ECB Monetary Policy Decision: December 2025

The ECB held its three key policy rates unchanged in December 2025, while staff projections still point to inflation converging to 2% and growth strengthening on firmer domestic demand.

-

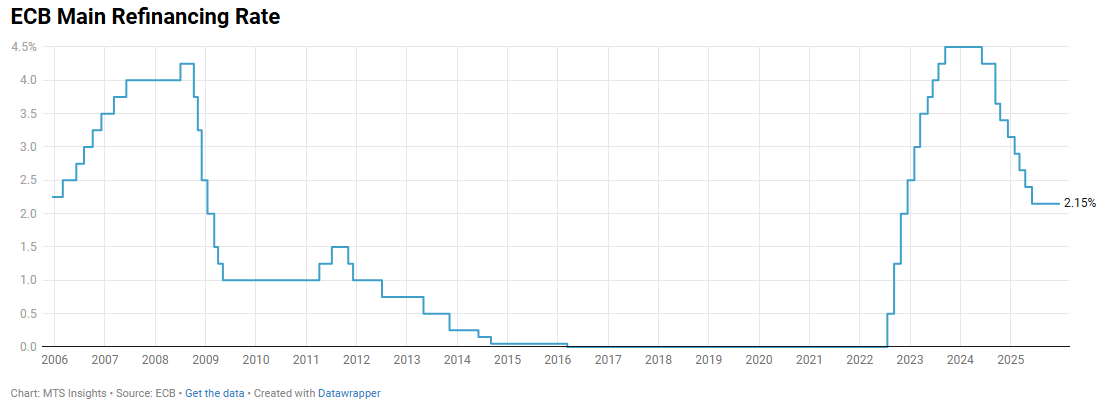

Policy rates: The deposit facility rate stayed at 2.00%, the main refinancing operations rate at 2.15%, and the marginal lending facility rate at 2.40%, maintaining an unchanged policy stance.

-

Inflation outlook (Dec projections): Headline inflation is projected to average 2.1% (2025), 1.9% (2026), 1.8% (2027), and 2.0% (2028), consistent with inflation stabilising around target over the medium term.

-

Underlying inflation (Dec projections): Inflation ex energy and food is projected at 2.4% (2025), 2.2% (2026), 1.9% (2027), and 2.0% (2028), with 2026 revised up because services inflation is expected to decline more slowly.

-

Growth outlook (Dec projections): Real GDP growth is projected at 1.4% (2025), 1.2% (2026), 1.4% (2027), and 1.4% (2028), revised higher versus September and attributed especially to stronger domestic demand.

-

Comparison with Sep projections: September projected headline inflation of 2.1% (2025), 1.7% (2026), and 1.9% (2027), and core inflation of 2.4% (2025), 1.9% (2026), and 1.8% (2027), implying a higher 2026 inflation track in December alongside modestly firmer growth.

-

Balance-sheet policy: APP and PEPP portfolios continue to decline in a “measured and predictable” way as maturing principal is no longer reinvested, reinforcing ongoing balance-sheet runoff.

-

Reaction function and backstops: The ECB reiterated a data-dependent, meeting-by-meeting approach with no pre-commitment to a rate path, and noted it can deploy tools including the Transmission Protection Instrument to address disorderly market dynamics that impair transmission.