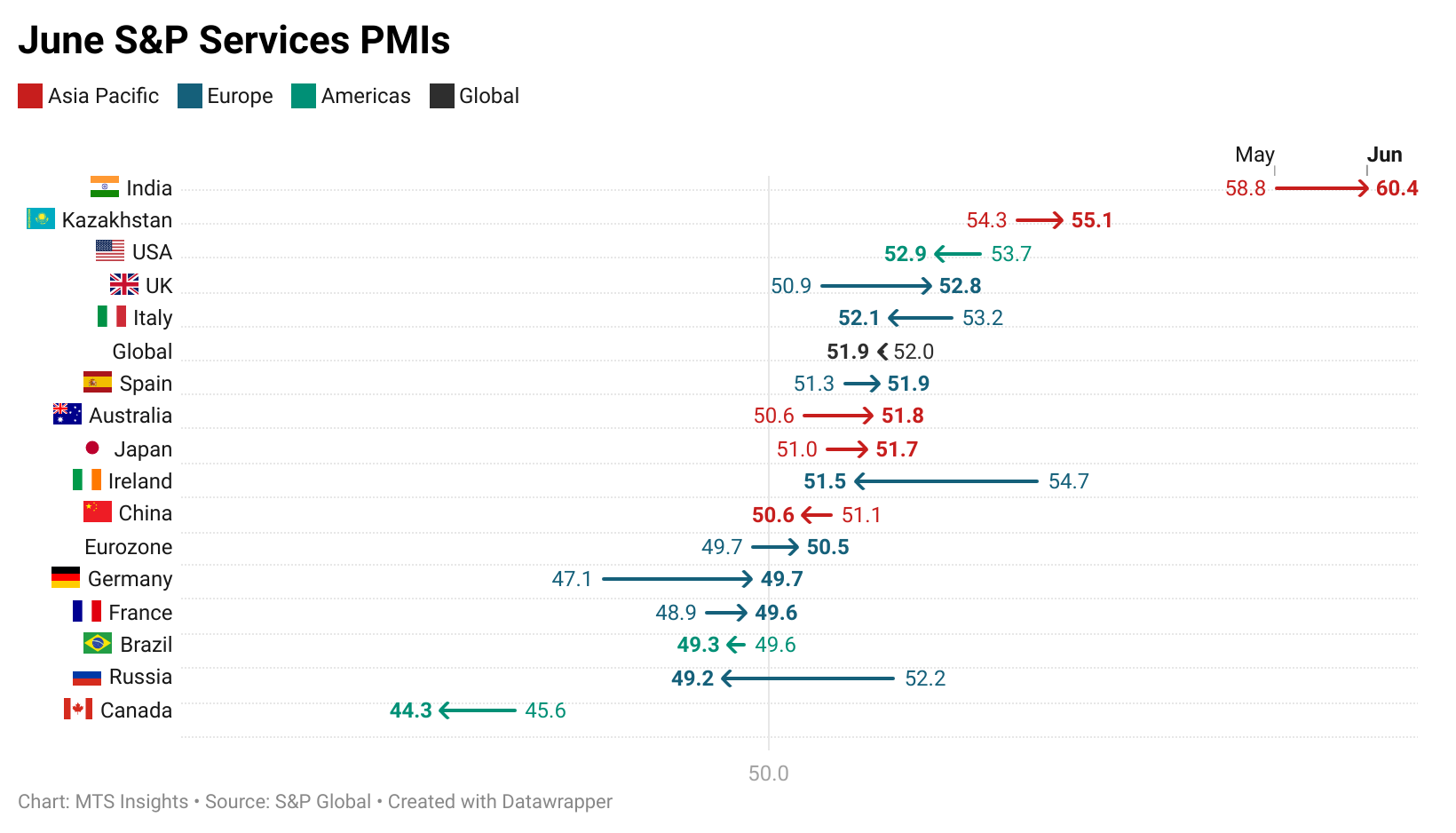

S&P Global Services PMIs: June 2025

Global - 7/3/2025

Asia Pacific

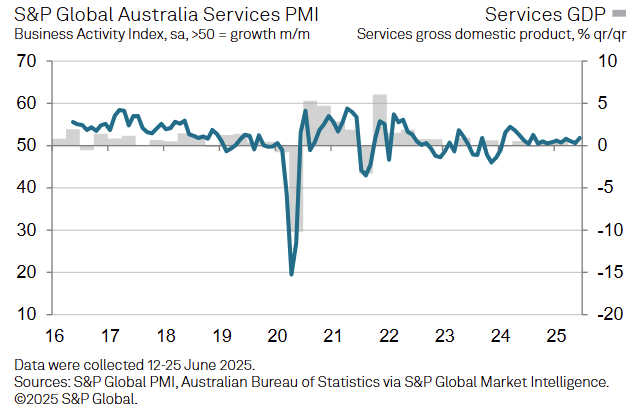

- Australia - 7/2/2025

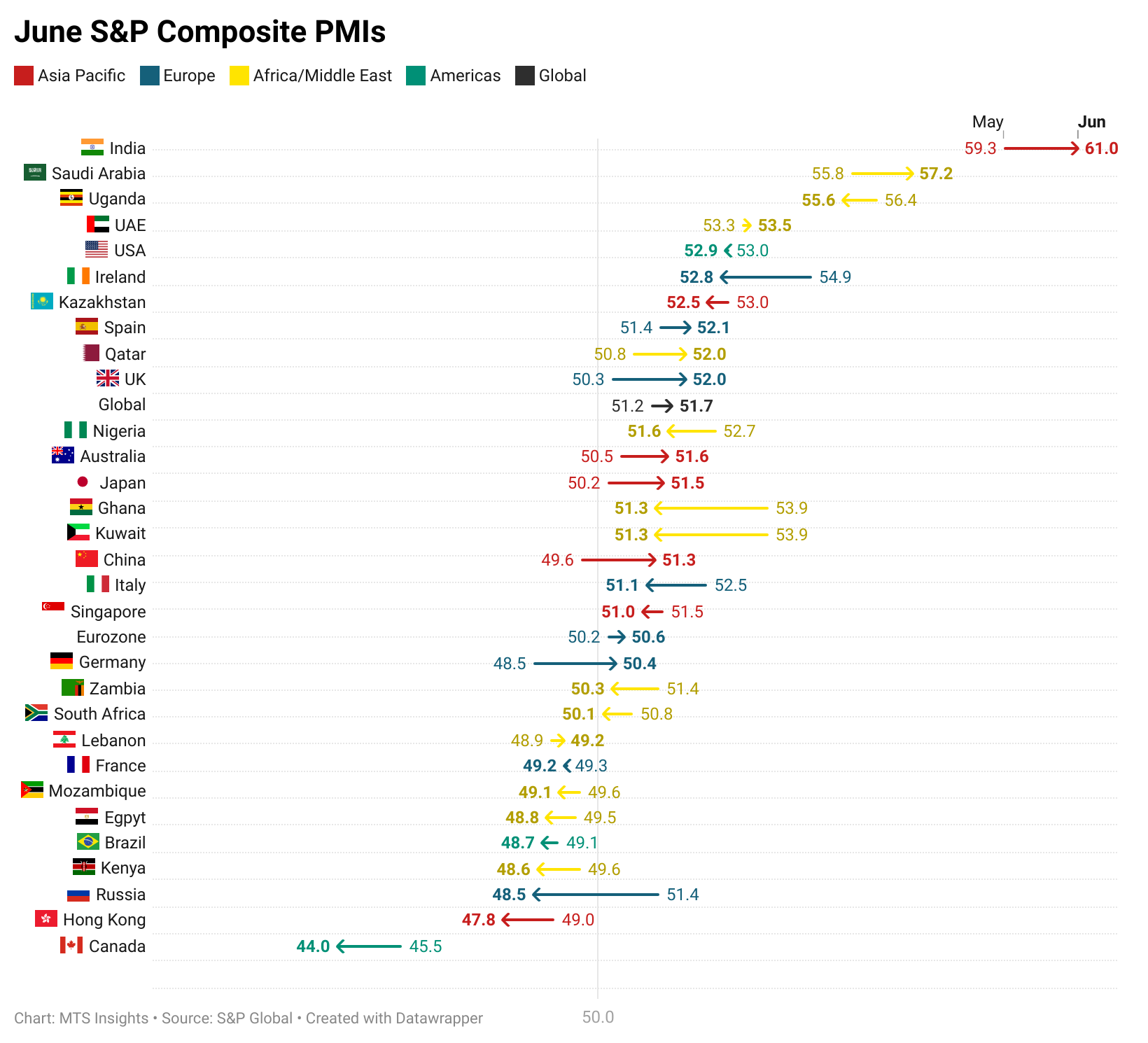

- Singapore (Composite only) – 7/3/2025

- Hong Kong (Composite only) – 7/3/2025

- Japan – 7/3/2025

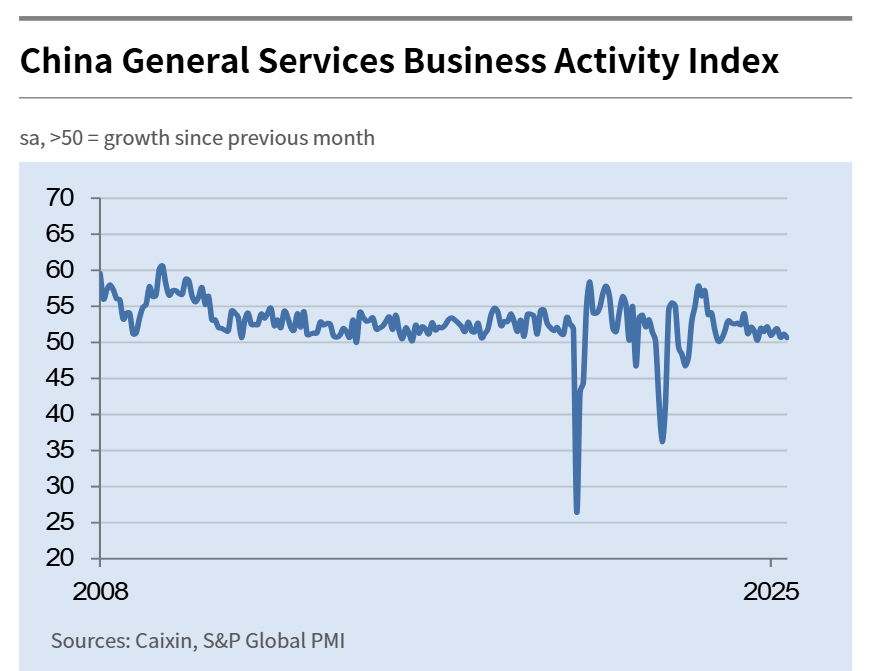

- China – 7/3/2025

- India – 7/3/2025

- Russia – 7/3/2025

- Kazakhstan – 7/3/2025

Africa & Middle East

- Nigeria (Composite only) - 7/1/2025

- Qatar (Composite only) - 7/3/2025

- Kuwait (Composite only) - 7/3/2025

- Egypt (Composite only) - 7/3/2025

- UAE (Composite only) - 7/3/2025

- Uganda (Composite only) – 7/3/2025

- South Africa (Composite only) – 7/3/2025

- Lebanon (Composite only) – 7/3/2025

- Ghana (Composite only) – 7/3/2025

- Zambia (Composite only) – 7/3/2025

- Saudi Arabia (Composite only) – 7/3/2025

- Mozambique (Composite only) – 7/3/2025

- Kenya (Composite only) – 7/3/2025

Europe

- Ireland – 7/3/2025

- Spain – 7/3/2025

- Italy – 7/3/2025

- France – 7/3/2025

- Germany – 7/3/2025

- Eurozone – 7/3/2025

- UK – 7/3/2025

North & South America

Key Results

Australia

Australia’s S&P Services PMI increased 1.2 pts to 51.8 in June, the highest since May 2024.

- New orders increased, driven by domestic sources of demand, while foreign demand contracted at the sharpest pace in 3.5 years.

- Services firms saw optimism rise to the highest level since May 2022.

China

The Caixin China General Services PMI fell -0.5 pts to 50.6 in June, the lowest in 9 months, indicating a softening in services activity.

- New business growth slowed, with new export orders falling at the fastest pace since December 2022.

- Employment declined for the third time in four months, contributing to the largest backlog buildup in a year.

- Input costs rose marginally, but output prices were cut at the sharpest pace since April 2022 due to competitive pressures.

- Business sentiment improved for a second month but remained well below the historical average.

- Composite PMI rose to 51.3 (from 49.6), as manufacturing rebounded and offset weaker services growth; selling prices fell at the fastest pace in over two years.

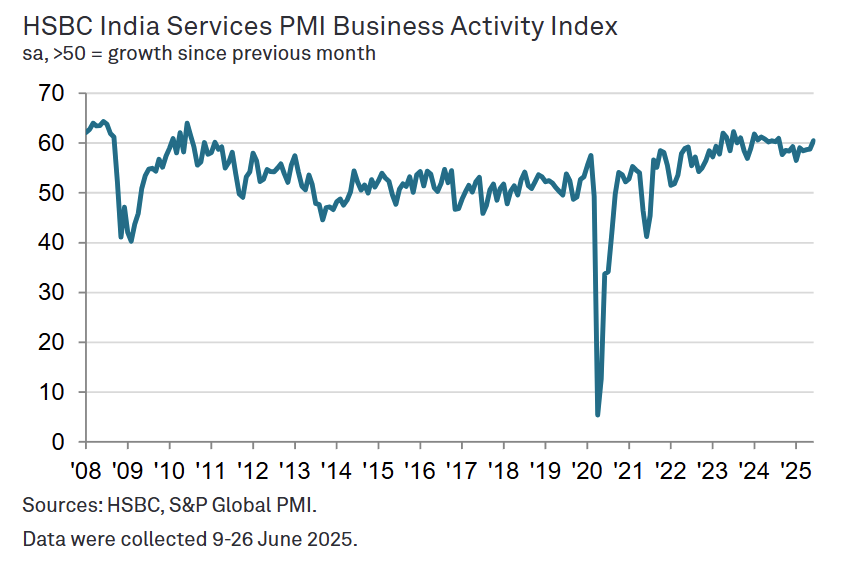

India

The S&P India Services PMI rose 1.6 pts to 60.4 in June, the highest in 10 months, signaling strong growth in activity driven by robust domestic and export demand.

- New orders expanded at the fastest pace since August 2024, with export orders remaining strong despite slowing modestly.

- Employment rose for the 37th straight month, though job creation softened from May’s record.

- Input cost inflation eased to a 10-month low, while output charge inflation also moderated but remained above the long-run average.

- Backlogs rose slightly, reflecting mild capacity pressures.

- Business optimism stayed positive but fell to its lowest level since mid-2022, below the long-run trend.

- The Composite PMI climbed to 61.0 (from 59.3), the strongest in 14 months, as manufacturing and services both contributed to broad-based private sector expansion.

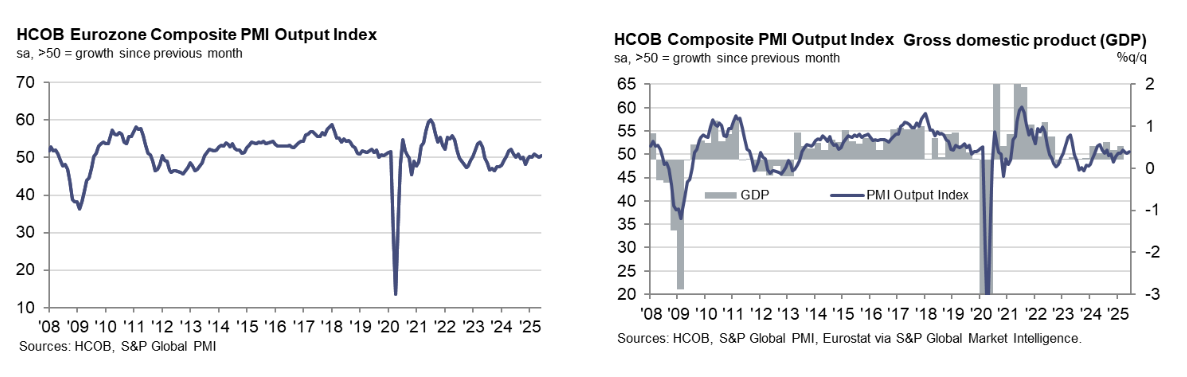

Eurozone

The S&P Eurozone Composite PMI rose to 50.6 in June from 50.2 in May, a 3-month high, signaling modest expansion in private sector output as both manufacturing and services activity increased.

- The Services PMI rose to 50.5 (from 49.7), also a 3-month high, with growth driven by employment gains and improved sentiment.

- New business fell for the 13th consecutive month, but the rate of contraction was the weakest in over a year.

- Input price inflation held at a 6-month low; services saw sustained cost pressures, while manufacturing input costs declined.

- Output charges rose at the fastest pace in 3 months, with services firms increasing prices more than manufacturers.

- Business confidence improved to its highest level since July 2024, though it remained below the long-run average.

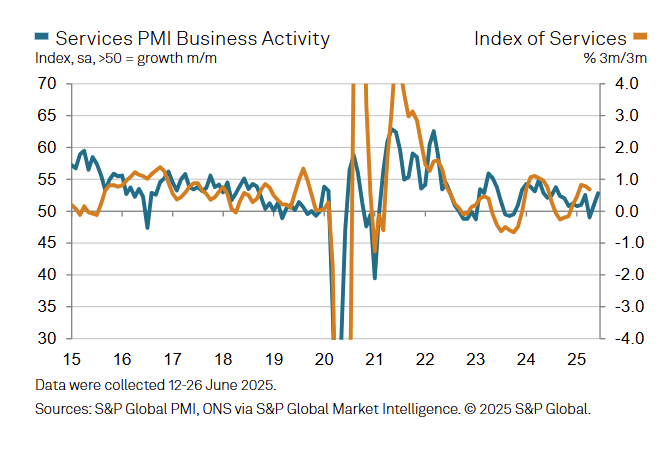

UK

The S&P Global UK Services PMI rose to 52.8 in June, up from 50.9in May, the highest in 10 months, reflecting the fastest pace of growth since August 2024 amid a rebound in domestic demand.

- New orders increased for the first time in three months, led by domestic sales; export sales fell for the third straight month.

- Employment declined for a ninth consecutive month, with job shedding slightly faster than in May due to cost concerns and weak capacity pressures.

- Input cost inflation eased to a 6-month low, while output charge inflation slowed to the weakest pace since February 2021.

- Business confidence remained positive but softened from May amid concerns over UK economic prospects and geopolitical risks.

- The Composite PMI rose to 52.0 (from 50.3), marking the fastest private sector growth since September 2024.

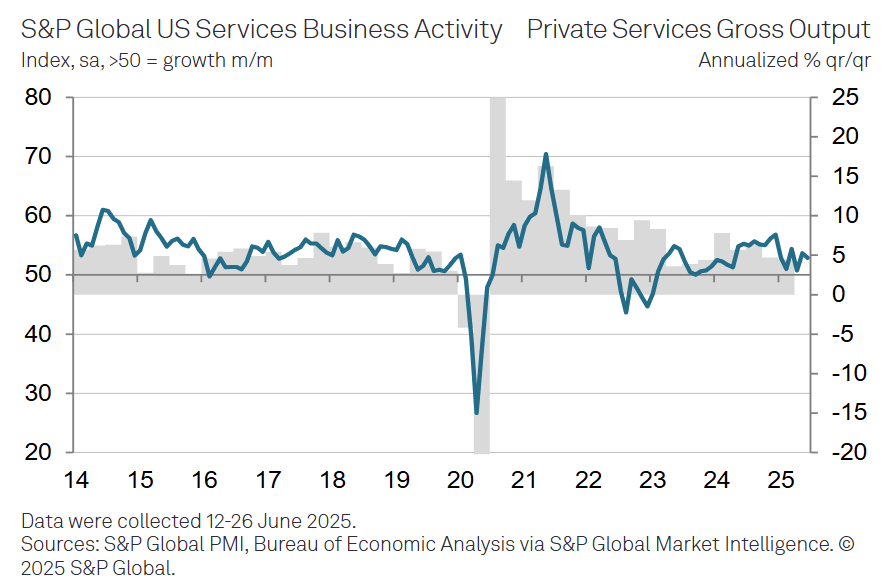

US

The S&P Global US Services PMI fell -0.8 pts to 52.9 in June, indicating slower but still solid growth in services activity as tariffs and policy uncertainty weighed on momentum.

- New business rose at a softer pace, while export sales declined for the third straight month, marking the steepest quarterly drop since late 2022.

- Input and output prices remained elevated, though inflation eased slightly from May’s near 2-year highs.

- Employment growth accelerated to a 5-month high, driven by rising workloads and improved hiring success.

- Business confidence stayed positive but softened further, remaining below the long-run average amid trade and policy concerns.

- The Composite PMI held nearly flat at 52.9 (vs 53.0 in May), with manufacturing rebounding and supporting overall private sector output.