgraded its projections of growth in 2024 and 2025 by 0.5 ppts to 2.5% and 0.1 ppts 2.1% respectively. Largely, this reflects stronger-than-expected growth in Q3 and another strong quarter likely in Q4. The 2025 shift looks more significant in the histogram. The mode has shifted from between 1.8% to 1.9% to 2.0% to 2.3%.

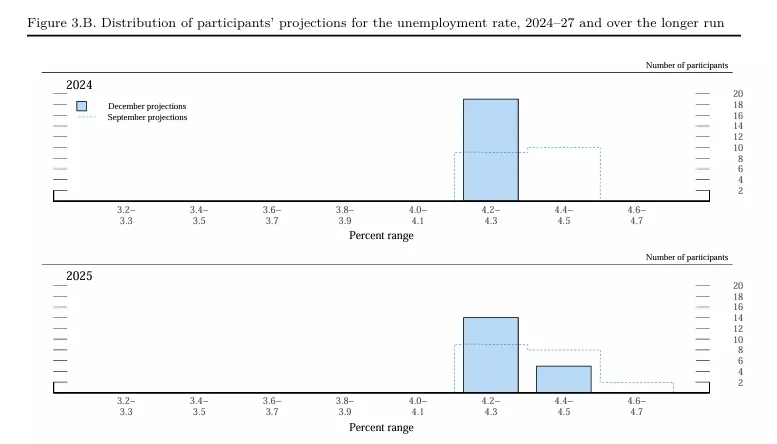

The Fed has adjusted its view of the labor market to account for stronger employment in the second half of 2024 and slightly stronger employment in 2025. Many more individuals have moved from expecting the unemployment rate at either 4.4% or 4.5% to either 4.2% or 4.3%. This appears to be an admission that the labor market is tighter than FOMC members initially thought and that the gradual weakening of the labor market might be very slight.

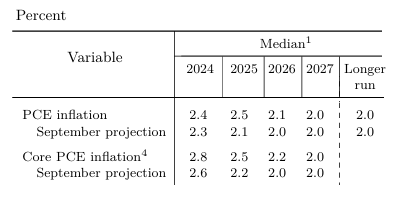

Inflation projections have moved quite considerably. The FOMC has admitted that core PCE inflation will overshoot its September projection at the end of 2024 with a reading around 2.8%. More concerning is a significant increase in the 2025 projection. Instead of core PCE inflation easing to 2.2% in 2025, the Fed now sees its favorite inflation indicator only falling to 2.5% by the end of next year. The upper bound of the range of FOMC projections increased 0.7% from September to December and sits at an ugly 3.2%. This could be the beginning of the Fed bringing the inflation mandate back into focus.

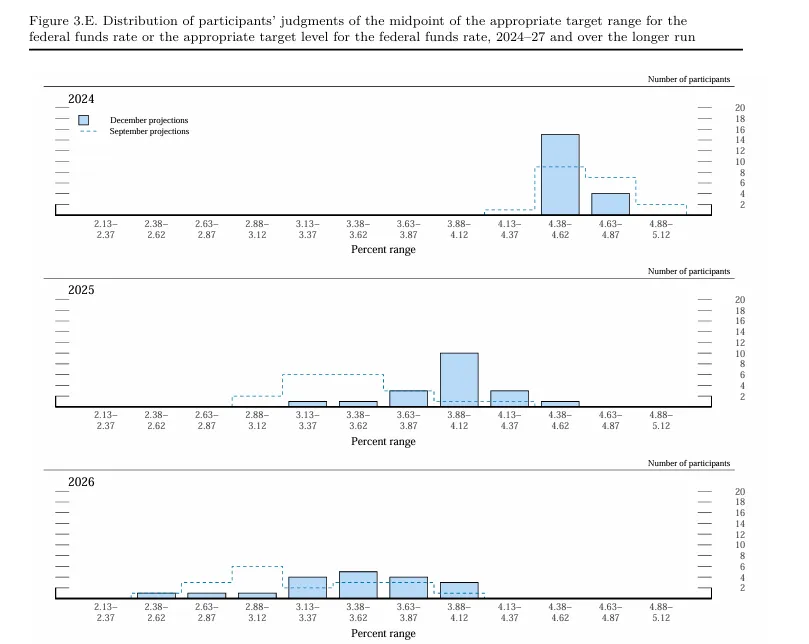

The Fed has completed a hawkish repositioning in response to stronger-than-expected growth and employment and renewed inflation concerns. The median forecast for the Fed funds rate at the end of 2025 was increased by 50 bps to 3.9% (Sep projection: 3.4%) in a significant upward shift in the distribution. There does seem to be a stronger consensus on where rates could land next year. 10/19 projections have a FFR midpoint of 3.9% with others split above or below that point roughly evenly.

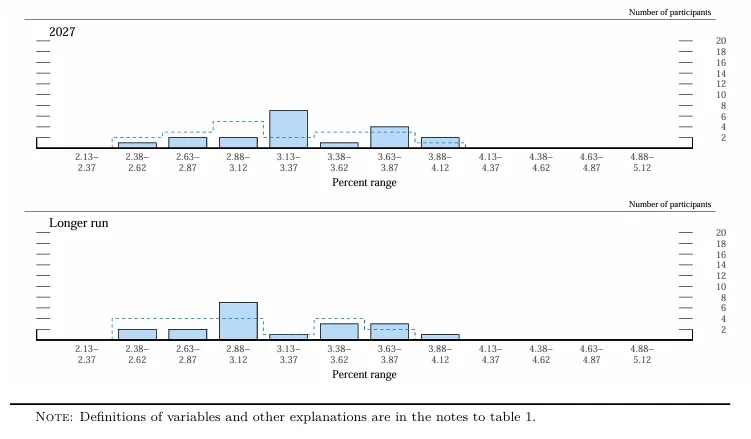

In 2026, there was a similar increase in the projection for the FFR by 50 bps to 3.4%. The distribution for projections shifted to the right but was more spread out. The range of projections was actually unchanged from September at 2.4% to 3.9%. In 2027 and the long run, the Fed sees rates settling at a higher level than before. The median long run rate, often used to represent where FOMC members see the neutral Fed funds rate, ticked to 3.0% with a mode being a range of 2.9% to 3.1%. Several members see a long-term rate settling above 3.3%.

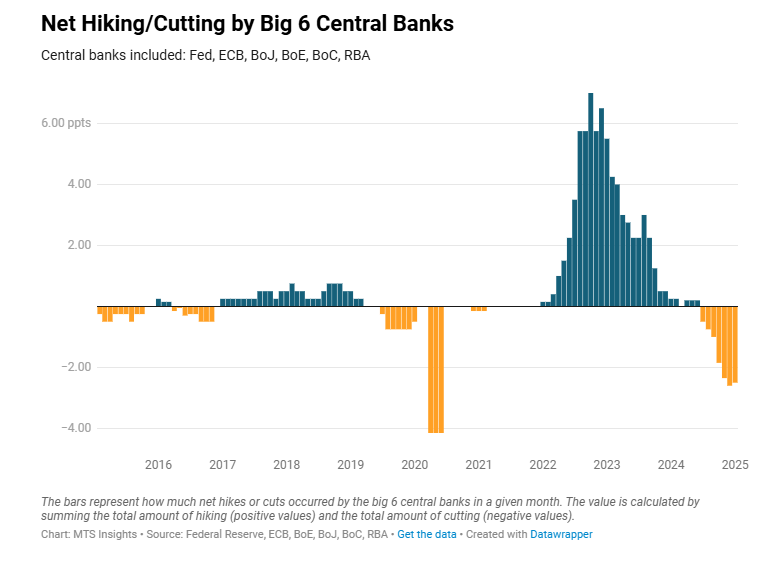

December falls to -2.5 ppts (or 250 bps of cuts). This is the second largest month in terms of cutting (behind only last month) since the pandemic.