PBoC Financial Statistics: December 2025

China’s M2 money supply rose +8.5% YoY (vs +8.0% YoY expected) to ¥340.29T at end-December 2025, signaling steady broad liquidity growth alongside continued credit expansion.

-

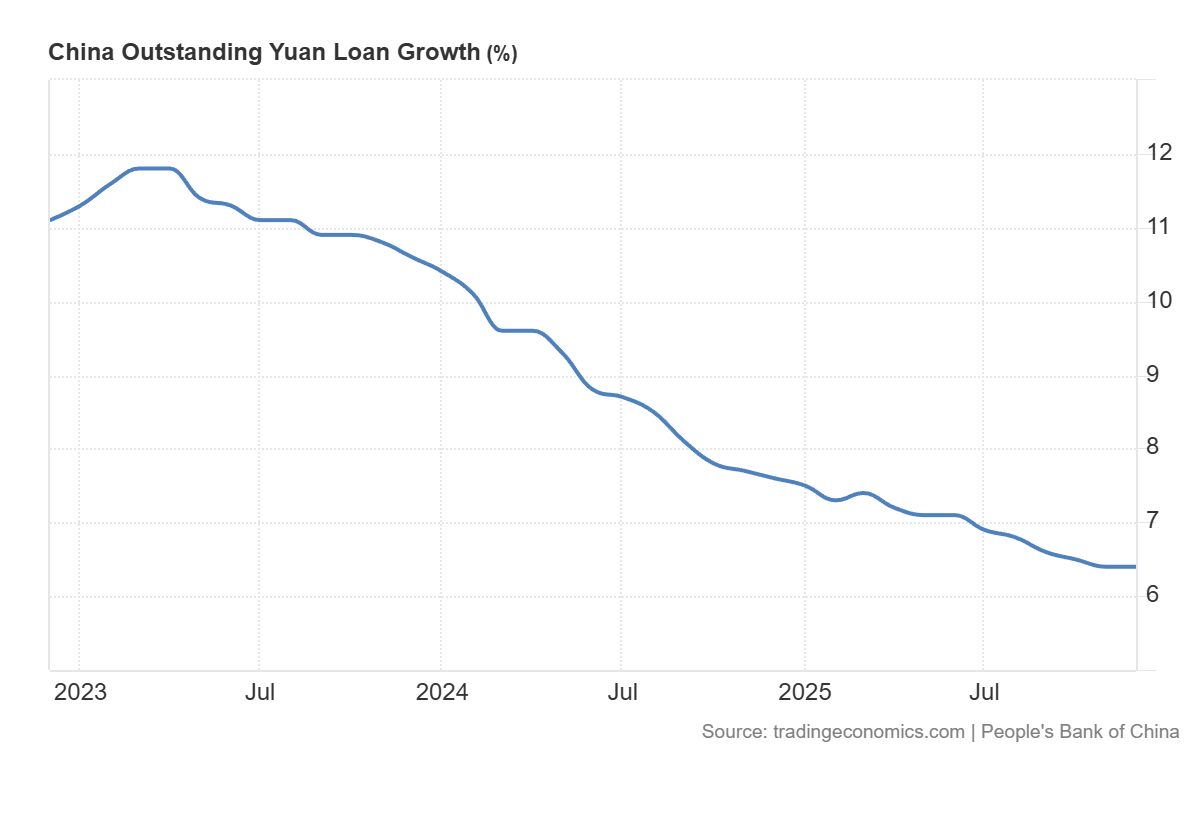

The stock of social financing (TSF) ended 2025 at ¥442.12T (+8.3% YoY), including RMB loans to the real economy of ¥268.4T (+6.3% YoY) and foreign currency loans of ¥1.05T (-18.0% YoY).

-

Government bonds outstanding reached ¥94.92T (+17.1% YoY) and accounted for 21.5% of TSF (+1.6pp YoY), while RMB loan share fell to 60.7% (-1.1pp YoY), indicating a shift in the composition of financing.

-

Corporate bonds outstanding were ¥34.24T (+6.0% YoY), while entrusted loans were ¥11.35T (+1.3% YoY), trust loans were ¥4.67T (+8.6% YoY), and undiscounted bank acceptances were ¥2.15T (-0.3% YoY), showing mixed growth across non loan channels.

-

The cumulative increase in TSF in 2025 was ¥35.6T, up ¥3.34T from the prior year; net government bond financing was ¥13.84T (+¥2.54T YoY) while RMB loans to the real economy rose ¥15.91T (-¥1.13T YoY).

-

Broad money (M2) rose +8.5% YoY to ¥340.29T, while M1 rose +3.8% YoY to ¥115.51T and M0 rose +10.2% YoY to ¥14.13T, with net cash injection of ¥1.31T over the year.

-

RMB deposits increased ¥26.41T in 2025 (households +¥14.64T, non financial enterprises +¥2.31T, fiscal deposits +¥0.658T, non bank financial institutions +¥6.41T), and foreign currency deposits rose to US$1.07T (+25% YoY).

-

RMB loans increased ¥16.27T in 2025, led by enterprise lending (+¥15.47T), while household loans rose only +¥0.442T as short term household loans fell -¥0.835T and medium to long term household loans rose +¥1.28T.

-

Interbank conditions eased in December, with the weighted average interbank lending rate at 1.36% (-0.06pp MoM, -0.21pp YoY) and pledged repo at 1.40% (-0.04pp MoM, -0.25pp YoY).