S&P Global Services PMIs: November 2025

Global - 12/3/2025

Asia Pacific

- Australia - 12/2/2025

- Singapore (Composite only) – 12/3/2025

- Hong Kong (Composite only) – 12/3/2025

- Japan – 12/3/2025

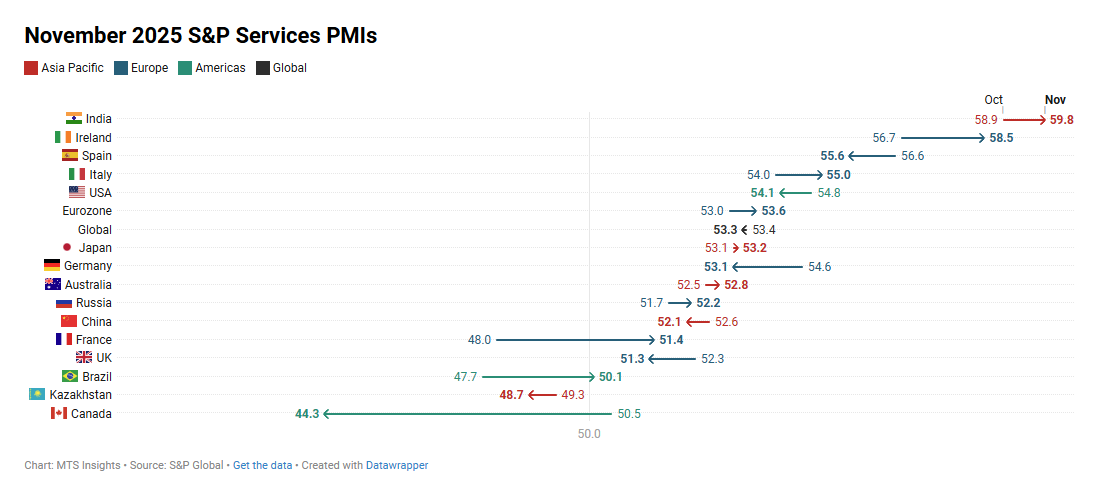

- China – 12/3/2025

- India – 12/3/2025

- Russia – 12/3/2025

- Kazakhstan – 12/3/2025

Africa & Middle East

- Nigeria (Composite only) - 12/1/2025

- Qatar (Composite only) - 12/3/2025

- Kuwait (Composite only) - 12/3/2025

- Egypt (Composite only) - 12/3/2025

- UAE (Composite only) - 12/5/2025

- Uganda (Composite only) – 12/3/2025

- South Africa (Composite only) – 12/3/2025

- Lebanon (Composite only) – 12/4/2025

- Ghana (Composite only) – 12/3/2025

- Zambia (Composite only) – 12/3/2025

- Saudi Arabia (Composite only) – 12/3/2025

- Mozambique (Composite only) – 12/3/2025

- Kenya (Composite only) – 12/3/2025

Europe

- Ireland – 12/3/2025

- Spain – 12/3/2025

- Italy – 12/3/2025

- France – 12/3/2025

- Germany – 12/3/2025

- Eurozone – 12/3/2025

- UK – 12/3/2025

North & South America

Key Results

Highlights and lowlights:

- Kenya's private sector growth was the strongest in over five years in November with its S&P Composite PMI at 55.0.

- Egypt's S&P Composite PMI increased to 51.1 in November, up from 49.2 in October and the highest reading since October 2020. S&P: "Historically, a PMI reading of 51.1 correlates with gross domestic product growing at an annual rate of more than 5%."

- The Italian service sector saw the strongest expansion in 2.5 years with an S&P Services PMI reading up 1.0 pt to 55.0 in November. Additionally, new business growth was the strongest in 19 months. A strong services reading led the S&P Composite PMI to rise 0.7 pts to 53.8, the strongest in over 2.5 years.

- France's S&P Services and Composite PMIs return to expansion territory for the first time in 15 months, rising 3.4 pts to 51.4 and 2.7 pts to 50.4, respectively.

China

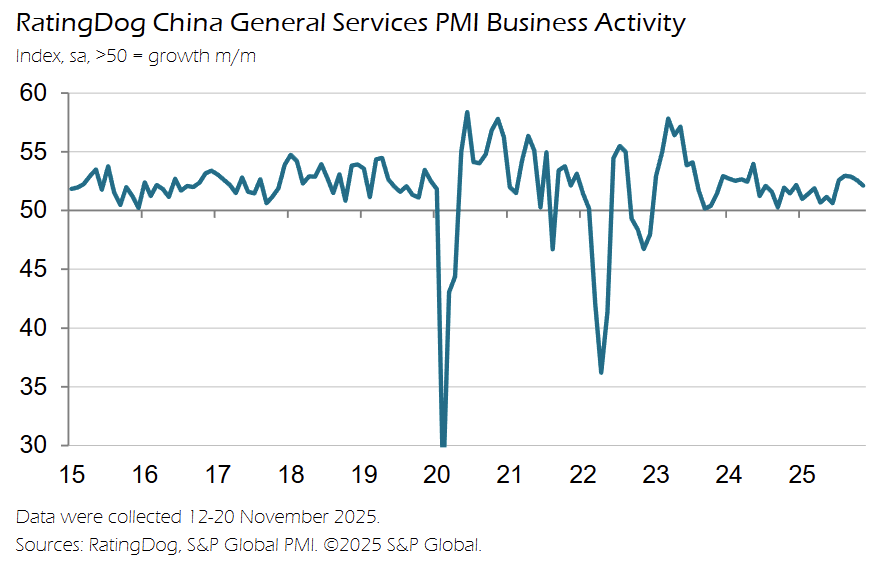

China’s RatingDog General Services Business Activity Index slipped to 52.1 in November (from 52.6 in October), marking the softest expansion in five months but still indicating ongoing growth in services activity.

-

New business rose at a slower pace, though growth remained solid, supported by increased client enquiries and renewed strength in new export orders after a mild decline in October.

-

Employment contracted again as firms cited non-replacement of leavers and cost-driven redundancies, contributing to a further rise in outstanding work, which accumulated at the fastest rate in three months.

-

Input prices increased for the ninth consecutive month, driven by higher materials, office supplies, and energy costs; providers raised output charges only fractionally to ease cost pressures.

-

Business confidence stayed positive but fell to one of the lowest levels on record, even as firms expressed hopes for better market conditions and expansion plans in the year ahead.

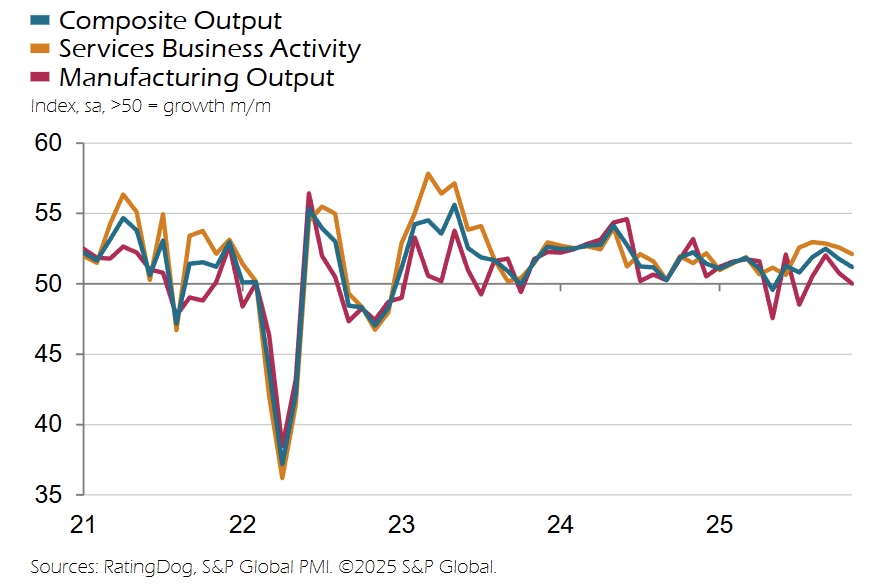

The Composite Output Index eased to 51.2 (from 51.8), showing a sixth straight month of growth but at a four-month low as manufacturing output stagnated and services growth moderated.

-

Total new business rose more slowly in the composite survey as well, despite another increase in new export orders, pointing to softer demand momentum late in the year.

-

Composite input costs increased for a fifth consecutive month, while output charges continued to fall, indicating persistent margin pressure across the broader private-sector economy.

Euro Area

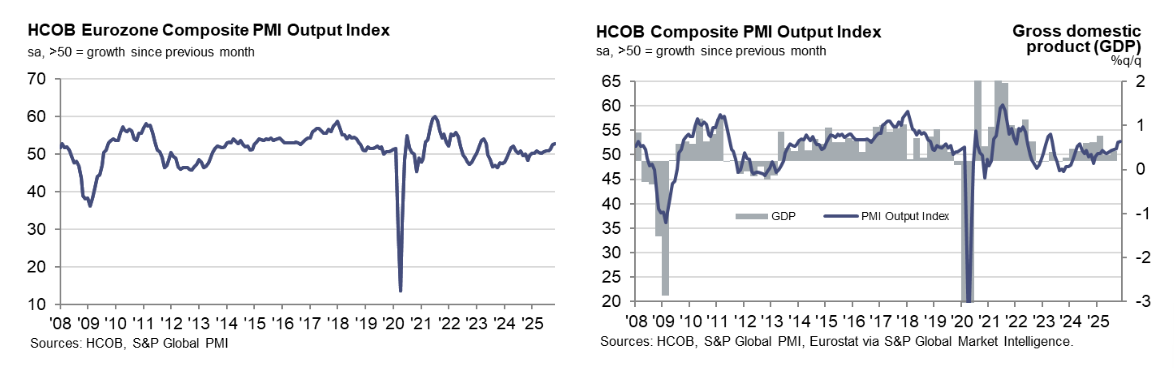

The HCOB Eurozone Composite PMI rose to 52.8 in November (from 52.5 in October), a 30-month high that reflects the fastest private sector expansion since mid-2023.

-

The Services PMI strengthened to 53.6 (from 53.0), also a 30-month high, showing the strongest services output growth since May 2023 and faster demand gains for a fourth straight month.

-

New business increased again at a solid rate, matching October’s two-and-a-half-year high, with all of the expansion concentrated in services as manufacturing orders fell slightly.

-

Backlogs of work declined after stabilizing in October, with manufacturers seeing a sharper depletion than services firms due to weaker factory demand.

-

Employment rose for the eighth time in nine months but at only a fractional pace; job creation was entirely driven by services while factory employment fell at the fastest rate since April.

-

Business confidence improved across both sectors, though expectations remained below their long-run average, indicating firms were cautiously optimistic.

-

Input price inflation picked up to an eight-month high amid rising manufacturing costs and faster services-sector expenses, while output charge inflation eased to a six-month low as firms made smaller price increases.

-

Country detail showed broad expansion: Ireland led at 55.8, Spain followed at 55.1, Italy reached a 31-month high at 53.8, Germany moderated to 52.4, and France posted its first expansion in 15 months at 50.4.

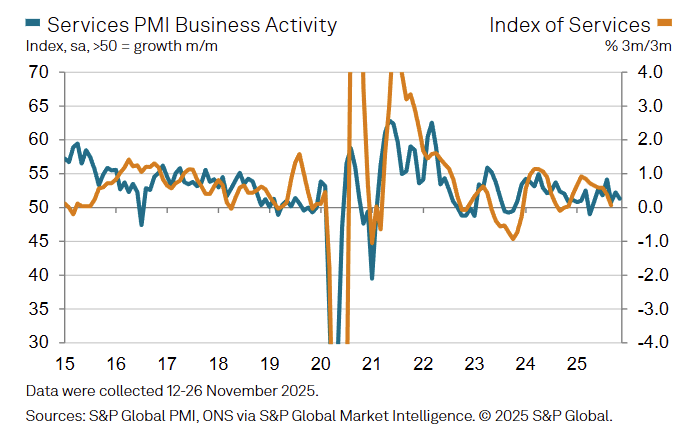

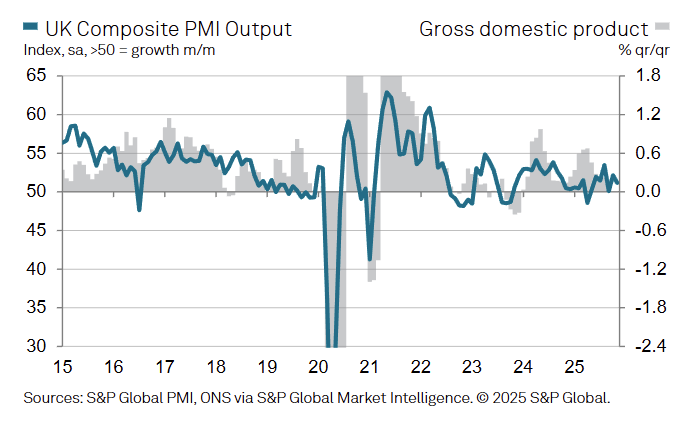

UK

The S&P Global UK Services PMI fell -1.0 pt to 51.3 in November (from 52.3 in October), indicating only marginal growth amid softer demand and rising cost pressures.

-

New business declined for the first time since July, with firms citing subdued domestic confidence and weaker foreign demand; export sales fell at the fastest rate since June due to global competition and geopolitical uncertainty.

-

Employment dropped at the quickest pace since February, extending the sequence of workforce reductions that began in October 2024 as firms cut staff amid lower workloads and elevated payroll costs.

-

Input cost inflation accelerated, driven by higher salaries, food and raw materials, energy, fuel, and insurance costs; around 29% of firms reported rising cost burdens versus 2% reporting declines.

-

Output charges rose only marginally, and prices charged inflation eased to the lowest reading since January 2021, reflecting intense price competition and weak sales pipelines.

-

Business confidence remained positive overall, with about half expecting higher activity over the next year, but optimism slipped below the post-pandemic trend due to policy uncertainty and concerns over the UK outlook.

The UK Composite PMI edged down to 51.2 (from 52.2), marking slower private sector expansion as modest service-sector growth and rising manufacturing output were offset by a fractional drop in total new work.

-

Backlogs continued to fall and contributed to reduced hiring, while firms noted delays in investment decisions ahead of the Budget as a headwind to business activity.

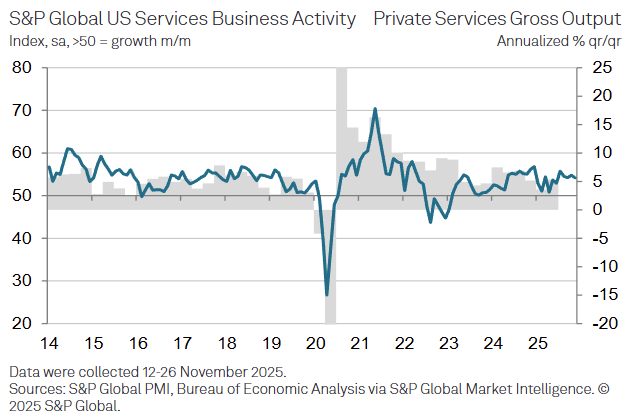

US

The S&P Global US Services PMI slipped -0.7 pts to 54.1 in November (from 54.8 in October), marking a five-month low but still signaling solid above-trend expansion.

-

New business rose at the strongest pace since December 2024, supported by more favorable market conditions, although export growth remained marginal and continued to lag amid international uncertainty.

-

Confidence improved noticeably, with firms citing the end of the government shutdown and expectations of higher federal spending, alongside plans for new products and increased advertising.

-

Employment increased at the fastest rate since June, extending the hiring streak that began in March; backlogs rose for a ninth month, indicating ongoing capacity pressure despite slower accumulation than over the summer.

-

Input cost inflation accelerated to a six-month high, driven by higher labor costs and tariff-related expenses, and remained above trend for a second month.

-

Output prices rose at a faster pace as firms attempted to pass through higher operating costs, though competitive pressures continued to limit pricing power.

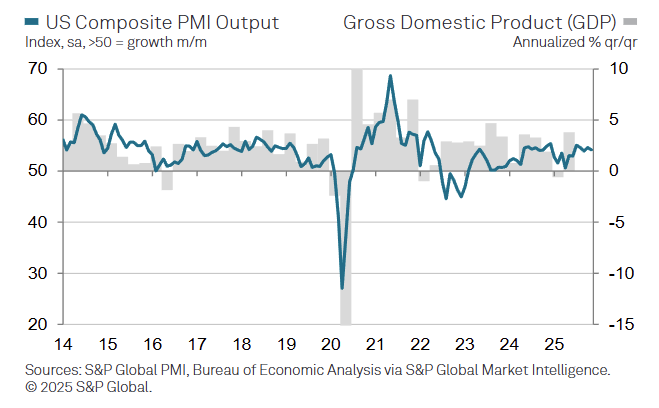

The US Composite PMI registered 54.2 (vs 54.6 in October), little changed overall and consistent with trend private-sector growth, with similar expansion across services and manufacturing.

-

Composite new business posted the strongest increase in three months, while input cost inflation reached a four-month high and output charges rose at a firmer rate.