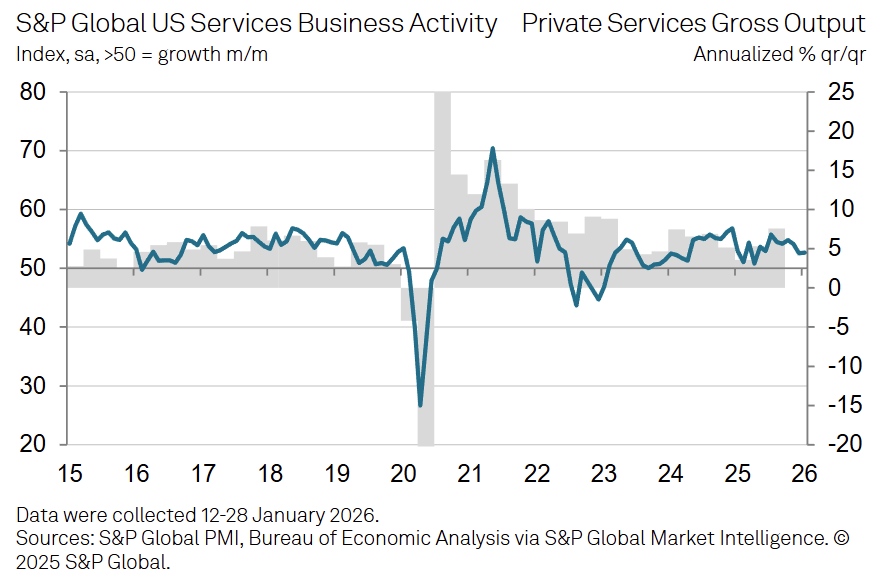

S&P Global US Services PMI: January 2026

The S&P Global US Services PMI edged up to 52.7 in January (from 52.5 in December), extending the expansion streak to exactly three years, though growth remained below typical 2025 levels.

-

New business inflows strengthened at the start of 2026, supported by new client wins and improved domestic demand, even as low consumer confidence and uncertainty limited overall gains.

-

New export business fell sharply to the weakest level since November 2022, reflecting a steep reduction in foreign demand linked to tariffs and an uncertain trading environment.

-

Backlogs of work increased solidly for an eleventh consecutive month and at the fastest pace since July, indicating ongoing capacity pressures across service providers.

-

Employment rose marginally after December’s slight decline, showing modest hiring that remained weak relative to the long-term survey trend.

-

Input cost inflation remained elevated but eased to the slowest pace since October, driven by tariffs alongside higher payroll and supplier costs.

-

Output charges continued to rise but at a softer rate than in December, pointing to slower price increases amid competition despite still-high cost pressures.

-

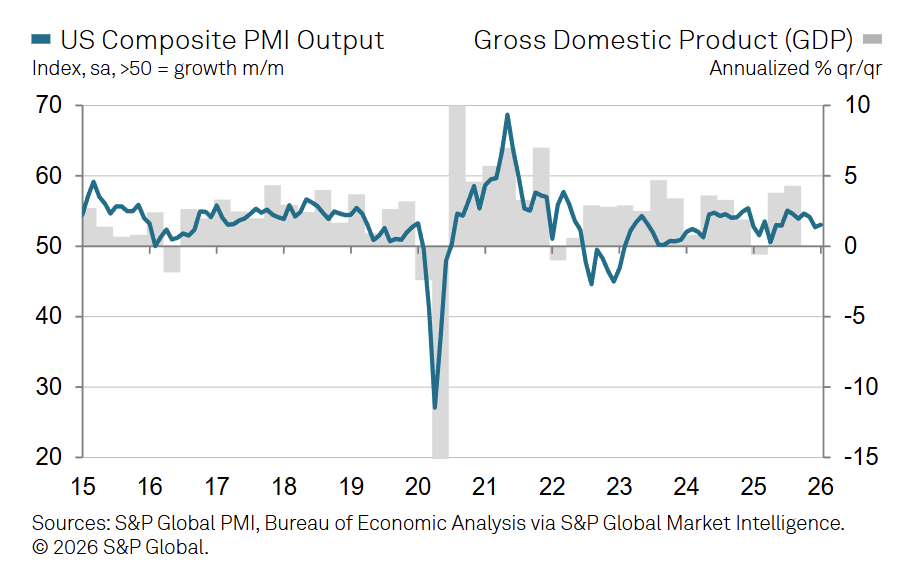

The US Composite PMI Output Index increased to 53.0 (Dec: 52.7), signaling a firmer overall expansion across both services and manufacturing.