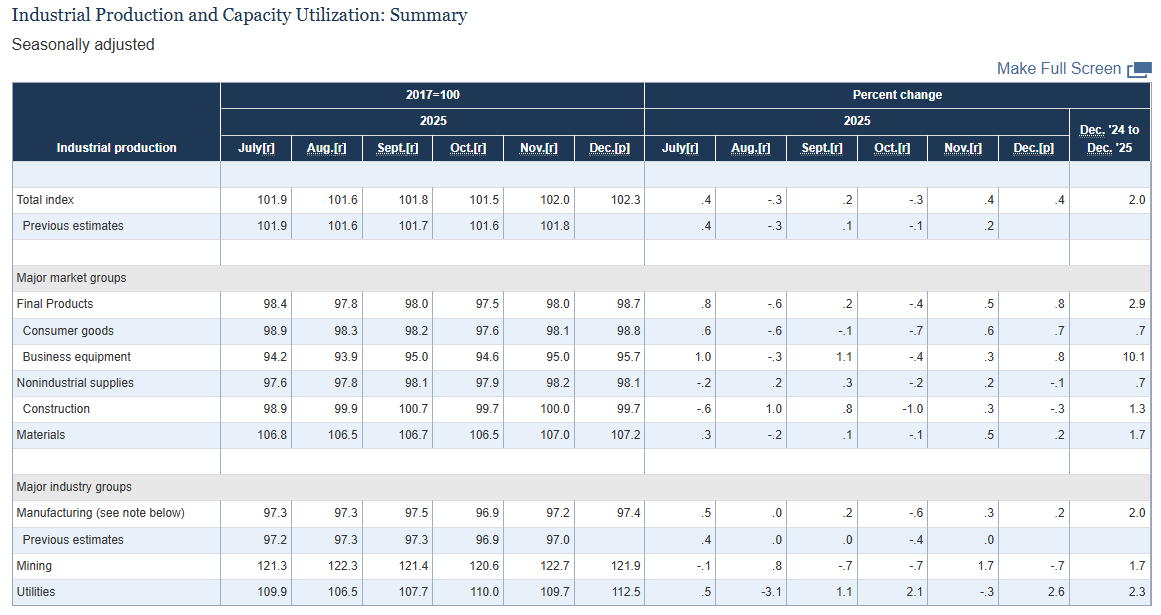

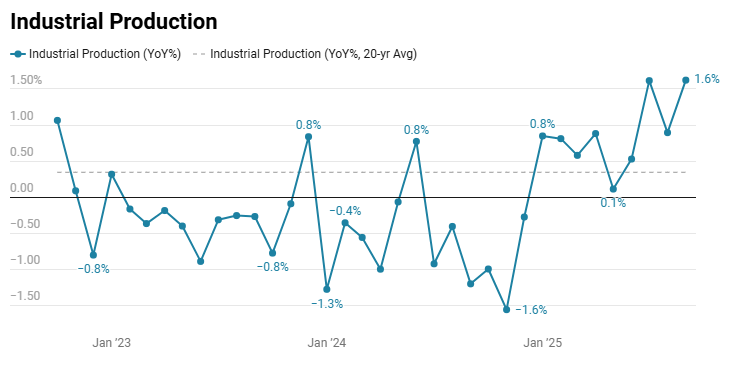

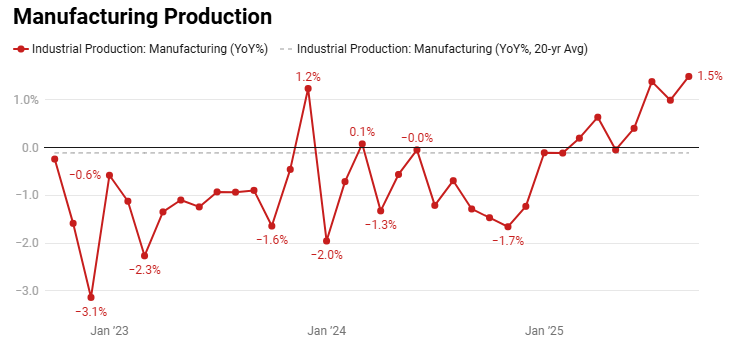

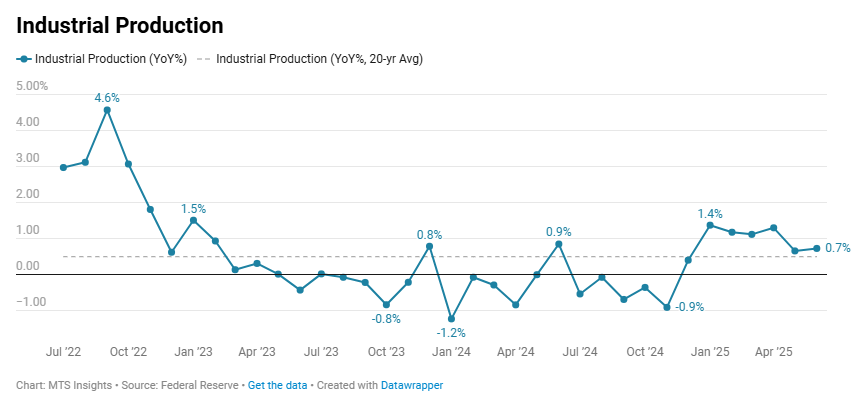

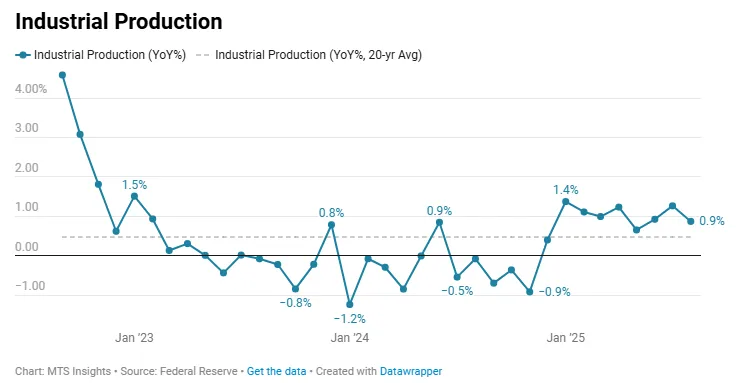

Industrial production increased just 0.1% MoM in August, ahead of the expectations of a -0.1% MoM drop, and the monthly drop in July was revised down from -0.1% MoM in the first estimate to a larger -0.4% MoM drop in the revised estimate. The acceleration in industrial activity seen at the beginning of this year continues to stall at the end of the summer. The annual increase in overall production slowed to 0.9% YoY after picking up to 1.3% YoY previously. Similarly, manufacturing production annual growth slowed from 1.3% YoY in July, which was the strongest increase since October 2022, to 0.9% YoY.

Despite the slight headline beat, the details of August’s industrial production report pointed to underlying softness. Capacity utilization remained stuck at 77.4%, well below its long-run average, while business equipment output slipped (-0.1% MoM) as declines in industrial equipment offset gains elsewhere. Within manufacturing, most of the modest 0.2% MoM increase was carried by a 2.6% MoM jump in motor vehicles and parts, with other factory output essentially flat and key categories like fabricated metals, machinery, and plastics posting declines. When excluding auto production, industrial production was flat, and durable goods production was down -0.2% MoM. Utilities were also a drag, with output falling -2.0% MoM as electric utilities contracted, underscoring the mixed performance across industrial sectors.