PBoC Financial Statistics: September 2025

China’s broad M2 money supply rose +8.4% YoY (vs +8.5% YoY expected) to ¥335.38 trillion at the end of September 2025, down from +8.8% YoY in August, showing stable liquidity growth supported by household savings and robust fiscal financing.

- The total social financing stock increased +8.7% YoY to ¥437.08 trillion, with strong government bond growth (+20.2% YoY) offsetting weaker corporate lending (+4.5% YoY) and falling foreign currency loans (-18% YoY).

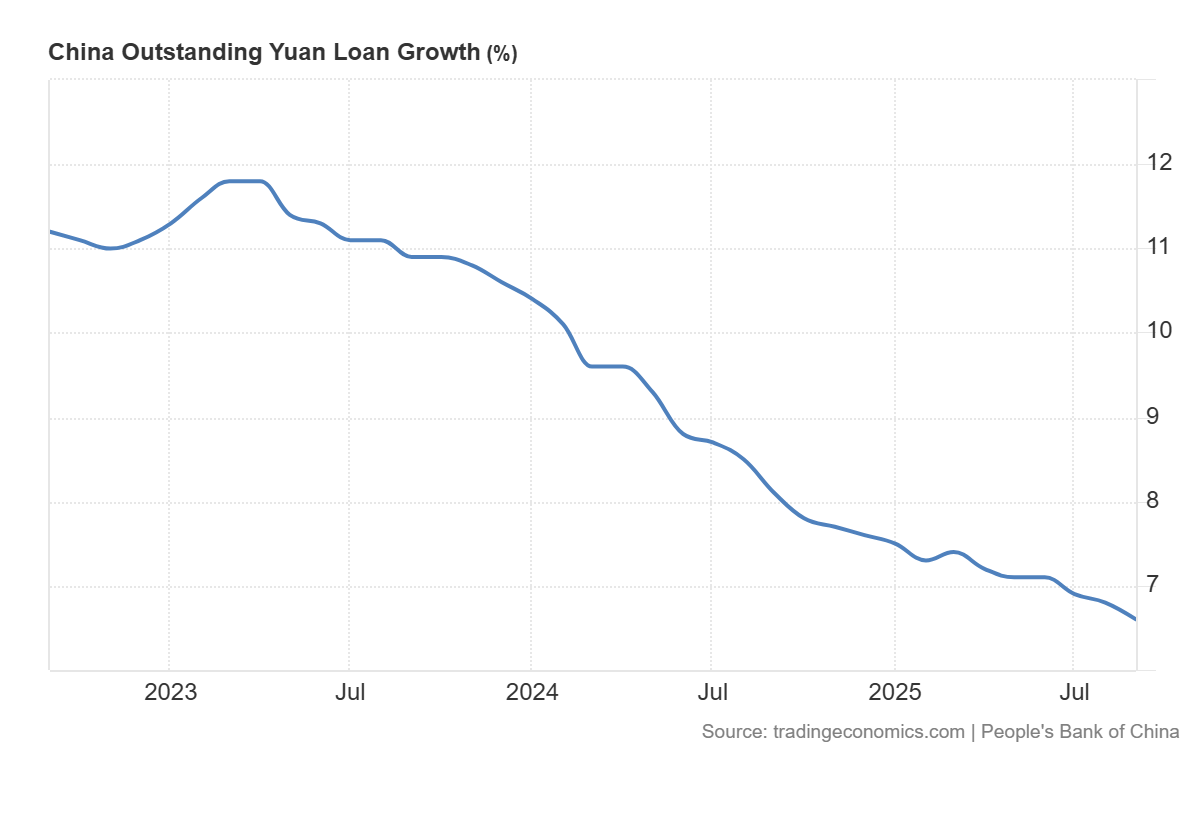

- Total loan growth was +6.6% YoY (vs +6.7% YoY expected) in September, down from +6.8% YoY in August, as the credit expansion continues to slowly decelerate.

- RMB loans to the real economy expanded +6.4% YoY to ¥267.03 trillion, while trust loans rose +5.7% YoY and undiscounted bank acceptance bills were up +4.4% YoY.

- RMB loans rose ¥14.75 trillion in Jan-Sep, with enterprise lending (+¥13.44 trillion) the main driver and short-term household loans contracting ¥230 billion.

- The cumulative increase in social financing during Jan-Sep reached ¥30.09 trillion, up ¥4.42 trillion YoY, driven mainly by government bond net issuance of ¥11.46 trillion (+¥4.28 trillion YoY).

- Narrow money (M1) grew +7.2% YoY, and cash in circulation (M0) rose +11.5% YoY; net cash injection totaled ¥761.9 billion in the first three quarters.

- RMB deposits increased ¥22.71 trillion, led by household deposits (+¥12.73 trillion) and non-bank financial institutions (+¥4.81 trillion); foreign currency deposits climbed +20% YoY to US$1.02 trillion.

- Interbank lending rates remained low: the weighted average stood at 1.45% in September and pledged repo at 1.46%, both down roughly 0.35 ppts YoY, indicating ample liquidity.

- Foreign exchange reserves stood at US$3.34 trillion at the end of September, while the RMB exchange rate was 7.1055 per US dollar.

- Cross-border RMB settlements totaled ¥19.10 trillion in Jan-Sep, including ¥13.06 trillion under current accounts and ¥6.04 trillion from direct investments.