PBoC Financial Statistics: October 2025

China’s broad M2 money supply rose +8.2% YoY (vs +8.1% YoY expected) in October 2025 to ¥335.13 trillion, down from +8.4% YoY in September, signaling stable overall liquidity conditions alongside firm growth in cash circulation and narrow money.

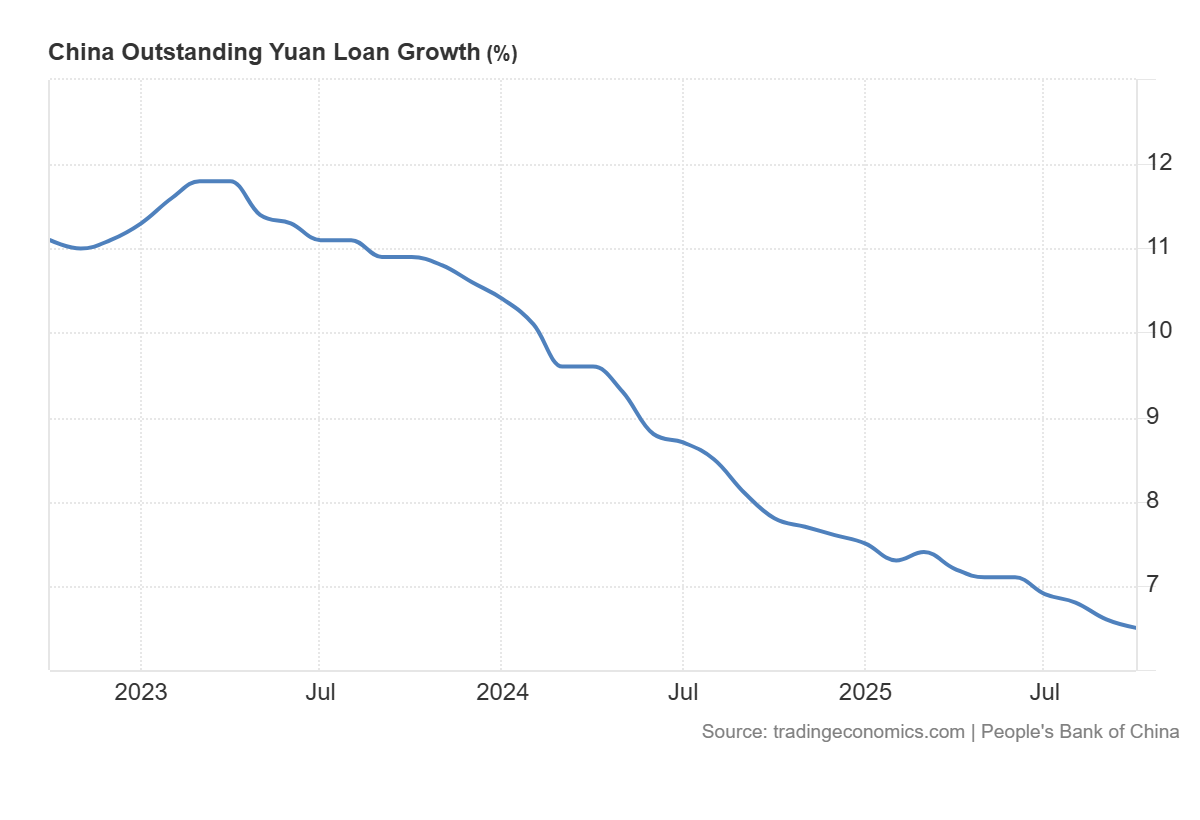

- The balance of RMB loans was ¥270.61 trillion yuan, up 6.5% YoY (vs 6.6% YoY expected), slightly slower than 6.6% YoY in September.

- The stock of social financing reached ¥437.72 trillion (+8.5% YoY), with RMB loans to the real economy up +6.3% YoY to ¥267.01 trillion and foreign currency loans down -16.9% YoY to ¥1.15 trillion.

- Government bond balances increased +19.2% YoY to ¥93.03 trillion, the strongest contributor to credit expansion, while corporate bonds rose +4.9% YoY to ¥33.68 trillion.

- Non-loan credit channels were mixed: trust loans grew +5.6% YoY and entrusted loans +1% YoY, while undiscounted bank acceptance bills declined -2.2% YoY.

- Cumulative social financing in Jan–Oct totaled ¥30.9 trillion, up ¥3.83 trillion YoY, driven largely by higher government bond net issuance (+¥3.72 trillion YoY) and stronger bill financing (+¥298.8 billion YoY).

- RMB deposits increased ¥23.32 trillion in the first ten months, led by households (+¥11.39 trillion) and non-bank financial institutions (+¥6.66 trillion), while foreign currency deposits rose +24.3% YoY to US$1.04 trillion.

- RMB loans expanded by ¥14.97 trillion in Jan–Oct, supported by enterprise lending (+¥13.79 trillion), whereas household short-term loans contracted -¥517 billion.

- Interbank funding costs continued to ease, with the weighted average lending rate at 1.39% and pledged repo at 1.40%, both down from September.

- Cross-border RMB settlements reached ¥1.41 trillion under the current account and ¥0.65 trillion in direct investment flows, indicating active trade and investment use of the currency.