S&P Global Services PMIs: October 2025

Global - 11/5/2025

Asia Pacific

- Australia - 11/4/2025

- Singapore (Composite only) – 11/5/2025

- Hong Kong (Composite only) – 10/6/2025

- Japan – 11/6/2025

- China – 11/5/2025

- India – 11/6/2025

- Russia – 11/6/2025

- Kazakhstan – 11/5/2025

Africa & Middle East

- Nigeria (Composite only) - 11/3/2025

- Qatar (Composite only) - 11/4/2025

- Kuwait (Composite only) - 11/4/2025

- Egypt (Composite only) - 11/4/2025

- UAE (Composite only) - 11/5/2025

- Uganda (Composite only) – 11/5/2025

- South Africa (Composite only) – 11/5/2025

- Lebanon (Composite only) – 11/5/2025

- Ghana (Composite only) – 11/5/2025

- Zambia (Composite only) – 11/5/2025

- Saudi Arabia (Composite only) – 11/4/2025

- Mozambique (Composite only) – 11/5/2025

- Kenya (Composite only) – 11/5/2025

Europe

- Ireland – 11/5/2025

- Spain – 11/5/2025

- Italy – 11/5/2025

- France – 11/5/2025

- Germany – 11/5/2025

- Eurozone – 11/5/2025

- UK – 11/5/2025

North & South America

Key Results

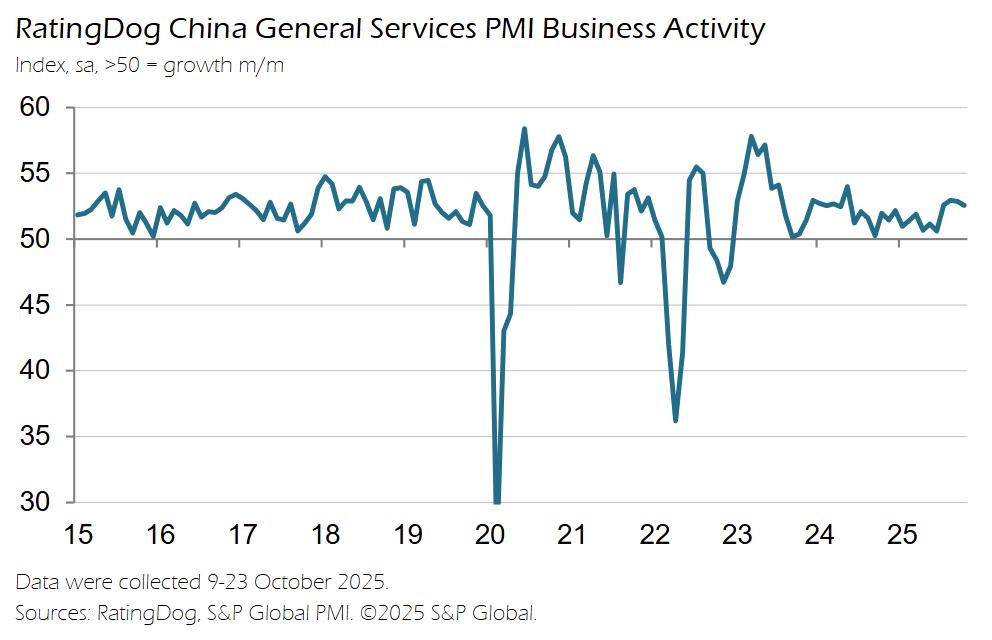

China

China’s RatingDog General Services Business Activity Index eased -0.3 pts to 52.6 in October 2025 (from 52.9 in September), marking continued but softer expansion; the Composite Output Index also slipped to 51.8 (from 52.5), indicating slower overall private sector growth.

-

New business growth accelerated, supported by new product launches and client wins, but new export orders fell modestly amid greater global trade uncertainty.

-

Backlogs of work declined for the first time in seven months, with firms citing better efficiency and reduced capacity pressure.

-

Employment contracted again as companies avoided replacing leavers and implemented selective redundancies driven by cost concerns.

-

Input prices rose for an eighth straight month and at the fastest pace in a year, reflecting higher raw material and wage costs.

-

Output charges fell fractionally, the second drop in three months, as firms absorbed costs and discounted to compete.

-

Business confidence remained positive but weakened slightly, with firms still expecting growth while noting tougher competition and trade risks.

-

Composite detail: total new business expanded at a slower rate, job shedding persisted for a third month, cost pressures intensified, and both goods and services producers lowered selling prices, pointing to margin pressure across the private economy.

Euro Area

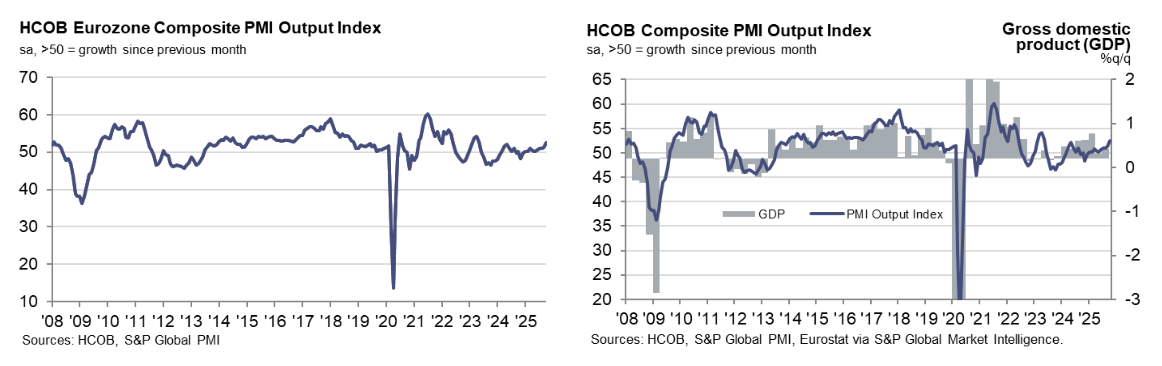

The HCOB Eurozone Composite PMI rose +1.3 pts to 52.5 in October 2025 (from 51.2 in September), marking the fastest private sector expansion since May 2023, supported by stronger domestic demand and rising employment.

-

Services PMI climbed to 53.0 (from 51.3), a 17-month high, signaling robust growth in the services sector and solid acceleration in new business volumes.

-

New business expanded at the sharpest pace in 2½ years, entirely driven by services as manufacturing orders were stagnant but improved from September’s decline.

-

Employment growth quickened to a 16-month high, driven by stronger hiring in services that offset faster factory job shedding.

-

Outstanding orders were unchanged, suggesting firms managed workloads effectively amid higher capacity.

-

Input cost inflation eased for the second month and fell below its long-term average, but output prices rose at the fastest rate in seven months as firms lifted charges more aggressively.

-

Business confidence stayed positive but softened slightly across both manufacturing and services, reflecting some caution despite stronger growth.

-

By country, Spain (56.0) led the euro area with the sharpest 10-month activity increase, followed by Germany (53.9), Ireland (53.7), and Italy (53.1), while France (47.7) fell further into contraction.

-

HCOB’s chief economist noted that the eurozone’s recovery is broadening, led by Germany’s sharp service-sector rebound and resilient growth across other economies, though France remains a drag amid political uncertainty.

UK

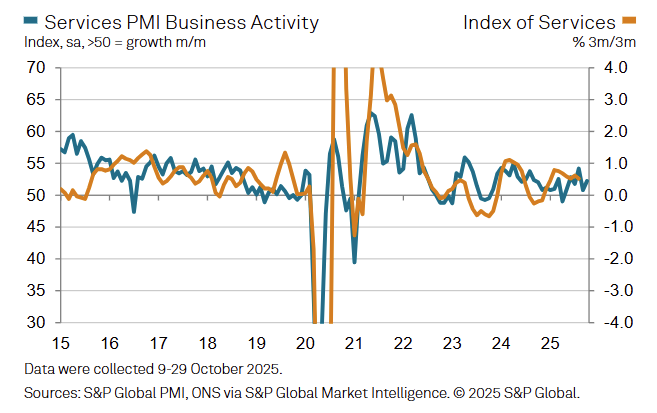

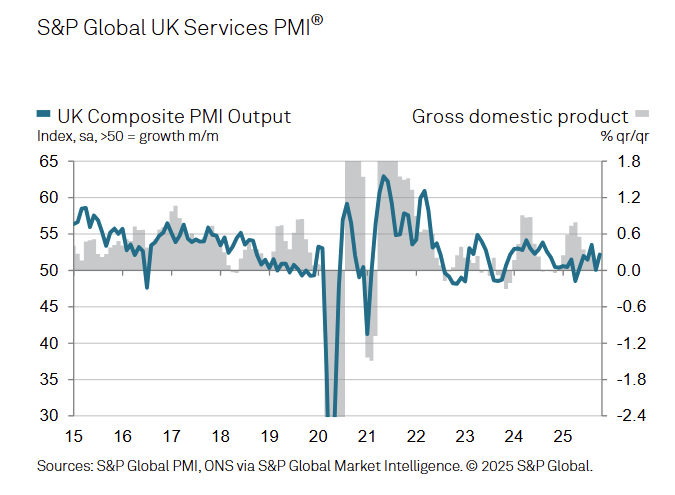

The S&P Global UK Services PMI rose +1.5 pts to 52.3 in October 2025 (from 50.8 in September), marking the strongest expansion in six months as domestic demand strengthened and business confidence improved to a 12-month high.

-

New business increased at the second-fastest pace since October 2024, driven by rising domestic orders, marketing efforts, and new product launches; however, export sales declined for a second month due to weak global demand.

-

Employment fell slightly, but the rate of decline was the slowest in a year, with firms noting better order books and some resumption of hiring amid cost controls.

-

Input cost inflation eased to its lowest level since November 2024, though wage, energy, and food costs remained elevated.

-

Output prices rose at the weakest pace since June, as firms limited price increases amid stronger competition and reduced cost pressure.

-

Business confidence reached its highest level since October 2024, supported by lower borrowing costs, investment in new technologies, and improved sales pipelines.

-

The Composite PMI climbed to 52.2 (from 50.1), confirming the sixth consecutive month of overall private-sector growth, with services leading and manufacturing output rising for the first time in a year.

-

S&P Global’s Tim Moore noted that October’s rebound reflected resilient domestic demand, slower job cuts, and easing inflation, though uncertainty around the broader UK outlook continued to weigh on sentiment.

US

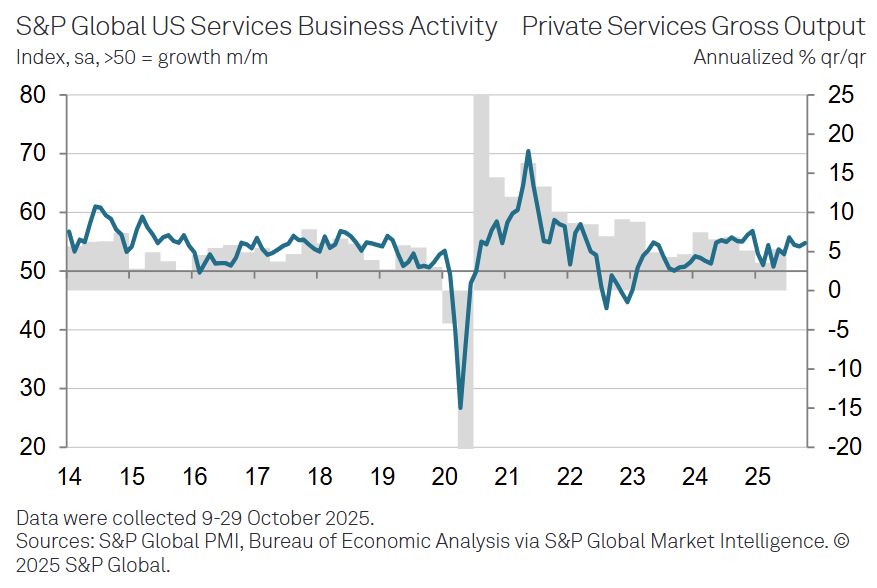

The S&P Global US Services PMI rose +0.6 pts to 54.8 in October 2025 (from 54.2 in September), marking the 33rd straight month of expansion and signaling solid momentum in service activity at the start of Q4.

-

New business increased at a slightly faster rate, supported by stronger client demand and inquiries, though new export orders declined marginally for the sixth time in seven months amid trade-related uncertainty.

-

Backlogs of work rose for an eighth month but only marginally, the slowest increase since March, suggesting firms managed workloads effectively amid rising activity.

-

Employment expanded for the eighth consecutive month, with hiring focused on sales and project support, though overall growth was modest due to cost controls and limited replacement of departing staff.

-

Input costs continued to rise sharply—driven by tariffs and labor expenses—but at the slowest pace in six months, easing overall cost pressure.

-

Selling price inflation moderated to the weakest since April, as firms absorbed cost increases amid competitive pricing and customer resistance to higher charges.

-

Business confidence fell to a six-month low, reflecting political and economic uncertainty, though firms noted that recent Fed rate cuts had improved sentiment slightly.

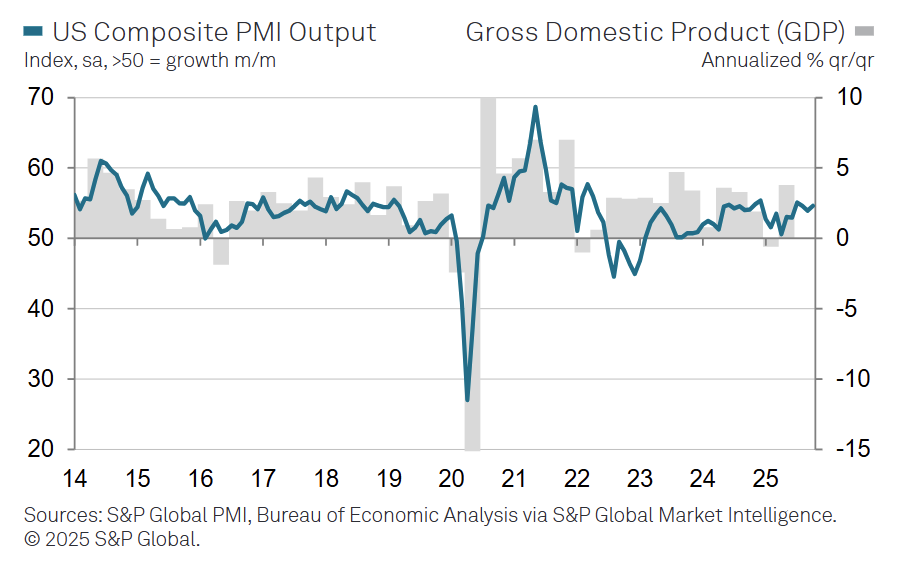

The S&P Global US Composite PMI rose +0.7 pts to 54.6 in October 2025 (from 53.9 in September), marking a modest acceleration in private sector growth driven by concurrent gains in manufacturing and services output.

-

New business expanded solidly, providing the main support to overall activity growth during the month.

-

Employment increased for a second month, though only modestly, as firms remained cautious amid weaker confidence in the outlook.

-

Business confidence fell to a six-month low, reflecting persistent uncertainty despite continued expansion in output and demand.

-

Input costs and selling prices both recorded their slowest increases since April, suggesting easing inflationary pressures across the private sector.

-

S&P Global’s Chris Williamson said the PMI data indicate that Q4 GDP growth is tracking near a 2.5% annualized rate, with financial and tech sectors leading expansion but profitability constrained by limited pricing power.