S&P Global Services PMIs: February 2026

Global - 3/4/2026

| Asia Pacific | Africa & Middle East | Europe | North & South America |

|---|---|---|---|

| Australia - 3/4/2026 | Nigeria* - 3/2/2026 | Ireland - 3/4/2026 | Brazil - 3/4/2026 |

| Singapore* - 3/4/2026 | Qatar* - 3/4/2026 | Spain - 3/4/2026 | Canada - 3/4/2026 |

| Hong Kong* - 3/4/2026 | Kuwait* - 3/4/2026 | Italy - 3/4/2026 | US - 3/4/2026 |

| Japan - 3/4/2026 | Egypt* - 3/4/2026 | France - 3/4/2026 | |

| China - 3/4/2026 | UAE* - 3/4/2026 | Germany - 3/4/2026 | |

| India - 3/4/2026 | Uganda* - 3/4/2026 | Eurozone - 3/4/2026 | |

| Russia - 3/4/2025 | South Africa* - 3/4/2026 | UK - 3/4/2026 | |

| Kazakhstan - 3/4/2026 | Lebanon* - 3/4/2026 | ||

| Ghana* - 3/4/2026 | |||

| Zambia* - 3/4/2026 | |||

| Saudi Arabia* - 3/4/2026 | |||

| Mozambique* - 3/4/2026 | |||

| Kenya* - 3/4/2026 |

* Composite only

Key Results

Highs & Lows

- Hong Kong (Composite) up 1.0 pt to 53.3, highest since March 2023.

- Singapore (Composite) up 2.4 pts to 59.2, highest since May 2022.

- China (Services) up 4.4 pts to 56.7, highest since May 2023.

- China (Composite) up 3.8 pts to 55.4, highest since May 2023.

- Kazakhstan (Services) down -2.5 pts to 48.0, lowest since February 2023.

- Kazakhstan (Composite) down -2.5 pts to 47.2, lowest since January 2022.

- US (Services) down -1.0 pt to 51.7, lowest since April 2025.

- Global (Composite) up 0.7 pts to 53.3, highest in 21 months.

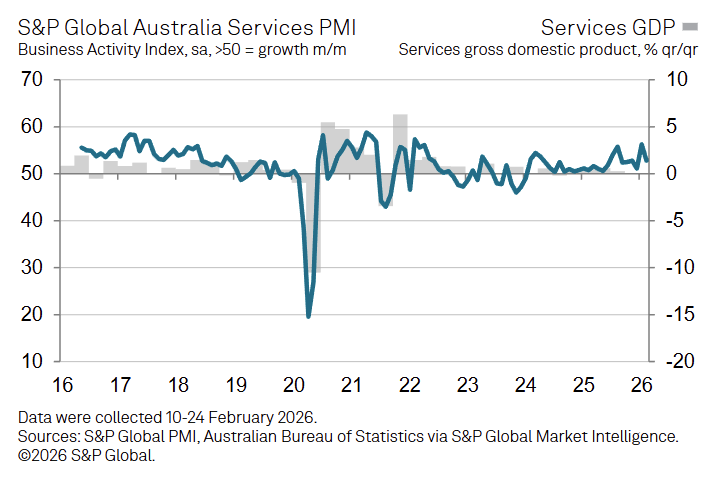

Australia

Australia’s Services PMI Business Activity Index eased to 52.8 in February (-3.5 pts MoM from 56.3) but remained above the 50 expansion threshold, extending the current services growth streak to just over two years.

-

Services activity remained in expansion at 52.8 in February (Jan: 56.3), indicating continued growth even as the pace slowed from an almost four-year high recorded at the start of the year.

-

New business continued to increase at a strong pace, though slower than in January, supported by new service launches and expanding customer bases among Australian service providers.

-

International demand for Australian services also rose further in February, although the rate of foreign demand growth moderated compared with the stronger increase seen earlier in the year.

-

Firms increased staffing levels at the fastest pace since April 2023 to manage rising workloads, reflecting stronger hiring activity across the services sector.

-

Outstanding business increased for a second consecutive month, indicating that demand continued to outpace firms’ capacity even as employment levels rose.

-

Input costs increased at a faster rate and reached the highest level in five months, with firms citing higher labor, electricity, and supply costs as the main drivers.

-

Output prices also increased more quickly, with the rate of charge inflation reaching the steepest level in six months and moving above the long-run average as firms passed higher costs onto clients.

-

Business confidence declined despite continued activity growth, indicating that firms remained cautious about the outlook even as demand conditions remained solid.

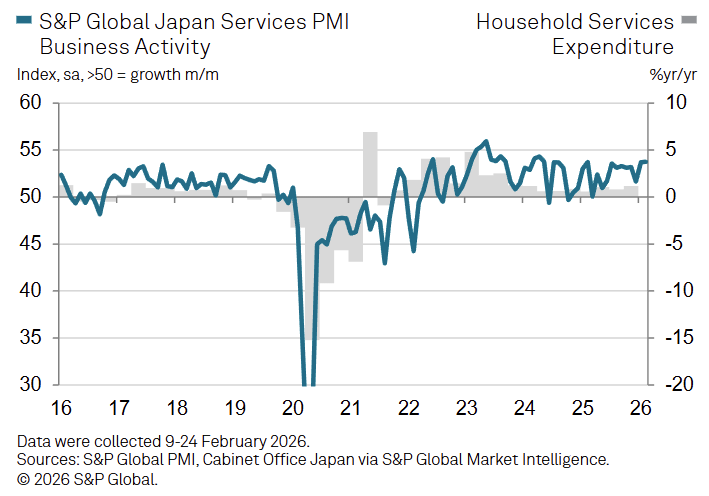

Japan

Japan’s Services PMI Business Activity Index edged up to 53.8 in February (+0.1 pts MoM from 53.7), marking the strongest services activity growth since May 2024 and extending the sector’s expansion streak to eleven consecutive months.

-

Services activity increased across all five monitored sub-industries, with Finance & Insurance recording the strongest gains and supporting the overall expansion in the sector.

-

New orders rose at the fastest pace since April 2024, reflecting stronger demand conditions and new client wins that lifted sales across service providers.

-

The increase in new business was driven largely by domestic demand, while new work from abroad rose only marginally, indicating limited contribution from international markets.

-

Staffing levels continued to increase but at a slower pace, with job creation easing to a three-month low as firms faced labor shortages, staff resignations, and difficulties filling vacancies.

-

Outstanding business increased at the fastest rate since June 2023, as stronger demand combined with slower hiring contributed to rising backlogs of work.

-

Input costs rose at a sharper and historically elevated pace, with firms reporting stronger cost pressures across the private sector.

-

Selling prices increased at the fastest rate since April 2014 as service providers passed higher costs on to customers, marking the steepest price increases in nearly twelve years.

-

The Composite PMI Output Index rose to 53.9 in February (Jan: 53.1), indicating the fastest expansion in Japan’s private sector activity in 33 months as both services and manufacturing output strengthened.

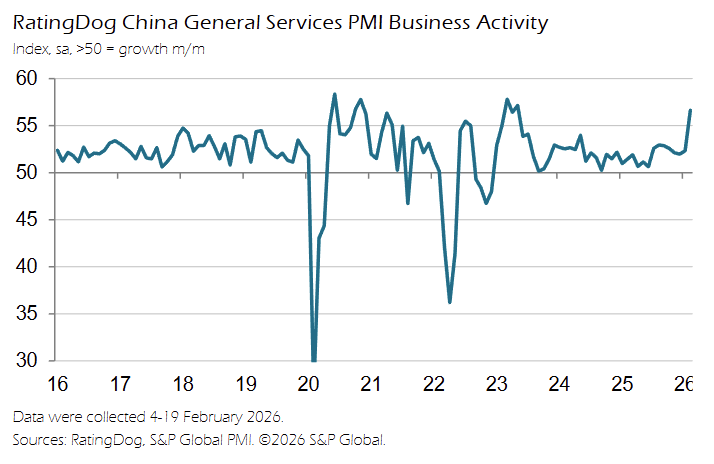

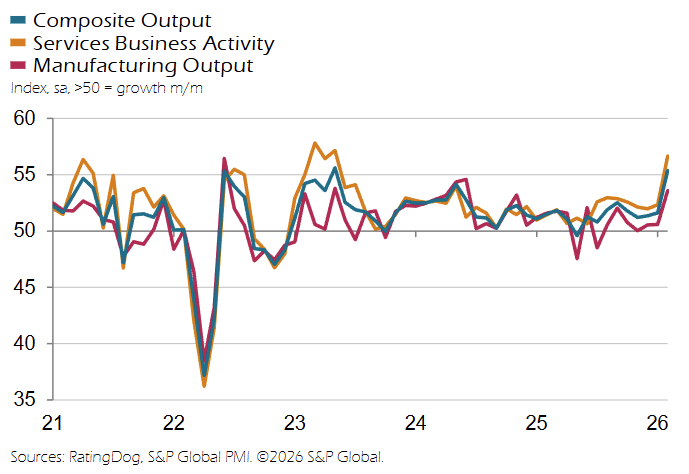

China

China’s Services PMI Business Activity Index rose to 56.7 in February (+4.4 pts MoM from 52.3), marking the strongest services activity growth in 33 months as stronger domestic and overseas demand lifted new business inflows.

-

Services activity expanded at 56.7 in February (Jan: 52.3), extending the current growth streak that began in January 2023 and representing the fastest expansion since May 2023.

-

Incoming new business increased at the joint-fastest pace since May 2024, driven by successful promotional efforts, rising client enquiries, and stronger overall demand conditions.

-

New export business also increased at the quickest pace in a year, reflecting improved overseas demand and stronger tourism-related activity.

-

Backlogs of work continued to accumulate as higher new business inflows lifted outstanding workloads, although the rate of backlog growth remained marginal and broadly similar to the previous two months.

-

Employment declined in February after a slight increase in January, as firms reduced staffing levels primarily for cost control amid rising operating expenses and limited capacity pressure.

-

Input costs increased at a faster rate than in January due to higher wage and energy expenses, indicating intensifying cost pressures across the services sector.

-

Selling prices increased for the first time in three months and rose at the fastest pace in 21 months as firms passed higher costs onto clients during a period of strengthening demand.

-

The Composite PMI Output Index rose to 55.4 in February (Jan: 51.6), signaling the fastest expansion in China’s private sector activity since May 2023 as both manufacturing and services output strengthened.

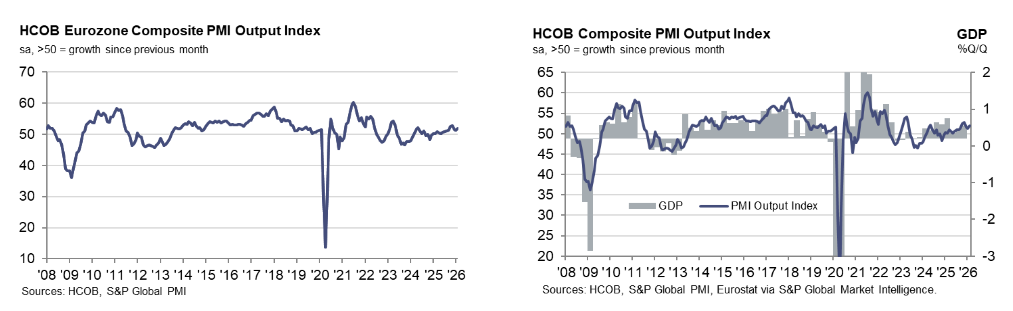

Euro Area

The HCOB Eurozone Composite PMI Output Index rose to 51.9 in February (+0.6 pts MoM from 51.3), a three-month high that signaled a slightly faster expansion in private sector activity as demand for goods and services improved.

-

The Composite PMI increased to 51.9 (Jan: 51.3), marking the quickest growth in three months and extending the eurozone’s current private sector expansion to 14 consecutive months.

-

Services activity strengthened modestly as the Services PMI Business Activity Index rose to 51.9 (Jan: 51.6), a two-month high, although the pace of expansion remained slightly below the survey’s long-run average.

-

New orders increased at a modest but faster pace in February, extending the current sequence of rising sales to seven months, with growth driven primarily by domestic demand.

-

New export business declined marginally again, indicating that external demand remained weak even as domestic order books improved.

-

Backlogs of work continued to decline, though only marginally and at the slowest rate since October, suggesting spare capacity persisted even as output expanded.

-

Employment levels were broadly unchanged across the eurozone private sector, marking another month with virtually no job creation despite continued growth in business activity.

-

Input costs rose at the fastest rate since April 2023, indicating intensifying cost pressures across the private sector as operating expenses accelerated for a fourth consecutive month.

-

Output price inflation eased slightly from January but remained the second-steepest in a year, while business confidence improved to its highest level since May 2024, reflecting stronger expectations for activity in the coming year.

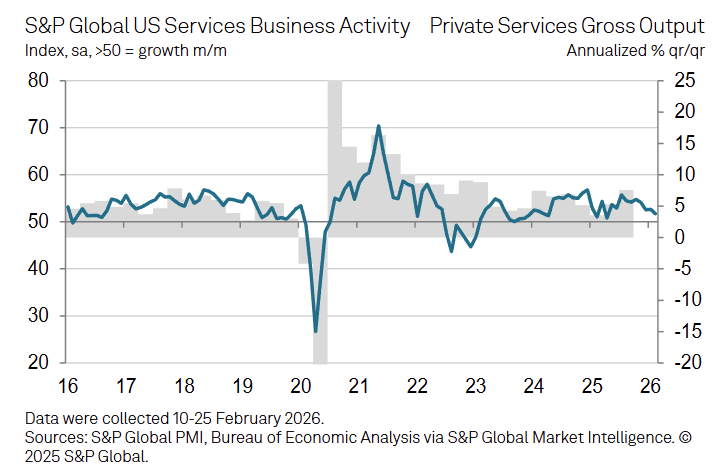

US

The S&P Global U.S. Services PMI Business Activity Index fell to 51.7 in February (-1.0 pts MoM from 52.7), signaling the slowest services sector expansion in ten months amid weaker demand and adverse weather effects.

-

Services activity slowed to 51.7 in February (Jan: 52.7) but remained above the 50 expansion threshold, extending the sector’s current growth streak to thirty-seven consecutive months.

-

New business increased for the twenty-second straight month, though the pace of growth cooled from January as adverse weather and uncertainty around tariffs and government policies constrained demand.

-

Export demand weakened further, with new export business declining marginally and extending the current contraction in international orders to three consecutive months.

-

Outstanding business increased at a steeper pace as activity growth lagged behind new orders, marking a continued accumulation of backlogs that has now persisted for one year.

-

Employment rose for a second successive month, but hiring remained fractional as firms primarily filled existing vacancies while broader hiring activity was limited by cost-cutting measures.

-

Input costs rose sharply in February, driven largely by higher labor-related expenses and tariff-related cost pressures reported by survey participants.

-

Selling prices increased at a faster pace during the month as service providers passed higher operating costs through to customers.

-

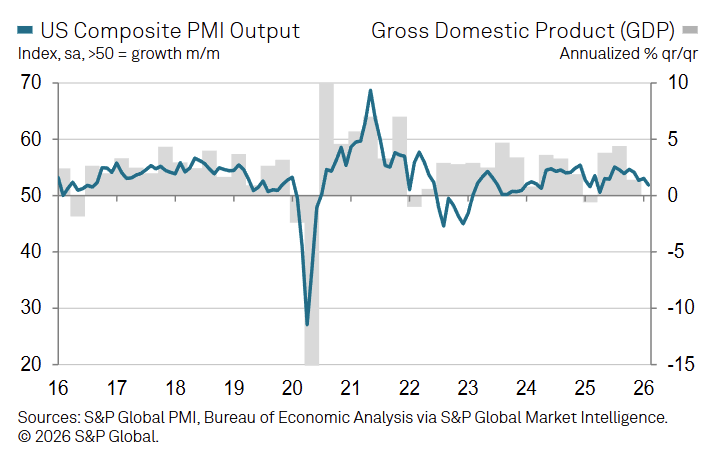

The S&P Global U.S. Composite PMI Output Index fell to 51.9 in February (Jan: 53.0), indicating slower overall private sector growth as both manufacturing and services output expansions moderated.