S&P Global Services PMIs: January 2026

Global - 2/4/2026

Asia Pacific

- Australia - 2/4/2026

- Singapore (Composite only) - 2/4/2026

- Hong Kong (Composite only) - 2/4/2026

- Japan - 2/4/2026

- China - 2/4/2026

- India - 2/4/2026

- Russia - 2/4/2025

- Kazakhstan - 2/4/2026

Africa & Middle East

- Nigeria (Composite only) - 2/2/2026

- Qatar (Composite only) - 2/4/2026

- Kuwait (Composite only) - 2/4/2026

- Egypt (Composite only) - 2/4/2026

- UAE (Composite only) - 2/4/2026

- Uganda (Composite only) - 2/4/2026

- South Africa (Composite only) - 2/4/2026

- Lebanon (Composite only) - 2/4/2026

- Ghana (Composite only) - 2/4/2026

- Zambia (Composite only) - 2/4/2026

- Saudi Arabia (Composite only) - 2/4/2026

- Mozambique (Composite only) - 2/5/2026

- Kenya (Composite only) - 2/4/2026

Europe

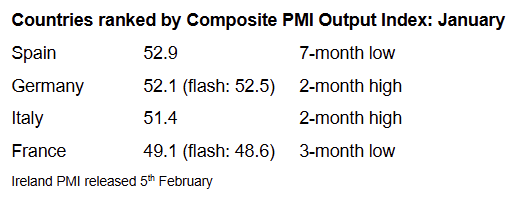

- Ireland - 2/5/2026

- Spain - 2/4/2026

- Italy - 2/4/2026

- France - 2/4/2026

- Germany - 2/4/2026

- Eurozone - 2/4/2026

- UK - 2/4/2026

North & South America

Key Results

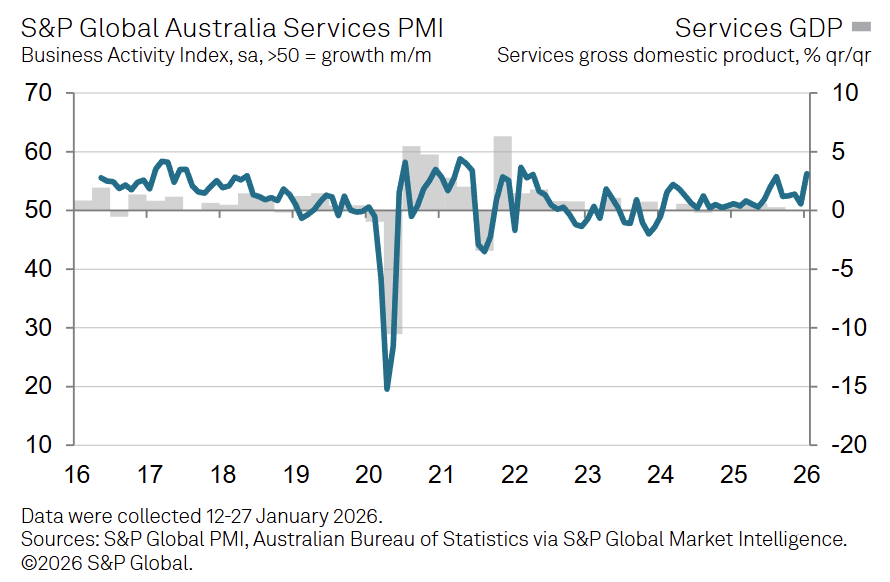

Australia

Australia’s Services PMI rose +5.2 pts MoM to 56.3 in January, the highest level since February 2022, extending the expansion streak to two consecutive years.

-

New business increased at the fastest pace since April 2022 for a third straight month, supported by stronger domestic demand and improved overseas orders.

-

Employment growth accelerated to its strongest rate since September, as firms added staff to manage higher workloads and rising outstanding work.

-

Backlogs of work increased again despite higher staffing levels, indicating labour constraints alongside stronger demand conditions.

-

Input costs continued to rise but inflation eased to the lowest level in 14 months, reflecting softer cost pressures than in December.

-

Output price inflation also slowed to a two-month low, pointing to reduced pass-through of costs to customers.

-

Business confidence declined to its lowest level since October 2024, despite stronger activity, reflecting concerns about the economic outlook and competition.

-

The Composite Output Index climbed to 55.7 (Dec: 51.0), the strongest expansion in 45 months, showing broad-based private sector growth driven by both services and manufacturing.

Japan

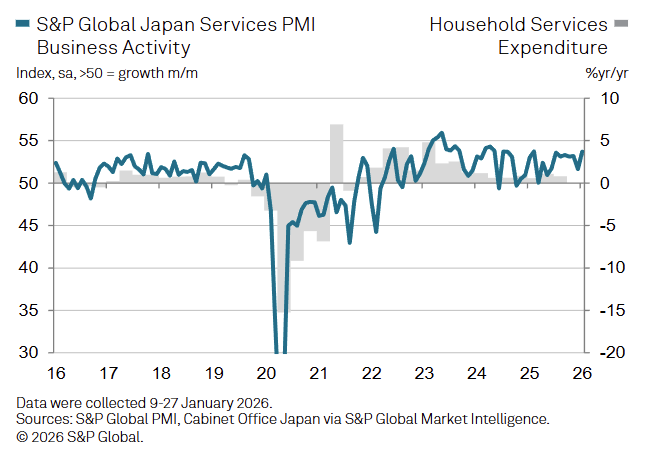

Japan’s Services PMI jumped to 53.7 in January, up from 51.6 in December, the strongest expansion in 11 months, indicating a solid acceleration in service sector output.

-

Business activity increased for a tenth consecutive month, showing a sustained run of monthly growth across Japanese services firms.

-

New business expanded at the fastest pace in four months, supported by marketing efforts, new client wins, and a more pronounced improvement in foreign demand.

-

Backlogs of work rose at the quickest rate since September, reflecting stronger inflows of new orders and rising pressure on existing capacity.

-

Employment continued to increase solidly, as firms added staff to manage higher workloads, extending the recent trend of job creation in services.

-

Input cost inflation eased to the softest pace in nearly two years, pointing to a cooling in expense pressures despite still-elevated costs.

-

Selling price inflation accelerated to a seven-month high, suggesting firms were increasingly passing higher costs through to customers.

-

Business sentiment remained positive but slipped to the lowest level since July, with concerns cited around global conditions, labour shortages, and tourism trends.

-

The Composite PMI increased to 53.1 in January, up from 51.1 in December, such that overall business activity expanded at the fastest rate since May 2023.

China

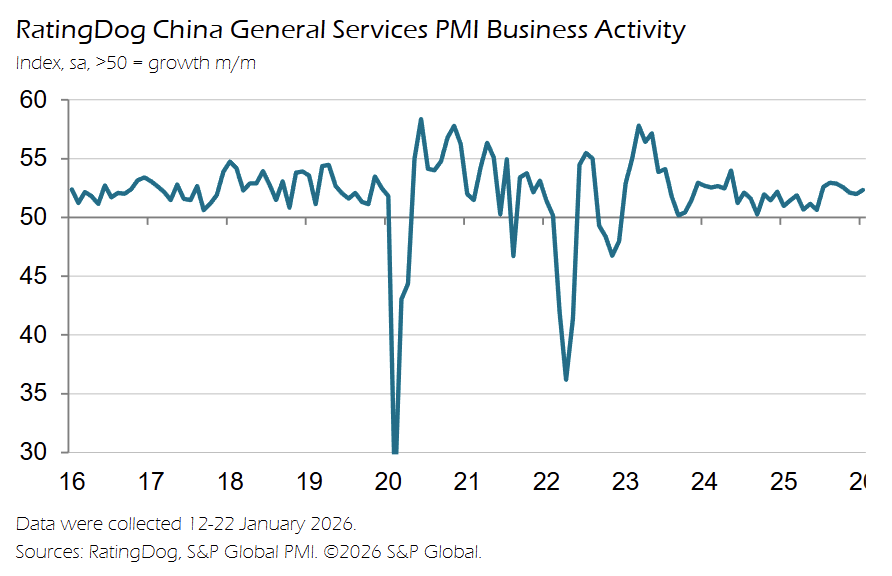

China’s General Services PMI increased to 52.3 in January, up from 52.0 in December, marking the fastest rise in services activity in three months and extending the expansion streak to just over three years.

-

New business growth accelerated for the first time in three months, supported by promotional activity, stronger client interest, and a renewed expansion in new export orders.

-

New export business returned to expansion after contracting in December, indicating a marginal recovery in external demand for Chinese services.

-

Employment rose for the first time in six months, representing only the fourth month of job growth over the past year as firms responded to stronger new work inflows.

-

Outstanding business continued to accumulate at a marginal pace, as increased labor capacity helped prevent a sharper build-up despite faster new order growth.

-

Input costs increased for an eleventh consecutive month but eased to a five-month low in inflation pace, pointing to softer cost pressures early in the year.

-

Output charges were broadly stable in January, showing little change in selling prices even as input costs continued to rise.

-

The Composite Output Index climbed to 51.6 (Dec: 51.3), reflecting a modest acceleration in overall business activity across both manufacturing and services, alongside a first rise in composite output prices in 14 months.

Euro Area

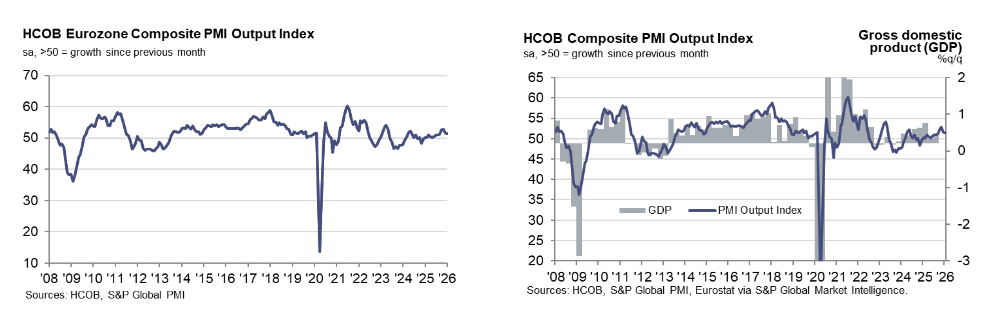

The HCOB Eurozone Composite PMI Output Index fell -0.2 pts MoM to 51.3 in January, a four month low, indicating continued expansion but at the weakest pace since September as services growth softened.

-

The Services PMI Business Activity Index declined to 51.6 (Dec: 52.4), also a four month low, pointing to more modest growth in services output early in the year.

-

New business across the eurozone barely rose in January, with services new orders increasing at the weakest pace since August, reflecting near-flat demand conditions.

-

Backlogs of work decreased at the fastest rate in eight months, showing firms cleared outstanding orders more quickly as sales momentum slowed.

-

Private sector employment virtually stagnated, as manufacturing job losses offset a mild increase in services hiring after three months of overall expansion.

-

Input cost inflation accelerated for a third straight month to an 11 month high, indicating a renewed build-up in cost pressures across the eurozone economy.

-

Output charge inflation rose to the strongest rate in nearly a year, suggesting firms increased selling prices more aggressively alongside rising costs.

-

Business expectations improved to the strongest level since May 2024, even as confidence remained below the long-run average.

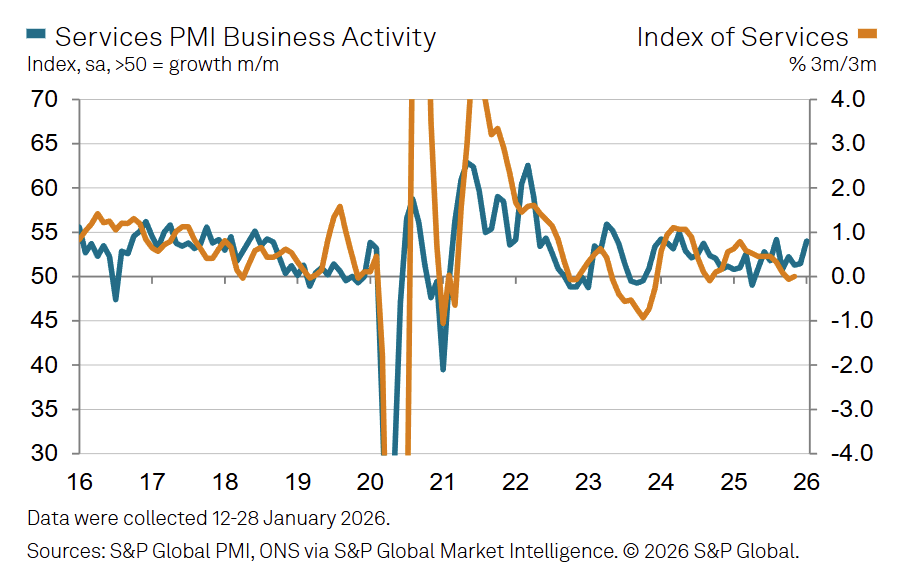

UK

The S&P Global UK Services PMI rose to 54.0 in January, up from 51.4 in December, the fastest expansion since August 2025 and a clear acceleration from the subdued pace seen in Q4 2025.

-

Total new business increased at a solid pace and reached a three-month high, indicating stronger order inflows even though growth remained below the long-run survey average.

-

New export orders rose modestly, posting the second fastest increase since October 2024, with firms citing stronger demand from European clients, particularly Ireland.

-

Employment continued to decline for a fourth consecutive month, extending the longest period of service sector job shedding in 16 years, with the pace of workforce reductions faster than in December.

-

Input cost inflation remained sharp but eased slightly from December’s seven-month high, driven primarily by higher payroll, technology, and raw material costs.

-

Output charges increased at the fastest rate since August 2025, showing firms raised prices more aggressively to offset rising business expenses.

-

Business optimism improved to the highest level since October 2024, with over half of firms expecting higher activity over the next 12 months despite ongoing concerns about costs and demand conditions.

-

The UK Composite PMI Output Index climbed to 53.7 (Dec: 51.4), the strongest reading since August 2024, reflecting faster growth across both services and manufacturing.

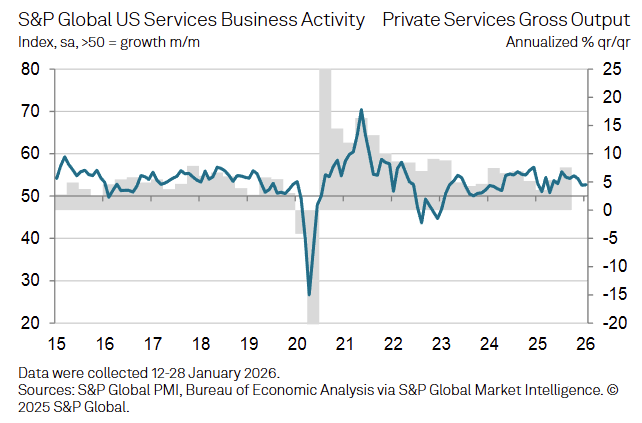

US

The S&P Global US Services PMI rose to 52.7 in January, up from 52.5 in December, extending the expansion streak to exactly three years, though growth remained below typical 2025 levels.

-

New business inflows strengthened at the start of 2026, supported by new client wins and improved domestic demand, even as low consumer confidence and uncertainty limited overall gains.

-

New export business fell sharply to the weakest level since November 2022, reflecting a steep reduction in foreign demand linked to tariffs and an uncertain trading environment.

-

Backlogs of work increased solidly for an eleventh consecutive month and at the fastest pace since July, indicating ongoing capacity pressures across service providers.

-

Employment rose marginally after December’s slight decline, showing modest hiring that remained weak relative to the long-term survey trend.

-

Input cost inflation remained elevated but eased to the slowest pace since October, driven by tariffs alongside higher payroll and supplier costs.

-

Output charges continued to rise but at a softer rate than in December, pointing to slower price increases amid competition despite still-high cost pressures.

-

The US Composite PMI Output Index increased to 53.0 (Dec: 52.7), signaling a firmer overall expansion across both services and manufacturing.