Texas Service Sector Outlook Survey

Texas Service Sector Outlook Survey

- Source

- Dallas Fed

- Source Link

- https://www.dallasfed.org/

- Frequency

- Monthly

- Next Release(s)

- May 27th, 2026 10:30 AM

-

June 30th, 2026 10:30 AM

-

July 28th, 2026 10:30 AM

-

September 1st, 2026 10:30 AM

-

September 29th, 2026 10:30 AM

-

October 27th, 2026 10:30 AM

-

December 1st, 2026 10:30 AM

-

December 29th, 2026 10:30 AM

Latest Updates

-

Texas Service Sector Outlook Survey: April 2026

-

Texas Service Sector Outlook Survey: March 2026

-

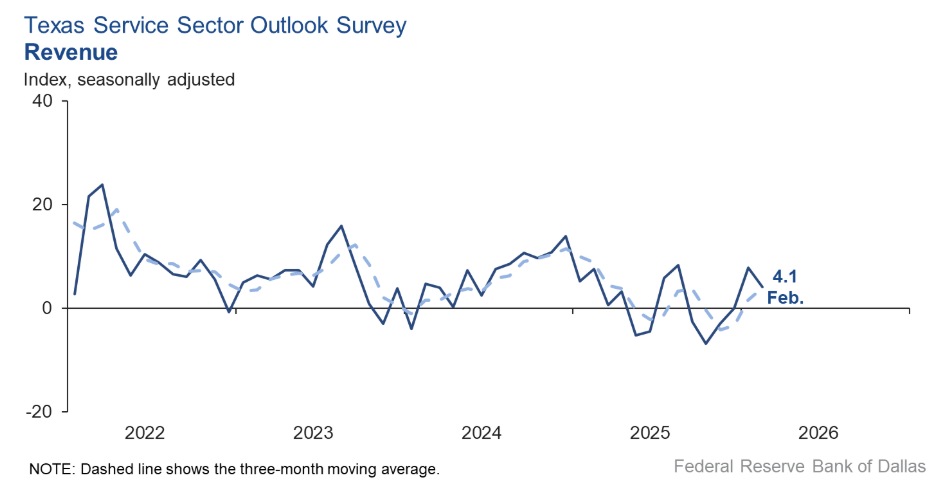

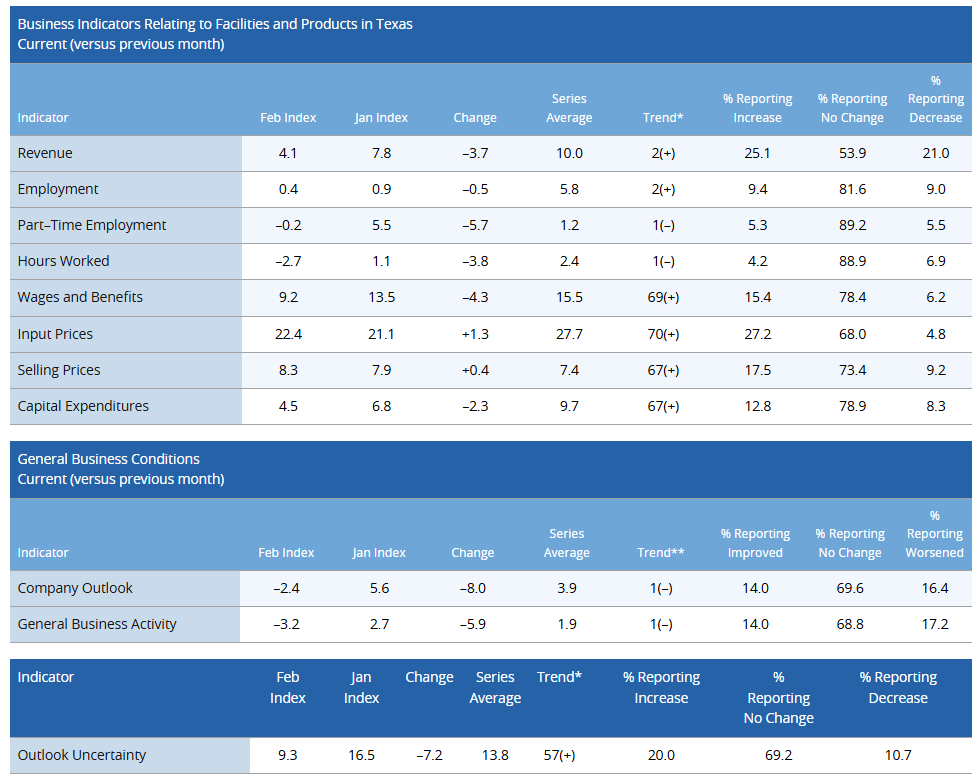

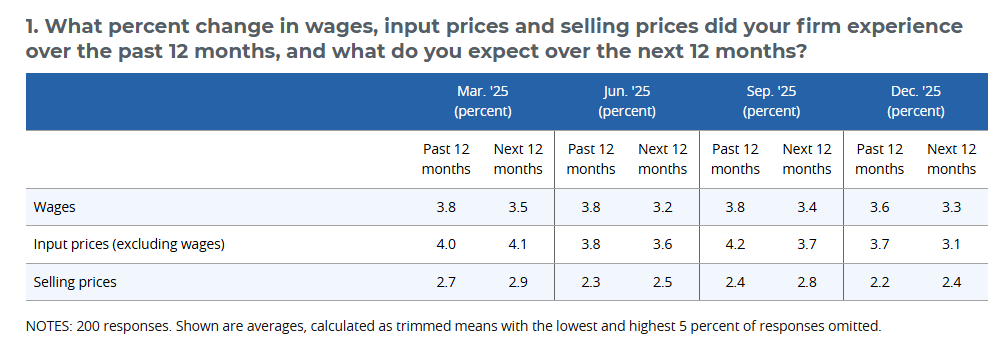

Texas service sector activity remained slightly positive in February, with the revenue index at 4.1, indicating modest expansion despite softer sentiment.

-

The revenue index slipped to 4.1 (Jan: 7.8), showing continued growth but at a slower pace month to month.

-

Employment indicators were near zero, with employment at 0.4 (Jan: 0.9) and part time employment at -0.2 (Jan: 5.5), pointing to little change in hiring conditions.

-

Hours worked fell to -2.7 (Jan: 1.1), indicating a small contraction in labor utilization even as headcounts held steady.

-

General business activity dropped to -3.2 (Jan: 2.7) and company outlook fell to -2.4 (Jan: 5.6), suggesting worsening perceptions of current conditions.

-

Outlook uncertainty declined to 9.3 (Jan: 16.5), its lowest since January 2025, showing reduced uncertainty despite weaker sentiment.

-

Input prices were 22.4 (Jan: 21.1) and selling prices 8.3 (Jan: 7.9), indicating price pressures continued at roughly the same pace as January.

-

The wages and benefits index decreased to 9.2 (Jan: 13.5), pointing to slower labor cost growth.

-

Future activity remained positive, with the future revenue index at 38.3 and future general business activity at 15.0, indicating continued expectations for expansion.

-

-

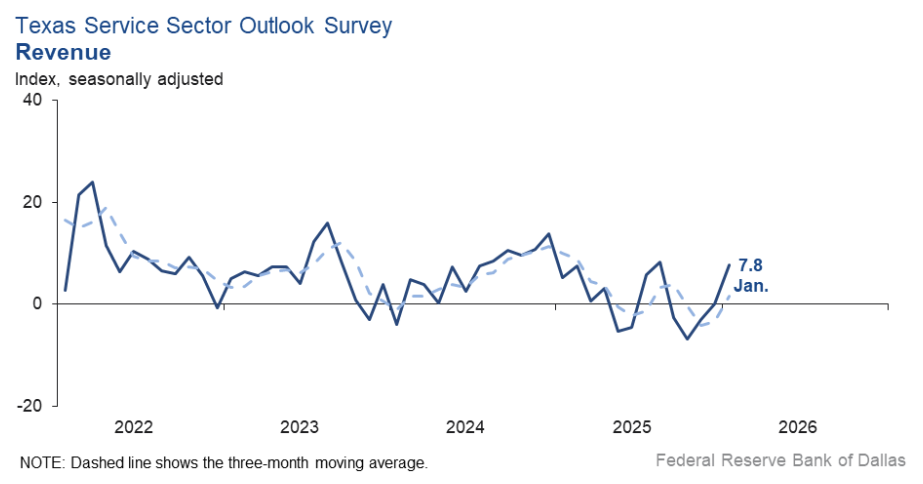

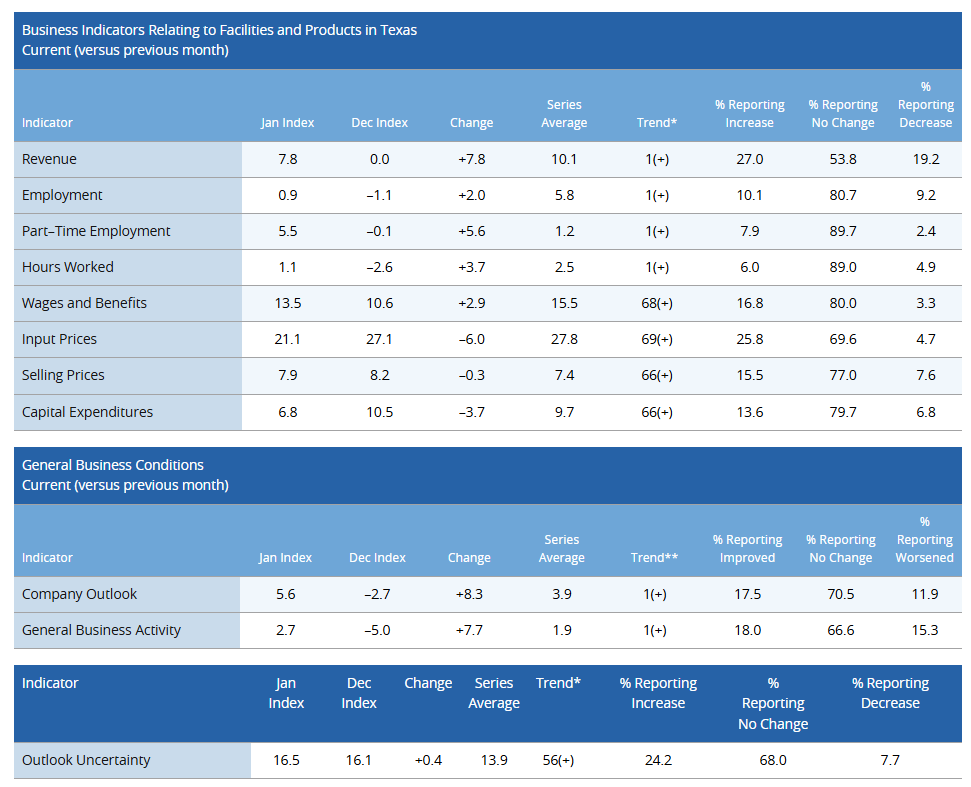

Texas service sector activity improved in January, with the revenue index rising to +7.8 from 0, indicating modest growth after flat conditions in December.

-

Employment edged up to +0.9 (Dec: -1.1) and hours worked rose to +1.1 (Dec: -2.6), both near zero and consistent with broadly stable labor conditions.

-

Part-time employment climbed to +5.5 (Dec: -0.1), reflecting a notable pickup relative to last month.

-

General business activity improved to +2.7 (Dec: -5.0), moving back into positive territory after four months of contraction.

-

Company outlook rose to +5.6 (Dec: -2.7), signaling firmer sentiment toward near-term conditions.

-

Input price pressures eased to 21.1 (Dec: 27.1), while selling prices were little changed at 7.9 (Dec: 8.2), indicating slower cost growth alongside steady output pricing.

-

Wages and benefits increased to 13.5 (Dec: 10.6), pointing to slightly stronger labor cost pressures.

-

Outlook uncertainty held near recent levels at 16.5 (Dec: 16.1), remaining elevated but largely unchanged.

-

-

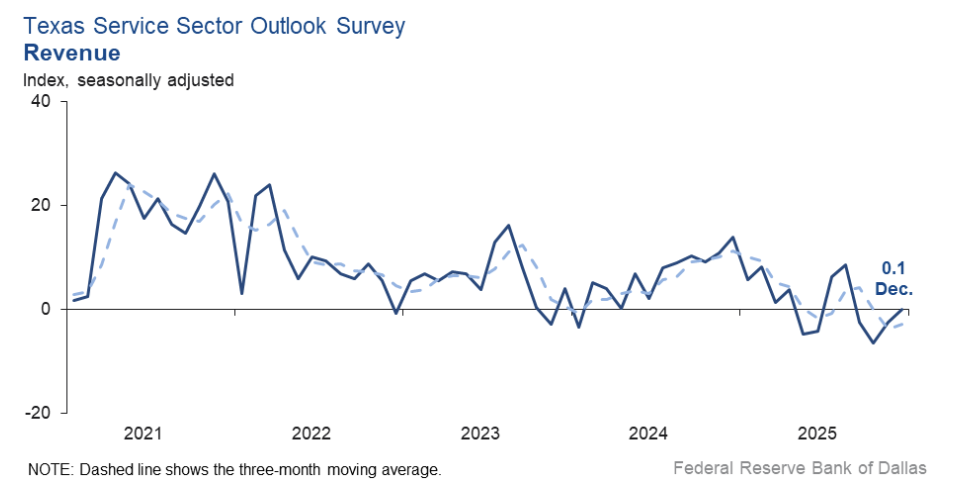

Texas service sector activity was flat in December, with the Revenue Index edging up 2.6 pts to 0.1, signaling unchanged conditions after weakening in November.

-

Labor indicators showed little change in head counts, as both the Employment Index (-0.8) and Part-Time Employment Index (-0.8) hovered near zero, suggesting broadly stable staffing levels.

-

Hours Worked declined further, with the index falling to -2.4, pointing to a modest contraction in workweeks despite steady employment.

-

Broader sentiment weakened slightly, with the General Business Activity Index at -3.3 and the Company Outlook Index at -2.9, keeping overall conditions in negative territory.

-

Outlook Uncertainty eased to 15.9 (from 18.2) but remained above the series average of 13.8, indicating elevated uncertainty despite a modest improvement.

-

Cost pressures were little changed, as the Input Prices Index held near recent levels at 26.2 and the Selling Prices Index came in at 7.9, similar to November.

-

Wage growth slowed, with the Wages and Benefits Index declining to 10.8 from 14.7, indicating softer labor cost pressures late in the year.

-

Forward-looking indicators stayed positive, with the Future Revenue Index at 35.3 and the Future General Business Activity Index at 12.0, suggesting expectations for higher activity in the months ahead.

- Expected input and output price growth in the service sector continued to slow in the latest special question to the lowest growth rates this year.

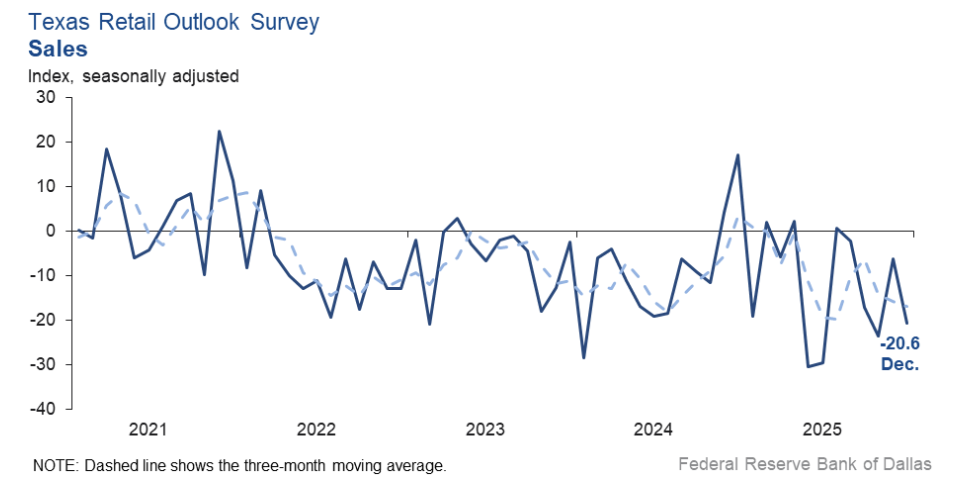

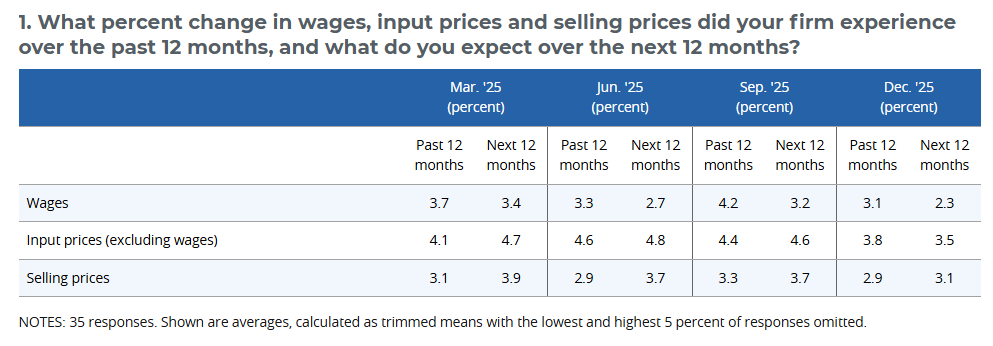

Texas retail sales fell sharply in December, with the Sales Index dropping -14.3 pts to -20.6, reflecting a significant contraction in retail activity.

-

Inventory levels were unchanged, with the Inventories Index at 0.0, indicating neither stock accumulation nor drawdown despite weaker sales.

-

Labor market conditions softened, as the Employment Index fell to -6.2 (-9.7 pts MoM) and the Part-Time Employment Index dropped to 0.0, suggesting reduced hiring momentum.

-

Hours Worked remained weak at -6.3, showing continued contraction in workweeks broadly in line with the prior month.

-

Broader sentiment worsened, with the General Business Activity Index falling to -15.9 and the Company Outlook Index declining to -15.4, both signaling deeper pessimism.

-

Outlook Uncertainty rose sharply to 21.1 (+7.9 pts MoM), moving further above its series average and indicating increased uncertainty among retailers.

-

Price pressures intensified, as the Selling Prices Index jumped to 28.2 (+12.0 pts) and the Input Prices Index climbed to 38.5 (+10.7 pts), while Wages and Benefits increased to 10.5.

-

Despite current weakness, future expectations improved, with the Future Sales Index rising to 18.8 and the Future General Business Activity Index holding near prior levels at 2.2.

- Expected input and output price growth in the retail sector continued to slow in the latest special question to the lowest growth rates this year.

-

-

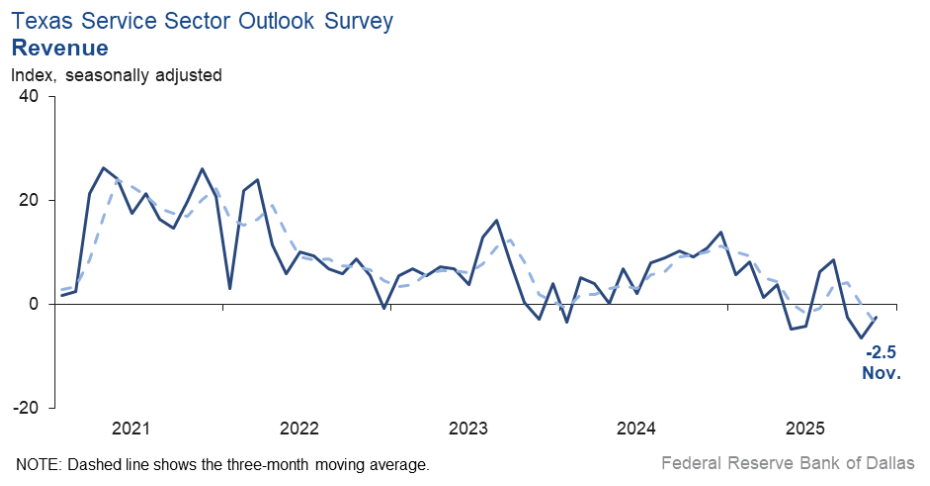

Texas service sector activity contracted slightly in November, with the Revenue Index rising to -2.5 (from -6.4 in October), marking a slower pace of decline and hinting at modest stabilization in activity.

-

Employment improved to 3.1 (from -5.8), reaching its highest level since November 2024 and indicating a return to modest job growth.

-

Hours Worked held nearly flat at -0.7 (from -1.4), showing little change in workweek length, while part-time employment remained steady at 0.2.

-

The General Business Activity Index rose to -2.3 (from -9.4), and Company Outlook improved to -4.2 (from -10.0), signaling reduced pessimism even as conditions remained weak.

-

Input Prices accelerated to 27.6 (from 23.0), and Selling Prices increased to 6.5 (from 4.6), pointing to firmer cost pressures and slightly stronger pricing power.

-

Wages and Benefits climbed to 14.7 (from 10.7), reflecting a pickup in labor cost growth.

-

Outlook Uncertainty decreased to 18.2 (from 22.2) but remained above the long-run average of 13.8, suggesting elevated but easing uncertainty.

-

Future activity indicators stayed positive, with the Future Revenue Index near 34.0 and the Future General Business Activity Index rising to 13.0, indicating continued expectations for growth in the months ahead.

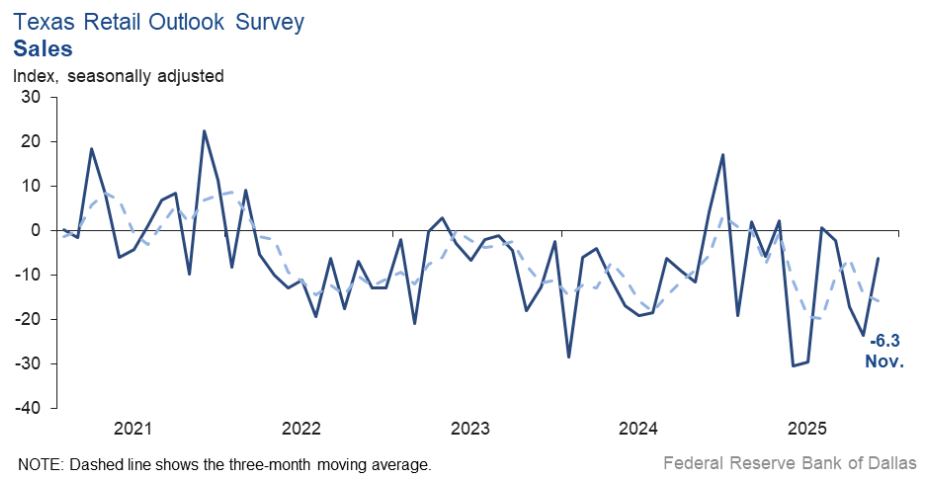

Texas retail activity contracted further in November, with the Sales Index rising to -6.3 from -23.5, marking a smaller decline but still indicating subdued demand across the sector.

-

Retail inventories increased sharply, with the Inventories Index up 7.4 (from 0.1), pointing to a buildup despite weaker sales.

-

Employment strengthened, as the Employment Index rose to 3.5 (from -15.3), and part-time employment improved to 6.8 (from -3.2), both now above their series averages.

-

Hours worked held steady at -7.7 (from -6.8), showing that retailers continued to trim work hours even as hiring picked up.

-

Wage pressures eased notably, with the Wages and Benefits Index falling to 6.1 (from 13.3), compared with little change in selling prices at 16.2.

-

Input prices moderated to 27.8 (from 30.6) but remained above the long-run average, indicating ongoing cost pressures.

-

Broader conditions remained weak; the General Business Activity Index improved to -12.6 (from -23.7), and the Company Outlook Index rose to -12.4 (from -22.3), though both stayed deeply negative.

-

Outlook uncertainty declined to 13.2 (from 17.3) but remained above the series average, reflecting continued caution among retailers.

-

Future retail expectations stayed positive overall, with the Future Sales Index at 6.9 (though down 16 points), and the Future General Business Activity Index steady at 4.1.

-

-

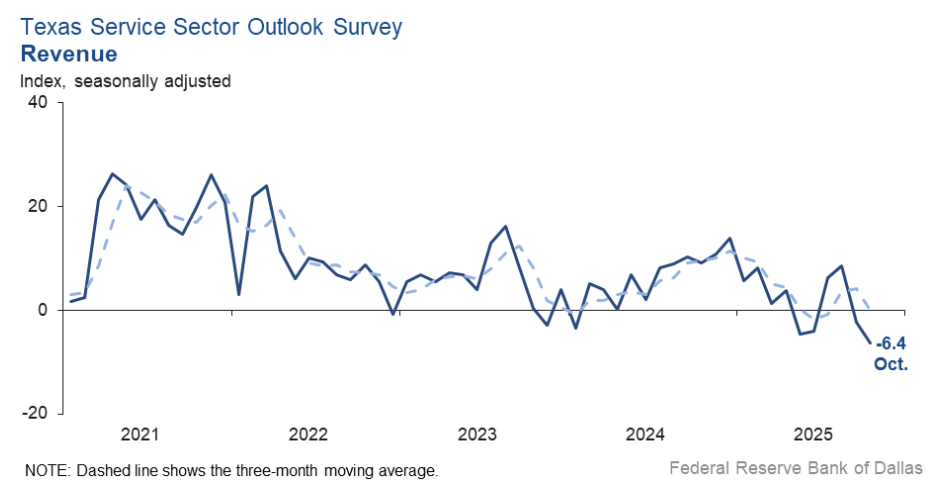

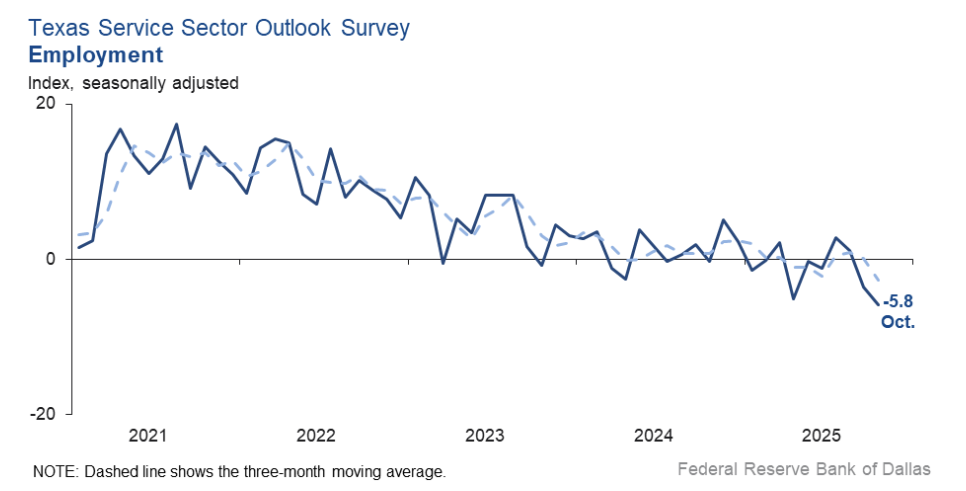

Texas service sector activity weakened further in October 2025, with the Revenue Index falling -4.0 pts to -6.4, marking the lowest reading since July 2020 and signaling continued contraction in business conditions.

-

Employment declined to -5.8 (Sep: -3.6), reflecting further job losses, while part-time employment (-0.1) and hours worked (-1.4) showed little change.

-

Wages and benefits were steady at 10.7 (Sep: 11.9), indicating continued but moderate upward pressure on labor costs.

-

Input prices eased slightly to 23.0 (Sep: 24.4), while selling prices increased to 4.6 (Sep: 1.6), suggesting some improvement in firms’ pricing power.

-

Capital expenditures edged lower to 5.8 (Sep: 7.3), remaining positive but below average levels.

-

General business activity dropped to -9.4 (Sep: -5.6) and company outlook fell sharply to -10.0 (Sep: -2.6), highlighting worsening sentiment.

-

Outlook uncertainty held steady at 22.2, well above the long-term average of 13.8.

-

Despite current weakness, future expectations stayed positive, with the future revenue index at 33.7 and future general business activity at 5.7, though both were below their long-run averages.

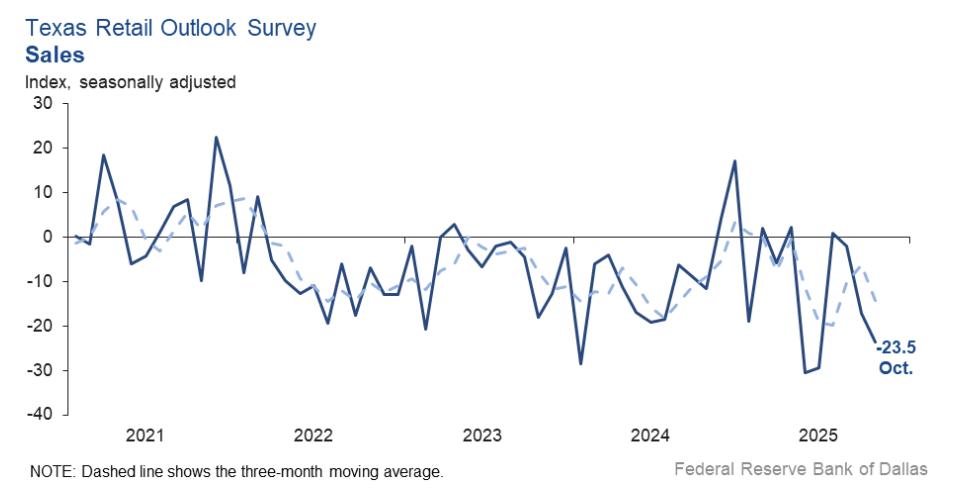

Texas retail activity contracted sharply in October 2025, with the Sales Index falling -6.3 pts to -23.5, marking the weakest reading since mid-2020 and indicating widespread declines in retail demand.

-

Employment fell steeply to -15.3 (from -3.0), while part-time employment was little changed at -3.2, reflecting further deterioration in retail labor conditions.

-

Hours worked remained subdued at -6.8 (from -8.2), indicating continued reductions in workweeks.

-

Wages and benefits edged up slightly to 13.3 (from 12.6), suggesting ongoing cost pressures despite weaker activity.

-

Input prices surged to 30.6 (from 22.0), and selling prices rose to 15.4 (from 9.2), signaling a pickup in inflationary pressures for retailers.

-

Capital expenditures increased to 15.7 (from 13.7), pointing to modest investment momentum despite weak sales.

-

General business activity deteriorated to -23.7 (from -14.7), and company outlook fell sharply to -22.3 (from -5.4), underscoring heightened pessimism across the sector.

-

Outlook uncertainty eased to 17.3 (from 26.3) but remained above the series average, indicating persistent caution among retailers.

-

-

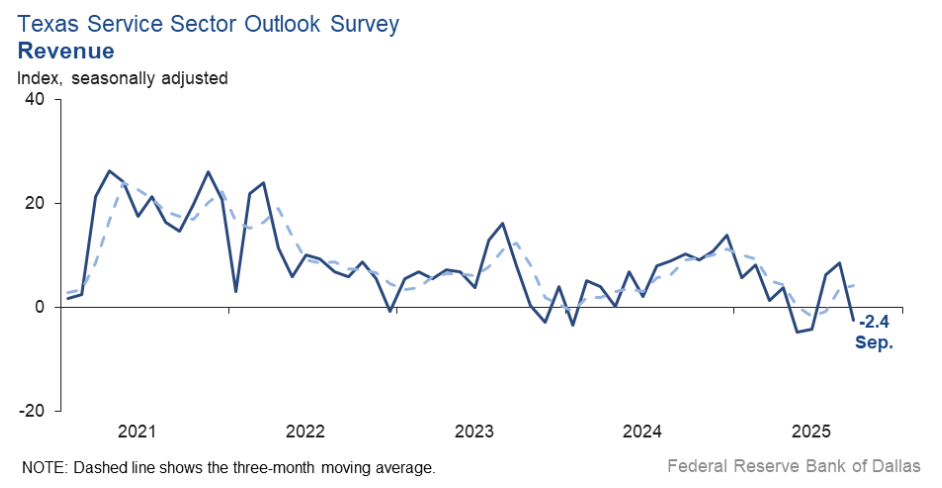

The Texas Service Sector Revenue Index fell -11.0 pts to -2.4 in September 2025, marking a shift back into contraction as broader activity and outlook measures weakened.

-

Employment declined to -3.6 (from 1.2), pointing to job losses, while part-time employment improved modestly to -0.6 (from -2.7).

-

Hours worked slipped -6.1 pts to -1.0, signaling little change in workweeks overall.

-

General business activity dropped -12.4 pts to -5.6, and the company outlook index fell -6.9 pts to -2.6, both reflecting weaker sentiment.

-

Outlook uncertainty rose sharply to 22.5 (from 11.2), indicating greater concern among firms.

-

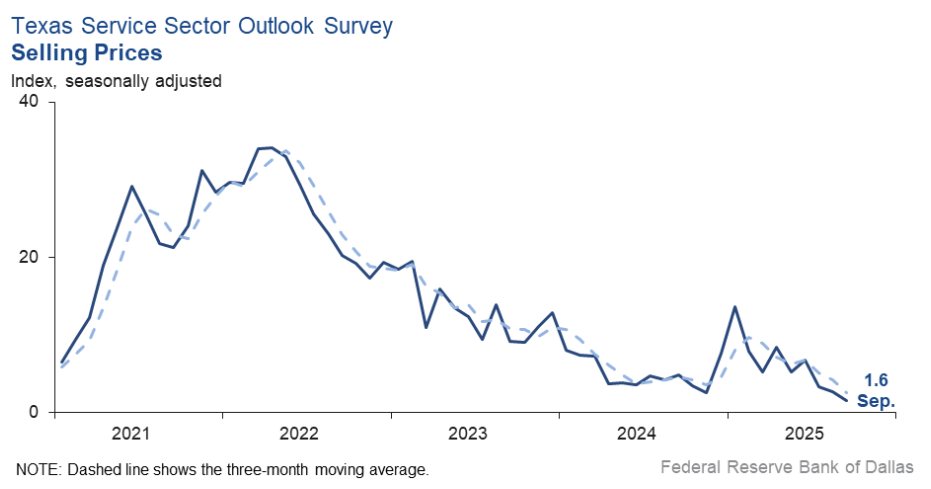

Input prices eased to 24.4 (from 27.9), and wages & benefits moderated to 11.9 (from 15.7), while selling prices held steady at 1.6.

-

Capital expenditures improved slightly to 7.3 (from 5.8), remaining in positive territory.

-

Future expectations stayed more optimistic, with the future revenue index at 35.3 and the future general business activity index at 11.6, suggesting firms anticipate growth in the next six months.

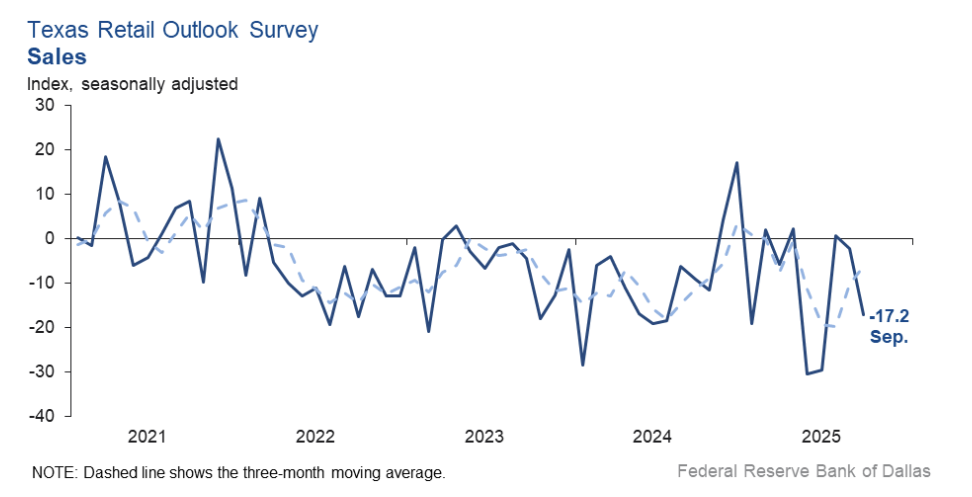

The Texas Retail Sales Index fell -15.1 pts to -17.2 in September 2025, signaling a sharper contraction in statewide retail activity as business sentiment and outlook weakened further.

-

Employment declined to -3.0 (from -2.0), while part-time employment improved to -3.9 (from -15.5), and hours worked slipped further to -8.2 (from -3.6), indicating softer labor demand.

-

General business activity dropped -16.6 pts to -14.7, and the company outlook index fell -6.1 pts to -5.4, both reflecting deteriorating sentiment.

-

Outlook uncertainty rose sharply to 26.6 (from 8.2), highlighting elevated concern among retailers.

-

Input prices were stable at 22.0, while selling prices increased to 9.2 (from 4.1), and wages & benefits held steady at 12.6, pointing to steady but persistent cost pressures.

-

Capital expenditures rose to 13.7 (from -0.1), signaling firmer investment activity despite weaker sales.

-

Companywide sales remained weak at -8.2, though companywide internet sales improved to -1.9 (from -10.0).

-

Future expectations softened, with the future sales index at 26.6 (down from 29.6), while future general business activity eased to 4.7 (from 13.8), suggesting slower but still positive growth ahead.

-

-

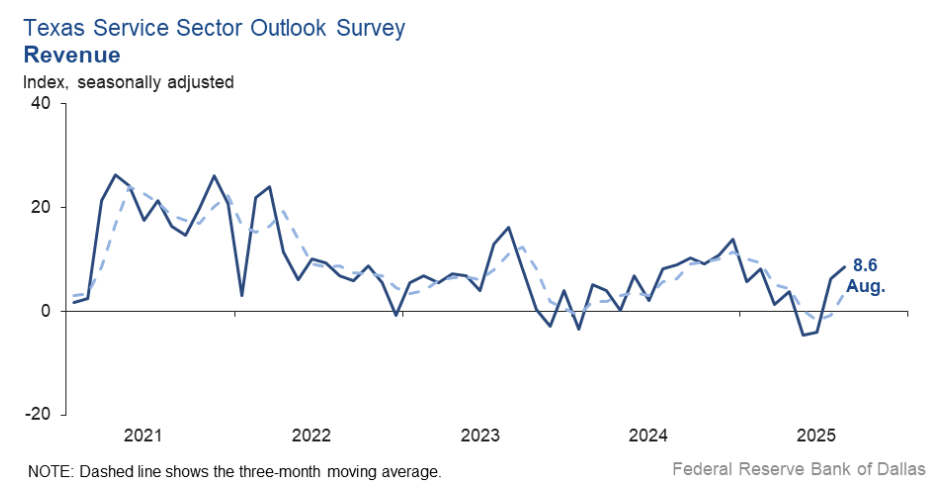

The Texas Service Sector Revenue Index rose 2.3 pts to 8.6 in August, indicating a slightly faster pace of expansion in statewide service activity.

-

Employment eased to 1.2 (from 2.8), signaling little change, while part-time employment improved to -2.7 (from -3.8) and hours worked increased to 5.1 (from 3.2).

-

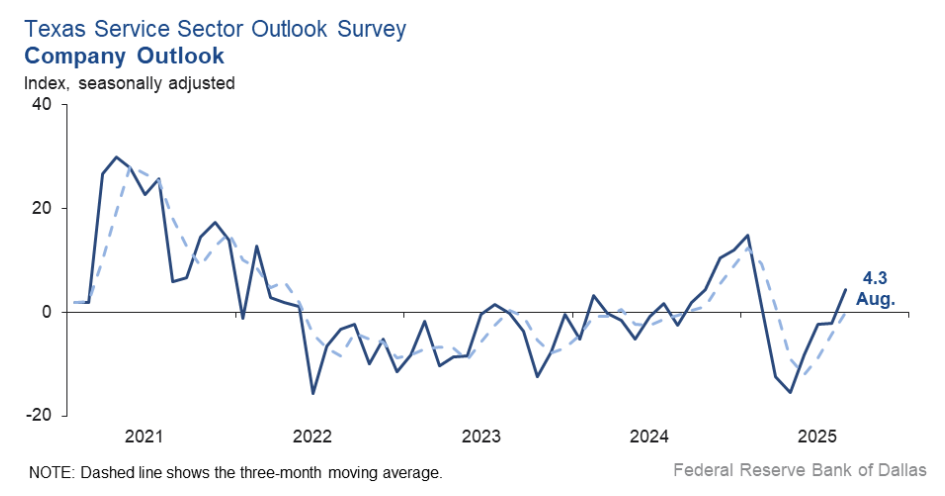

General Business Activity strengthened to 6.8 (from 2.0), and the Company Outlook turned positive at 4.3 (from -2.1), its first positive reading in six months.

-

Outlook Uncertainty declined to 11.2 (from 12.8), suggesting somewhat firmer sentiment.

-

Input Prices rose to 27.9 (from 25.3) and Wages & Benefits increased to 15.7 (from 13.4), while Selling Prices held steady at 2.7 (vs 3.3).

-

Future Revenue expectations improved to 33.8 (from 30.8), with other forward-looking indicators—including employment and capex—remaining in positive territory

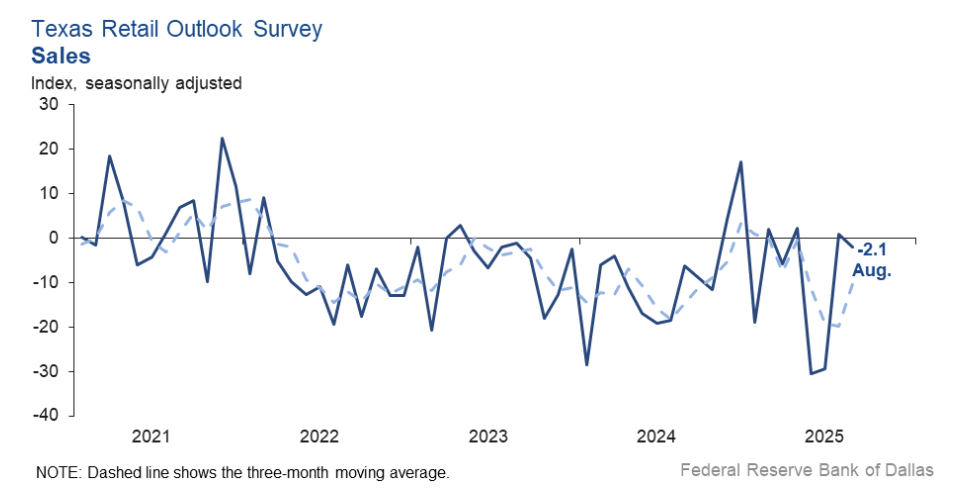

The Texas Retail Sales Index fell 3 pts to -2.1 in August, signaling a renewed contraction in statewide retail activity, while broader business sentiment turned modestly positive.

-

Retail inventories declined for the seventh straight month, with the index at -2.7, indicating persistent stock drawdowns.

-

Employment weakened to -2.0 (from -0.8), part-time employment dropped sharply to -15.5, and hours worked fell to -3.6.

-

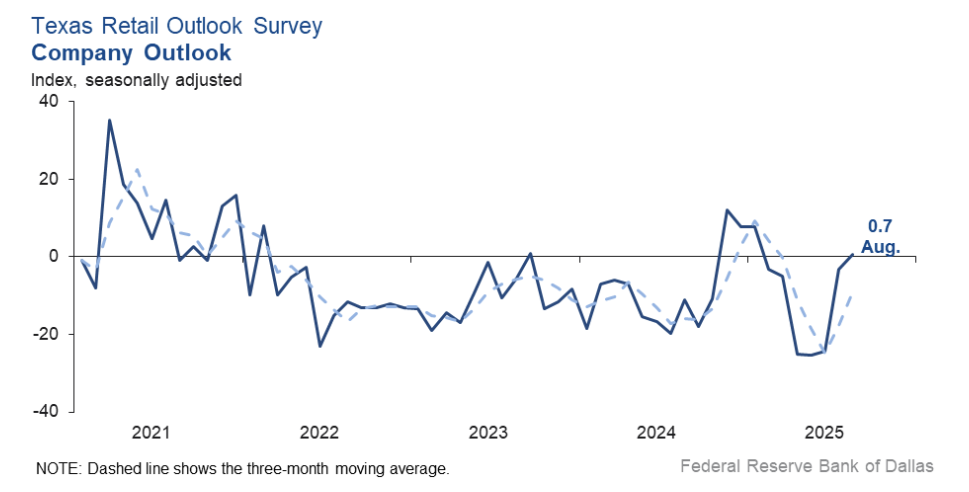

General Business Activity improved to 1.9 (from -4.0), and the Company Outlook stabilized at 0.7, while Outlook Uncertainty eased to 8.2 (from 16.3).

-

Input Prices fell to 22.4 (from 31.6), Selling Prices declined to 4.1 (from 9.0), and Wages & Benefits eased to 11.5 (from 14.4), pointing to softer cost pressures.

-

Future sales expectations held at 29.6, while overall activity and employment outlooks remained positive, suggesting continued moderate growth ahead.

-

-

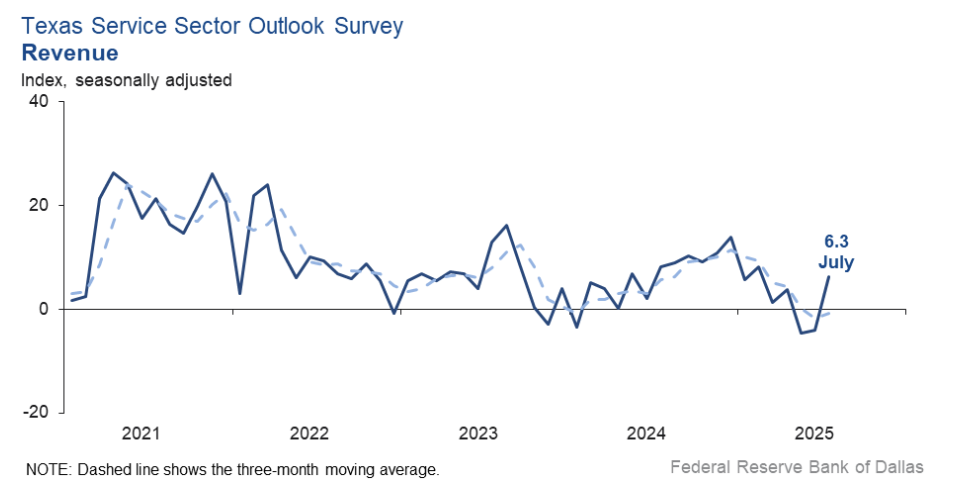

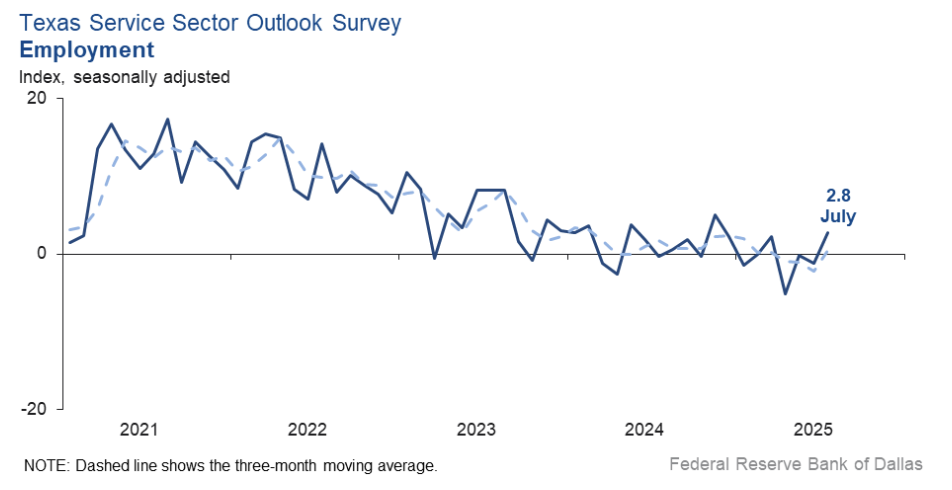

The Texas Service Sector Revenue Index rose 10.4 pts to 6.3 in July, signaling a return to expansion after two months of contraction.

- Employment improved to 2.8 (from -1.2), while hours worked rose to 3.2; part-time employment weakened further to -3.8.

- Input prices climbed to 25.3 (from 21.3) and wages/benefits increased to 13.4 (from 8.6), indicating stronger cost pressures.

- Selling prices fell -3.5 pts to 3.3, suggesting slower price pass-through to customers.

- Capital expenditures rose 4.6 pts to 12.1, above the series average.

- General Business Activity rebounded to 2.0 (from -4.4), while the Company Outlook remained negative at -2.1; Outlook Uncertainty declined sharply to 12.8 (from 19.7).

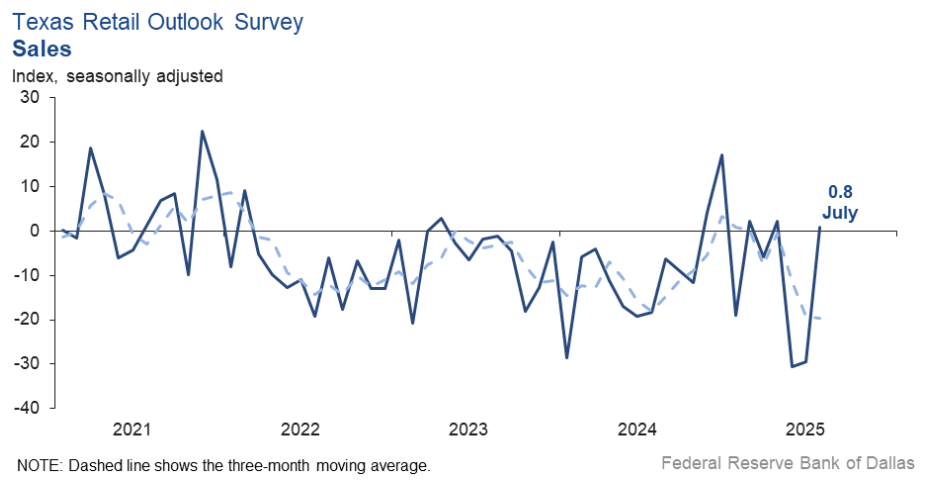

The Texas Retail Sales Index rebounded sharply to 0.8 in July (from -29.5 in June), indicating flat sales after two months of steep declines.

- Employment improved to -0.8 (from -9.0), and hours worked rose to 0.6 (from -14.1), suggesting stable labor conditions.

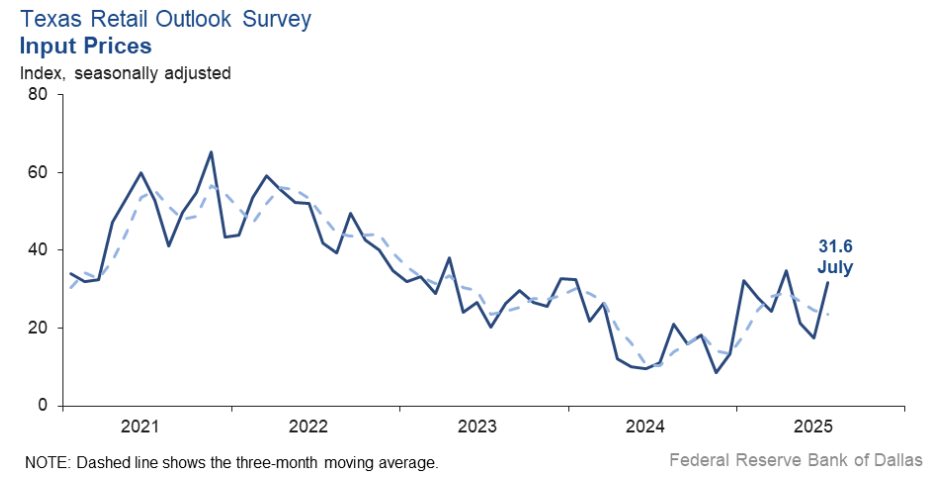

- Input prices surged to 31.6 (from 17.5), and wages and benefits jumped to 14.4 (from -3.3), while selling price pressures eased to 9.0 (from 14.1).

- Inventories remained negative at -2.1, the sixth straight monthly decline.

- Companywide retail activity remained weak with sales at -15.3 and internet sales at -9.0, though both improved from June.

- General Business Activity and Company Outlook rose over 20 pts each to -4.0 and -3.3, respectively, while Outlook Uncertainty fell to 16.3 but stayed above average.

-

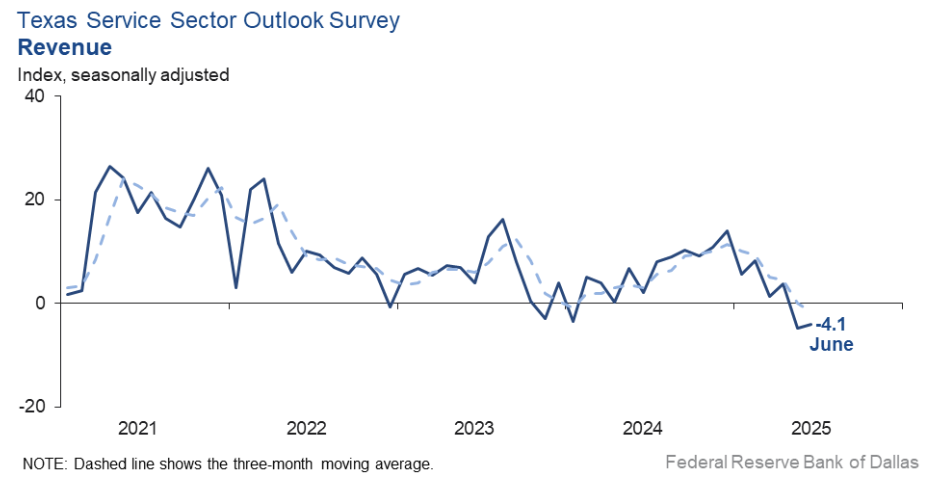

The Texas Service Sector Revenue Index edged up 0.6 pts to -4.1 in June, indicating continued contraction at a similar pace to May.

- Employment slipped -1.0 pts to -1.2, while hours worked held flat at 0.0, signaling stagnant labor conditions.

- Selling prices rose 1.6 pts to 6.8, while input prices increased slightly to 21.3, both remaining below historical averages.

- Capital expenditures jumped 3.1 pts to 7.5, showing modest investment growth.

- Company Outlook improved 5.9 pts to -2.4, and General Business Activity rose 5.7 pts to -4.4, though both remained negative.

- Outlook Uncertainty rose slightly to 19.7, staying elevated above its 13.6 series average.

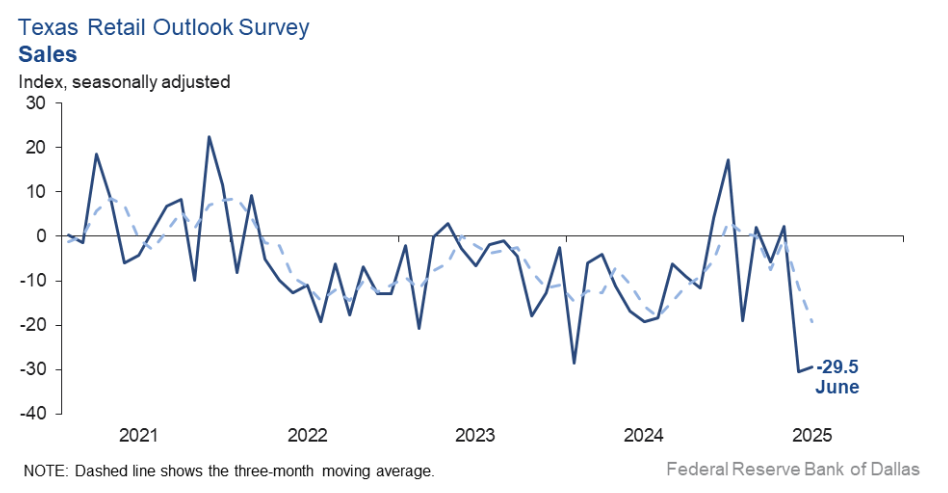

The Texas Retail Sales Index remained weak at -29.5 in June, up slightly from -30.5 in May, signaling continued sharp contraction in activity across the retail sector.

- Employment fell to -9.0 (from -8.1), while Hours Worked plunged -10.3 pts to -14.1, indicating steeper labor market declines.

- Selling Prices jumped 8.9 pts to 14.1, rising above the long-run average, while Input Prices fell -3.8 pts to 17.5.

- Capital Expenditures rebounded 9.2 pts to 6.9, and Inventories rose 7.9 pts to -2.8, though both remained in low territory.

- Companywide Sales improved to -24.0 (from -35.8), and Internet Sales rose to -16.0 (from -25.2), though both remain deeply negative.

- General Business Activity and Company Outlook stayed depressed at -24.4 and -24.2, while Outlook Uncertainty held elevated at 18.8.

-

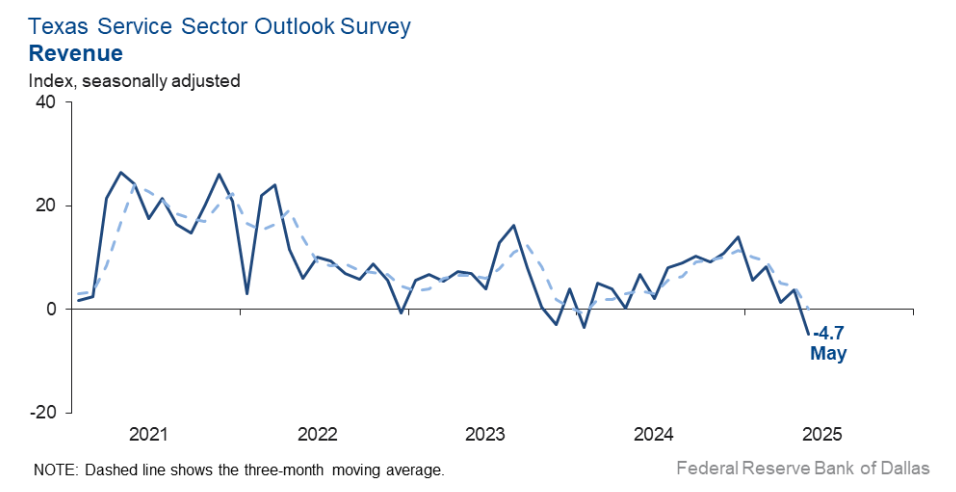

The Texas Service Sector Revenue Index fell -8.5 pts to -4.7 in May, indicating a modest contraction in activity, while General Business Activity improved but remained negative at -10.1 (from -19.4).

- Employment rose to -0.2 (from -5.1), and Part-Time Employment increased to -0.7 (from -3.4), suggesting stabilization in labor markets.

- Input Prices dropped -12 pts to 20.5, and Selling Prices eased -3.2 pts to 5.2; Wages held steady at 9.7.

- Outlook Uncertainty declined sharply to 18.7 (from 40.5).

- Company Outlook improved to -8.3 (from -15.5), and Future Revenue and Business Activity indexes turned neutral to slightly positive.

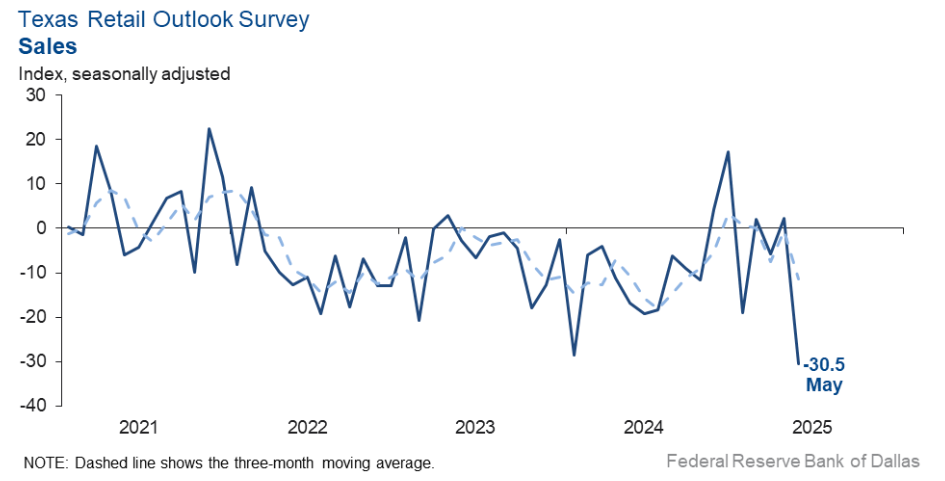

The Texas Retail Sales Index plunged -32.8 pts to -30.5 in May, the weakest since April 2020, as retail conditions deteriorated sharply.

- Retail Employment remained weak at -8.1, while Hours Worked held at -3.8; Wages dropped to -1.1, the lowest since July 2020.

- Input Prices fell -13.6 pts to 21.3 and Selling Prices fell -16.1 pts to 5.2.

- Inventories dropped further to -10.7 (from -2.4), and Companywide Sales collapsed to -35.8.

- General Business Activity declined to -23.7 (from -14.8); Future outlook improved slightly but remains weak (e.g., Future Activity at -1.3, Company Outlook at -3.3).