UK Employment

UK Employment

- Source

- ONS

- Source Link

- https://www.ons.gov.uk/

- Frequency

- Monthly

- Next Release(s)

- March 19th, 2026 2:00 AM

-

April 21st, 2026 2:00 AM

-

May 19th, 2026 2:00 AM

-

June 16th, 2026 2:00 AM

-

July 21st, 2026 2:00 AM

-

August 18th, 2026 2:00 AM

-

September 15th, 2026 2:00 AM

-

October 20th, 2026 2:00 AM

-

November 17th, 2026 2:00 AM

-

December 15th, 2026 2:00 AM

Latest Updates

-

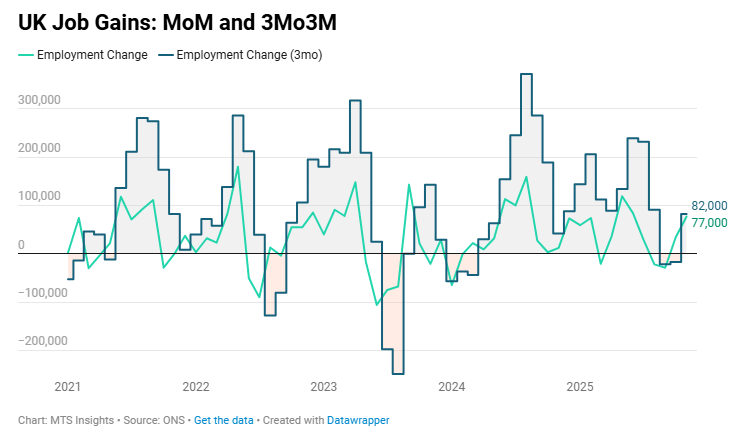

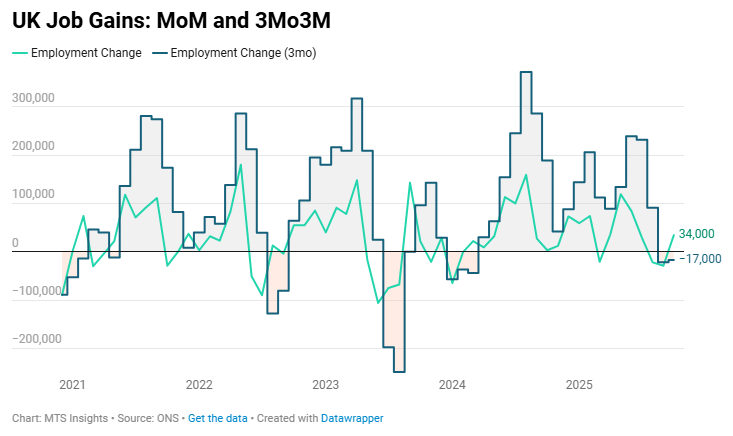

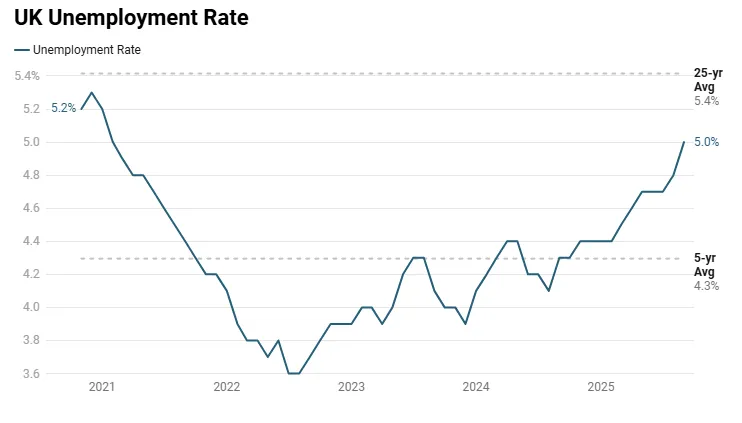

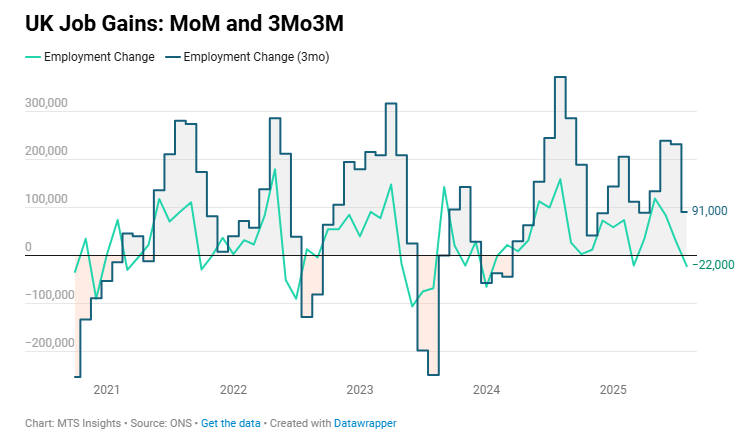

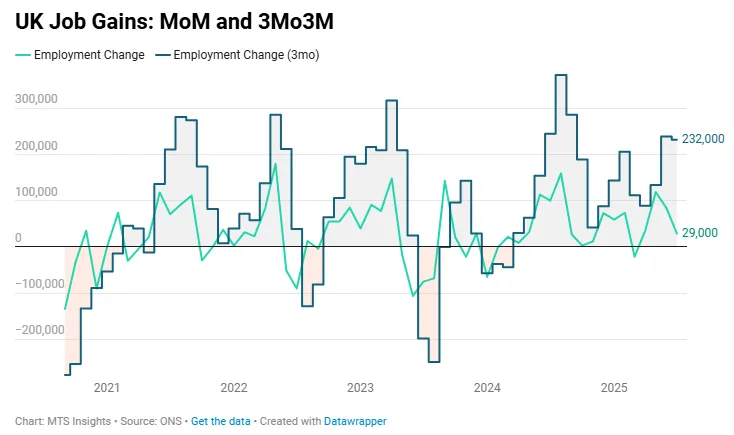

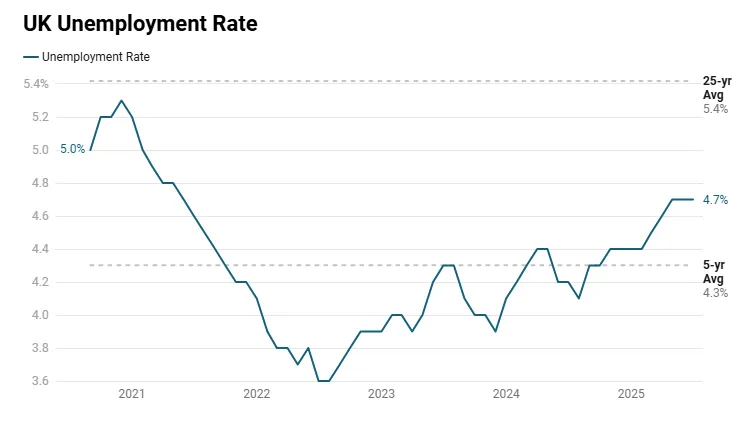

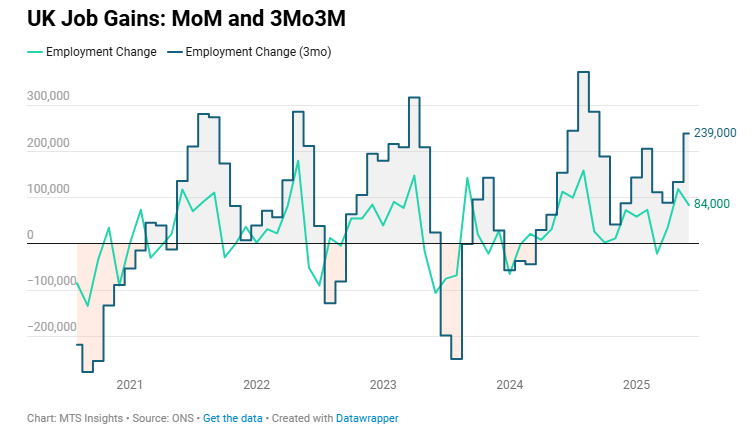

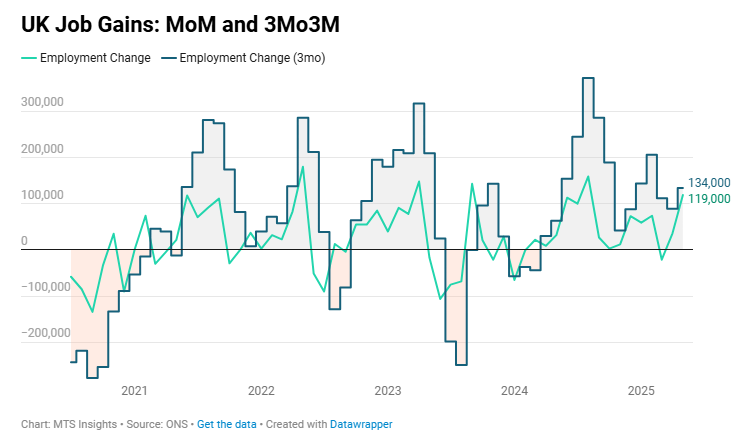

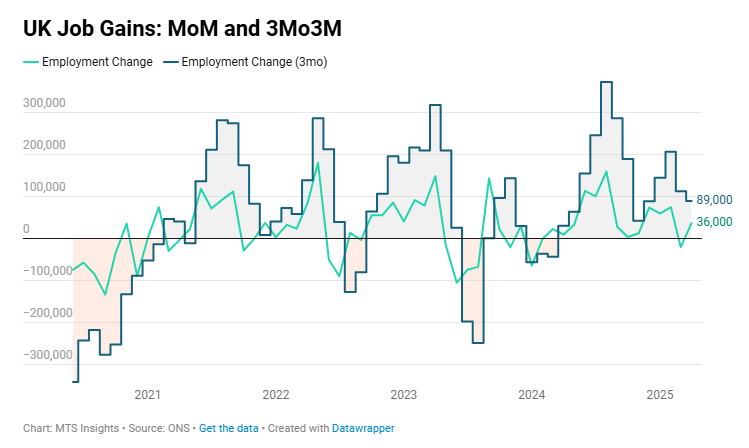

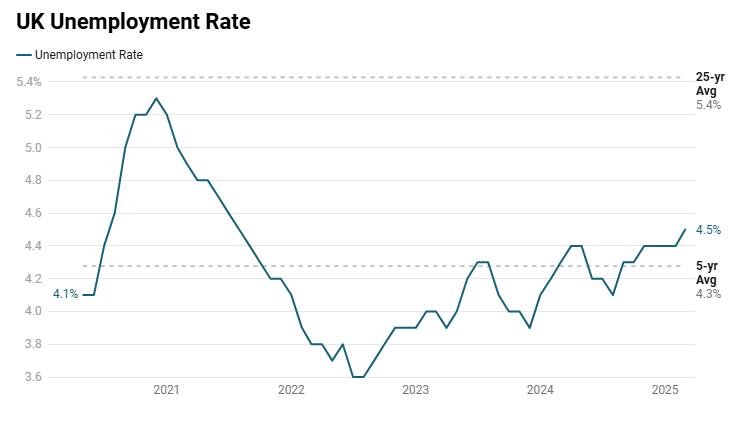

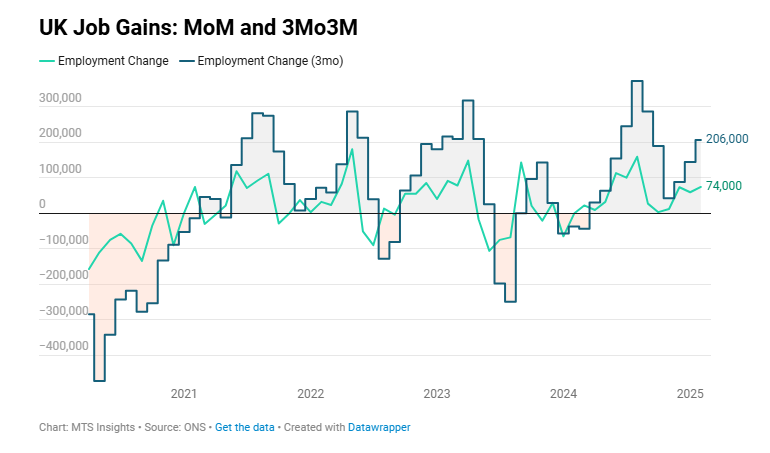

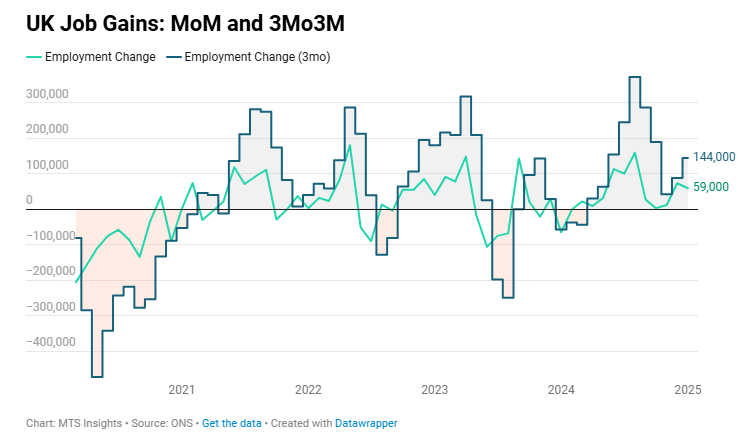

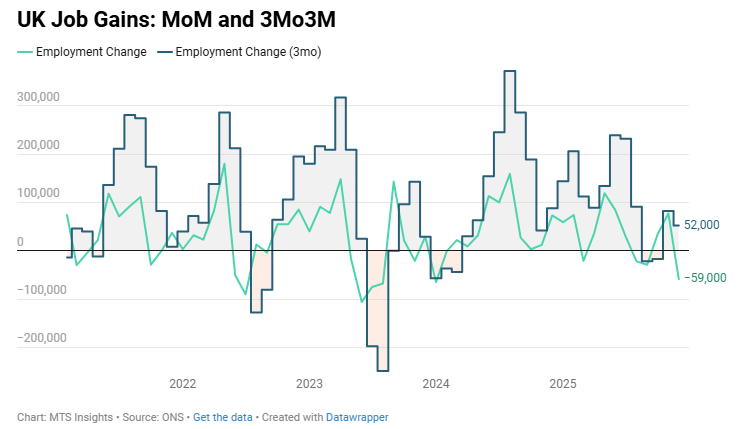

UK employment increased by 52k in the three months to December, with employment dropping -59k in December alone.

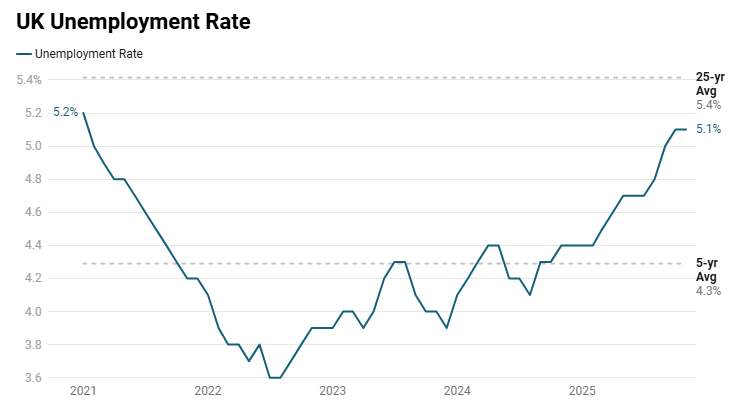

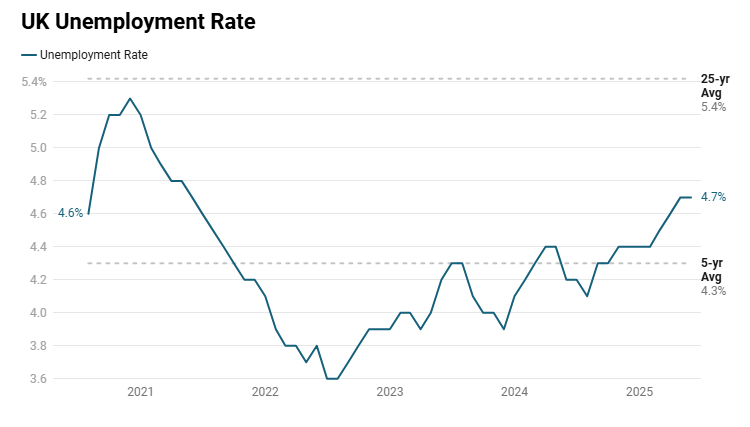

- The overall employment rate edged down -0.1 ppt to 75.0% in December, unchanged from a year ago.

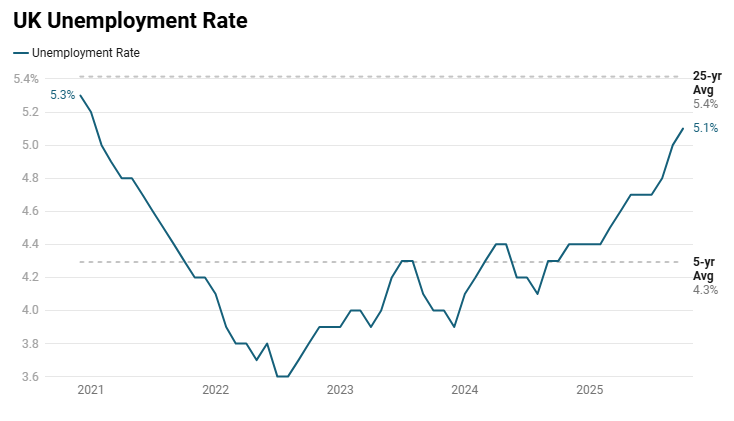

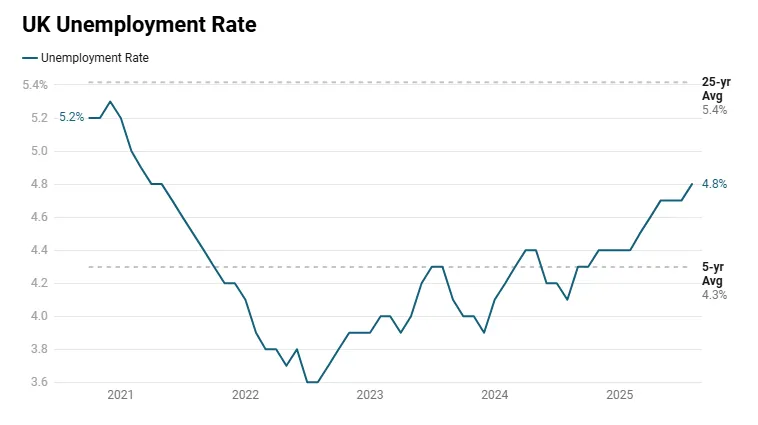

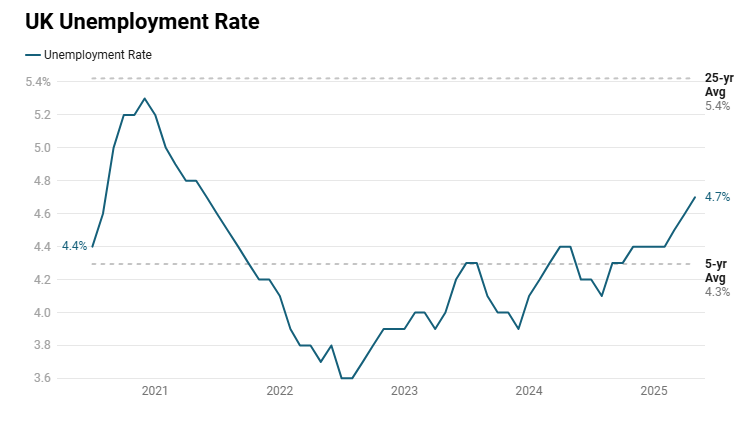

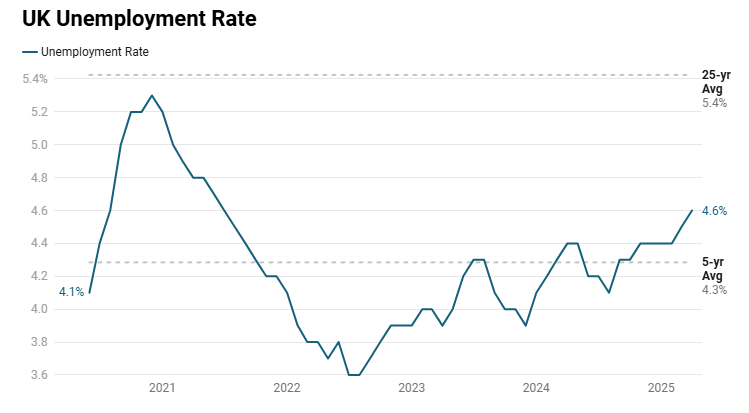

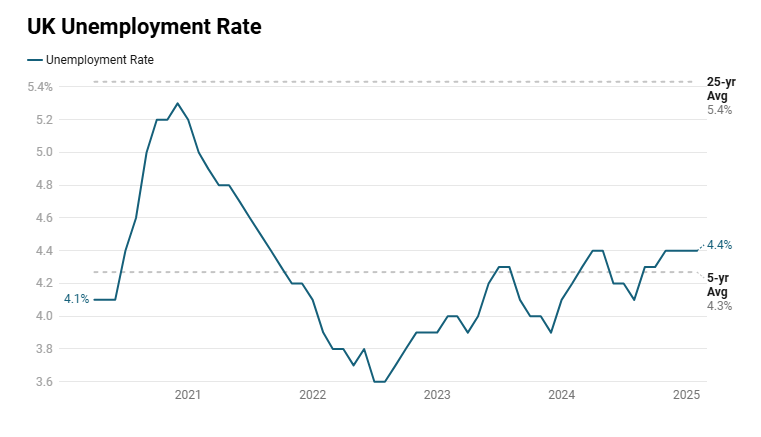

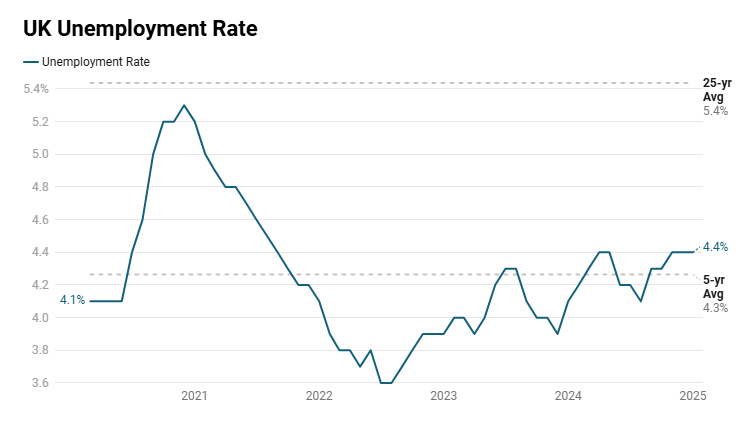

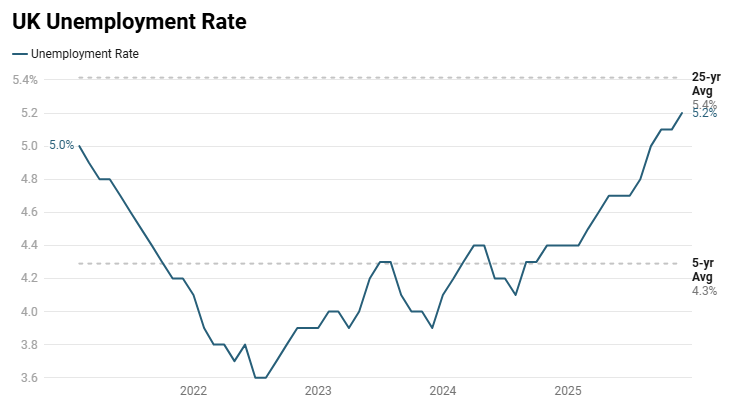

- The unemployment rate increased 0.1 ppt to 5.2% (vs 5.1% expected) in December, the highest since February 2021 and a 0.8 ppt increase from a year ago.

- The overall unemployment level has increased by 94k in the last three months and is up 331k in the last year.

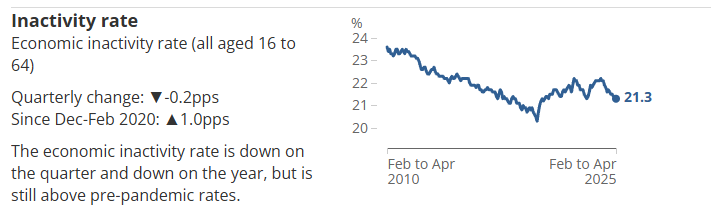

- The economic inactivity rate remained at 20.8% and is down -0.7 ppts YoY.

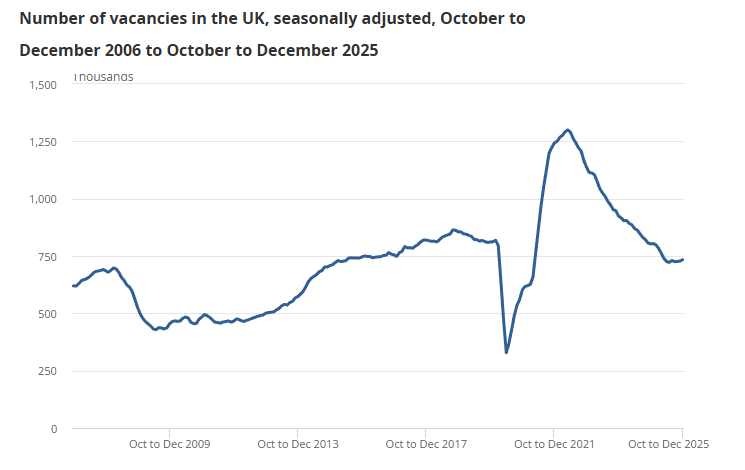

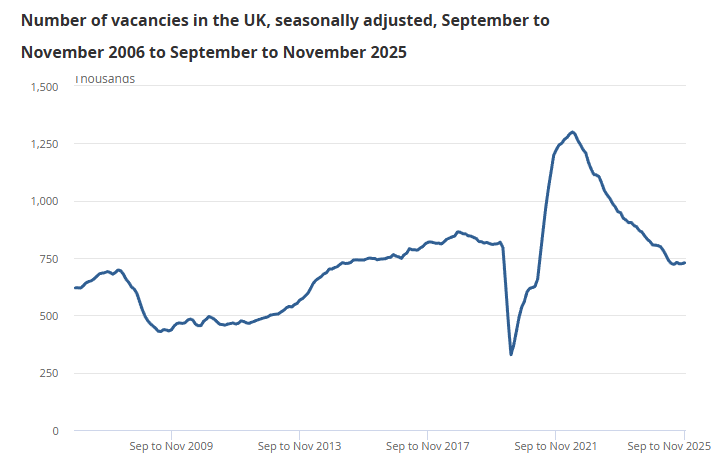

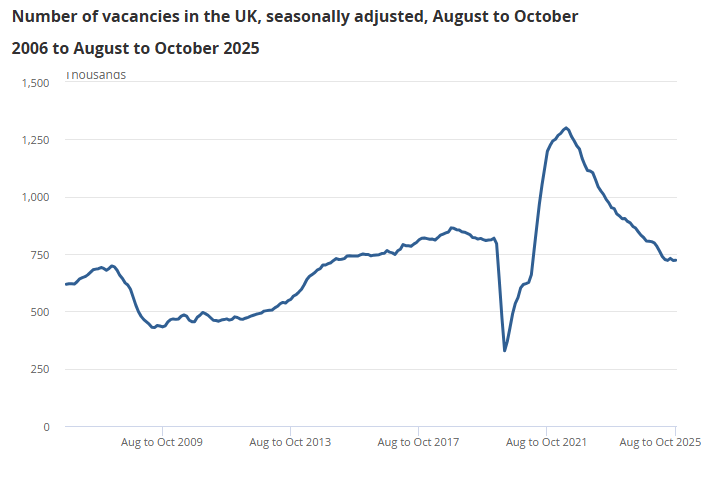

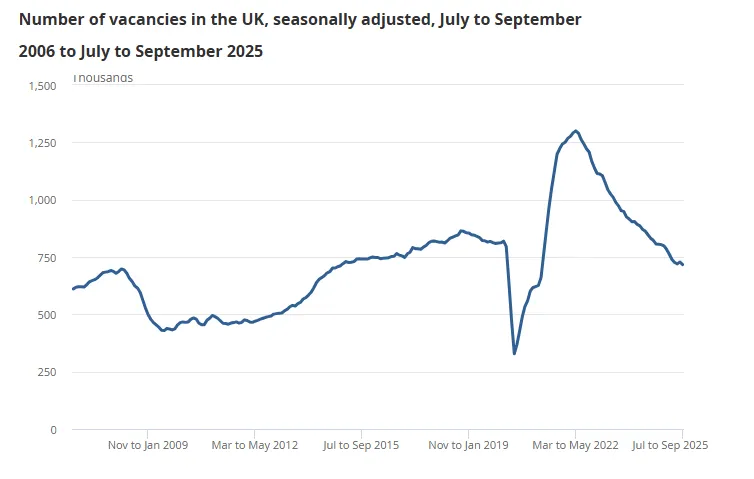

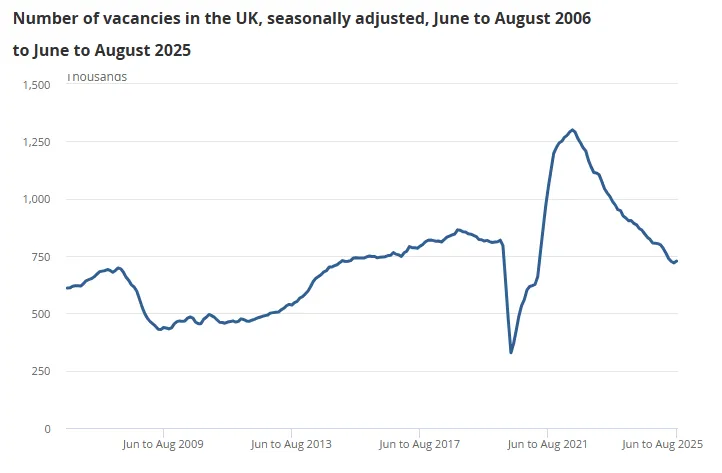

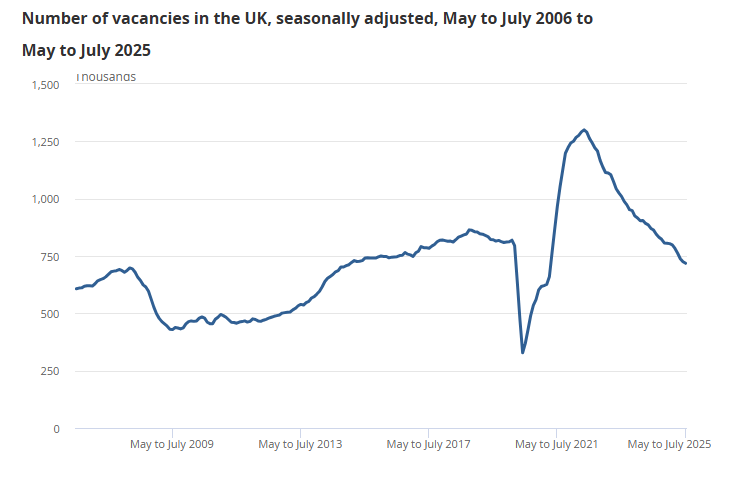

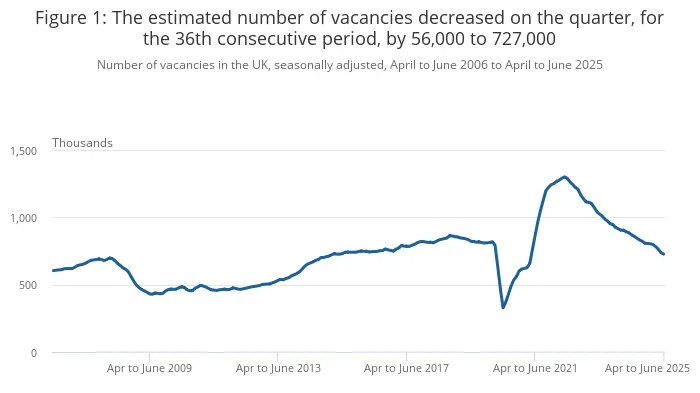

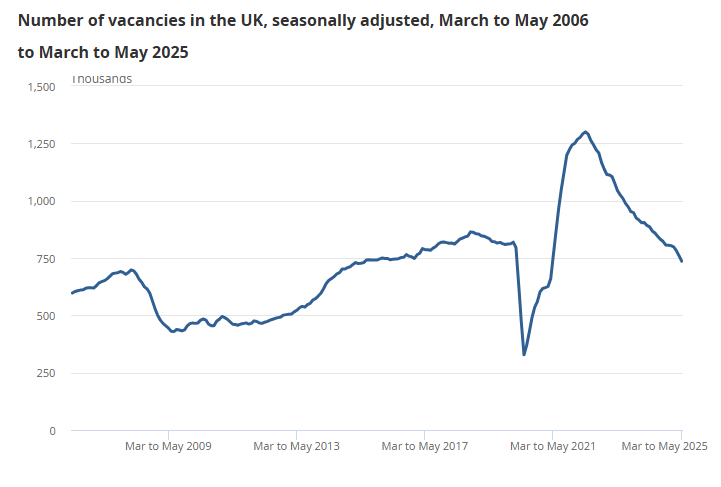

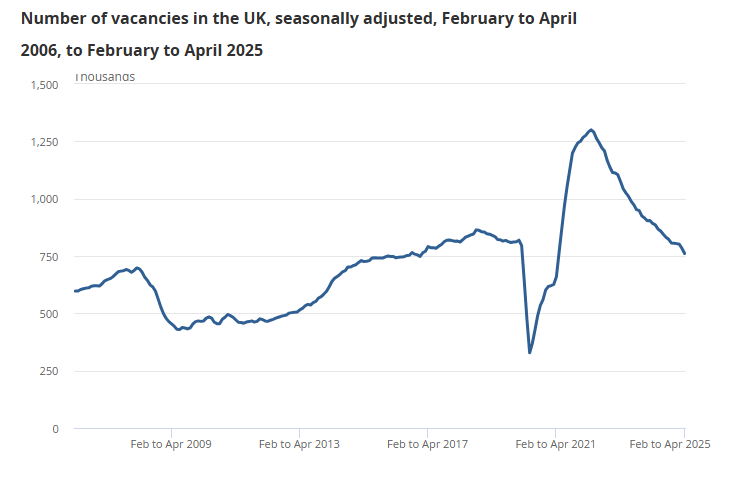

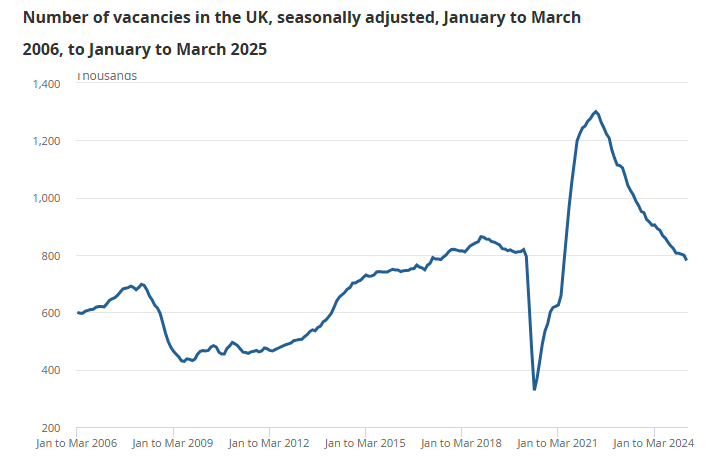

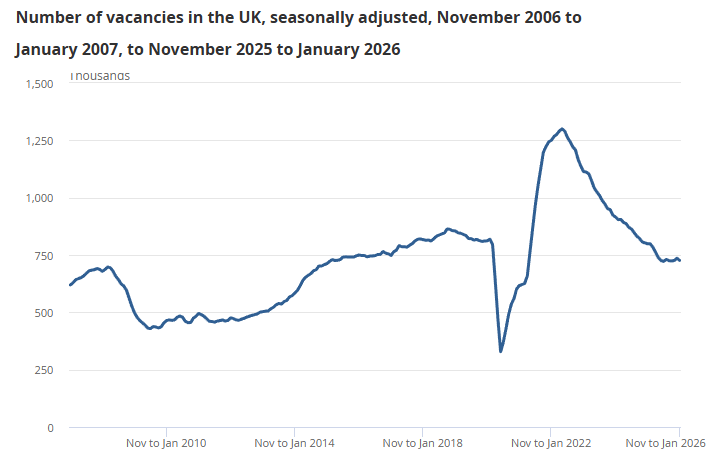

UK vacancies rose +0.3% QoQ to 726k but were still down -9.2% YoY, signaling stabilization after a prolonged decline.

-

Vacancies increased by +2k QoQ (Aug–Oct vs Nov–Jan) but remained broadly flat and within the ±32k confidence interval, indicating little meaningful short-term change.

-

Compared with a year earlier, vacancies declined -73k (-9.2%) and sit -69k (-8.7%) below pre-pandemic Jan–Mar 2020 levels, showing hiring demand remains structurally lower.

-

Labour market tightness eased, with 2.6 unemployed persons per vacancy (vs 2.5 prior quarter; 1.9 YoY), the highest non-pandemic level since Nov 2014–Jan 2015.

-

Quarterly increases occurred in 7 of 18 sectors, led by arts & recreation (+12.3%), while manufacturing and transport/storage posted the largest volume gains (+4k each), reflecting limited sectoral improvement.

-

YoY declines were broad-based across 14 of 18 sectors, steepest in construction (-32.4%) and mining & quarrying (-26.7%), indicating ongoing cooling across cyclical industries.

-

Larger firms drove quarterly gains, with businesses employing 2,500+ workers up +8k (+3.5%) QoQ, while small firms (1–49 employees) recorded the largest annual declines (-18k each), showing weaker small-business hiring.

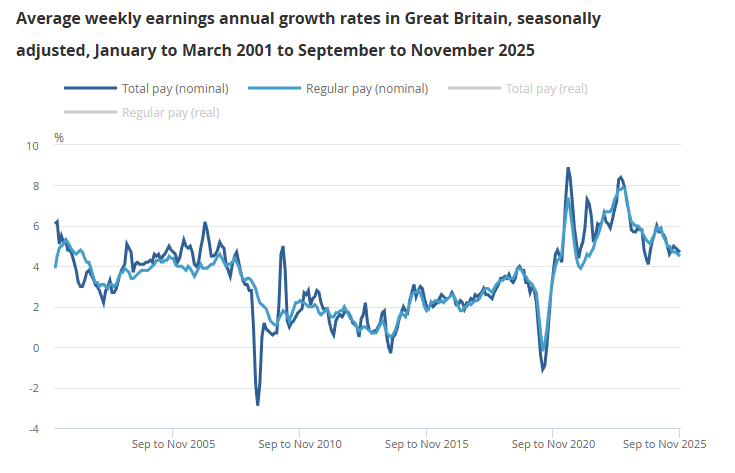

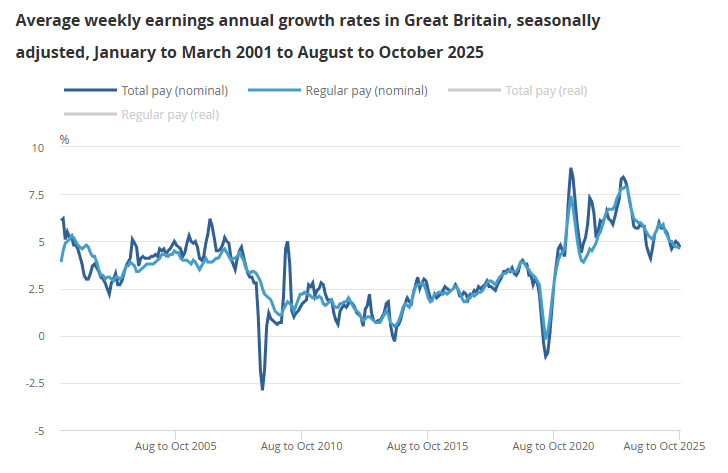

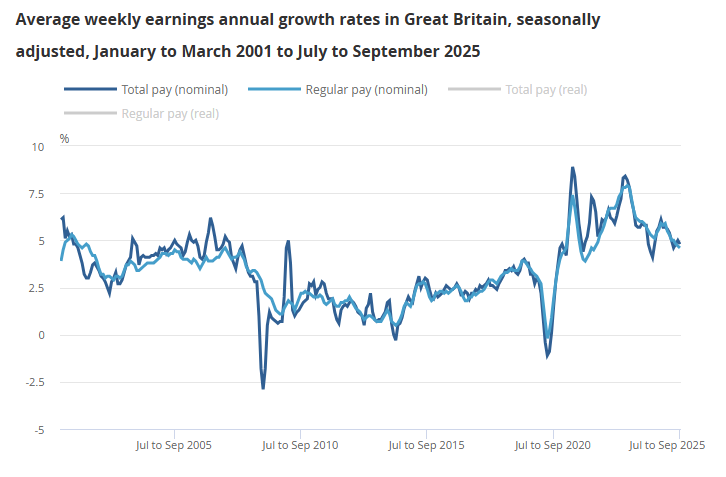

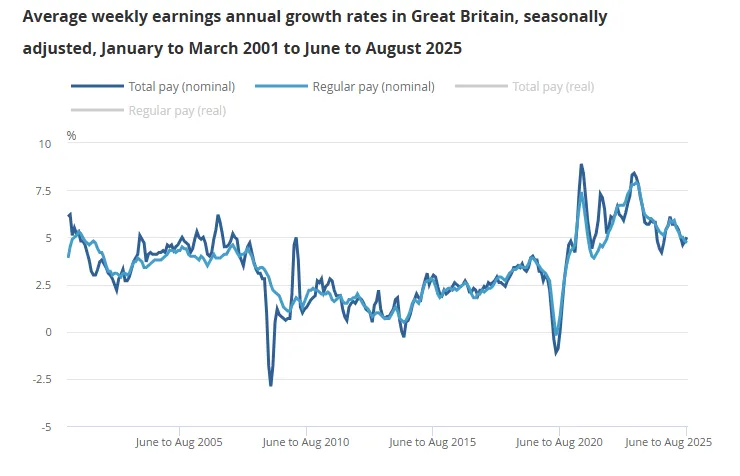

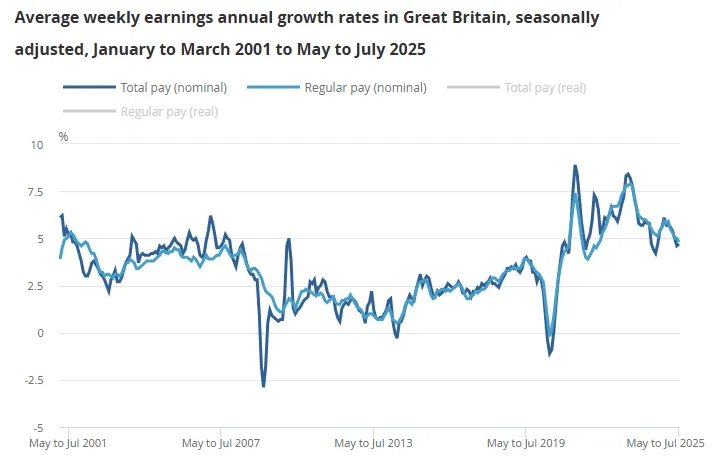

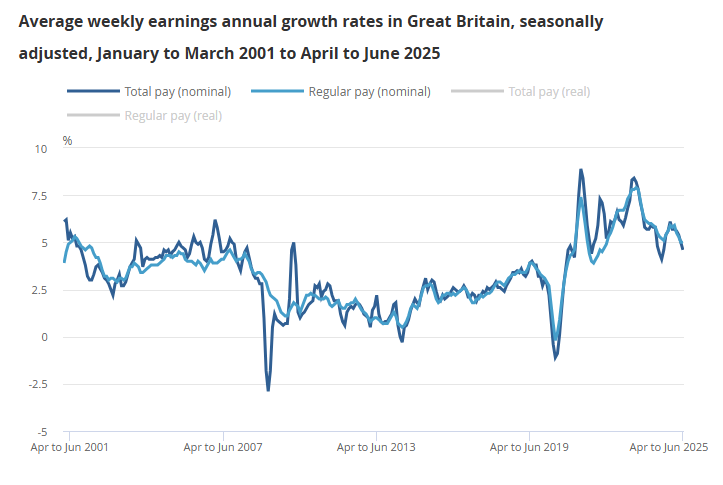

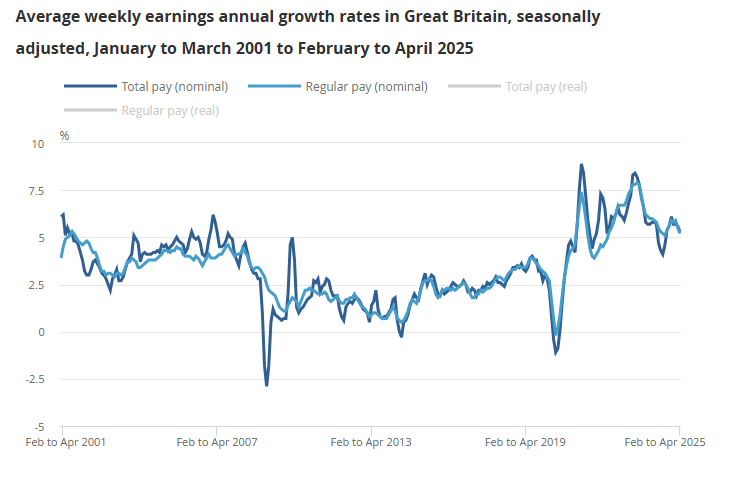

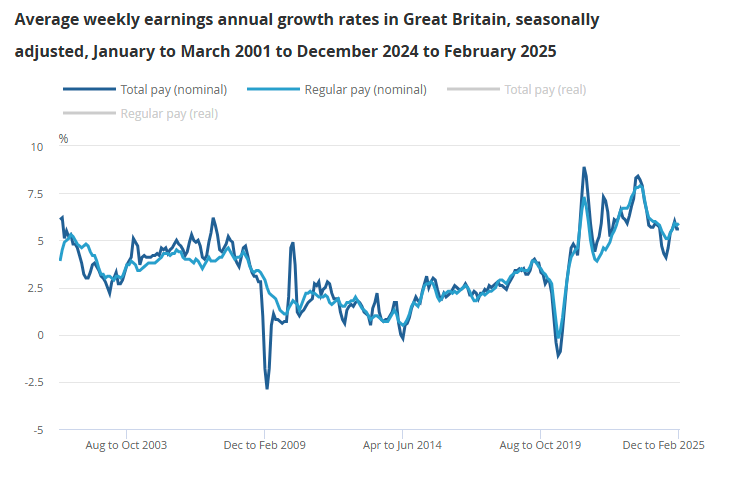

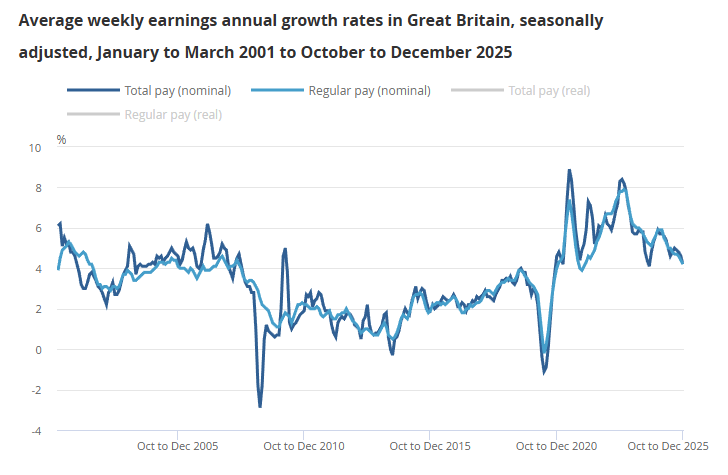

UK average weekly earnings (including bonuses) grew +4.2% YoY in Oct–Dec 2025, easing from +4.6% YoY in Sep-Nov 2025 to the lowest growth since August 2021.

-

UK regular pay (average weekly earnings excluding bonuses) was up +4.2% YoY in December, down from +4.4% YoY in November and the lowest since January 2022.

-

Real earnings rose +0.5% YoY using CPIH for both regular and total pay, indicating modest positive real wage gains after inflation adjustment.

-

Using CPI, real regular pay increased +0.8% YoY and real total pay +0.7% YoY, slightly stronger than CPIH-adjusted measures but still subdued.

-

Public sector regular earnings rose +7.2% YoY (total +7.0%), boosted by timing-related base effects from earlier 2025 pay settlements that will fade soon.

-

Private sector regular earnings grew +3.4% YoY and total pay +3.5% YoY, down from prior periods and the weakest pace since 2020, reflecting ongoing cooling.

-

Nominal wage growth has slowed over the past year, with 4.2% the lowest since late 2021–early 2022 for regular pay and mid-2024 for total pay.

-

Sector dispersion remained, with wholesaling/retailing/hotels/restaurants strongest at +5.1% YoY while finance & business services lagged at +2.0% YoY.

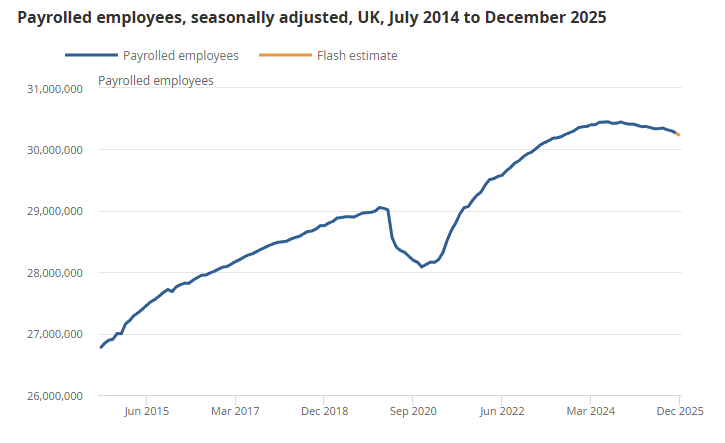

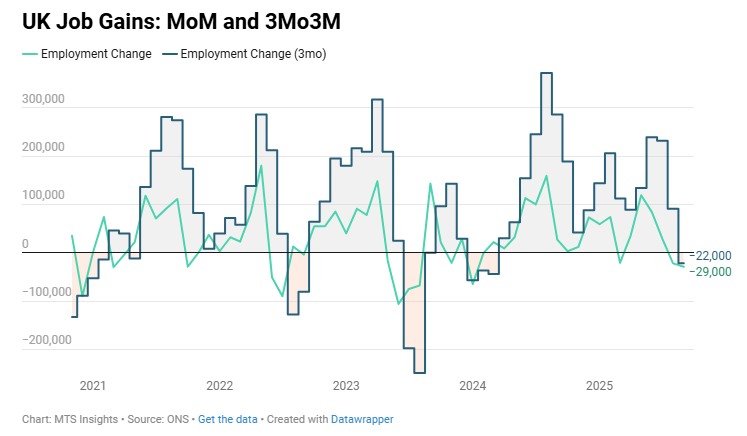

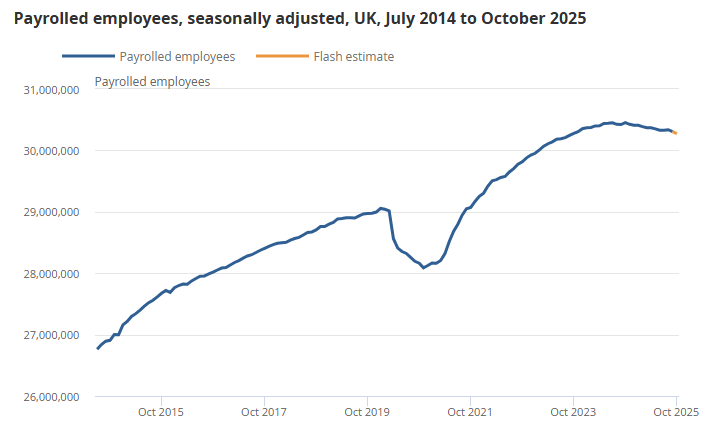

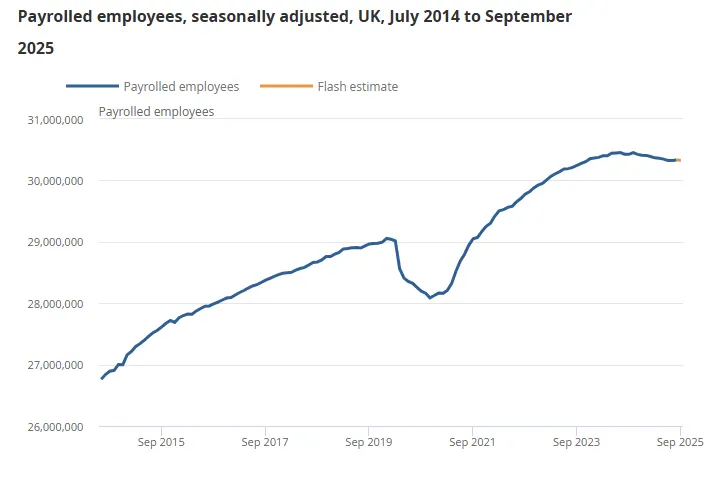

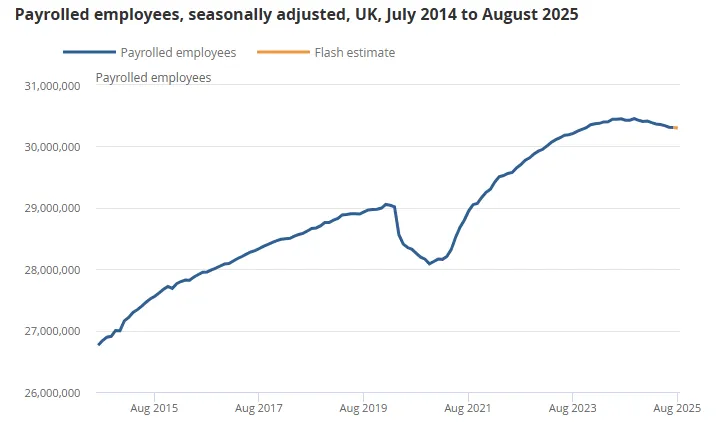

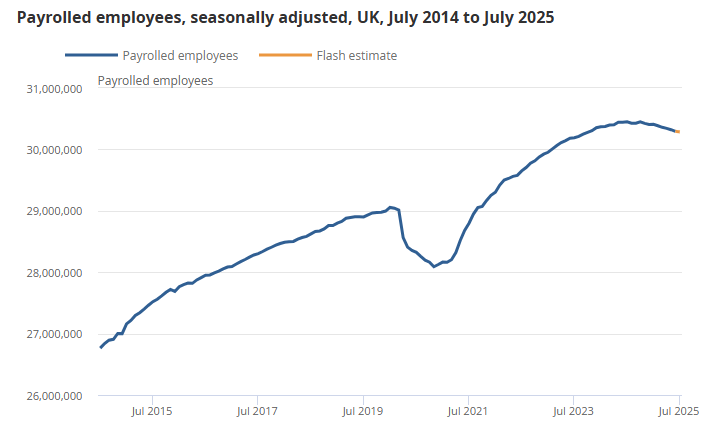

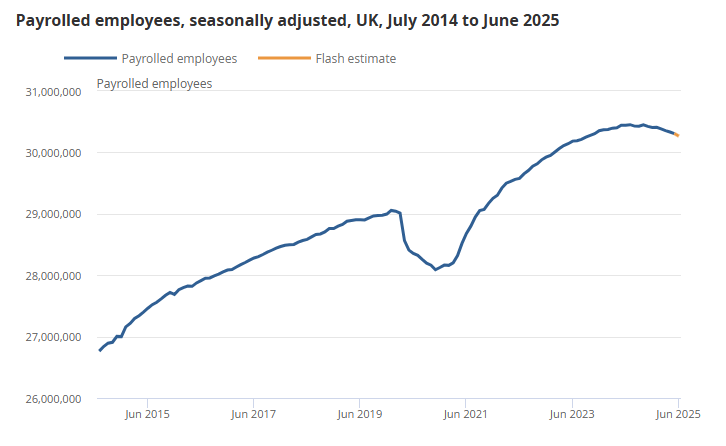

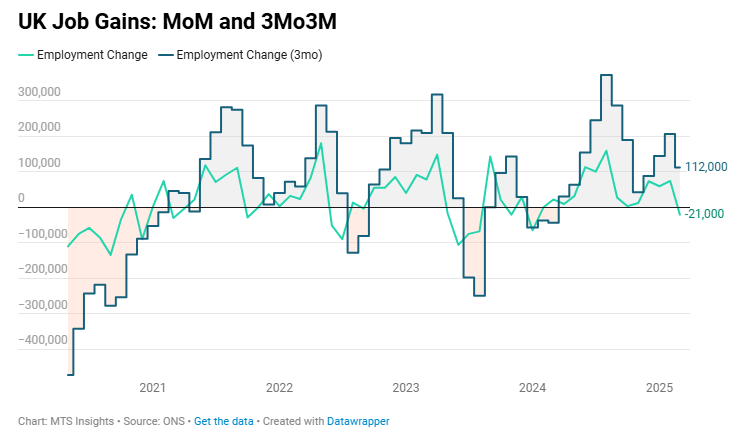

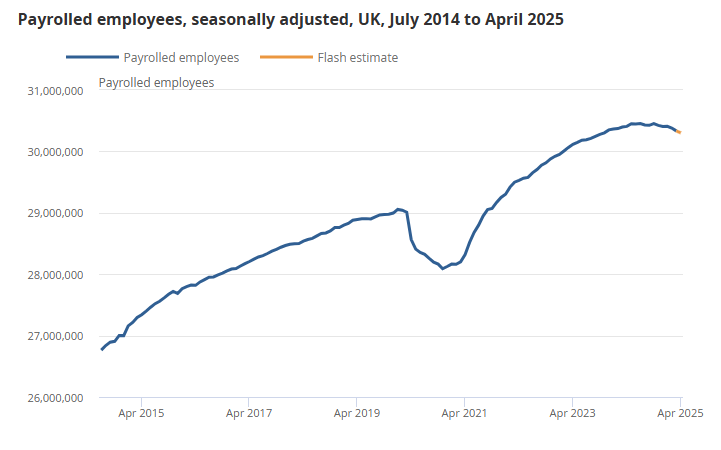

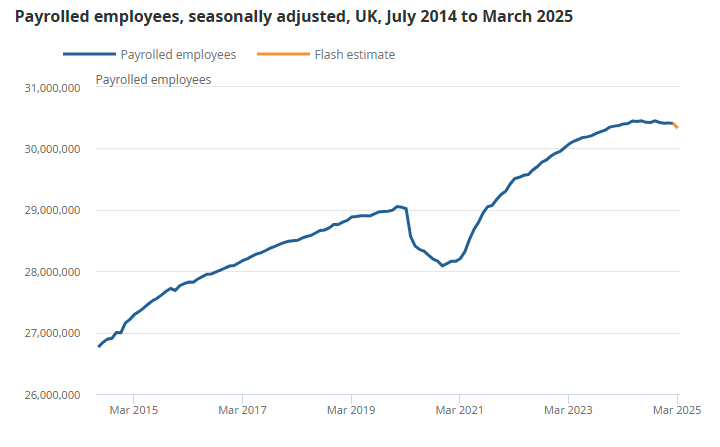

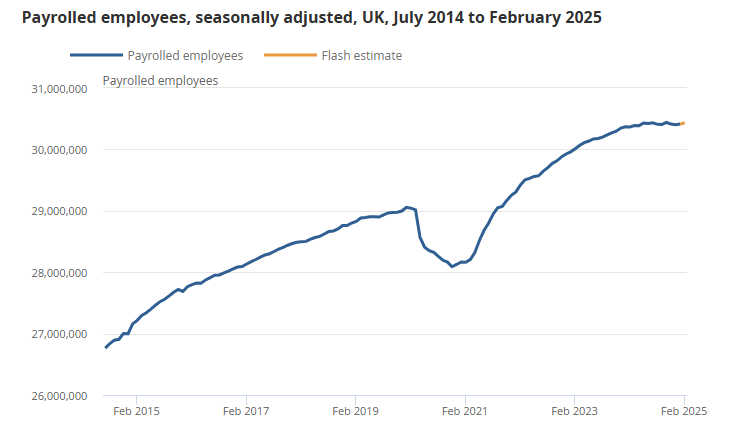

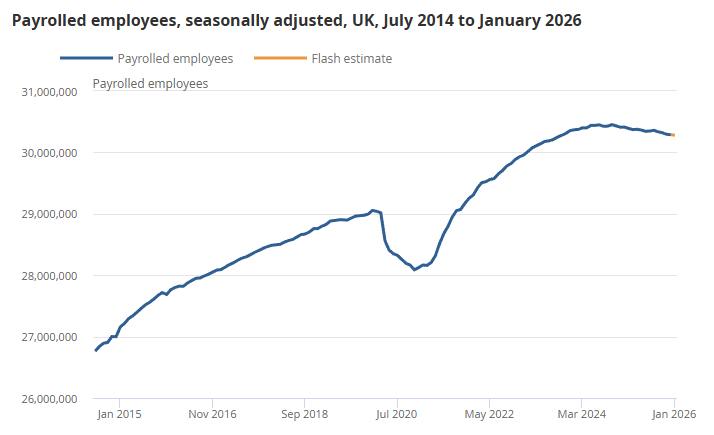

UK payrolled employment was broadly flat MoM and -0.4% YoY in January 2026, continuing negative employee growth trend.

-

Total payrolled employees were 30.3M (-11k MoM; -134k YoY), with January figures provisional and subject to revision as more RTI submissions arrive.

-

December 2025 employment was revised from -43k MoM to -6k MoM, showing typical upward revisions as additional PAYE data are incorporated.

-

Health and social work added +39k employees YoY while wholesale and retail lost -65k, indicating uneven sectoral labor demand.

-

Annual employee growth has been declining steadily since 2022 and is now negative, following earlier post-pandemic recovery strength.

-

Median monthly pay rose +4.6% YoY to £2,588, consistent with pay growth remaining near recent ranges after slowing from earlier peaks.

-

Sector pay growth was highest in wholesale and retail (+6.2% YoY) and lowest in finance and insurance (+2.1%), showing dispersion across industries.

-

Early estimates are based on roughly 85% of available data and typically revised toward 98–99% coverage in later releases.