UMich Index of Consumer Sentiment: January 2026 (Final)

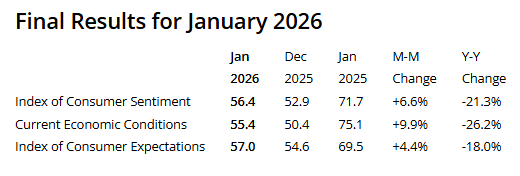

The University of Michigan’s Index of Consumer Sentiment rose to 56.4 in January 2026 (+6.6% MoM; -21.3% YoY), revised up from the preliminary estimate of 54.0.

-

The Current Economic Conditions Index increased to 55.4 (+9.9% MoM; -26.2% YoY), indicating a broad-based monthly improvement in assessments of present conditions despite large YoY deterioration.

-

The Index of Consumer Expectations rose to 57.0 (+4.4% MoM; -18.0% YoY), pointing to slightly firmer forward-looking views even as expectations remain below year-ago levels.

-

Overall sentiment improved by about 3.5 points, with minor gains across all components, suggesting the monthly rise was not concentrated in one category.

-

The sentiment uptick was broad-based across income, education, age, and political affiliation, indicating widespread (though small) improvement across demographic groups.

-

Despite the MoM gains, sentiment remained more than 20% below a year ago, with consumers citing pressure on purchasing power from high prices and the prospect of weakening labor markets as ongoing headwinds.

-

Year-ahead inflation expectations fell to 4.0%, the lowest reading since January 2025 but still above the 3.3% level recorded then, implying near-term inflation concerns eased but remain elevated versus last year.

-

Long-run inflation expectations increased to 3.3% (from 3.2% in December), moving further above the 2024 range of 2.8% to 3.2% and remaining well above sub-2.8% levels seen in 2019 to 2020.

-

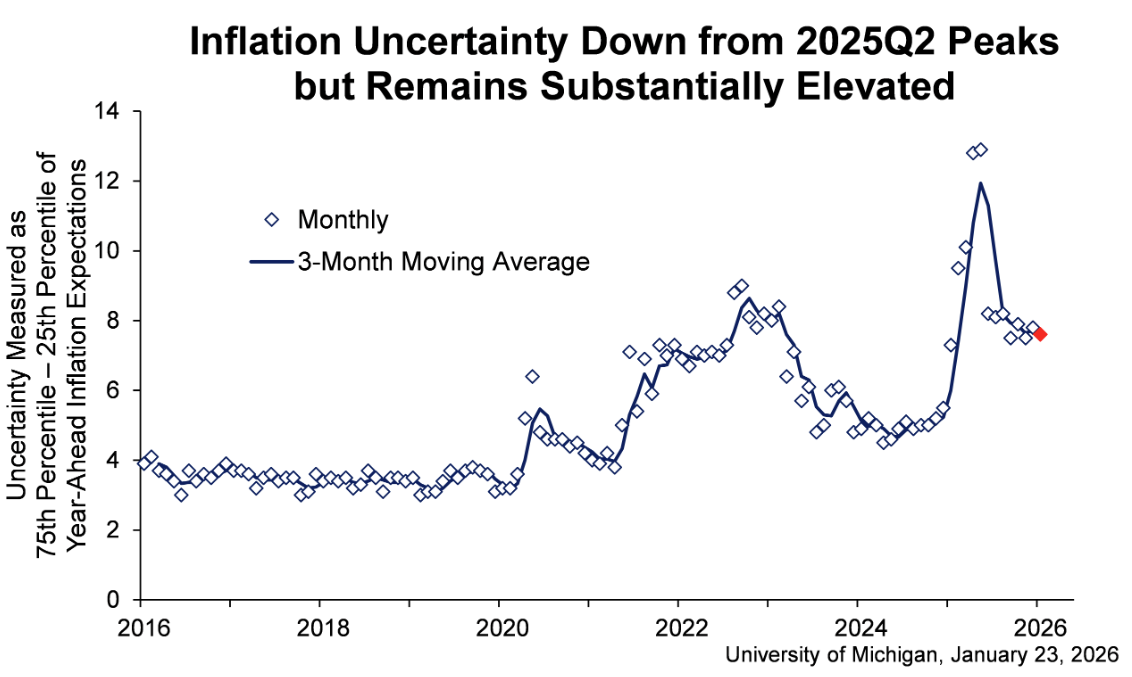

Short-run inflation uncertainty declined from mid-2025 but remained elevated and comparable to 2022 levels, indicating dispersion in inflation expectations is still relatively high.

January 2026 Update: Current versus Pre-Pandemic Long-Run Inflation Expectations