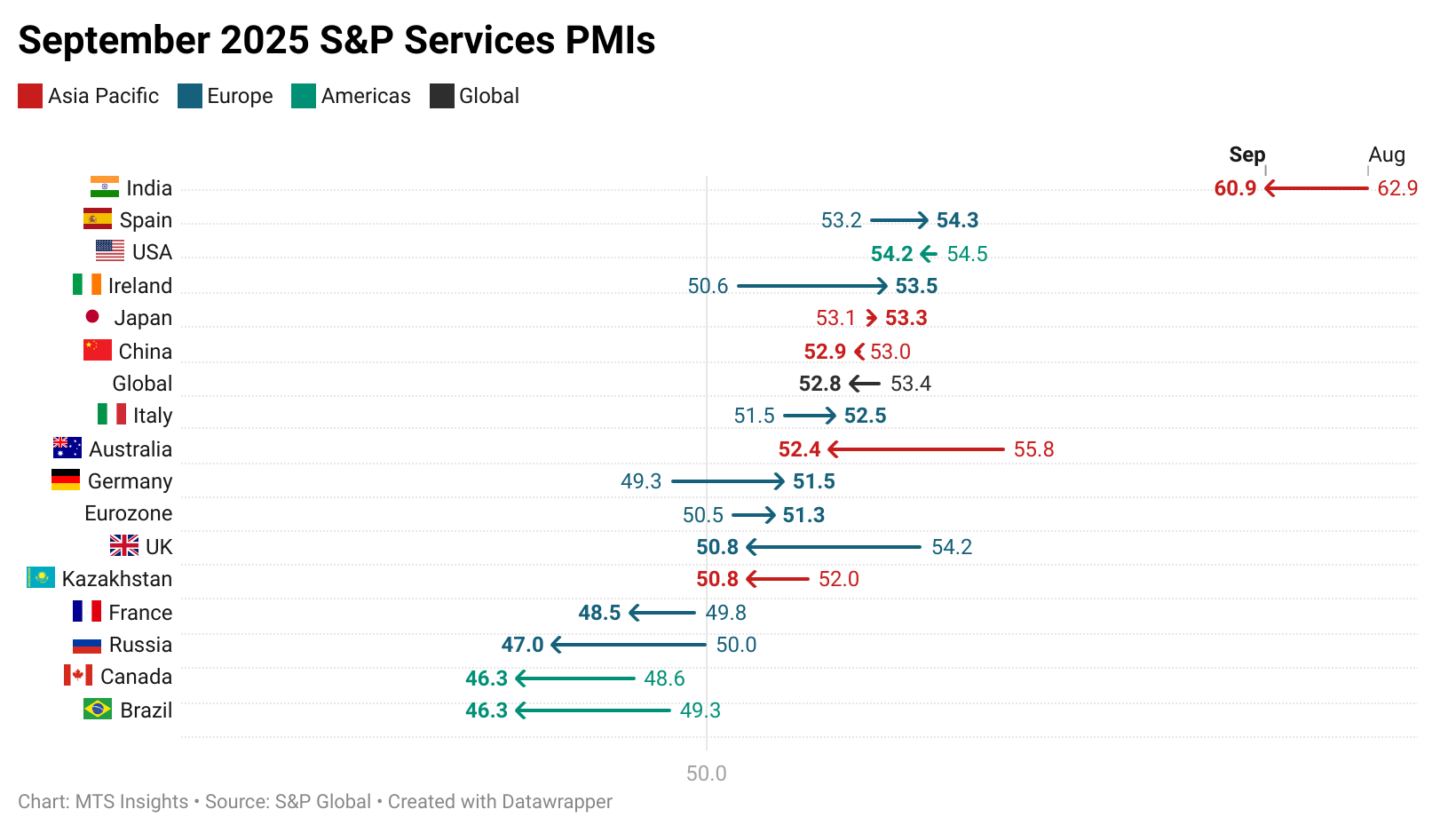

S&P Global Services PMIs: September 2025

Global - 10/3/2025

Asia Pacific

- Australia - 10/2/2025

- Singapore (Composite only) – 10/3/2025

- Hong Kong (Composite only) – 10/6/2025

- Japan – 10/3/2025

- China – 10/3/2025

- India – 10/6/2025

- Russia – 10/3/2025

- Kazakhstan – 10/3/2025

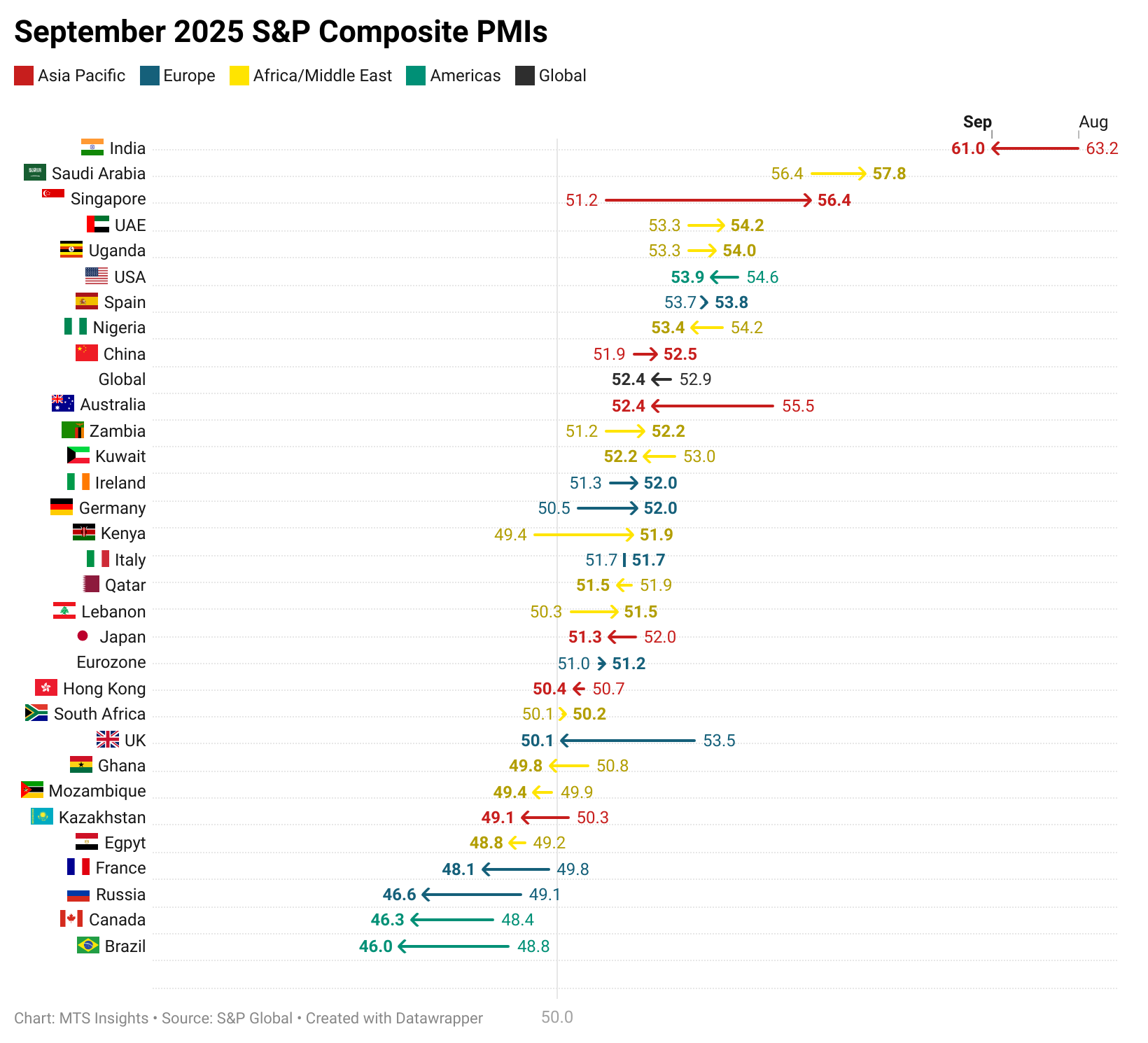

Africa & Middle East

- Nigeria (Composite only) - 10/1/2025

- Qatar (Composite only) - 10/6/2025

- Kuwait (Composite only) - 10/6/2025

- Egypt (Composite only) - 10/6/2025

- UAE (Composite only) - 10/3/2025

- Uganda (Composite only) – 10/3/2025

- South Africa (Composite only) – 10/3/2025

- Lebanon (Composite only) – 10/3/2025

- Ghana (Composite only) – 10/3/2025

- Zambia (Composite only) – 10/6/2025

- Saudi Arabia (Composite only) – 10/3/2025

- Mozambique (Composite only) – 10/3/2025

- Kenya (Composite only) – 10/3/2025

Europe

- Ireland – 10/3/2025

- Spain – 10/3/2025

- Italy – 10/3/2025

- France – 10/3/2025

- Germany – 10/3/2025

- Eurozone – 10/3/2025

- UK – 10/3/2025

North & South America

Key Results

Russia

The S&P Global Russia Services PMI fell to 47.0 in September (from 50.0 in August), marking the sharpest services contraction since December 2022 amid a steep decline in new orders.

-

Business activity decreased for the third time in four months, with subdued client demand and weaker purchasing power weighing on output.

-

New orders contracted at the fastest pace since December 2022, highlighting sustained weakness in sales volumes.

-

Despite falling demand, service firms raised employment at the quickest pace since January 2024, with some citing efforts to clear backlogs.

-

Backlogs of work fell for the first time in 11 months, with the rate of depletion the steepest since December 2022.

-

Input costs rose at the fastest rate in five months on higher supplier, wage, and utility expenses, though firms moderated selling price increases due to competitive pressures.

-

Business confidence improved from August but remained below the long-run trend, supported by hopes of greater economic stability and stronger customer numbers.

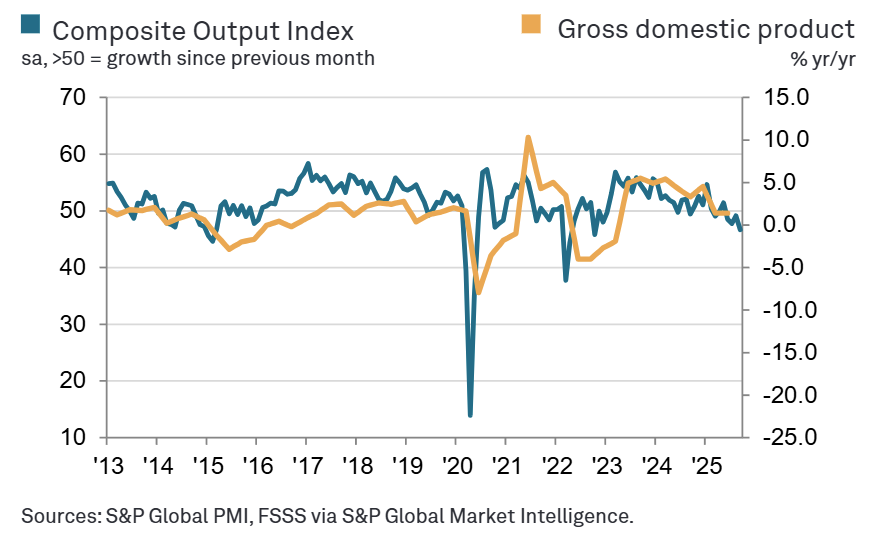

The Russia Composite PMI Output Index fell to 46.6 in September (from 49.1 in August), the steepest contraction in private sector activity since October 2022.

-

Sharper contractions in both manufacturing and services new orders drove the fastest fall in total private sector sales since May 2022.

-

Workforce numbers rose at the strongest pace since August 2024, as services hiring offset renewed declines in manufacturing jobs.

-

Backlogs of work shrank for the third month in a row, reflecting broad-based weakness in demand across sectors.

-

Input costs and output charges both increased at faster rates, pointing to rising cost pressures despite soft demand conditions.

-

Overall business confidence improved from August but remained below the historical average, signaling only cautious optimism.

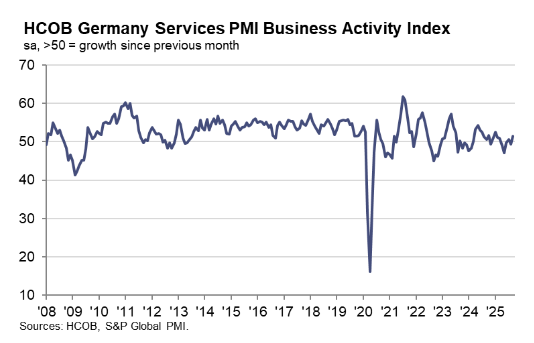

Germany

The HCOB Germany Services PMI rose to 51.5 in September (from 49.3 in August), its highest in eight months, signaling a modest rebound in activity despite fragile demand conditions.

-

Business activity expanded for the first time since July, supported by the completion of outstanding projects, though it remained below the long-run average of 52.7.

-

New business fell for the second month in a row, with firms citing customer budget cuts and weaker export sales; however, the pace of decline eased compared to August.

-

Backlogs of work continued to shrink, extending a depletion trend since May 2024.

-

Employment fell at the sharpest rate since June 2020, reflecting weak demand and limited pipeline work.

-

Input costs rose steeply, driven mainly by wage pressures, while output price inflation edged up to a four-month high and remained above the long-run trend.

-

Business confidence strengthened slightly to its highest level since May 2024, as firms expressed optimism about improving economic conditions.

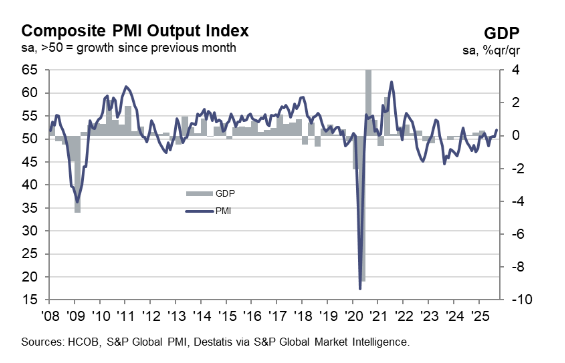

The Germany Composite PMI Output Index rose to 52.0 in September (from 50.5), the strongest expansion in 16 months, driven by gains in both manufacturing and services.

-

New work declined across both sectors, with manufacturing orders falling for the first time in four months and services orders contracting at a softer pace.

-

Employment fell in both sectors, producing the steepest overall workforce decline since November 2024, as capacity pressures eased further.

-

Backlogs of work dropped broadly, reinforcing signs of weak demand despite higher output levels.

-

Output price inflation accelerated to a four-month high, even as input cost growth slowed slightly, pointing to persistent cost pressures.

Eurozone

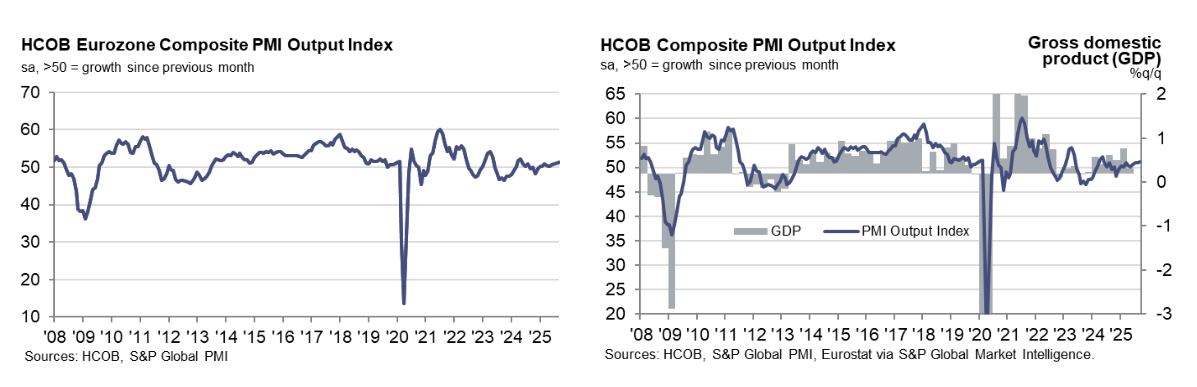

The HCOB Eurozone Composite PMI rose to 51.2 in September (from 51.0 in August), a 16-month high, signaling continued though muted private sector growth across the bloc.

-

The Eurozone Services PMI increased to 51.3 (from 50.5), its highest in eight months, marking a modest rebound in activity.

-

New business rose for the first time since May 2024, though the improvement was mild and driven by domestic demand, while new export orders continued to decline.

-

Backlogs of work fell for the 17th consecutive month, with the pace of depletion the quickest in three months, reflecting limited demand pressures.

-

Employment edged lower in September, marking the first overall workforce reduction since February, though the scale of job losses was marginal.

-

Input cost inflation eased to below the historical average, while output charges rose at the weakest pace since May, signaling softer price pressures.

-

Business confidence strengthened to an 11-month high in services and the second-highest overall since July 2024, supported by expectations of improved economic conditions.

-

Country detail: Spain led with a Composite PMI of 53.8, followed by Germany (52.0), Ireland (52.0), and Italy (51.7), while France remained an outlier at 48.1, signaling faster contraction.

USA

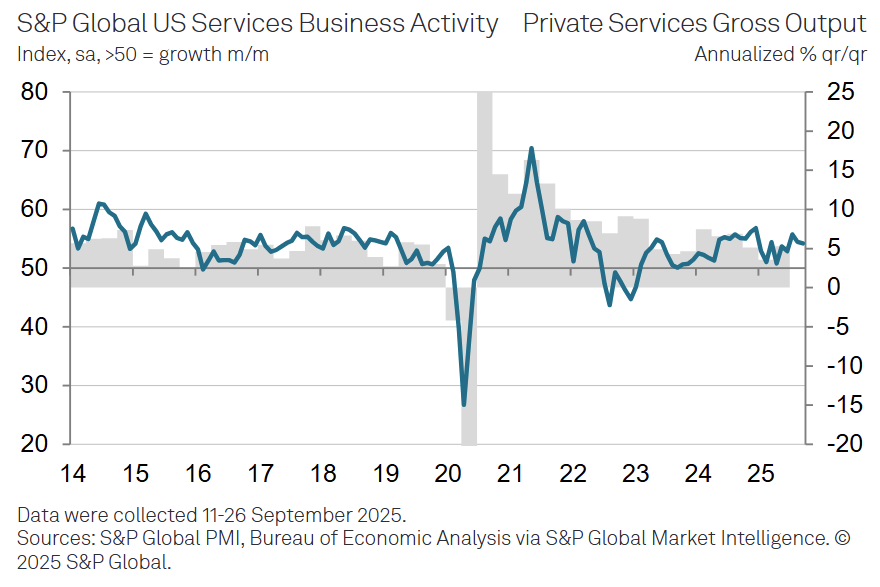

The S&P Global US Services PMI slipped to 54.2 in September (from 54.5 in August), marking the second straight monthly decline though still indicating solid expansion, with Q3 growth the strongest so far in 2025.

-

Business activity continued to expand for the 32nd consecutive month, though the pace slowed from July’s year-to-date peak.

-

New business growth softened to a three-month low, with tariffs and uncertainty weighing on demand; however, new export sales rose for the first time since March.

-

Backlogs of work increased solidly for the seventh consecutive month, underscoring ongoing capacity pressures.

-

Employment edged up only marginally, reflecting firms’ reluctance to add staff despite continued expansion; payroll growth has nonetheless now extended to seven months.

-

Input costs rose sharply, driven by tariffs, higher supplier charges, and wages, marking a slight acceleration in cost pressures.

-

Selling prices increased at the slowest rate in five months, as weaker demand and competition limited pricing power despite elevated costs.

-

Business confidence strengthened to its highest since May, supported by lower interest rates and expectations of supportive government policies.

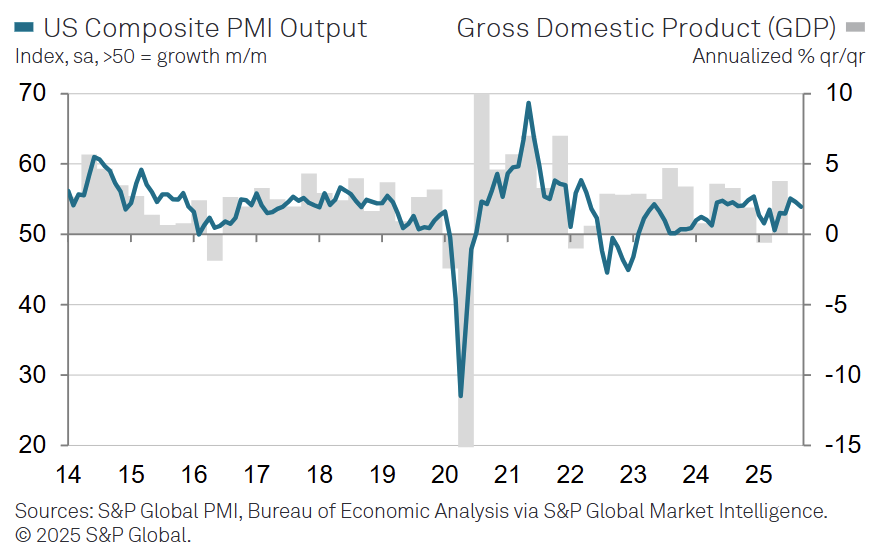

The S&P Global US Composite PMI fell to 53.9 in September (from 54.6 in August), marking the slowest pace of growth in three months as both manufacturing and services saw softer expansions.

-

Output growth moderated across both sectors, reflecting slower gains in new business.

-

Employment rose only marginally, showing limited hiring momentum despite continued expansion.

-

Business confidence strengthened noticeably, indicating greater optimism for future activity.

-

Input cost inflation remained elevated but eased to a five-month low, suggesting some relief in price pressures.

-

Output charges followed a similar trend, with selling price inflation also softening to its weakest level in five months.