RBA Monetary Policy Decision: November 2025

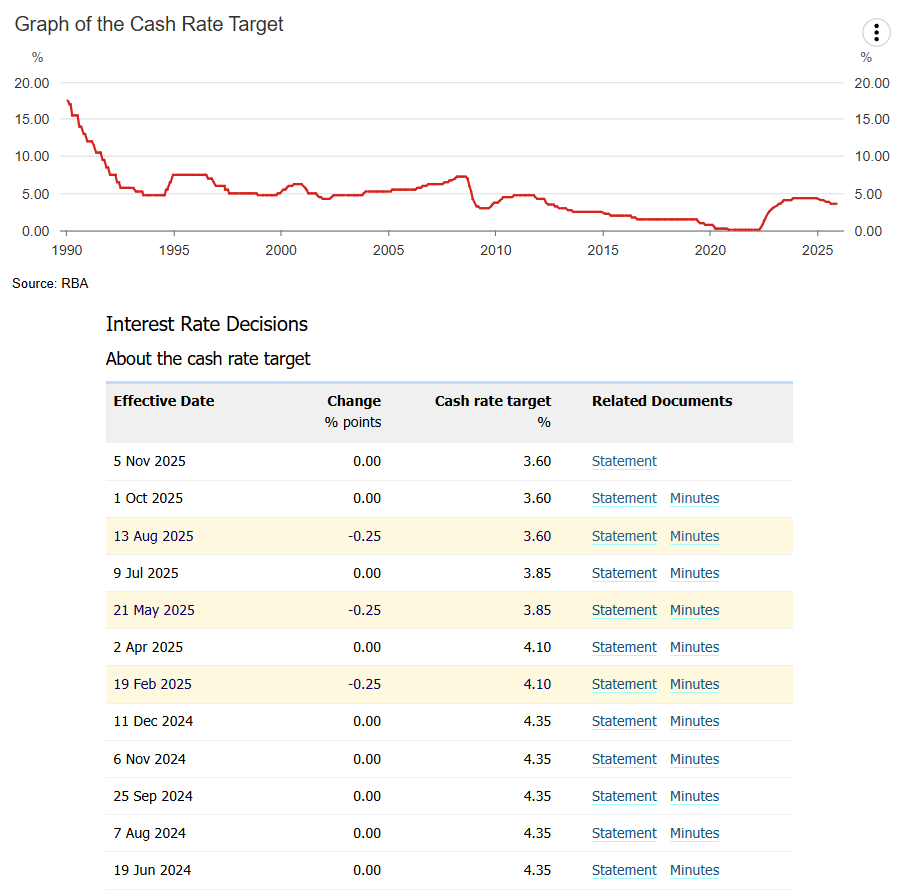

The Reserve Bank of Australia kept the cash rate unchanged at 3.60% in November 2025, citing stronger-than-expected inflation and ongoing tightness in the labour market, while acknowledging signs of continued recovery in private demand and housing activity.

-

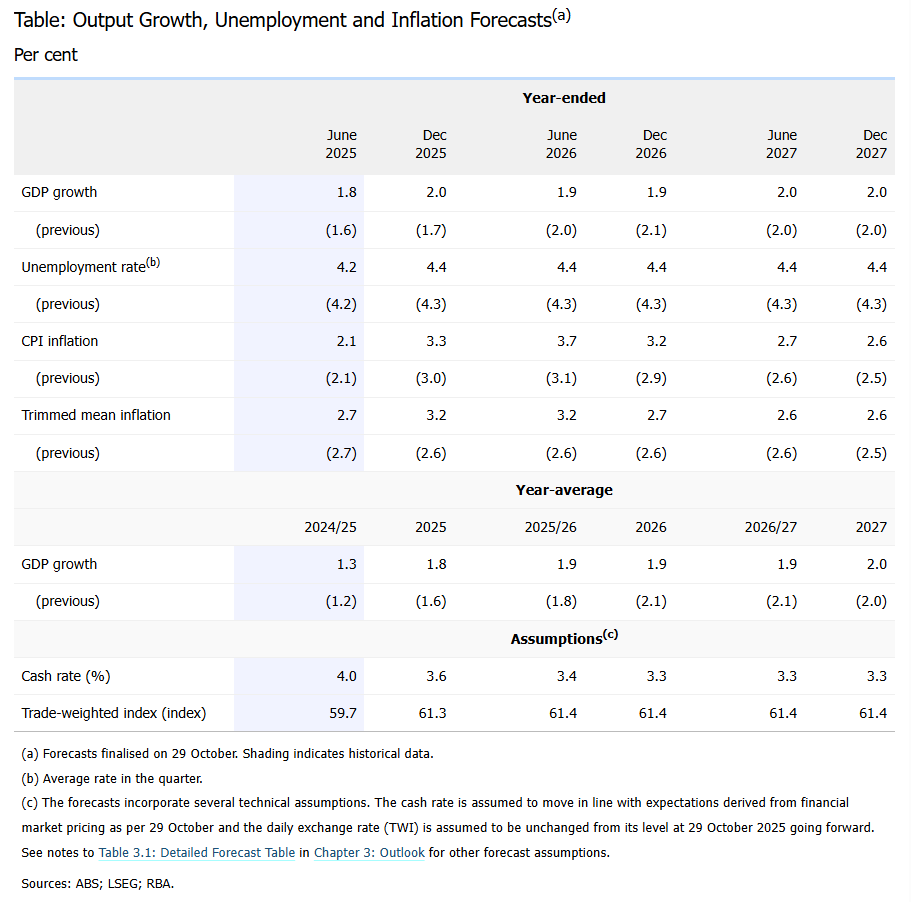

Trimmed mean inflation rose +1.0% QoQ and +3.0% YoY in Q3 (up from +2.7% YoY in Q2), exceeding expectations in the August Statement and suggesting more persistent inflation pressures than previously assessed.

-

Headline inflation climbed to +3.2% YoY, boosted by the end of electricity rebates, higher fuel costs, and rising housing construction prices.

-

The unemployment rate increased to 4.5% in September (from 4.3% in August), with employment growth slowing slightly more than anticipated, though indicators such as job vacancies and underutilization still point to residual labour market tightness.

-

Private demand continued to recover, supported by easier financial conditions and rising housing prices, with credit availability remaining strong for households and businesses.

-

GDP growth is expected to stabilize near potential over the forecast period, while capacity pressures are projected to remain slightly above the August outlook due to resilient demand and limited slack.

-

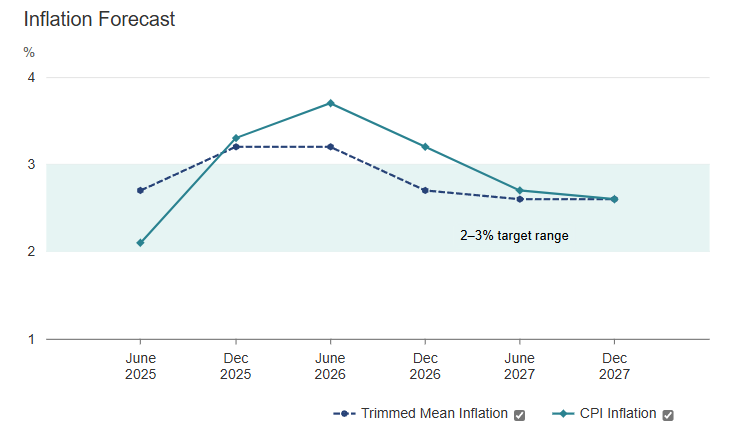

The RBA’s central forecast sees underlying inflation staying above the 2-3% target range through mid-2026 before easing to around 2.6% in 2027.

-

Global growth has been more resilient than expected, though downside risks persist from tariffs, geopolitical uncertainty, and potential shifts in global financial conditions.

-

The Board reaffirmed its commitment to price stability and full employment, noting that the recent easing in financial conditions and stronger inflation warranted a cautious approach to further rate adjustments.