ZEW Indicator of Economic Sentiment Germany

About

-

August 18th, 2026 · 5:00 AM

-

September 15th, 2026 · 5:00 AM

-

October 20th, 2026 · 5:00 AM

-

November 17th, 2026 · 5:00 AM

-

December 15th, 2026 · 5:00 AM

-

January 19th, 2027 · 5:00 AM

Latest Releases

12

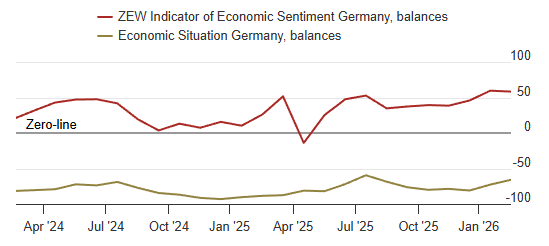

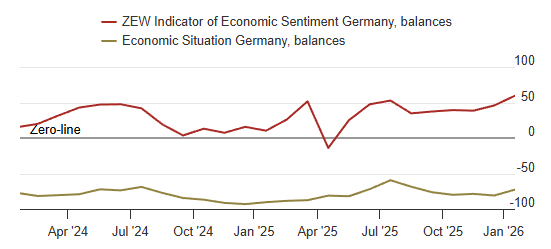

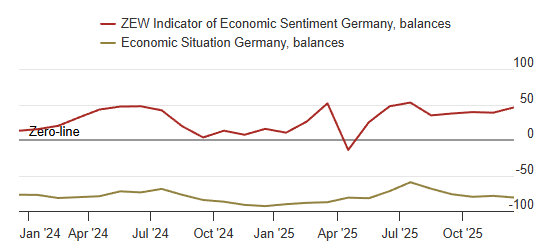

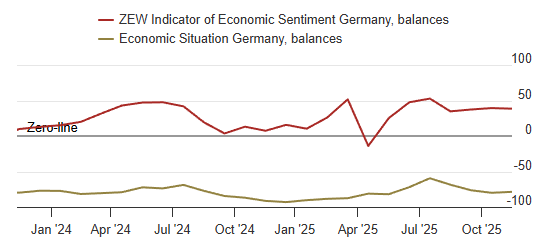

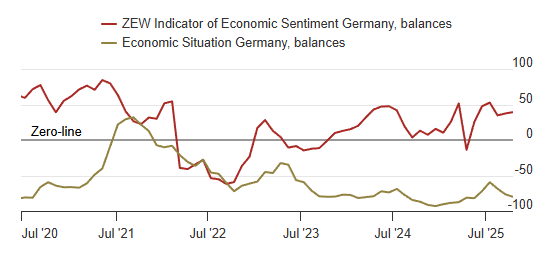

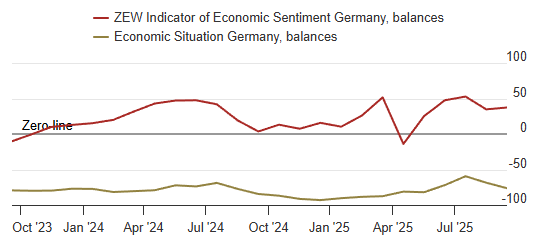

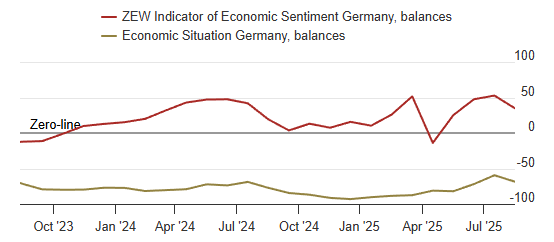

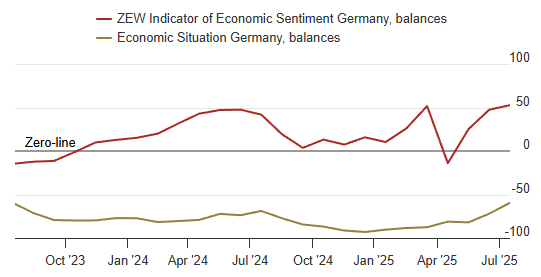

Germany’s ZEW Economic Sentiment fell -1.3 pts MoM to 58.3 in February, while the current conditions gauge improved, indicating stabilising expectations amid gradual recovery.

-

Germany current situation index rose +6.8 pts MoM to -65.9, showing the assessment of present economic conditions remains negative but continues to improve month to month.

-

Export-oriented industries recorded notable gains: chemicals/pharma +7.5 pts, steel/metal +8.6 pts, and mechanical engineering +10.9 pts, which the survey linked to stronger-than-expected incoming orders late in 2025.

-

Expectations for private consumption increased +6.0 pts, pointing to a modest improvement in household outlook despite ongoing uncertainty.

-

Sentiment weakened in banks, insurance, and information technology sectors, highlighting divergence across industries rather than a uniform improvement.

-

Eurozone expectations were 39.4 (-1.4 pts MoM), suggesting the broader regional outlook remained largely steady compared with the prior month.

-

Eurozone current conditions rose +4.5 pts to -13.6, indicating the present situation is still negative but improving similarly to Germany’s trend.

-

ZEW described the recovery as fragile and emphasized structural challenges, particularly in industry and private investment, even as sentiment stabilises.

Germany’s ZEW Indicator of Economic Sentiment rose +13.8 pts to +59.6 in January 2026, reflecting a sharp improvement in expectations alongside a less negative assessment of current conditions.

-

The ZEW current situation indicator for Germany improved to -72.7 in January (from -81.0), a +8.3 pt MoM move, indicating the present-day assessment is still weak but less pessimistic than last month.

-

Euro area expectations also strengthened, with the eurozone expectations balance rising to +40.8 (+7.1 pts MoM), while the euro area current situation balance improved to -18.1 (+10.4 pts MoM).

-

Survey breakdown for Germany’s current situation showed 75.0% rated conditions as “bad” (vs 22.7% “normal” and 2.3% “good”), leaving the balance at -72.7 despite the monthly improvement.

-

Germany expectations were heavily skewed positive, with 63.7% expecting improvement (32.2% no change; 4.1% worse), producing the +59.6 expectations balance and underscoring the optimism shift.

-

Export-oriented industries recorded notable sentiment gains despite new US tariff announcements, with balances rising +18.2 pts in steel/metal and +22.7 pts in mechanical engineering, suggesting improved outlooks in cyclically sensitive segments.

-

Sector sentiment improved across autos (+16.5 pts to -5.5), chemicals/pharma (+12.4 pts), and electrical engineering (+14.0 pts), which ZEW linked to stronger-than-expected industrial production in November 2025 and a surprisingly strong rise in orders.

-

ZEW cited the Mercosur agreement as supportive for export-intensive industries, while emphasizing unpredictable US trade policy as a continuing burden on Germany’s export economy.

Germany’s ZEW Indicator of Economic Sentiment rose +7.3 pts MoM to +45.8 in December 2025, reflecting improved expectations after prolonged economic stagnation.

-

The ZEW Current Situation Index fell -2.3 pts MoM to -81.0, indicating a slightly weaker assessment of present economic conditions despite better forward-looking sentiment.

-

ZEW highlighted that expectations have turned more positive after three years of stagnation, with expansive fiscal policy cited as a source of potential economic momentum.

-

Sentiment toward the automobile industry improved notably, with its sector indicator rising +7.7 pts to -22.0, marking one of the strongest gains among industries.

-

Other export-oriented sectors, including chemicals, pharmaceuticals, and metals, also saw sentiment improve, though gains were smaller and conditions remained constrained by weak export volumes.

-

ZEW noted that high tariffs and structural competitive disadvantages continue to weigh on export-driven industries, despite supportive fiscal policy.

-

Euro area expectations rose +8.7 pts MoM to +33.7, outperforming Germany’s increase, while the eurozone current situation index slipped slightly by -1.2 pts to -28.5, suggesting modest regional improvement led by expectations rather than current activity.

Germany’s ZEW Indicator of Economic Sentiment edged down -0.8 pts to +38.5 in November 2025, remaining broadly stable and signaling cautious optimism, while the Current Situation Index rose slightly by +1.3 pts to -78.7.

-

ZEW noted that confidence in Germany’s economic policy has weakened, with structural challenges continuing to weigh despite potential support from new investment programs.

-

Outlooks in the chemical and metal sectors worsened, and the banking and insurance industries also reported declines compared with October.

-

Sentiment improved for private consumption (+13.3 pts) and rebounded modestly in electrical engineering, telecommunications, IT, and services, though earnings expectations remain lower overall.

-

For the euro area, the expectations index rose +2.3 pts to +25.0, while the Current Situation Index increased +4.5 pts to -27.3, suggesting mild improvement in the regional outlook.

The ZEW Indicator of Economic Sentiment for Germany rose +2.0 pts to 39.3 (vs 40.5 expected) in October 2025, showing modest improvement in expectations, while assessments of the current situation continued to worsen.

-

The Current Situation Index for Germany fell -3.6 pts to -80.0 (vs -75.0 expected), extending its downward trend and signaling persistent weakness in present conditions.

-

The ZEW noted that experts “still hope for an upturn in the medium term,” despite uncertainty surrounding global demand and domestic investment policy.

-

Expectations improved notably for export-oriented industries such as metal production, pharmaceuticals, mechanical engineering, and electrical equipment, though the automotive sector saw a slight decline.

-

For the euro area, the expectations index dropped -3.4 pts to 22.7, while the Current Situation Index fell -3.0 pts to -31.8, reflecting renewed pressure from the ongoing budget dispute in France.

The ZEW Indicator of Economic Sentiment for Germany rose +2.6 pts to 37.3 in September 2025, stabilising after August’s sharp decline, though the assessment of the current economic situation continued to weaken.

-

The Current Situation Index for Germany dropped -7.8 pts to -76.4, marking a further deterioration in conditions.

-

For the euro area, economic expectations improved slightly to 26.1 (+1.0 pts), while the current situation assessment rose modestly to -28.8 (+2.4 pts).

-

In the US, expectations strengthened to -30.2 (+11.6 pts), but the current situation balance remained weak at -33.8 (-7.4 pts).

-

For China, expectations edged up to 6.2 (+2.3 pts), while the current situation stayed firmly negative at -32.8 (+7.9 pts).

-

Inflation expectations stayed subdued in Europe, with the euro area at -3.4 (+3.3 pts) and Germany at -6.8 (+3.3 pts), while the US recorded a strong positive balance of +69.5 (+4.3 pts).

-

Short-term interest rate expectations were mostly negative, with balances of -22.6 for the euro area, -73.3 for the US, and -24.1 for China.

-

Long-term rate expectations diverged, with Germany (+37.3), the euro area (+34.0), and the US (+30.4) all positive, while China’s balance was more muted at +5.7.

The ZEW Indicator of Economic Sentiment for Germany fell -18.0 pts to 34.7 in August 2025, ending several months of gains, as experts reacted negatively to the announced EU–US trade deal and weak Q2 performance.

- The Current Situation Index for Germany dropped -9.1 pts to -68.6, while the eurozone index fell -7.0 pts to -31.2.

- Eurozone sentiment declined -11.0 pts to 25.1, reflecting downgraded growth expectations despite earlier positive Q2 estimates.

- Outlook worsened most for chemicals, pharmaceuticals, mechanical engineering, metals, and automotive industries.

- The expectations index for the US eased -7.0 pts to -41.2, while for China slipped just -0.3 pts to 3.9.

- Inflation expectations stayed negative in the eurozone (-6.7) and Germany (-5.1), while a net 74.5% of respondents expect the US to see higher inflation.

The ZEW Indicator of Economic Sentiment for Germany rose 5.2 pts to 52.7 in July 2025, continuing its upward trend and reflecting firming optimism despite global trade uncertainties.

- The Current Situation Index for Germany rose 12.5 pts to -59.5, still negative but improving.

- Sentiment in the eurozone rose 0.8 pts to 36.1, while the eurozone Current Situation Index increased 6.5 pts to -24.2.

- ZEW attributes rising optimism to easing US-EU trade tensions and Germany’s planned investment stimulus.

- Sector-specific sentiment improved notably in mechanical engineering, metal production, and the electrical industry.