S&P Global Services PMIs: August 2025

Global - 9/4/2025

Asia Pacific

- Australia - 9/2/2025

- Singapore (Composite only) – 9/3/2025

- Hong Kong (Composite only) – 9/3/2025

- Japan – 9/3/2025

- China – 9/3/2025

- India – 9/3/2025

- Russia – 9/3/2025

- Kazakhstan – 9/3/2025

Africa & Middle East

- Nigeria (Composite only) - 9/1/2025

- Qatar (Composite only) - 9/3/2025

- Kuwait (Composite only) - 9/3/2025

- Egypt (Composite only) - 9/3/2025

- UAE (Composite only) - 9/3/2025

- Uganda (Composite only) – 9/3/2025

- South Africa (Composite only) – 9/3/2025

- Lebanon (Composite only) – 9/3/2025

- Ghana (Composite only) – 9/3/2025

- Zambia (Composite only) – 8/6/2025

- Saudi Arabia (Composite only) – 9/3/2025

- Mozambique (Composite only) – 9/3/2025

- Kenya (Composite only) – 9/3/2025

Europe

- Ireland – 9/3/2025

- Spain – 9/3/2025

- Italy – 9/3/2025

- France – 9/3/2025

- Germany – 9/3/2025

- Eurozone – 9/3/2025

- UK – 9/3/2025

North & South America

Key Results

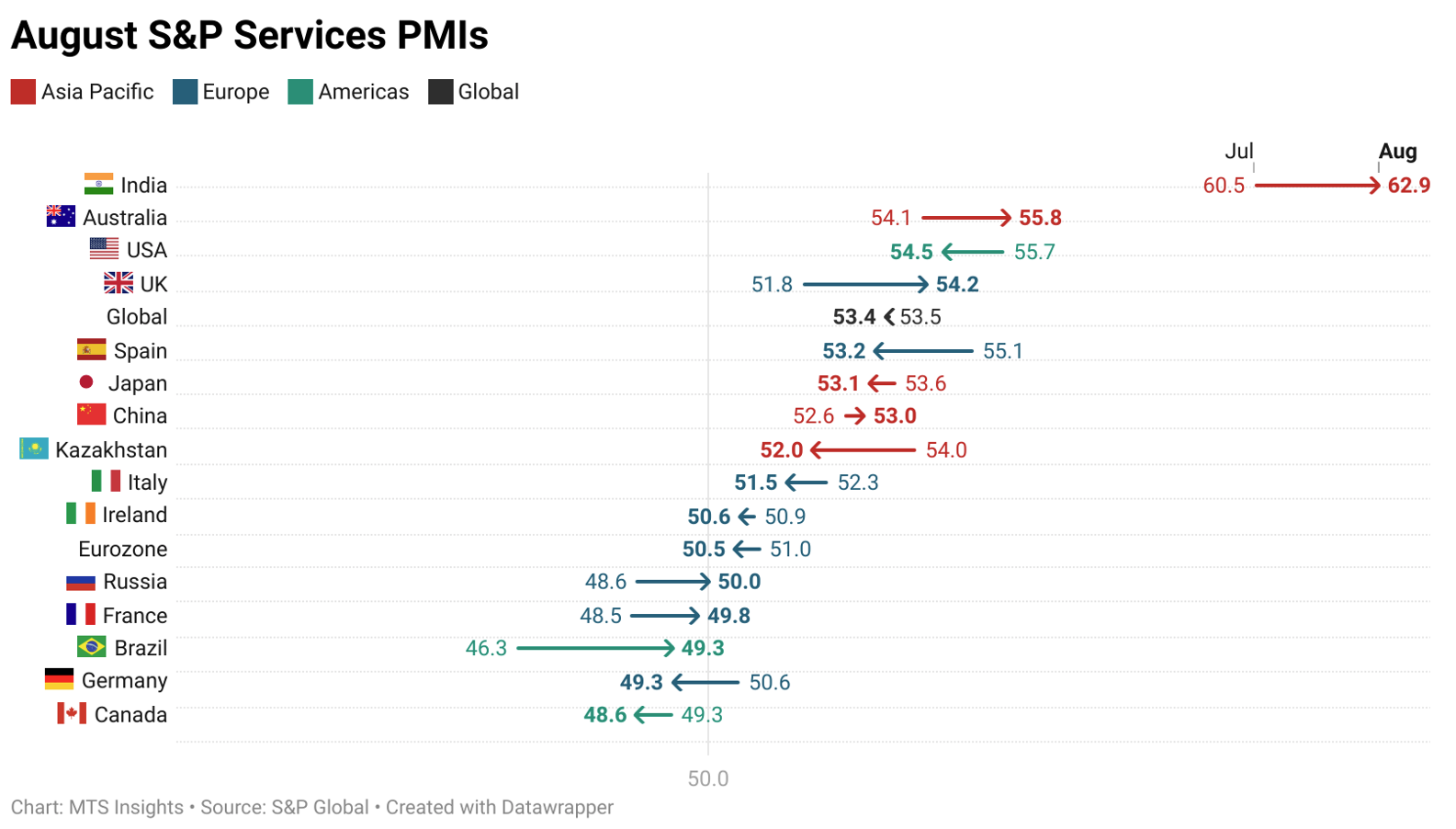

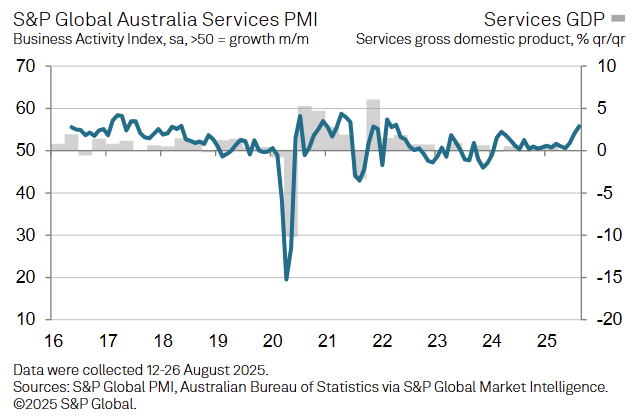

Australia

The S&P Global Australia Services PMI rose to 55.8 in August (from 54.1 in July), marking the strongest services expansion since April 2022 and extending the growth streak to 19 months.

-

New business rose sharply, with export orders increasing for the first time since February and at the fastest pace since June 2022, while domestic demand remained robust.

-

Employment growth accelerated to its highest in four months, as firms hired to manage workloads and ease capacity pressures, though backlogs continued to decline only fractionally.

-

Input costs, including supplies, fuel, and labour, increased again but at a slower pace than July; output prices also rose at a weaker rate, signaling softer inflationary pressures.

-

Business confidence improved, supported by expectations of continued sales growth and firmer global demand conditions.

-

The Composite Output Index, which includes both manufacturing and services, climbed to 55.5 (from 53.8), the fastest pace of private-sector growth since April 2022.

China

China’s General Services PMI rose to 53.0 in August (from 52.6 in July), the fastest expansion since May 2024, with stronger domestic and export demand offset by weaker employment trends.

-

New business expanded at the quickest pace since May 2024, with new export orders rising at the fastest rate since February, driven by better market conditions, tourism, and business development.

-

Backlogs of work increased for the fifth consecutive month, with growth accelerating compared to July, highlighting sustained pressure on capacity.

-

Employment declined at the sharpest pace in five months, as firms reported redundancies and non-replacement of leavers amid cost concerns.

-

Input costs continued to rise for the sixth straight month on higher wages and raw materials, though the pace of increase softened; output charges fell back into contraction, signaling persistent margin pressures.

-

The Composite Output Index climbed to 51.9 (from 50.8), the strongest expansion since November 2024, supported by services-led growth and improved business confidence, though manufacturing remained weaker.

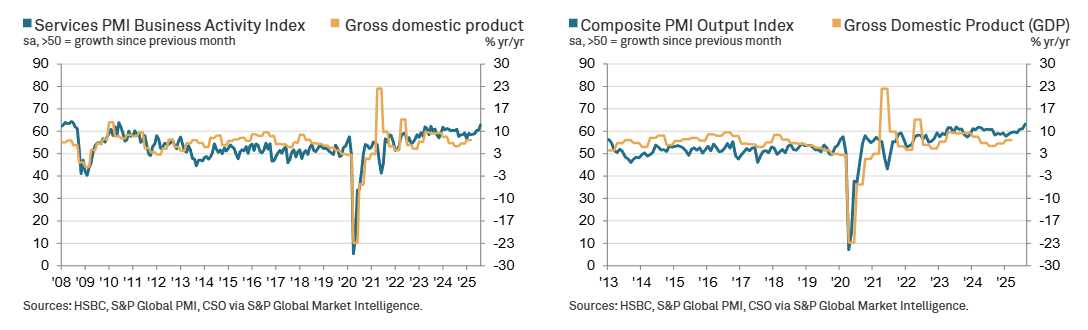

India

India’s Services PMI rose to 62.9 in August (from 60.5 in July), marking the steepest expansion since June 2010, supported by surging demand and strong international sales.

-

New orders expanded for the 49th straight month, reaching their highest rate in over 15 years; export orders also rose sharply, recording the third-strongest increase since the series began in 2014.

-

Employment increased moderately, aided by part-time hiring, while strong recent job creation ensured firms had sufficient capacity, keeping backlogs nearly stable.

-

Input costs rose at the fastest pace since November 2024, driven mainly by higher wages and overtime payments, while some firms also cited transport and material costs.

-

Output charges increased at the steepest rate since July 2012, reflecting firms’ ability to pass higher expenses onto clients amid robust demand.

-

The Composite PMI climbed to 63.2 (from 61.1), a 17-year high, indicating broad-based acceleration across both services and manufacturing.

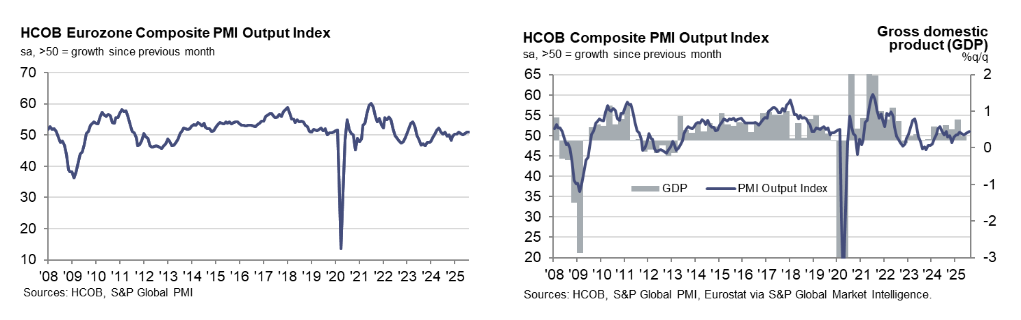

Eurozone

The HCOB Eurozone Composite PMI edged up to 51.0 in August from 50.9 in July, a 12-month high, signalling a slight acceleration in growth.

-

Services PMI eased to 50.5 (down from 51.0) while manufacturing recorded its strongest production rise in almost 3½ years, showing growth constrained mainly by services.

-

Total new orders rose for the first time since May 2024, but new export orders fell at the quickest pace since March, indicating demand was domestically led.

-

Employment increased for a sixth month at the fastest pace in 14 months, though factory headcounts continued to shrink; backlogs were reduced only slightly, the softest depletion in nearly 2½ years.

-

Input cost inflation accelerated to the fastest since March and firms raised output charges at the greatest rate in four months; in services, input costs hit a 3-month high and charges rose at the fastest pace since March.

-

Country detail: Spain 53.7 (2-month low), Italy 51.7 (3-month high), Ireland 51.3 (14-month low), Germany 50.5 (2-month low), and France 49.8 (12-month high but still <50).

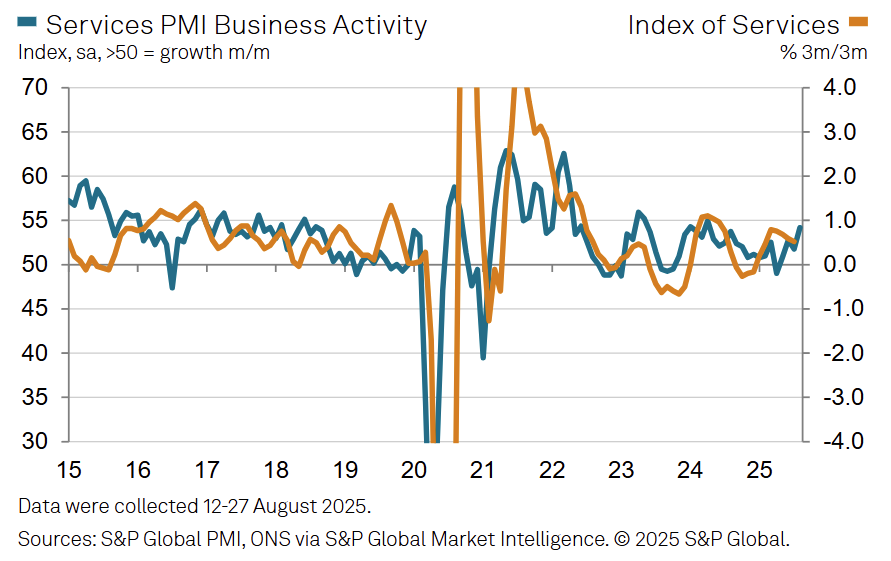

UK

UK Services PMI rose to 54.2 in August (from 51.8 in July), a 16-month high, while the Composite Output Index increased to 53.5 (from 51.5), marking a one-year high and signalling firmer momentum.

-

New orders returned to growth, rising at the strongest pace since Sep 2024; export orders increased for the first time since March, indicating demand improved both domestically and abroad.

-

Backlogs were depleted for the 27th straight month and at a solid pace, suggesting firms retained sufficient capacity despite stronger workloads.

-

Employment fell for the 11th consecutive month amid hiring freezes, non-replacement of leavers, and redundancies, reflecting margin pressure from rising payroll costs.

-

Input cost inflation re-accelerated to a 3-month high on higher wages (incl. NI contributions), food, and technology costs; output charge inflation hit its highest since April, showing persistent pricing pressures.

-

Business optimism rose to a 10-month high (49% expect higher activity vs 14% expecting a decline), supported by lower borrowing costs and improved sales pipelines, though policy uncertainty remains a headwind.